|

市場調查報告書

商品編碼

2044183

主機板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Motherboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

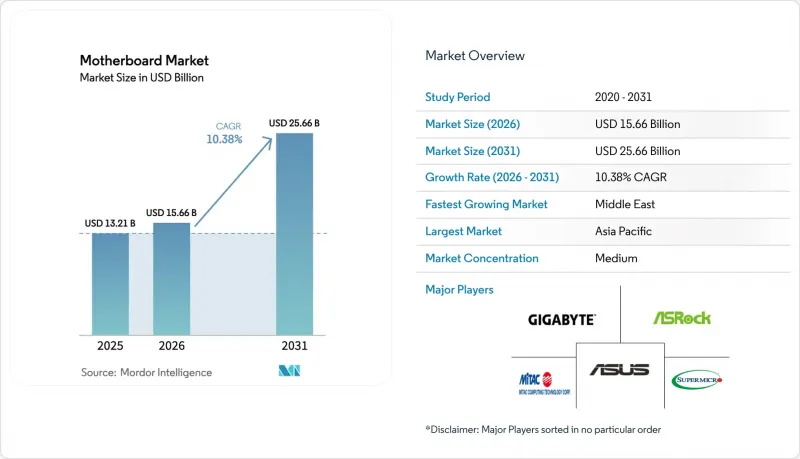

預計主機板市場將從 2025 年的 132.1 億美元和 2026 年的 156.6 億美元成長到 2031 年的 256.6 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 10.38%。

人工智慧伺服器的日益普及推高了高階伺服器主機板的平均售價。同時,消費市場DDR5記憶體價格波動。向AMD AM5和Intel LGA-1851插槽的過渡縮短了升級週期,而工業用戶則轉向能夠承受嚴苛環境的堅固耐用型設計。亞太地區憑藉著台灣的ODM叢集和中國的契約製造基地,仍然是主機板的主要銷售基地,但隨著中東地區對數位基礎設施投資的加速,該地區正崛起為成長最快的市場。元件關稅、多層PCB工程師短缺以及二手基板取得困難等因素抑制了短期需求,但這些因素並未阻礙主機板市場的長期成長。

全球主機板市場趨勢與洞察

人工智慧資料中心對伺服器主機板的需求

2024年,超大規模營運商的AI基礎設施年增61%。 Supermicro的X14主機板每個節點最多支援12個GPU,展示了高密度拓撲結構如何增加基板的複雜性和獲利能力。多層堆疊、冗餘VRM和帶外管理為物料清單(BOM)創造了消費級SKU無法實現的附加價值。台灣ODM廠商憑藉其與基板供應商的地理接近性,在2024年供應了全球超過60%的伺服器主機板出貨量。採用符合PCI-SIG CEM 5.0規範的PCIe 5.0插槽提高了平均售價(ASP),同時也增加了訊號完整性的挑戰。隨著主要雲端服務供應商計劃在2027年前投資數十億美元用於GPU叢集,伺服器主機板仍然是重要的成長引擎。

AM5 和 LGA-1851 平台的快速更新週期

英特爾的Z890和B860晶片組將於2024年底隨Arrow Lake處理器一同推出,它們不再支援DDR4內存,並將Wi-Fi 7和Thunderbolt 4作為標配功能,加速了管道庫存的更新換代。同時,AMD的AM5插槽承諾晶片組相容性將持續到2027年,這使得主機板製造商能夠提供從入門級B650到旗艦級X870E的廣泛產品線,同時最大限度地減少插槽的重新設計。華擎的B850系列將於2025年1月在中端價位區間上市,雖然沒有超頻功能,但提供了PCIe 5.0 M.2介面。這種縮短的開發週期有利於能夠快速切換生產系統的敏捷型ODM廠商,但投資回報期的縮短也給小規模企業的利潤率帶來了壓力。消費者覺得產品壽命正在縮短,升級頻率也朝著類似訂閱的模式轉變。

由於每一代產品價格上漲,終端用戶猶豫不決。

2025年初,一套中階LGA-1851系統需要200美元的主機板、150美元的32GB DDR5-6000記憶體和120美元的PCIe 5.0固態硬碟,不包括CPU和GPU,總成本為470美元。相比之下,2024年同等配置的電腦只需320美元。在亞太地區,39%的PC出貨量為翻新機,凸顯了消費者對價格的敏感度。南美地區的買家還面臨額外的進口關稅,巴西的工業產品稅(IPI)將使組件成本增加10-15%。這種不斷擴大的價格差距正在推遲消費者的購買意願,延長更換週期,並減少短期出貨量。廠商正在透過推出功能有限的晶片組SKU、內存套裝和分期付款選項來應對,但在低收入地區,價格彈性仍然有限。

細分市場分析

預計到2025年,ATX主機板的銷量將佔總銷量的45.28%,憑藉其強大的擴充槽佈局和充足的VRM餘量,佔據主機板市場最大的佔有率。同時,隨著發燒友追求節省空間的遊戲PC,以及系統整合商在有限的機殼內部署邊緣AI設備,Mini-ITX主機板預計將以10.41%的複合年成長率加速成長至2031年。除了假期季節尖峰時段外,ATX主機板預計將保持穩定的更新周期,以滿足企業客戶的需求;而Mini-ITX主機板需求的激增則與展會上展示的高密度PCIe 5.0儲存功能的新產品發布密切相關。

PCIe 5.0通道和16相VRM的引入,縮小了Mini-ITX主機板與其他規格主機板之間的性能差距。華擎的「Taichi OCF Mini-ITX」和技嘉的「X870E Aorus Master」均在170mm x 170mm的機箱內配備了105A的供電模組,這表明機殼尺寸不再是決定性能的唯一因素。 Micro-ATX仍然是低成本OEM塔式機殼的旗艦產品,它透過簡單的6層PCB堆疊結構,實現了四個擴充槽的平衡。 Extended-ATX主要用於雙路伺服器和超頻主機板,代表著一個細分市場,其主機板市場規模足以支撐超寬PCB的高價。

受電競咖啡館和家庭用戶對RGB燈效、高刷新率輸出和增強型PCIe插槽的需求驅動,消費者和DIY用戶預計到2025年將佔主機板銷售額的38.72%。儘管銷售成長放緩,中國和印度的遊戲場所仍保持著較高的平均售價(ASP)。相較之下,工業和嵌入式領域以10.44%的複合年成長率成長,透過五年組件藍圖以及自動化和智慧城市部署(這些部署需要符合IEC標準的可靠性),推動了主機板市場規模的擴大。

同時,企業和資料中心買家需要帶外管理、ECC記憶體和用於AI訓練的多GPU拓撲結構。 Supermicro的伺服器主機板採用NVIDIA NVLink雙通道技術,體現了消費級產品所不具備的設計特性。與消費級產品12至18個月的生產週期相比,36至48個月的更長生產週期降低了設計變更的頻率,提高了毛利率。遊戲主機板的平均售價(ASP)比工業主機板高出30%至50%,但工業主機板正透過整合認證、遠端監控硬體和延長保固服務,不斷縮小這一價格差距。

區域分析

到2025年,亞太地區將佔據全球36.71%的市場佔有率,這主要得益於台灣的ODM生態系統,該系統能夠縮短從原型到量產的前置作業時間;以及中國擁有1.2億台產能的組裝基地。日本廠商正將業務重心轉向符合IEC認證標準的工廠自動化(FA)主機板,而韓國則憑藉其在記憶體領域的優勢,供應可簡化基板設計的DDR5記憶體模組。澳洲和紐西蘭的貢獻小規模但意義重大,主要集中在企業桌面和教育機構部署領域,可預測的更新換代預算為其提供了穩定的收入基礎。

中東是成長最快的地區,預計到2031年將以10.52%的複合年成長率成長。沙烏地阿拉伯到2025年將擁有1,000億美元的數位經濟,加上該地區金融科技的蓬勃發展,正推動低成本桌上型電腦的研發,以滿足客服中心和政府機構的工作負載需求。阿拉伯聯合大公國價值200億美元的電子產業目前正在本地組裝用於資料中心部署的主機板,降低了進口障礙。間歇性停電和寬頻限制推動了對寬範圍電源(PSU)和被動散熱基板的需求,這些產品符合工業級規格,並提升了高功率SKU主機板在該地區市場的佔有率。

北美和歐洲是成熟市場,但它們是具有重要戰略意義的地區,關稅政策和生態設計法規會影響採購。美國根據《301條款》徵收的25%至35%的關稅促使生產基地轉移到越南和墨西哥。同時,《晶片法案》(CHIPS Act)提供的20億美元津貼支持美國國內的印刷基板)生產。歐盟關於可維修性的2024/1799號指令要求供應商提供七年的備件供應,這推動了模組化子板的設計。德國和英國在人工智慧伺服器的應用方面主導,法國正在推廣自主運算,俄羅斯正在加速本地組裝,所有這些都在推動主機板市場緩慢但持續的成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AM5 和 LGA-1851 平台的快速更新週期

- AI驅動的BIOS公用程式方便用戶自行升級。

- 工業IoT的發展需要堅固耐用的基板

- 人工智慧資料中心對伺服器主機板的需求

- 生態設計法規建議使用可維修基板。

- DDR5價格的下降導致總製造成本降低。

- 市場限制因素

- 由於世代交替導致的價格上漲,使得終端用戶在購買時猶豫不決。

- 多層PCB製造技術短缺

- 主要PCB原料的地緣政治關稅

- 二手LGA 1151基板正在蠶食市場佔有率。

- 價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按外形規格

- ATX

- Micro-ATX

- Mini-ITX

- Extended-ATX(E-ATX)

- 按最終用戶行業分類

- 消費者/DIY

- 遊戲和電競中心

- 工業/嵌入式

- 企業和資料中心

- 中央處理器

- 英特爾(LGA-1700/1851)

- AMD(AM4/AM5)

- 基於ARM的

- RISC-V 及其他

- 透過使用

- 桌上型電腦

- 工作站

- 伺服器

- 邊緣人工智慧和物聯網閘道器

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ASUSTeK Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd.(MSI)

- ASRock Incorporation

- Super Micro Computer, Inc.

- Advantech Co., Ltd.

- MiTAC Computing Technology Corporation

- Biostar Microtech International Corp.

- EVGA Corporation

- Acer Inc.

- Shenzhen Seavo Technology Co., Ltd.

- Sapphire Technology Ltd.

- AAEON Technology Inc.

- Kontron AG

- Advantech Europe BV

- DFI Inc.

- IEI Integration Corp.

- Dell Technologies Inc.

- Intel Corporation

- Lenovo Group Ltd.

第7章 市場機會與未來展望

The motherboard market size is projected to expand from USD 13.21 billion in 2025 and USD 15.66 billion in 2026 to USD 25.66 billion by 2031, registering a CAGR of 10.38% between 2026 to 2031.

Growing AI-centric server rollouts are lifting average selling prices for high-layer server boards even as the consumer segment grapples with DDR5 cost swings. Socket transitions to AMD AM5 and Intel LGA-1851 are compressing upgrade windows, while industrial buyers shift toward ruggedized designs that tolerate harsh environments. Asia-Pacific continues to anchor volume through Taiwan's ODM cluster and China's contract-manufacturing base, yet the Middle East is emerging as the fastest-growing region as digital-infrastructure investments accelerate. Component tariffs, multi-layer PCB skill shortages, and second-hand board availability temper near-term demand but do not derail the long-run trajectory of the motherboard market.

Global Motherboard Market Trends and Insights

Server Motherboard Demand From AI Data-Centres

Hyperscale operators expanded AI infrastructure by 61% year-over-year in 2024, and Supermicro's X14 boards supporting up to 12 GPUs per node illustrate how dense topologies are lifting board complexity and margins. Multi-layer stack-ups, redundant VRMs, and out-of-band management add bill-of-materials value that consumer SKUs cannot match. Taiwan ODMs supplied more than 60% of global server-board volume in 2024, leveraging proximity to substrate vendors. Adoption of PCIe 5.0 slots per PCI-SIG CEM 5.0 spec compounds signal-integrity challenges but secures higher ASPs. With major cloud providers budgeting multi-billion-dollar GPU clusters through 2027, server boards remain a pivotal growth engine.

Rapid AM5 and LGA-1851 Platform Refresh Cycles

Intel's Z890 and B860 chipsets, introduced alongside Arrow Lake CPUs in late 2024, dropped DDR4 support and folded Wi-Fi 7 and Thunderbolt 4 into baseline features, forcing faster channel inventory transitions. AMD's AM5 socket, conversely, pledges chipset compatibility through 2027, allowing board brands to span entry-level B650 to halo X870E with minimal socket redesign. ASRock's B850 series debuted in January 2025 at mid-market price points, providing PCIe 5.0 M.2 without overclocking extras. The compressed cadence benefits agile ODMs that can re-tool quickly, but smaller firms face margin squeeze as payback windows narrow. Consumers confront shorter perceived longevity, nudging upgrade behavior toward subscription-like frequency.

End-User Hesitation Due to Generational Price Jumps

A mid-tier LGA-1851 system in early 2025 required USD 200 for the motherboard, USD 150 for 32 GB DDR5-6000, and USD 120 for a PCIe 5.0 SSD, totaling USD 470 before CPU and GPU, versus USD 320 for a comparable 2024 build. Asia-Pacific sees 39% of PC shipments refurbished, highlighting price sensitivity. South American buyers confront additional import duties, with Brazil's IPI adding 10-15% to component costs. The wider delta delays purchase intent, lengthening replacement cycles and trimming short-run shipments. Vendors respond with cut-down chipset SKUs, bundled memory promotions, and financing options, but elasticity remains limited in low-income regions.

Other drivers and restraints analyzed in the detailed report include:

- AI-Accelerated BIOS Utilities Driving DIY Upgrades

- Growth of Industrial IoT Requiring Rugged Boards

- Skill Shortage In Multi-Layer PCB Manufacturing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ATX accounted for 45.28% of 2025 revenue, securing the largest motherboard market share for its robust expansion-slot layout and ample VRM headroom. Mini-ITX, however, is forecast to accelerate at a 10.41% CAGR through 2031 as enthusiasts pursue space-efficient gaming rigs and integrators deploy edge-AI appliances in constrained enclosures. Outside holiday peaks, ATX maintains a steady enterprise refresh cadence, while Mini-ITX spikes align with trade-show launches that unveil high-density PCIe 5.0 storage capabilities.

PCIe 5.0 lanes and 16-phase VRMs have migrated into Mini-ITX, eroding the historical performance gap. ASRock's Taichi OCF Mini-ITX and Gigabyte's X870E Aorus Master showcase 105 A power stages inside 170 mm X 170 mm footprints, signaling that footprint no longer dictates capability. Micro-ATX remains the volume workhorse for budget OEM towers, balancing four expansion slots against simpler six-layer PCB stack-ups. Extended-ATX persists mainly in dual-socket servers and showcase overclocking boards, niches where the motherboard market size supports premium pricing on extra-wide PCBs.

Consumer and DIY builders generated 38.72% of 2025 sales, fueled by eSports cafes and home creators who value RGB lighting, high-refresh outputs, and reinforced PCIe slots. Gaming venues in China and India sustain high ASPs despite moderating unit growth. The industrial and embedded segment, by contrast, is on a 10.44% CAGR path that elevates the motherboard market size across automation and smart-city rollouts needing 5-year component roadmaps and IEC-compliant ruggedness.

Enterprise and data-center buyers demand out-of-band management, ECC memory, and multi-GPU topologies for AI training. Supermicro's server boards with NVIDIA NVLink bifurcation exemplify design features absent from the consumer realm. Longer 36-48 month production runs reduce design churn, improving gross margins relative to 12-18 month consumer cadences. Although gaming boards sell at 30-50% ASP premiums, industrial motherboards increasingly match that uplift by layering certifications, remote-monitoring hardware, and extended warranty packages.

The Motherboard Market Report is Segmented by Form Factor (ATX, Micro-ATX, Mini-ITX, and Extended-ATX), End-User Industry (Consumer/DIY, Gaming and ESports Centres, Industrial/Embedded, and Enterprise and Data-Centre), CPU Platform (Intel LGA-1700/1851, AMD AM4/AM5, and More), Application (Desktop PCs, Workstations, Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 36.71% of the 2025 value, sustained by Taiwan's ODM ecosystem that compresses prototype-to-production lead times and China's 120 million-unit assembly base. Japanese vendors pivot toward factory-automation motherboards with IEC certifications, while South Korea's memory dominance supplies DDR5 modules that streamline board design. Australia and New Zealand contribute modest volumes, mainly in enterprise desktops and educational deployments, yet predictable refresh budgets create a resilient revenue floor.

The Middle East is the fastest-growing territory at a 10.52% CAGR through 2031. Saudi Arabia's USD 100 billion 2025 digital economy and the region's fintech boom are catalyzing low-cost desktop builds for call-center and government workloads. The United Arab Emirates's USD 20 billion electronics sector now locally assembles motherboards for data-center rollouts, reducing import friction. Intermittent power and broadband constraints drive demand for boards with wide-input PSUs and passive cooling, aligning with industrial-grade specifications and boosting regional motherboard market share for rugged SKUs.

North America and Europe represent mature but strategically important regions where tariff policies and eco-design mandates shape sourcing. The United States' 25%-35% Section 301 duties sparked diversification to Vietnam and Mexico, while USD 2 billion in CHIPS Act grants targets domestic substrate production. Europe's Directive 2024/1799 on repairability obliges vendors to supply spares for seven years, nudging designs toward modular daughtercards. Germany and the United Kingdom spearhead AI server deployments, whereas France promotes sovereign compute and Russia accelerates local assembly, all reinforcing sustained, if moderate, motherboard market growth.

- ASUSTeK Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- ASRock Incorporation

- Super Micro Computer, Inc.

- Advantech Co., Ltd.

- MiTAC Computing Technology Corporation

- Biostar Microtech International Corp.

- EVGA Corporation

- Acer Inc.

- Shenzhen Seavo Technology Co., Ltd.

- Sapphire Technology Ltd.

- AAEON Technology Inc.

- Kontron AG

- Advantech Europe B.V.

- DFI Inc.

- IEI Integration Corp.

- Dell Technologies Inc.

- Intel Corporation

- Lenovo Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid AM5 and LGA-1851 Platform Refresh Cycles

- 4.2.2 AI-Accelerated BIOS Utilities Driving DIY Upgrades

- 4.2.3 Growth of Industrial IoT Requiring Rugged Boards

- 4.2.4 Server Motherboard Demand From AI Data-Centres

- 4.2.5 Eco-Design Regulations Favoring Repairable Boards

- 4.2.6 Falling DDR5 Prices Lowering Total Build Costs

- 4.3 Market Restraints

- 4.3.1 End-User Hesitation Due to Generational Price Jumps

- 4.3.2 Skill Shortage in Multi-Layer PCB Manufacturing

- 4.3.3 Geopolitical Tariffs on Key PCB Raw Materials

- 4.3.4 Second-Hand LGA 1151 Boards Cannibalizing Sales

- 4.4 Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Form Factor

- 5.1.1 ATX

- 5.1.2 Micro-ATX

- 5.1.3 Mini-ITX

- 5.1.4 Extended-ATX (E-ATX)

- 5.2 By End-user Industry

- 5.2.1 Consumer / DIY

- 5.2.2 Gaming and eSports Centres

- 5.2.3 Industrial / Embedded

- 5.2.4 Enterprise and Data-centre

- 5.3 By CPU Platform

- 5.3.1 Intel (LGA-1700 / 1851)

- 5.3.2 AMD (AM4 / AM5)

- 5.3.3 ARM-based

- 5.3.4 RISC-V and Others

- 5.4 By Application

- 5.4.1 Desktop PCs

- 5.4.2 Workstations

- 5.4.3 Servers

- 5.4.4 Edge-AI and IoT Gateways

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASUSTeK Computer Inc.

- 6.4.2 GIGABYTE Technology Co., Ltd.

- 6.4.3 Micro-Star International Co., Ltd. (MSI)

- 6.4.4 ASRock Incorporation

- 6.4.5 Super Micro Computer, Inc.

- 6.4.6 Advantech Co., Ltd.

- 6.4.7 MiTAC Computing Technology Corporation

- 6.4.8 Biostar Microtech International Corp.

- 6.4.9 EVGA Corporation

- 6.4.10 Acer Inc.

- 6.4.11 Shenzhen Seavo Technology Co., Ltd.

- 6.4.12 Sapphire Technology Ltd.

- 6.4.13 AAEON Technology Inc.

- 6.4.14 Kontron AG

- 6.4.15 Advantech Europe B.V.

- 6.4.16 DFI Inc.

- 6.4.17 IEI Integration Corp.

- 6.4.18 Dell Technologies Inc.

- 6.4.19 Intel Corporation

- 6.4.20 Lenovo Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

嵌入式板、模組和系統:現代產品開發和邊緣解決方案建構的基本平台。

嵌入式板、模組和系統:現代產品開發和邊緣解決方案建構的基本平台。 工業主機板市場報告:按類型、應用和地區分類(2026-2034 年)

工業主機板市場報告:按類型、應用和地區分類(2026-2034 年) 小型化電路板市場:2026-2032年全球市場預測(按組件、部署模式、定價模式、技術、應用、最終用途和分銷管道分類)主機板市場:按外形規格、記憶體支援、散熱設計、應用、最終用戶和分銷管道分類-2026-2032年全球預測

小型化電路板市場:2026-2032年全球市場預測(按組件、部署模式、定價模式、技術、應用、最終用途和分銷管道分類)主機板市場:按外形規格、記憶體支援、散熱設計、應用、最終用戶和分銷管道分類-2026-2032年全球預測 工業主機板市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、組件、銷售管道、地區和競爭格局分類),2021-2031年冗餘I/O模組和系統市場(按模組類型、系統類型、資料速率、應用和最終用戶分類)-2026年至2032年全球預測整合主機板市場:按記憶體支援、晶片組、外形規格、價格範圍、應用、最終用戶和分銷管道分類,全球預測,2026-2032年主機板市場-2025年至2030年預測

工業主機板市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、組件、銷售管道、地區和競爭格局分類),2021-2031年冗餘I/O模組和系統市場(按模組類型、系統類型、資料速率、應用和最終用戶分類)-2026年至2032年全球預測整合主機板市場:按記憶體支援、晶片組、外形規格、價格範圍、應用、最終用戶和分銷管道分類,全球預測,2026-2032年主機板市場-2025年至2030年預測 嵌入式板和模組:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

嵌入式板和模組:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 全球工業主機板市場

全球工業主機板市場