|

市場調查報告書

商品編碼

2044168

東協低溫運輸物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)ASEAN Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

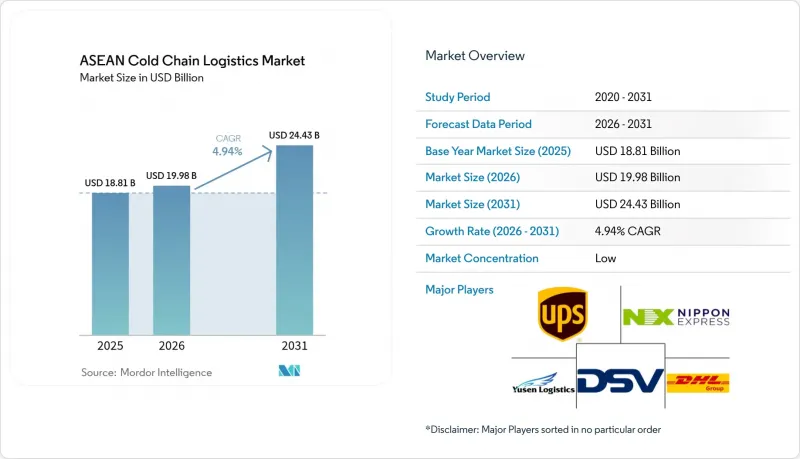

東協低溫運輸物流市場規模預計將從 2025 年的 188.1 億美元和 2026 年的 199.8 億美元成長到 2031 年的 244.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.94%。

隨著東協地區食品供應鏈日益規範化和出口導向化,該地區的低溫運輸物流市場正逐步擴張。泰國、越南和印尼等水產品、肉類和熱帶水果產量較高的國家正在增加對冷藏和溫控運輸的投資,以減少採後損失並支持出口。同時,現代零售、快餐食品平台和藥品分銷的擴張也推動了全部區域對更可靠的低溫運輸基礎設施的需求。然而,市場仍存在不平衡;新加坡等先進樞紐擁有完善的物流能力,而東協一些新興經濟體仍缺乏足夠的冷藏保管能力和分銷網路。因此,物流公司正致力於建立區域性冷藏保管樞紐、改善監控技術並加強跨境供應鏈,以滿足不斷成長的需求。

東協低溫運輸物流市場趨勢與洞察

中產階級可支配收入的增加推動了對進口冷凍和冷藏食品的需求。

東協主要經濟區收入的成長推動了對進口蛋白質、優質乳製品和預製食品的需求,而這些產品需要可靠的冷凍和冷藏運輸。都市區零售商正在擴大溫控商品的種類,以滿足消費者對新鮮度和品質日益成長的需求。在穆斯林人口占多數的市場,對清真認證的冷凍和加工食品的需求不斷成長,因為這些食品需要單獨的儲存條件並遵守清真物流法規。季節性災害,例如菲律賓的颱風季,凸顯了儲備物資和可靠配送路線的重要性。隨著買家將溫度敏感貨物的管理放在首位,這些趨勢正在推動東協低溫運輸物流市場的成長。

現代零售商店和超級市場超市在二、三線城市的擴張

便利商店和連鎖超市正將業務拓展至都會區以外的區域城市,從而催生了對短途冷藏補貨和微型倉配的分散需求。易買得24計畫在2026年在馬來西亞、柬埔寨和寮國開設130家門市,並採用24小時營運模式,這要求飲料和已調理食品的儲存和配送溫度維持在攝氏2-8度之間。印尼的Alfamart正在將其業務拓展至主要群島以外的島嶼,增加冷藏車的配送密度,以服務先前依賴常溫庫存的城鎮。零售商正在實施冷藏櫃的遠端溫度監控和異常預警系統,加強門市與上游物流中心之間的協作,並提高對承運商和倉庫資料視覺的期望。隨著這些基礎設施的改進,東協低溫運輸物流市場正朝著模組化交叉轉運、規模適宜的冷藏庫和靈活的卡車運輸模式發展。能夠擴展小規模地點並快速調整路線的供應商,相對於依賴大規模集中式地點的營運商而言,正在獲得優勢。

成員國之間監管不一致和低溫運輸標準差異

各國對清真食品和藥品的相關法規各不相同,這使得設施設計、員工培訓和跨境文件處理都變得複雜。印尼第42/2024號法規強制要求設立專用的清真冷藏室和清真處理流程,增加了認證設施的成本。馬來西亞的MS 2400標準要求物流區域之間必須隔離,提高了設施配置和審核要求。與一些鄰近市場不同,新加坡的HSA GDP規則強制要求藥品物流必須使用經過驗證的設施並建立監管鏈。這些差異增加了實施成本,並提高了因文件不一致而導致運輸延誤的風險。擁有集中合規方案的領先整合商正在更快地適應這些變化,從而影響了它們在東協低溫運輸物流市場的佔有率。

細分市場分析

到2025年,冷藏保管將佔49.3%的市場佔有率,而附加價值服務將以5.7%的複合年成長率快速成長。這是因為品牌所有者正在將生命科學貨物的快速冷凍、重新包裝、符合GDP標準的標籤以及經過驗證的包裝等服務外包。就東協低溫運輸物流市場規模而言,具備-80 度C儲存能力和數位化管理功能的醫藥專用設施正在不斷擴展,因為越來越多的營運商正在為臨床試驗材料和生技藥品建立符合GDP標準的環境。 UPS於2025年6月將其在新加坡的儲存容量加倍,新增了超低溫冷凍庫和視覺功能。這將有助於醫療保健托運人更容易滿足審計要求和交付限制。陸路運輸仍是國內物流的主要運輸方式,GPS遙測技術被用於處理異常情況和最佳化敏感路線的運輸路線。海運網路持續擴展冷凍食品的島際連接,區域航運公司已宣布增加冷藏貨櫃運力,以滿足國內和出口貨運的需求。航空貨運支援生技藥品和高度敏感貨物,這些貨物需要嚴格遵守交貨時間,在運輸過程中保持品質並記錄儲存歷史是選擇承運人的關鍵因素。

公共倉庫正逐漸佔據主導地位,進口商和經銷商更傾向於可擴展且資產密集度較低的倉儲方式,而非可能受監管變化影響的私人投資。對於優先考慮存貨周轉管理、產品擴充性和出口準備的垂直整合加工商而言,私人冷庫仍然至關重要。泰國新建的多溫區倉庫於2024年12月在曼谷附近投入運作,其建設模式凸顯了支持電子商務和零售整合的趨勢,因為隨著門市網路的擴張,這種整合正在加速。在醫藥產業,良好儲存和運輸(GDP)法規正推動物流企業向擁有經審計設施和驗證設備的地區轉移,從而促進加值服務的差異化。隨著能源韌性和監控的標準化,東協低溫運輸物流市場的服務期望不斷提高,供應商也開始將合規狀態作為衡量自身能力的指標。因此,東協低溫運輸物流行業正朝著更高的服務標準邁進,而文件和技術的應用則為其提供了支持。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中產階級可支配收入的增加推動了對進口冷凍和冷藏食品的需求。

- 現代零售商店和超級市場超市在二、三線城市的擴張

- 外國直接投資(FDI)流入待開發區冷庫和物流中心開發

- 政府糧食安全計畫要求在收穫後具備冷藏保管能力。

- 越南、泰國和印尼水產養殖業的快速發展促進了水產品冷藏物流的發展。

- 區域自由貿易協定(RCEP、CPTPP)促進了冷藏農產品的貿易流動。

- 市場限制因素

- 成員國之間監管不一致和低溫運輸標準差異

- 高昂的初始資本投入阻礙了中小低溫運輸企業進入該領域。

- 非官方和不受監管的冷藏倉庫營運商的競爭正在壓低價格。

- 容易受到氣候變遷和極端天氣事件的影響,這些事件會破壞低溫運輸。

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 排放標準和法規的影響

- 冷媒和包裝材料的見解

- 清真標準與認證概況(印度和馬來西亞)

- 對環境溫度和溫控儲存的深入了解

- 地緣政治影響力

第5章 市場規模與成長預測

- 按服務類型

- 冷藏保管。

- 公共倉庫

- 私人倉庫

- 冷藏運輸

- 路

- 鐵路

- 海

- 航空郵件

- 附加價值服務

- 冷藏保管。

- 按溫度類型

- 冷藏(0-5 度C)

- 冷凍(-18~0 度C)

- 環境的

- 超低溫(低於-20 度C)

- 透過使用

- 水果和蔬菜

- 肉類/家禽

- 魚貝類

- 乳製品和冷凍甜點

- 麵包糖果甜點

- 已調理食品

- 藥品和生物製藥

- 疫苗和臨床試驗樣本

- 化學品/特殊材料

- 其他生鮮食品

- 按地區

- 新加坡

- 泰國

- 越南

- 印尼

- 馬來西亞

- 菲律賓

- 其他東南亞國協

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deutsche Post DHL

- Nippon Express

- United Parcel Service(UPS)

- Yusen Logistics(Part of NYK Line)

- DSV

- Yamato Transport

- JWD Logistics

- Royal Cargo

- KOSPA Logistics

- PT Wahana Cold Storage

- Thai Max Co. Ltd

- HAVI Logistics

- Lineage Logistics

- Kuehne+Nagel

- Nichirei Logistics

- Kerry Logistics

- AJ Total Vietnam

- YCH Group

- Linfox

- MGM Bosco Logistics

第7章 市場機會與未來展望

The ASEAN Cold Chain Logistics Market size is projected to expand from USD 18.81 billion in 2025 and USD 19.98 billion in 2026 to USD 24.43 billion by 2031, registering a CAGR of 4.94% between 2026 to 2031.

The ASEAN cold chain logistics market is gradually strengthening as regional food supply chains become more organized and export-oriented. Countries with strong seafood, meat, and tropical fruit production, such as Thailand, Vietnam, and Indonesia, are increasing investments in refrigerated storage and temperature-controlled transportation to reduce post-harvest losses and support exports. At the same time, the expansion of modern retail, quick-commerce grocery platforms, and pharmaceutical distribution is pushing demand for more reliable cold chain infrastructure across the region. However, the market remains uneven, with developed hubs like Singapore having advanced logistics capabilities while several emerging ASEAN economies still face gaps in cold storage capacity and distribution networks. As a result, logistics companies are focusing on building regional cold storage hubs, improving monitoring technologies, and strengthening cross-border supply chains to capture growing demand.

ASEAN Cold Chain Logistics Market Trends and Insights

Growing Middle-Class Disposable Income Driving Demand for Imported Frozen and Chilled Goods

Rising incomes in large ASEAN economies are driving demand for imported proteins, premium dairy, and ready-to-cook formats requiring reliable frozen and chilled transport. Urban retailers are increasing temperature-sensitive assortments to meet higher demand for freshness and quality. In Muslim-majority markets, halal-certified frozen meals and processed foods necessitate segregated storage and compliance with halal logistics rules, boosting demand for certified providers. Seasonal disruptions, like storm seasons in the Philippines, highlight the need for stockpiles and reliable distribution routes. These trends are fueling growth in the ASEAN cold chain logistics market as buyers prioritize custody control for sensitive cargo.

Modern Retail and Supermarket Chain Expansion Across Tier-2 and Tier-3 Cities

Convenience and grocery chains are scaling beyond capitals into secondary cities, which creates distributed demand for short-haul chilled replenishment and micro-fulfillment. E-Mart24's 2026 plan to open 130 stores in Malaysia, Cambodia, and Laos introduces 24-hour formats that require consistent 2-8°C storage and delivery routines for beverages and ready meals. Indonesia's Alfamart is extending its footprint across secondary islands, which deepens route density for chilled fleets serving towns that previously relied on ambient stock. Retailers are bringing in remote temperature monitoring and exception alerts for cold cases, which tightens coordination between stores and upstream distribution and raises expectations for data visibility from carriers and warehouses. This buildout shifts the ASEAN cold chain logistics market toward modular cross-docks, right-sized cold rooms, and flexible trucking. Providers that can scale smaller nodes and adjust routing quickly are gaining an edge over operators concentrated in large centralized sites.

Regulatory Inconsistencies and Varying Cold Chain Standards Across Member States

Halal and pharmaceutical regulations vary by country, complicating facility design, staff training, and cross-border documentation. Indonesia's Regulation 42/2024 mandates halal-only cold rooms and dedicated handling flows, increasing costs for certified sites. Malaysia's MS 2400 standard requires segregation across logistics zones, raising configuration and audit demands. Singapore's HSA GDP rules enforce validated equipment and chain-of-custody for pharmaceutical logistics, unlike some neighboring markets. These differences increase onboarding costs and risk shipment delays due to misaligned paperwork. Large integrators with centralized compliance programs adapt faster, influencing market share in the ASEAN cold chain logistics market.

Other drivers and restraints analyzed in the detailed report include:

- FDI Inflows in Greenfield Cold Storage and Distribution Center Development

- Government Food Security Programs Mandating Post-Harvest Cold Storage Capacity

- High Upfront Capital Expenditure Deterring SME Cold Chain Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage commands 49.3% share in 2025, while value-added services are growing fastest at 5.7% CAGR as brand owners outsource blast-freezing, repackaging, GDP-compliant labeling, and validated packing for life-sciences loads. Within the ASEAN cold chain logistics market size context, pharma-focused nodes with -80°C capacity and digitized custody are expanding as operators build GDP-ready environments for clinical-trial materials and biologics. UPS doubled Singapore capacity in June 2025, adding ultra-low freezers and visibility features that help healthcare shippers meet audit requirements and timing constraints. Road remains the primary mode for intra-country logistics and uses GPS-linked telemetry for exception handling and route optimization in sensitive lanes. Maritime networks continue to scale inter-island connectivity for frozen foods, and regional carriers have signaled reefer expansion to serve domestic and export flows. Airfreight supports time-bound biologics and high-care shipments, where transit integrity and chain-of-custody records define provider choice.

Public warehousing dominates, where importers and distributors prefer scalable, asset-light access rather than private investment that may be exposed to regulatory change. Private cold rooms remain critical for vertically integrated processors that prioritize control of inventory turns, blending, and export readiness. Thailand's new multi-temperature warehouse commissioned near Bangkok in December 2024 highlights a build pattern that supports e-commerce and retail consolidation as store networks expand. In pharmaceuticals, GDP rules steer flows toward audited facilities and handling zones with validated equipment, which supports premium service differentiation. As energy resilience and monitoring become standard, service expectations are rising across the ASEAN cold chain logistics market, and providers are using compliance status to signal capability. The ASEAN cold chain logistics industry is therefore shifting toward higher service baselines supported by documentation and technology adoption.

The ASEAN Cold Chain Logistics Market is Segmented by Service Type (Refrigerated Storage, Transportation, and Value-Added Services), by Temperature (Chilled, Frozen, Ambient, and Deep-Frozen), by Application (Fruits and Vegetables, Meat and Poultry, Fish and Seafood and More), and by Geography (Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines, and Rest of ASEAN). Forecasts are in Value (USD).

List of Companies Covered in this Report:

- Deutsche Post DHL

- Nippon Express

- United Parcel Service (UPS)

- Yusen Logistics (Part of NYK Line)

- DSV

- Yamato Transport

- JWD Logistics

- Royal Cargo

- KOSPA Logistics

- PT Wahana Cold Storage

- Thai Max Co. Ltd

- HAVI Logistics

- Lineage Logistics

- Kuehne + Nagel

- Nichirei Logistics

- Kerry Logistics

- AJ Total Vietnam

- YCH Group

- Linfox

- MGM Bosco Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Middle-Class Disposable Income Driving Demand for Imported Frozen and Chilled Goods

- 4.2.2 Modern Retail and Supermarket Chain Expansion Across Tier-2 And Tier-3 Cities

- 4.2.3 FDI Inflows in Greenfield Cold Storage and Distribution Center Development

- 4.2.4 Government Food Security Programs Mandating Post-Harvest Cold Storage Capacity

- 4.2.5 Aquaculture Industry Boom in Vietnam, Thailand, and Indonesia Boosting Seafood Cold Logistics

- 4.2.6 Regional Free Trade Agreements (RCEP, CPTPP) are Facilitating Chilled Agri-Food Trade Flows

- 4.3 Market Restraints

- 4.3.1 Regulatory Inconsistencies and Varying Cold Chain Standards Across Member States

- 4.3.2 High Upfront Capital Expenditure Deterring SME Cold Chain Operators

- 4.3.3 Competition From Informal and Unregulated Cold Storage Providers is Undercutting Prices

- 4.3.4 Climate Vulnerability and Extreme Weather Disrupting Cold Chain Continuity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Emission Standards and Regulations

- 4.9 Insights into Refrigerants and Packaging Materials

- 4.10 Insights into Halal Standards and Certifications (ID and MY)

- 4.11 Insights into Ambient / Temperature-controlled Storage

- 4.12 Geopolitical Impact

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5°C)

- 5.2.2 Frozen (-18-0°C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen/Ultra-Low (less than-20°C)

- 5.3 By Application

- 5.3.1 Fruits and Vegetables

- 5.3.2 Meat and Poultry

- 5.3.3 Fish and Seafood

- 5.3.4 Dairy and Frozen Desserts

- 5.3.5 Bakery and Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals and Biologics

- 5.3.8 Vaccines and Clinical Trial Materials

- 5.3.9 Chemicals and Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Geography

- 5.4.1 Singapore

- 5.4.2 Thailand

- 5.4.3 Vietnam

- 5.4.4 Indonesia

- 5.4.5 Malaysia

- 5.4.6 Philippines

- 5.4.7 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Deutsche Post DHL

- 6.4.2 Nippon Express

- 6.4.3 United Parcel Service (UPS)

- 6.4.4 Yusen Logistics (Part of NYK Line)

- 6.4.5 DSV

- 6.4.6 Yamato Transport

- 6.4.7 JWD Logistics

- 6.4.8 Royal Cargo

- 6.4.9 KOSPA Logistics

- 6.4.10 PT Wahana Cold Storage

- 6.4.11 Thai Max Co. Ltd

- 6.4.12 HAVI Logistics

- 6.4.13 Lineage Logistics

- 6.4.14 Kuehne + Nagel

- 6.4.15 Nichirei Logistics

- 6.4.16 Kerry Logistics

- 6.4.17 AJ Total Vietnam

- 6.4.18 YCH Group

- 6.4.19 Linfox

- 6.4.20 MGM Bosco Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

城市低溫運輸物流市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類)都市區低溫運輸配送市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類)

城市低溫運輸物流市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類)都市區低溫運輸配送市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類) 低溫運輸物流市場:依服務類型、溫度區域和最終用途分類-2026-2032年全球市場預測低溫運輸市場:2026-2032年全球市場預測(依溫度範圍、設備類型、服務模式、最終用戶及通路分類)

低溫運輸物流市場:依服務類型、溫度區域和最終用途分類-2026-2032年全球市場預測低溫運輸市場:2026-2032年全球市場預測(依溫度範圍、設備類型、服務模式、最終用戶及通路分類) 2026年全球低溫運輸市場報告2026年全球冷凍食品物流市場報告

2026年全球低溫運輸市場報告2026年全球冷凍食品物流市場報告 低溫運輸市場:按類型、包裝產品、材料、設備、應用和地區分類2026年全球低溫運輸物流市場報告

低溫運輸市場:按類型、包裝產品、材料、設備、應用和地區分類2026年全球低溫運輸物流市場報告 南美洲低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年

南美洲低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年