|

市場調查報告書

商品編碼

2043984

南美洲低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

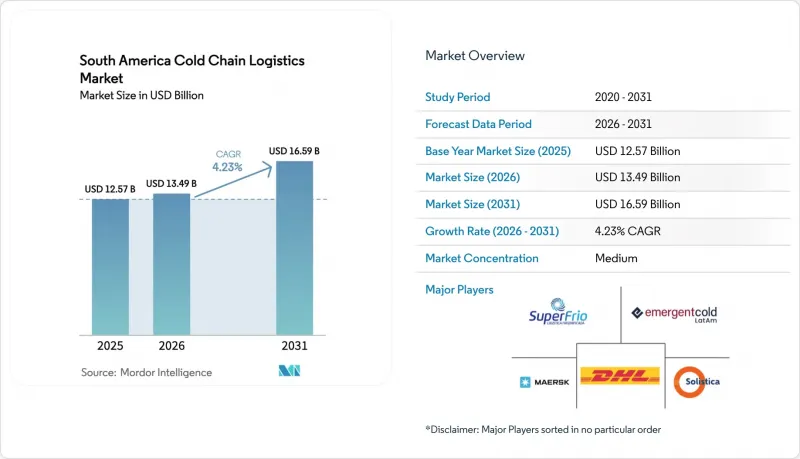

預計南美低溫運輸物流市場規模將從 2025 年的 125.7 億美元和 2026 年的 134.9 億美元成長到 2031 年的 165.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.23%。

市場正從傳統的商品出口通道轉型為生物製藥、線上食品零售商的微型倉配以及近岸蛋白質加工的溫控樞紐。歐盟與南方共同市場於2026年1月簽署的過渡貿易協定,正迫使出口商實施符合無毀林採購規則的可追溯系統。此外,疫苗分發系統的持續改進正在加速許多國家老舊冷藏設施的現代化改造。一線城市冷藏倉庫的緊缺空率正促使投資轉向二線城市,這些城市的土地價格更低、電網更可靠、最後一公里配送距離更短。各國根據《基加利修正案》制定的法規正在推動天然冷媒的應用,雖然這會增加初始投資成本,但可以降低長期能源成本,改善整體擁有成本,並加強永續性發展。儘管成熟的全球公司透過收購本地專家和實施自動化及物聯網監控維修資產,競爭仍然較為溫和,但國內公司在需要細緻服務的細分領域仍然保持著強大的地位。

南美洲低溫運輸物流市場趨勢與分析

都市區對加工食品和冷凍食品的需求增加

預計到2025年,都市化將超過87%,單身和雙薪家庭將推動對依賴高效冷藏物流的速食食品的需求。在聖保羅和聖地牙哥,冷凍主菜、速凍蔬菜和高級冰淇淋佔食品雜貨消費的22%,高於2023年的16%。 iFood公司正將其170億雷亞爾(約34億美元)基礎設施計畫中的30%用於建設溫控區,以支援15分鐘送達服務,並敦促倉庫營運商在人口密集區5公里範圍內建立基地。零售商正在採用可根據當地需求變化進行移動的模組化冷藏單元,從而降低資產閒置的風險。智利和阿根廷也出現了類似的趨勢,預計到2025年,兩國人均冷凍食品消費量將分別成長9%和11%,這顯示全部區域都呈現出強勁的成長動能。

擴大疫苗和生技藥品分銷網路

到2025年,多邊金融機構將投資1.8億美元,用於秘魯、哥倫比亞和玻利維亞的疫苗物流現代化改造,更換農村診所的老舊設備,這些診所的疫苗浪費率曾超過10%。新的基礎設施包括太陽能冷卻器和即時數據記錄儀,製藥公司也將其用於運輸臨床實驗藥物,從而將患者入組時間縮短5至7天。藥品監管規程的協調統一已將巴西和阿根廷的進口核准時間從90天縮短至不到45天,申辦方現在可以預先將藥品儲存在-80 度C的低溫環境中。因此,藥品和生技藥品目前以6.94%的複合年成長率成為成長最快的細分市場,是傳統蛋白質類藥品成長率的兩倍。

冷藏公路基礎設施有限,能源成本飆漲

巴西僅有12%的鋪裝道路達到「良好」或「優秀」標準,使得卡車平均時速僅45公里/小時,柴油消耗量比智利高出20%。路面坑洞造成的震動會加速壓縮機的磨損,導致大修週期從18個月縮短至12個月。 2025年,巴西北部工業用電平均價格為0.52雷亞爾/千瓦時(0.10美元),但頻繁的停電迫使工廠在高達20%的運作時間內依靠發電機供電,這給低利潤率的蛋白質貨物運輸帶來了壓力。阿根廷農村電網也面臨類似的問題,停電時間長達六小時,增加了缺乏足夠溫度緩衝措施的工廠食品變質的風險。

細分市場分析

到2025年,冷藏運輸將佔據最大的市場佔有率,達到55.69%,這表明南美低溫運輸物流市場在長途運輸方面嚴重依賴卡車運輸。然而,預計到2031年,冷藏鐵路運輸的複合年成長率將達到5.54%,成為該細分市場中成長最快的領域。由Lumo Logistica營運的從馬托格羅索州到桑托斯港的1000公里鐵路,已將大豆產品的運輸時間縮短了18小時,並將每噸公里排放降低了65%,凸顯了其環境和成本優勢。道路運輸仍然是300公里以下「最後一公里」運輸的主要方式,但柴油價格的波動正促使托運人在排放管制地區轉向天然氣卡車。雖然冷藏海運在現有航線上保持穩定的需求,但空運仍僅限於高階水產品和緊急生技藥品等小眾市場。

隨著企業收入來源多元化,附加價值服務日益受到重視。快速冷凍、套件組裝和溫控電履約通常比標準倉儲服務溢價20-30%。隨著線上食品市場的進一步滲透,位於都市區倉庫內的微型倉配中心數量不斷增加,對高速揀貨包裝系統和即時溫度監控提出了更高的要求。在消費者行為變化和零售商對當日補貨需求的推動下,受這些服務的驅動,南美洲低溫運輸物流市場預計將以超過整體市場成長率的速度成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 都市區對加工食品和冷凍食品的需求增加

- 擴大疫苗和生技藥品的溫控配送網路

- 政府出口獎勵措施強調低溫運輸合規性

- 北美地區的蛋白質採購正逐漸轉向南方共同市場(南美共同市場)地區的供應商。

- 巴西二線城市電子商務食品微型倉配業務的成長

- 南方共同市場國家肉類、家禽及水產品出口增加。

- 市場限制因素

- 冷藏公路基礎設施有限且能源成本不斷上漲

- 缺乏統一的跨境監管標準

- 工業冷凍設備操作熟練人員短缺。

- 電費上漲和電力供應可靠性問題反覆出現。

- 價值/供應鏈分析

- 監理情勢

- 技術創新前景

- 波特五力分析

- 新參與企業的威脅

- 供應商議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭關係

第5章:市場規模與成長率預測(以金額為準,2026-2031 年)

- 按服務類型

- 冷藏保管。

- 冷藏運輸

- 路

- 鐵路

- 船運

- 航空

- 附加價值服務

- 按溫度類型

- 冷藏(0-5 度C)

- 冷凍(-18~0 度C)

- 室溫

- 超低溫(低於-20 度C)

- 透過使用

- 水果和蔬菜

- 肉類/家禽

- 魚貝類

- 乳製品和冷凍甜點

- 麵包糖果甜點

- 即食食品

- 藥品和生物製藥

- 疫苗和臨床試驗樣本

- 化學品/特殊材料

- 其他生鮮食品

- 國家

- 阿根廷

- 巴西

- 智利

- 秘魯

- 哥倫比亞

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 主要策略趨勢

- 市佔率分析

- 公司簡介

- Emergent Cold LatAm

- Solistica(Traxion)

- SuperFrio Logistica Frigorificada

- Friozem Armazens Frigorificados

- DHL Supply Chain

- Maersk(Sealand Americas Cold Chain)

- Americold Realty Trust

- JSL Transportadora(Fadel Logistica Fria)

- Serbom

- TPC Logistica

- Arfrio

- Ransa Comercial SA

- Iceport

- Kuehne+Nagel

- CMA CGM(incl. CEVA Logistics)

- Refrio Armazens Gerais Frigorificos

- IceStar

- Brado Logistica SA

- AGUNSA

- CAP Logistica Frigorificada

第7章 市場機會與未來展望

The South America cold chain logistics market size is projected to expand from USD 12.57 billion in 2025 and USD 13.49 billion in 2026 to USD 16.59 billion by 2031, registering a CAGR of 4.23% between 2026 to 2031.

The market is shifting from its historic role as a commodity-export conduit toward a temperature-controlled hub for biologics, e-grocery micro-fulfillment, and near-shored protein processing. The January 2026 EU-Mercosur interim trade agreement is spurring exporters to install traceability systems that satisfy deforestation-free sourcing rules, while ongoing vaccine-distribution upgrades have accelerated replacement of obsolete refrigeration equipment across multiple countries. Tight cold-storage vacancy in Tier-1 metros is redirecting investment to Tier-2 cities where land is cheaper, grid reliability is better, and first-mile distances are shorter. Rising adoption of natural refrigerants mandated by national Kigali Amendment regulations is lifting capital costs but lowering long-run energy spend, improving total cost of ownership, and bolstering sustainability credentials. Competitive intensity remains moderate as global incumbents buy regional specialists and retrofit assets with automation and IoT monitoring, yet domestic players still hold strong positions in niche high-touch segments.

South America Cold Chain Logistics Market Trends and Insights

Increasing Urban Demand for Processed and Frozen Food Products

Urbanization surpassed 87% in 2025, and single-person as well as dual-income households are fueling demand for convenience meals that rely on robust refrigeration logistics. Frozen entrees, IQF vegetables, and premium ice creams now occupy 22% of grocery baskets in Sao Paulo and Santiago, up from 16% in 2023. iFood earmarked 30% of its BRL 17 billion (USD 3.4 billion) infrastructure plan for temperature-controlled zones that support 15-minute delivery, forcing warehouse operators to locate within five kilometers of high-density districts. Retailers are adopting modular cold rooms that can be moved as neighborhood demand shifts, cutting stranded-asset risk. Chile and Argentina echo the trend, with per-capita frozen-food intake rising 9% and 11% respectively in 2025, signaling region-wide momentum.

Expansion of Vaccine & Biologics Distribution Networks

Multilateral lenders invested USD 180 million in 2025 to modernize vaccine logistics in Peru, Colombia, and Bolivia, replacing obsolete equipment in rural clinics where spoilage once exceeded 10%. The new infrastructure includes solar-powered coolers and real-time data loggers that pharmaceutical firms are re-deploying for investigational therapies, shaving 5-7 days off patient-enrollment timelines. Harmonized drug-regulation protocols have cut import-permit approvals from 90 days to under 45 days in Brazil and Argentina, allowing sponsors to pre-position -80 °C materials. Consequently, pharmaceuticals and biologics now post the fastest segment growth at 6.94% CAGR, doubling the pace of traditional protein categories.

Limited Refrigerated Road Infrastructure and Rising Energy Costs

Only 12% of Brazil's paved highways meet "good" or "excellent" standards, limiting average truck speeds to 45 km/h and inflating diesel burn by 20% relative to Chilean hauls. Pothole-induced vibration accelerates compressor wear, shortening overhaul intervals from 18 to 12 months. Northern Brazil's industrial-power tariff averaged BRL 0.52/kWh (USD 0.10) in 2025, and frequent outages force facilities to run generators for up to 20% of operating hours, eroding profit on low-margin protein cargos. Argentina's rural grid faces similar blackouts lasting up to six hours, raising spoilage risk in sites without sufficient thermal buffering.

Other drivers and restraints analyzed in the detailed report include:

- Government Export Incentives Requiring Temperature Compliance

- Near-Shoring of North-American Protein Sourcing to Mercosur Suppliers

- Lack of Harmonized Regulatory Standards Across Borders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated transportation captured the largest slice of 2025 revenue at 55.69%, illustrating the dependence of the South America cold chain logistics market on trucking for long hauls. Yet refrigerated rail is registering a 5.54% CAGR to 2031, the strongest within the segment. Rumo Logistica's 1,000-km rail route from Mato Grosso to the Port of Santos trims transit time by 18 hours and cuts per-ton-kilometer emissions 65% for soy derivatives, underscoring environmental and cost advantages. Road remains dominant for last-mile legs under 300 km, but diesel price volatility is nudging shippers toward natural-gas trucks in low-emission zones. Sea-based refrigerated transport holds steady on established routes, while air remains a niche for premium seafood and urgent biologics.

Value-added services are rising as operators seek margin diversity. Blast freezing, kitting, and temperature-controlled e-commerce fulfillment often command 20%-30% premiums over commodity storage. As e-grocery penetration deepens, micro-fulfillment nodes embedded inside urban warehouses are proliferating, requiring high-velocity pick-and-pack systems and real-time temperature monitoring. The South America cold chain logistics market size attributable to such services is projected to expand faster than headline growth, underpinned by shifting consumer behavior and retailer demand for same-day replenishment.

The South America Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), by Temperature Type (Chilled, Frozen, Ambient, Deep-Frozen), by Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood, Dairy & Frozen Desserts, and More), by Country (Brazil, Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Emergent Cold LatAm

- Solistica (Traxion)

- SuperFrio Logistica Frigorificada

- Friozem Armazens Frigorificados

- DHL Supply Chain

- Maersk (Sealand Americas Cold Chain)

- Americold Realty Trust

- JSL Transportadora (Fadel Logistica Fria)

- Serbom

- TPC Logistica

- Arfrio

- Ransa Comercial S.A.

- Iceport

- Kuehne+Nagel

- CMA CGM (incl. CEVA Logistics)

- Refrio Armazens Gerais Frigorificos

- IceStar

- Brado Logistica S.A.

- AGUNSA

- CAP Logistica Frigorificada

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Urban Demand for Processed and Frozen Food Products

- 4.2.2 Expansion of Temperature-Controlled Distribution Networks for Vaccines and Biologics

- 4.2.3 Government Export Incentive Schemes Emphasizing Cold Chain Compliance

- 4.2.4 Shift Toward Nearshoring North American Protein Sourcing to Mercosur-Based Suppliers

- 4.2.5 Growth of E-Grocery Micro-Fulfillment Operations in Tier-2 Brazilian Cities

- 4.2.6 Rising Exports of Meat, Poultry, And Seafood from Mercosur Countries

- 4.3 Market Restraints

- 4.3.1 Limited Refrigerated Road Infrastructure and Rising Energy Costs

- 4.3.2 Lack of Harmonized Regulatory Standards Across Borders

- 4.3.3 Shortage of Skilled Personnel in Industrial Refrigeration Operations

- 4.3.4 Elevated Electricity Tariffs and Recurring Power Reliability Issues

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Application

- 5.3.1 Fruits & Vegetables

- 5.3.2 Meat & Poultry

- 5.3.3 Fish & Seafood

- 5.3.4 Dairy & Frozen Desserts

- 5.3.5 Bakery & Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals & Biologics

- 5.3.8 Vaccines & Clinical Trial Materials

- 5.3.9 Chemicals & Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Chile

- 5.4.4 Peru

- 5.4.5 Colombia

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Emergent Cold LatAm

- 6.4.2 Solistica (Traxion)

- 6.4.3 SuperFrio Logistica Frigorificada

- 6.4.4 Friozem Armazens Frigorificados

- 6.4.5 DHL Supply Chain

- 6.4.6 Maersk (Sealand Americas Cold Chain)

- 6.4.7 Americold Realty Trust

- 6.4.8 JSL Transportadora (Fadel Logistica Fria)

- 6.4.9 Serbom

- 6.4.10 TPC Logistica

- 6.4.11 Arfrio

- 6.4.12 Ransa Comercial S.A.

- 6.4.13 Iceport

- 6.4.14 Kuehne+Nagel

- 6.4.15 CMA CGM (incl. CEVA Logistics)

- 6.4.16 Refrio Armazens Gerais Frigorificos

- 6.4.17 IceStar

- 6.4.18 Brado Logistica S.A.

- 6.4.19 AGUNSA

- 6.4.20 CAP Logistica Frigorificada

7 Market Opportunities & Future Outlook

城市低溫運輸物流市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類)都市區低溫運輸配送市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類)

城市低溫運輸物流市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類)都市區低溫運輸配送市場預測至2034年-全球分析(依溫度等級、運輸方式、服務類型、包裝類型、最終用戶及地區分類) 低溫運輸物流市場:依服務類型、溫度區域和最終用途分類-2026-2032年全球市場預測低溫運輸市場:2026-2032年全球市場預測(依溫度範圍、設備類型、服務模式、最終用戶及通路分類)

低溫運輸物流市場:依服務類型、溫度區域和最終用途分類-2026-2032年全球市場預測低溫運輸市場:2026-2032年全球市場預測(依溫度範圍、設備類型、服務模式、最終用戶及通路分類) 2026年全球低溫運輸市場報告2026年全球冷凍食品物流市場報告2026年全球低溫運輸物流市場報告RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年

2026年全球低溫運輸市場報告2026年全球冷凍食品物流市場報告2026年全球低溫運輸物流市場報告RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年 2026-2030年全球低溫運輸市場

2026-2030年全球低溫運輸市場 低溫運輸市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、解決方案、最終用戶分類

低溫運輸市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、解決方案、最終用戶分類