|

市場調查報告書

商品編碼

2044134

北美金屬罐市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

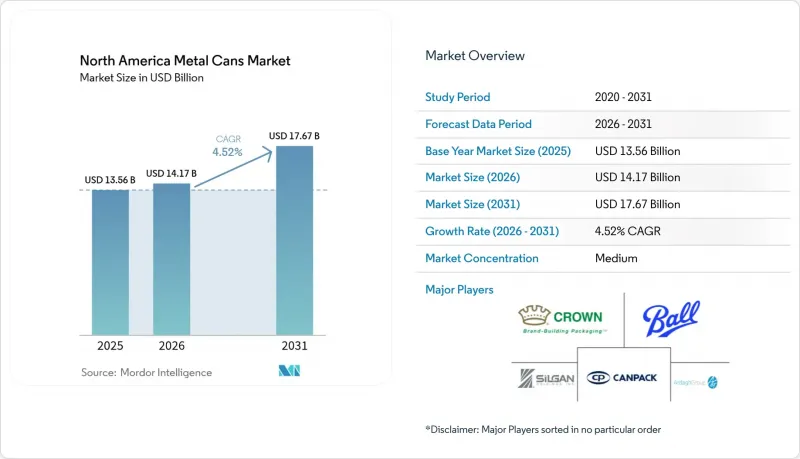

預計北美金屬罐市場規模將從 2025 年的 135.6 億美元和 2026 年的 141.7 億美元成長到 2031 年的 176.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.52%。

原生塑膠生產者延伸責任制(EPR)費用的不斷上漲、馬口鐵關稅導致的進口成本增加,以及品牌所有者的優質化策略,正推動包裝需求持續轉向可無限循環利用的鋁罐。輕量化技術已將355毫升飲料罐的重量降低至12.2克,提高了加工商的利潤率。墨西哥近岸產能的擴大,使訂單到交貨的週期縮短了40%。阿拉巴馬州和美國東南部高純度罐鋼產量的增加,使每噸運輸成本降低了40至50美元,從而為市場抵禦倫敦金屬交易所(LME)價格波動提供了緩衝。採用一體成型氣霧罐的個人護理品牌和轉型採用先進355毫升規格的即飲酒精飲料生產商,正在帶來高利潤的銷售成長,抵消了軟性飲料和保存食品的銷量下滑。

北美金屬罐市場趨勢與洞察

該地區飲料業的成長

2025年,北美灌裝商消耗了約1,200億個鋁罐。這主要得益於能量飲料、硬蘇打水和精釀啤酒的成長,抵消了碳酸飲料1.2%的下滑。在墨西哥,2024年啤酒產量增加了4.3%,12億美元的擴建工程使年產能增加了2,500萬百公升,國內包裝中有36%轉向罐裝。在美國,2024年即飲雞尾酒的零售量成長了18%,其中高階價位的鋁罐裝佔比高達82%。加拿大的情況則有所不同,受可重複使用玻璃容器的獎勵影響,2024年加拿大飲料製造業銷售額下降了1.7%。跨境供應鏈重組導致墨西哥對美國的罐裝出口增加了12%,而國內產能運轉率維持在88%左右。

過渡到可無限循環利用的鋁製包裝

迄今為止生產的鋁中,75%仍在繼續使用,這反映了閉合迴路的優勢。加州參議院第54號法案規定,到2032年,再生材料的使用比例必須達到65%。奧勒岡州擴大的押金返還計畫預計到2026年將達到82%的回收率,將使原生材料和再生材料之間的價格差距縮小38%。百事可樂和摩森康勝承諾到2027年,將在部分產品線中推出100%再生鋁罐,每年可減少18萬噸廢鋁需求。這些規定進一步增強了鋁相對於聚對苯二甲酸乙二醇酯(PET,回收率僅9%)和軟包裝袋(尚未建立商業性回收途徑)的優勢。

PET和軟包裝袋在食品飲料領域的普及

到2024年,聚對苯二甲酸乙二醇酯(PET)瓶和軟包裝袋將佔據北美果汁和乳製品包裝市場22%的佔有率,這將蠶食金屬罐在常溫保存食品領域的市場佔有率,因為透明度和可重複密封性對食品包裝至關重要。由於PET包裝的單位成本最多可降低30%,Ocean Spray和Tropicana已將其高達20%的無菌填充產品從鋼罐轉向PET包裝。軟包裝袋比硬罐輕40-50%,體積小60%,品牌商已利用軟包裝袋在2024年達到即食食品市場18%的佔有率。在墨西哥果汁市場,紙盒和PET包裝袋的總合佔有率已達到68%,顯示市場正在發生更大的轉變。加工商正在透過減輕重量和採用數位印刷來應對這一變化,但這些措施旨在節省成本,並未解決消費者對包裝的根本偏好。

細分市場分析

到2025年,鋁將佔據北美金屬罐市場79.76%的佔有率,超過鋼鐵,這主要得益於生產者延伸責任制(EPR)法規對閉合迴路可回收性的評估。在北美金屬罐市場,鋁製應用市場預計將以4.93%的複合年成長率成長,而鋼鐵市場預計僅成長3.12%。 2025年,232條款關稅翻倍將使進口馬口鐵的成本每噸增加150至200美元,這將擠壓鋼鐵罐的利潤空間,並進一步鞏固鋁的成本優勢。

諾貝麗斯和波爾公司總合增產90萬噸製罐用鋼板,將增強國內供應,並進一步降低運輸成本。雖然鋼罐對於蒸餾殺菌的食品、油漆和工業化學品仍然至關重要,但隨著軟包裝袋逐漸蠶食三片式鋼罐的市場佔有率,預計到2025年,鋼罐的市場佔有率將從20.24%下降。不同地區的材料偏好也有差異。墨西哥28%的鋼罐市場佔有率反映了當地馬口鐵的供應情況,而美國的市場佔有率已縮減至18%。

預計到2025年,兩片式拉伸壓製罐將佔據61.32%的市場佔有率,這主要得益於大規模生產的飲料市場對無縫罐壁和輕量化設計的需求。同時,具有防篡改功能、外觀高階且比三片式罐輕15%的一體式氣霧罐預計將以5.07%的複合年成長率實現最高成長。三片式鋼罐目前仍用於油漆和湯品領域,但由於軟包裝袋的興起,其成長速度已放緩至3.21%。

衝擊擠出機能夠生產無側縫的整體式註塑件,但高達 800 萬至 1200 萬美元的模具成本阻礙了小規模新進入者的步伐。對於希望在飲料市場盈利的加工商而言,將傳統的三片式生產線改造為拉拔鐵模是一種過渡措施。隨著個人護理品牌對設計柔軟性的需求不斷成長,預計到 2031 年,整體式射出成型件的市佔率將超過 12%。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 該地區飲料業的成長

- 過渡到可無限循環利用的鋁製包裝

- 罐裝葡萄酒和雞尾酒(即飲型)的優質化

- 美國高純度鋼板製造廠擴建(用於罐頭生產)

- 店內消費限制正在加速多包裝外帶的普及。

- 品牌所有者要求基於區塊鏈的可追溯性。

- 市場限制因素

- PET和軟包裝袋在食品飲料領域的普及

- 鋁捲和鋼捲價格波動劇烈

- 一次性罐裝飲料面臨的挑戰,以及有關填充和重複使用的法律法規的增加。

- 車身製造商和D&I生產線設備的供應瓶頸

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場規模與成長預測

- 依材料類型

- 鋁

- 鋼

- 透過可結構

- 2 件

- 3 件

- 單體氣霧劑

- 按生產能力和規模

- 50毫升或以下

- 250~500ml

- 500~1,000ml

- 1000毫升或更多

- 透過製造程序

- 拉伸和軋延(D&I)

- 拉動和再拉動(DRD)

- 衝擊擠壓

- 按最終用戶行業分類

- 食物

- 飲料

- 個人護理和化妝品

- 製藥

- 油漆和工業化學品

- 汽車用液體和潤滑劑

- 其他

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ball Corporation

- Crown Holdings, Inc.

- Silgan Holdings Inc.

- Ardagh Group SA

- CAN-PACK SA

- Mauser Packaging Solutions Holding Company

- Envases Universales de Mexico, SA de CV

- Trivium Packaging BV

- Tecnocap SpA

- DS Containers Inc.

- CCL Industries Inc.

- Independent Can Company

- Allstate Can Corporation

- Sonoco Products Company

- BWAY Corporation

- Trinity Packaging Supply, LLC

- O.Berk Company, LLC

- Peerless Beverage Packaging LLC

- Consolidated Container Company LLC

- Pacific Coast Producers Inc.

第7章 市場機會與未來展望

The North America metal cans market size is projected to expand from USD 13.56 billion in 2025 and USD 14.17 billion in 2026 to USD 17.67 billion by 2031, registering a CAGR of 4.52% between 2026 to 2031.

Rising extended-producer-responsibility fees on virgin plastics, tariff-driven import costs for tinplate, and brand owners' premiumization strategies continue to redirect packaging demand toward infinitely recyclable aluminum cans. Converter margins improved after lightweighting trimmed 355-milliliter beverage-can weights to 12.2 grams, while nearshored capacity in Mexico shortened order-to-delivery cycles by 40%. High-purity can-sheet expansions in Alabama and the southeastern United States reduce freight outlays by USD 40-50 per tonne and cushion the market against London Metal Exchange price swings. Personal-care brands embracing monobloc aerosols and ready-to-drink alcohol producers shifting to sleek 355-milliliter profiles create incremental high-margin volume that offsets soft beverages and shelf-stable food declines.

North America Metal Cans Market Trends and Insights

Growing Beverage Industry in the Region

North American fillers consumed nearly 120 billion aluminum cans in 2025 as energy drinks, hard seltzers, and craft beer offset a 1.2% slide in carbonated soft drinks. Mexico's beer output rose 4.3% in 2024 after a USD 1.2 billion expansion lifted annual capacity by 25 million hectoliters and shifted 36% of domestic packaging into cans. Ready-to-drink cocktails in the United States posted 18% retail-sales growth in 2024, with aluminum capturing 82% of volume at premium price points. Canada diverged, with beverage manufacturing sales contracting 1.7% in 2024 amid refillable-glass incentives. Cross-border supply realignment saw Mexican can exports to the United States climb 12%, while domestic U.S. capacity utilization hovered near 88%.

Shift Toward Infinitely Recyclable Aluminum Packaging

Seventy-five percent of all aluminum ever produced remains in use, underpinning a closed-loop advantage as California's Senate Bill 54 mandates 65% recycled content by 2032. Oregon's expanded deposit-return system is projected to lift redemption rates to 82% by 2026, compressing the virgin-to-recycled price spread by 38%. PepsiCo and Molson Coors pledged 100% recycled-content cans for select lines by 2027, redirecting 180,000 tonnes of annual scrap demand. These mandates elevate aluminum against polyethylene terephthalate's 9% recycling rate and against flexible pouches that lack commercial reclamation streams.

Proliferation of PET and Flexible Pouches in Food and Drink

Polyethylene terephthalate bottles and flexible pouches held 22% of North American juice and dairy packaging in 2024, eroding metal-can share in shelf-stable meals where transparency and resealability resonate. Ocean Spray and Tropicana each shifted up to 20% of their aseptic volume from steel cans to PET, citing unit costs up to 30% lower. Flexible pouches captured 18% of ready-to-eat meal volume in 2024 after brands leveraged 40-50% lighter weights and 60% smaller cube sizes compared to rigid cans. Mexican juice segments show even higher displacement, as cartons and PET hold a combined 68% share. Converters answer with lightweighting and digital printing, yet these actions address cost rather than core format preference.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization of Canned Wines and Cocktails (RTDs)

- Expansion of High-Purity Can-Sheet Mills in the United States

- Volatile Aluminum and Steel Coil Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum captured 79.76% of North America's metal can market share in 2025, outpacing steel as extended producer responsibility rules reward closed-loop recyclability. The North America metal cans market for aluminum applications is forecast to expand at a 4.93% CAGR, whereas the steel market grows at only 3.12%. Tariff hikes that doubled Section 232 duties in 2025 inflated imported tinplate costs by USD 150-200 per tonne, squeezing steel-can margins and reinforcing aluminum's cost edge.

Novelis's and Ball's combined 900,000-tonne can-sheet additions fortify domestic supply and further lower freight outlays. Steel remains indispensable for retort-sterilized foods, paints, and industrial chemicals, but its 20.24% share in 2025 is expected to slip as flexible pouches chip away at three-piece formats. Material preferences also diverge geographically: Mexico's 28% steel-can share reflects local tinplate availability, while the United States' share contracted to 18%.

Two-piece drawn-and-ironed cans delivered a 61.32% share in 2025, serving high-volume beverages that demand seamless walls and low unit weights. Monobloc aerosols, however, exhibit the fastest 5.07% CAGR, offering tamper evidence, premium aesthetics, and 15% lighter weight than three-piece counterparts. Three-piece steel cans persist in paint and chunky soups, yet flexible pouches erode their growth to 3.21%.

Impact-extrusion presses enable monobloc geometry without side seams, but USD 8-12 million tooling bills curb smaller entrants. Retrofitting older three-piece lines with drawn-and-ironed tooling is an interim step for converters chasing beverage economics. As personal-care brands heighten demand for design flexibility, monobloc share is set to climb above 12% by 2031.

The North American Metal Cans Market Report is Segmented by Material Type (Aluminium, and Steel), Can Structure (Two-Piece, Three-Piece, and Monobloc Aerosol), Capacity/Size (Less Than 50ML, 250-500 Ml, and More), Manufacturing Process (Drawn and Ironed, Drawn and Redrawn, and Impact Extrusion), and End-User Industry (Food, Beverage, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ball Corporation

- Crown Holdings, Inc.

- Silgan Holdings Inc.

- Ardagh Group S.A.

- CAN-PACK S.A.

- Mauser Packaging Solutions Holding Company

- Envases Universales de Mexico, S.A. de C.V.

- Trivium Packaging B.V.

- Tecnocap S.p.A.

- DS Containers Inc.

- CCL Industries Inc.

- Independent Can Company

- Allstate Can Corporation

- Sonoco Products Company

- BWAY Corporation

- Trinity Packaging Supply, LLC

- O.Berk Company, LLC

- Peerless Beverage Packaging LLC

- Consolidated Container Company LLC

- Pacific Coast Producers Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Beverage Industry in the Region

- 4.2.2 Shift Toward Infinitely-Recyclable Aluminium Packaging

- 4.2.3 Premiumisation of Canned Wines and Cocktails (RTDs)

- 4.2.4 Expansion of High-Purity Can-Sheet Mills in the United States

- 4.2.5 On-Premise Restrictions Accelerating Take-Home Multi-Packs

- 4.2.6 Blockchain-Enabled Traceability Demands From Brand Owners

- 4.3 Market Restraints

- 4.3.1 Proliferation of PET and Flexible Pouches in Food and Drink

- 4.3.2 Volatile Aluminium and Steel Coil Prices

- 4.3.3 Rising Refill-and-Reuse Legislation Challenging Single-Use Cans

- 4.3.4 Supply Bottlenecks in Body-Maker and D and I Line Equipment

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Can Structure

- 5.2.1 Two-Piece

- 5.2.2 Three-Piece

- 5.2.3 Monobloc Aerosol

- 5.3 By Capacity / Size

- 5.3.1 Less than 50 ml

- 5.3.2 250-500 ml

- 5.3.3 500-1,000 ml

- 5.3.4 More than 1,000 ml

- 5.4 By Manufacturing Process

- 5.4.1 Drawn and Ironed (D and I)

- 5.4.2 Drawn and Redrawn (DRD)

- 5.4.3 Impact Extrusion

- 5.5 By End-User Industry

- 5.5.1 Food

- 5.5.2 Beverage

- 5.5.3 Personal Care and Cosmetics

- 5.5.4 Pharmaceuticals

- 5.5.5 Paints and Industrial Chemicals

- 5.5.6 Automotive Fluids and Lubricants

- 5.5.7 Other End-User Industries

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ball Corporation

- 6.4.2 Crown Holdings, Inc.

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 Ardagh Group S.A.

- 6.4.5 CAN-PACK S.A.

- 6.4.6 Mauser Packaging Solutions Holding Company

- 6.4.7 Envases Universales de Mexico, S.A. de C.V.

- 6.4.8 Trivium Packaging B.V.

- 6.4.9 Tecnocap S.p.A.

- 6.4.10 DS Containers Inc.

- 6.4.11 CCL Industries Inc.

- 6.4.12 Independent Can Company

- 6.4.13 Allstate Can Corporation

- 6.4.14 Sonoco Products Company

- 6.4.15 BWAY Corporation

- 6.4.16 Trinity Packaging Supply, LLC

- 6.4.17 O.Berk Company, LLC

- 6.4.18 Peerless Beverage Packaging LLC

- 6.4.19 Consolidated Container Company LLC

- 6.4.20 Pacific Coast Producers Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

金屬罐和玻璃瓶市場:2026-2032年全球市場預測(按包裝類型、材料、蓋子類型、容量、最終用戶和分銷管道分類)

金屬罐和玻璃瓶市場:2026-2032年全球市場預測(按包裝類型、材料、蓋子類型、容量、最終用戶和分銷管道分類) 金屬罐市場報告:趨勢、預測及競爭分析(至2035年)

金屬罐市場報告:趨勢、預測及競爭分析(至2035年) 金屬罐市場規模、佔有率、趨勢和預測:按材料類型、製造方法、罐型和地區分類,2026-2034年金屬罐、桶、鼓和桶市場:依材質、產品類型、容量、終端用戶產業和銷售管道分類-2026-2032年全球市場預測

金屬罐市場規模、佔有率、趨勢和預測:按材料類型、製造方法、罐型和地區分類,2026-2034年金屬罐、桶、鼓和桶市場:依材質、產品類型、容量、終端用戶產業和銷售管道分類-2026-2032年全球市場預測 金屬罐市場規模、佔有率和趨勢分析報告:按材料、產品、蓋類型、應用、地區和細分市場預測(2026-2033 年)

金屬罐市場規模、佔有率和趨勢分析報告:按材料、產品、蓋類型、應用、地區和細分市場預測(2026-2033 年) 美國金屬罐:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國金屬罐:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球金屬桶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球特種馬口鐵罐罐市場(按產品類型、材料、塗層和最終用途分類)預測(2026-2032)

全球金屬桶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球特種馬口鐵罐罐市場(按產品類型、材料、塗層和最終用途分類)預測(2026-2032) 金屬食品飲料罐市場規模、佔有率及成長分析(依材料、罐型、應用、飲料類型、食品類型及地區分類)-2026-2033年產業預測金屬罐市場-2025-2030年預測

金屬食品飲料罐市場規模、佔有率及成長分析(依材料、罐型、應用、飲料類型、食品類型及地區分類)-2026-2033年產業預測金屬罐市場-2025-2030年預測