|

市場調查報告書

商品編碼

2044184

歐洲託管服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

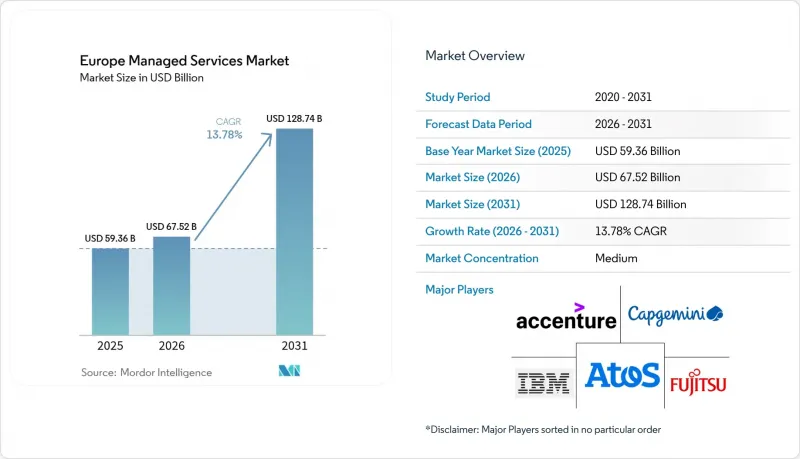

歐洲託管服務市場預計到 2025 年將達到 593.6 億美元,到 2026 年將達到 675.2 億美元,到 2031 年將達到 1287.4 億美元,2026 年至 2031 年的複合年成長率為 13.78%。

隨著企業從資本密集型資料中心資產轉向可預測的營運成本合約(這些合約整合了基礎設施、安全和應用管理),市場需求正在加速成長。混合雲和多重雲端戰略正逐漸成為主流,因為企業可以在滿足歐盟嚴格的資料主權法律要求的同時,平衡延遲、合規性和成本。由於網路威脅激增、《網路資訊安全指令2》(NIS2) 和《數位營運彈性法案》(DORA) 的實施,託管安全服務正成為成長最快的服務領域,而歐盟為支援中小企業數位轉型提供的津貼也在擴大基本客群。同時,位於主權司法管轄區內的邊緣雲端資料中心正在幫助服務提供者支援製造業、金融交易和遠端醫療行業的低延遲工作負載。競爭依然適中,全球系統整合商、電信業者和印度IT服務公司透過與超大規模資料中心業者建立平台無關的合作夥伴關係,競相爭取多年期合約。

歐洲託管服務市場的趨勢和洞察

加速採用混合雲和多重雲端架構

為了平衡效能和合規性要求,歐洲企業正擴大將工作負載分佈在本地資產、私有雲端和多個公共雲端平台之間。普華永道的一項調查顯示,到2025年,68%的企業將至少運作三個雲端平台,但只有22%的企業具備足夠的內部技能來整合身分聯合、網路自動化和災害復原工作流程。託管服務供應商正透過提供Kubernetes控制平面、整合可觀測性和雲端仲介層來進入市場,以確保資料可攜性,而歐盟資料法的防鎖死條款推動了這一趨勢。金融機構正是這一趨勢的典型代表,它們將交易資料保留在本地,同時將分析處理外包給德國電信營運的主權區域。這清楚地表明了亞毫秒級連接和SD-WAN疊加網路為何如今至關重要。由於對延遲的容忍度極高,電信業者正在將專用互連作為捆綁式託管服務的一部分進行貨幣化,並將網路和安全服務等級協定(SLA)整合到單一合約中。

對成本最佳化和可預測營運支出的需求日益成長

過度使用雲端服務正在削弱最初促使企業遷移的成本節約。德勤的報告顯示,到2024年,54%的歐洲財務長的雲端預算超出了20%以上。將FinOps模組整合到託管服務中,無需重構即可實現15-30%的成本節約,其原理是透過持續最佳化計算資源、全面標記成本以提高透明度,以及在非高峰時段關閉非生產工作負載。這些捆綁式服務對沒有專門採購團隊的中小型企業(SME)極具吸引力,可以將原本難以預測的資本支出轉化為穩定的月度費用。公共資金進一步放大了這種效應。歐洲投資銀行已撥款12億歐元(12.8億美元)用於支持中小企業在2025年採用雲端服務。申請津貼的前提是與經過認證的託管服務提供者(MSP)簽訂合約。西班牙、義大利和波蘭的中小企業數位化程度落後於北歐國家,但由於津貼大幅降低了准入門檻,這些國家的數位轉型曲線最為陡峭。

歐盟複雜的資料主權和隱私法規

GDPR、歐盟資料法和醫療設備法規等特定產業框架的並存迫使託管服務提供者 (MSP) 維護獨立的架構,從而加重了合規負擔。德國聯邦資訊安全局 (BSI) 禁止公共部門工作負載流向歐盟總部營運商管理的獨立雲端之外。法國的 SecNumCloud 認證規定更為嚴格,有時需要長達 18 個月才能獲得。這種碎片化現象,以及各成員國採用略有不同的審核標準,正在增加法律成本並延長採購週期。旨在協調認證的自願性 CISPE舉措仍處於試點階段,法規的激增仍在持續減緩託管服務的部署。

細分市場分析

截至2025年,混合環境和託管環境將佔歐洲託管服務市場佔有率的46.32%,而純雲環境預計到2031年將以14.18%的複合年成長率穩步成長。為了滿足GDPR合規性要求,企業將敏感資料集保留在本地,同時利用雲端的突發容量進行分析。電信交換器內的邊緣雲端區域提供亞毫秒延遲和主權認證,使服務供應商能夠在效能和合規性之間取得平衡。託管部署在中型企業中持續成長,這些企業傾向於選擇收費系統。 2025年,法蘭克福和阿姆斯特丹的託管容量顯著成長。儘管歐洲託管服務市場中本地部署支出的比例正在下降,但其絕對值仍保持穩定,因為德國製造商和義大利銀行選擇透過託管基礎設施合約升級硬體,而不是完全遷移到雲端。

Gaia-X聯盟透過認證兼具雲端規模與資料居住保障的互通服務,正在改變市場格局。託管服務提供者(MSP)目前正在整合符合Gaia-X標準的編配層,並在主權區域和超大規模資料中心業者之間遷移工作負載,從而將混合環境確立為長期標準。由於資本支出預算有限,中小企業(SME)正在加速向雲端遷移,但通常採用較為溫和的混合方案,例如在本地運行備份和敏感的人力資源資料。因此,歐洲託管服務市場仍然青睞那些能夠最佳化工作負載在這些混合環境中部署的服務提供者。

預計到2025年,託管安全服務將佔總營收的29.54%,仍將維持成長最快的細分市場,複合年成長率(CAGR)為15.58%。監管期限、勒索軟體風險以及董事會層面的監督迫使企業將全天候監控、事件回應和取證分析納入更廣泛的基礎設施合約中。託管資料中心服務受到交易中心的青睞,這些中心需要低延遲、靠近倫敦、法蘭克福和巴黎交易所的環境。同時,諸如SD-WAN和營運商中立互連等託管網路服務正在整合本地、邊緣和多重雲端環境。遠距辦公熱潮過後,通訊和協作服務的成長趨於平緩,供應商正將重心轉向即時翻譯和用於客服中心的AI。

託管基礎設施和主機服務仍然是基礎服務,但隨著超大規模資料中心業者透過程式碼範本實現伺服器配置自動化,它們正面臨商品化的壓力。因此,服務提供者正透過整合災害復原培訓和預測性容量規劃來凸顯自身優勢。在醫療保健和現場服務等關鍵任務型產業,遠端設備配置和合規性至關重要,而託管行動性服務也正在蓬勃發展。託管安全和網路營運的整合使託管服務提供者 (MSP) 能夠在單一主機上匹配威脅情報和流量異常——監管機構已開始將此功能視為《災難復原法案》(DORA) 下的必備功能。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速採用混合雲和多重雲端架構

- 對成本最佳化和可預測營運支出的需求日益成長

- 日益嚴重的網路安全威脅正在推動託管安全解決方案的普及。

- 歐洲各地企業內部IT人員短缺

- 面向資料主權工作負載的邊緣雲區域資料中心的興起

- MSP 將 AI Ops 和 FinOps 平台商品搭售,以實現自動化成本管治。

- 市場限制因素

- 複雜的歐盟資料主權和隱私法規

- 與舊有系統整合的複雜性

- 能源成本上漲給資料中心服務的利潤率帶來了壓力。

- 加強對外包工作負載的碳計量監管

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 雲

- 混合/主機

- 按服務類型

- 託管資料中心

- 託管安全

- 主機網路

- 管理溝通與協作

- 託管基礎設施和主機

- 行動管理

- 託管雲端和應用程式

- 託管工作場所/服務台

- 按公司規模

- 小型企業

- 大公司

- 按最終用戶行業分類

- BFSI

- 製造業

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 資訊科技和通訊

- 能源與公共產業

- 其他終端用戶產業

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 俄羅斯

- 波蘭

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Fujitsu Limited

- Capgemini SE

- Atos SE

- Accenture plc

- AT&T Inc.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Microsoft Corporation

- Deutsche Telekom AG

- Orange SA(Orange Business Services)

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- NTT Data Corporation

- Tech Mahindra Limited

- DXC Technology Company

- Rackspace Technology, Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- Sopra Steria Group SA

- CGI Inc.

- Kyndryl Holdings, Inc.

- Capita plc

第7章 市場機會與未來展望

The Europe managed services market size is projected to be USD 59.36 billion in 2025, USD 67.52 billion in 2026, and reach USD 128.74 billion by 2031, growing at a CAGR of 13.78% from 2026 to 2031.

Demand is accelerating as organizations migrate from capital-intensive data-center assets to predictable operating-expense agreements that bundle infrastructure, security, and application management. Hybrid and multi-cloud strategies dominate because they let firms balance latency, compliance, and cost while still meeting strict EU data-sovereignty laws. Escalating cyber-threat volumes, the NIS2 Directive, and the Digital Operational Resilience Act are turning managed security into the fastest-growing service line, while EU grants for SME digitalization are widening the customer base. At the same time, edge-cloud data-centers positioned inside sovereign jurisdictions are helping providers support low-latency workloads for manufacturing, financial trading, and telemedicine. Competitive intensity remains moderate; global systems integrators, telecom carriers, and Indian IT services companies are racing to lock in multi-year contracts, often through platform-agnostic alliances with hyperscalers.

Europe Managed Services Market Trends and Insights

Accelerated Adoption of Hybrid and Multi-Cloud Architectures

European enterprises are increasingly distributing workloads across on-premises assets, private clouds, and several public-cloud platforms to align performance with compliance mandates. A PwC survey showed that 68% managed at least three clouds in 2025, but only 22% had enough in-house skills to integrate identity federation, network automation, and disaster-recovery workflows. Managed service providers are stepping in with Kubernetes control planes, unified observability, and cloud brokerage layers that keep data portable, an outcome reinforced by the EU Data Act's anti-lock-in clauses. Financial institutions exemplify the trend by keeping transaction data on-premises while pushing analytics to sovereign zones run by Deutsche Telekom, illustrating why sub-10 ms connectivity and SD-WAN overlays are now must-have features. Because latency budgets are tight, telecom carriers monetize dedicated interconnects as part of bundled managed services, blending network and security SLAs in a single contract.

Rising Demand for Cost Optimization and Predictable OPEX

Cloud overspending is eroding the savings that initially justified migration; Deloitte reported that 54% of European CFOs blew past their 2024 cloud budgets by more than 20%. FinOps modules embedded within managed services continuously right-size compute, enforce tagging for cost show-back, and park non-production workloads during off-peak hours, delivering 15-30% savings without refactoring. Bundled offerings appeal to SMEs that lack procurement teams, essentially converting unpredictable capital outlays into steady monthly fees. Public money amplifies the effect. The European Investment Bank issued EUR 1.2 billion (USD 1.28 billion) in 2025 to subsidize SME cloud uptake, with certified MSP engagement mandated for grant eligibility. Spain, Italy, and Poland, where SME digitization lags Northern Europe, are showing the steepest adoption curves because subsidies sharply lower entry barriers.

Complex EU Data-Sovereignty and Privacy Regulations

The coexistence of GDPR, the EU Data Act, and sector-specific frameworks such as the Medical Device Regulation forces MSPs to maintain separate infrastructure stacks, raising compliance overhead. Germany's BSI bars public-sector workloads from traveling outside sovereign clouds controlled by EU-headquartered operators. France's SecNumCloud certificate adds even stricter controls and can take 18 months to earn. Fragmentation inflates legal costs and stretches procurement cycles because each member state enforces slightly different audit standards. A voluntary CISPE initiative to harmonize certifications is still in pilot, so managed-services rollouts remain slowed by regulatory sprawl.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Cybersecurity Threats Driving Managed Security Uptake

- Shortage of In-House IT Talent Across Europe

- Integration Complexity with Legacy Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid and hosted environments captured 46.32% of Europe managed services market share in 2025, while cloud-only setups are recording a brisk 14.18% CAGR to 2031. Enterprises keep sensitive datasets on-premises to meet GDPR while exploiting cloud burst capacity for analytics. Edge-cloud zones inside telecom exchanges offer sub-5 ms latency and sovereign certifications, letting providers strike a balance between performance and compliance. Hosted deployments keep growing among mid-sized firms that prefer predictable fees without multitenancy risk, particularly in Frankfurt and Amsterdam where colocation capacity expanded in 2025. Although on-premises spending is declining as a share of the Europe managed services market size, absolute dollars remain steady because German manufacturers and Italian banks refresh hardware through managed-infrastructure contracts instead of full cloud migrations.

The Gaia-X federation is reshaping the landscape by certifying interoperable services that combine cloud scale with data-residency guarantees. MSPs now embed Gaia-X-compliant orchestration layers to move workloads among sovereign zones and hyperscaler regions, reinforcing hybrid as the long-term norm. SMEs accelerate straight to cloud because they lack capex budgets, but even they often adopt a light hybrid stance by running backups or sensitive HR data locally. Consequently, the Europe managed services market continues to favor providers that can optimize workload placement across this hybrid continuum.

Managed security held 29.54% revenue share in 2025 and is projected to remain the fastest-growing line at 15.58% CAGR. Regulatory deadlines, ransomware risk, and board-level scrutiny push enterprises to embed 24X7 monitoring, incident response, and forensic analysis within wider infrastructure contracts. Managed data-center services appeal to trading hubs that need low-latency proximity to exchanges in London, Frankfurt, and Paris, while managed network services such as SD-WAN and carrier-neutral interconnects weave together on-premises, edge, and multi-cloud domains. Communications and collaboration services have plateaued after the remote-work boom, causing vendors to shift focus toward real-time translation and contact-center AI.

Managed infrastructure and hosting remain baseline offerings but face commoditization as hyperscalers automate server provisioning through code templates. Consequently, providers differentiate by layering disaster-recovery drills and predictive capacity planning. Managed mobility is growing in healthcare and field services, where remote device provisioning and compliance enforcement are mission-critical. The convergence of managed security and network operations lets MSPs map threat intelligence to traffic anomalies in a single console, a feature regulators are starting to deem essential under DORA.

The Europe Managed Services Market Report is Segmented by Deployment Model (On-Premises, Cloud, and Hybrid/Hosted), Service Type (Managed Data Centre, Managed Security, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Vertical (BFSI, Manufacturing, and More), and Country (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- IBM Corporation

- Fujitsu Limited

- Capgemini SE

- Atos SE

- Accenture plc

- AT&T Inc.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Microsoft Corporation

- Deutsche Telekom AG

- Orange S.A. (Orange Business Services)

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- NTT Data Corporation

- Tech Mahindra Limited

- DXC Technology Company

- Rackspace Technology, Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- Sopra Steria Group SA

- CGI Inc.

- Kyndryl Holdings, Inc.

- Capita plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of Hybrid and Multi-Cloud Architectures

- 4.2.2 Rising Demand for Cost Optimization and Predictable OPEX

- 4.2.3 Increasing Cybersecurity Threats Driving Managed Security Uptake

- 4.2.4 Shortage of In-House IT Talent Across Europe

- 4.2.5 Emergence of Edge-Cloud Zonal Datacentres for Data-Sovereign Workloads

- 4.2.6 MSP Bundling of AI Ops and FinOps Platforms to Automate Cost Governance

- 4.3 Market Restraints

- 4.3.1 Complex EU Data-Sovereignty and Privacy Regulations

- 4.3.2 Integration Complexity with Legacy Systems

- 4.3.3 Rising Energy Costs Squeezing Data-Centre Service Margins

- 4.3.4 Escalating Carbon-Accounting Scrutiny on Outsourced Workloads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid/Hosted

- 5.2 By Service Type

- 5.2.1 Managed Data Centre

- 5.2.2 Managed Security

- 5.2.3 Managed Network

- 5.2.4 Managed Communication and Collaboration

- 5.2.5 Managed Infrastructure and Hosting

- 5.2.6 Managed Mobility

- 5.2.7 Managed Cloud and Application

- 5.2.8 Managed Workplace / Service Desk

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Government and Public Sector

- 5.4.6 IT and Telecom

- 5.4.7 Energy and Utilities

- 5.4.8 Rest of End-User Verticals

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Sweden

- 5.5.8 Russia

- 5.5.9 Poland

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Fujitsu Limited

- 6.4.3 Capgemini SE

- 6.4.4 Atos SE

- 6.4.5 Accenture plc

- 6.4.6 AT&T Inc.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Microsoft Corporation

- 6.4.10 Deutsche Telekom AG

- 6.4.11 Orange S.A. (Orange Business Services)

- 6.4.12 Tata Consultancy Services Limited

- 6.4.13 Wipro Limited

- 6.4.14 Cognizant Technology Solutions Corporation

- 6.4.15 Nokia Corporation

- 6.4.16 Telefonaktiebolaget LM Ericsson

- 6.4.17 NTT Data Corporation

- 6.4.18 Tech Mahindra Limited

- 6.4.19 DXC Technology Company

- 6.4.20 Rackspace Technology, Inc.

- 6.4.21 Verizon Communications Inc.

- 6.4.22 Vodafone Group Plc

- 6.4.23 Sopra Steria Group SA

- 6.4.24 CGI Inc.

- 6.4.25 Kyndryl Holdings, Inc.

- 6.4.26 Capita plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球託管通訊服務市場報告2026年全球氣尖管理服務市場報告2026年全球託管Hazelcast服務市場報告

2026年全球託管通訊服務市場報告2026年全球氣尖管理服務市場報告2026年全球託管Hazelcast服務市場報告 託管服務市場報告:按類型、部署模式、企業規模、最終用途和地區分類(2026-2034 年)

託管服務市場報告:按類型、部署模式、企業規模、最終用途和地區分類(2026-2034 年) 託管服務市場:2026-2032年全球市場預測(按服務類型、合約類型、組織規模、最終用戶和部署模式分類)2026年全球託管服務市場報告

託管服務市場:2026-2032年全球市場預測(按服務類型、合約類型、組織規模、最終用戶和部署模式分類)2026年全球託管服務市場報告 全球託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球託管Memcached服務市場報告2026年全球託管服務供應商市場報告2026年全球託管資訊服務市場報告

全球託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球託管Memcached服務市場報告2026年全球託管服務供應商市場報告2026年全球託管資訊服務市場報告