|

市場調查報告書

商品編碼

1940740

美國金屬罐:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States (US) Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

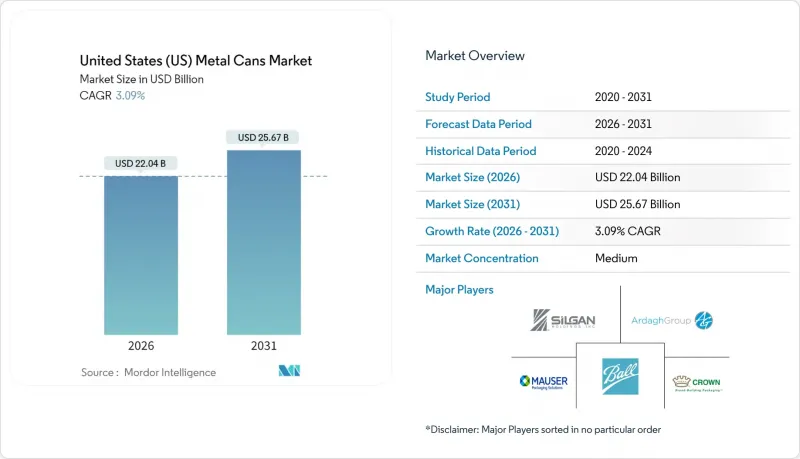

美國金屬罐市場預計將從 2025 年的 213.8 億美元成長到 2026 年的 220.4 億美元,預計到 2031 年將達到 256.7 億美元,2026 年至 2031 年的複合年成長率為 3.09%。

消費者對可無限循環利用的鋁材日益成長的偏好,以及品牌所有者的永續性舉措,使得市場需求持續超過國內供應,工廠使用率也接近滿負荷運轉,即便墨西哥空罐進口被徵收25%的關稅。飲料、醫藥和高階個人護理品牌正不斷轉向金屬包裝,以滿足耐用性和循環經濟的目標。同時,輕量化技術正在降低材料消耗和運輸成本。主要製造商的垂直整合策略確保了罐坯供應,並強化了競爭壁壘,但原料價格波動和軟包裝技術的創新仍然是潛在的威脅。總體而言,美國金屬罐市場受益於強勁的終端用戶需求、高價值細分市場穩定的定價能力以及有利於單一材料包裝形式的監管政策。

美國金屬罐市場趨勢與洞察

推廣高回收率的替代包裝材料

金屬罐平均含有75%的再生材料,並且可以無限次重熔而不會劣化,與平均含有35%再生樹脂的寶特瓶相比,在成本和永續性具有明顯的優勢。由於市政回收項目每回收一噸鋁可產生約1200美元的收入,而PET瓶僅200美元,因此地方政府有獎勵優先建造金屬罐回收基礎設施。品牌所有者的強制性要求,例如可口可樂35-40%的再生材料含量目標,確保了多年的採購量,即使在經濟低迷時期也能保證最低需求。聯邦採購標準設定了再生材料含量的閾值,確保了機構需求的持續成長。隨著各州生產者延伸責任制(EPR)附加稅對複合材料層壓產品施加壓力,金屬罐在常溫保存食品和特種飲料領域正獲得更大的市場佔有率。

精釀啤酒和即飲飲料的快速成長正在重塑需求模式

全美超過9,000家精釀啤酒廠青睞鋁罐,因為它能有效遮光、保持碳酸化,並能呈現鮮豔的圖案,進而強化品牌故事。即飲型(RTD)酒精飲料是成長最快的細分市場,推動了對12盎司和8.4盎司規格的精製包裝的需求,這些規格佔據了高階貨架位置。硬蘇打水生產商為防止串味而支付的先進阻隔塗層費用比普通包裝高出15%至20%。這一趨勢正在促進區域性聯合包裝網路的發展,縮短產品從生產到商店的周期,並為靈活、快速換型的罐裝生產線創造了機會。像Independent Can Company這樣的專業供應商正在擴大其西海岸的生產能力,以滿足小批量訂單的需求,這表明市場對本地飲料趨勢的應對力迅速。

替代包裝形式的激增加劇了競爭壓力。

採用高阻隔薄膜製成的立式袋比同類罐裝產品輕60-70%,並可設有透明窗口展示產品新鮮度,從而吸引千禧世代消費者。輕質寶特瓶的重量持續下降,降低了單位成本,加劇了其與罐裝產品在對價格敏感的飲料品類中的價格競爭。在某些湯類產品中,內襯鋁層的紙盒包裝比金屬罐價格低15-25%,吸引了注重成本的食品加工商。材料科學的快速創新和快速更換包裝圖案的能力,使軟包裝在行銷方面更具優勢。儘管面臨這些挑戰,在需要蒸餾、維持碳酸氣含量和延長保存期限的品類中,罐裝產品仍佔據主導地位。

細分市場分析

截至2025年,鋁罐占美國金屬罐市場70.48%的佔有率,這主要得益於飲料行業的強勁需求,該行業對鋁罐的耐腐蝕性和高階展示效果有較高要求。然而,鋼罐在大包裝食品和寵物食品領域正重新獲得市場青睞,其三點焊接的罐體結構不僅成本更低,而且能夠承受蒸餾滅菌製程。

輕量化技術使每罐鋁材用量減少了13%,抵銷了金屬價格的波動。同時,馬口鐵罐製造商正在引入更薄的鋼板,並採用改良的有機溶劑塗層,以減輕鋼製容器的重量。區域原料採購模式也影響材料的選擇:鋁廠集中在南部和中西部回收槽源附近,而鋼罐生產線則位於與鋼鐵廠配套的工廠附近。這些位置優勢是現有企業和新參與企業選擇生產地點的決定性因素。

到2025年,雙板拉拔熨燙罐將占美國金屬罐市場規模的53.78%,這主要得益於每分鐘超過2300罐的高速生產線以及其優異的軸向強度,尤其適用於碳酸飲料。同時,受醫藥噴霧劑和皮膚泡沫劑需求的推動,一體式氣霧劑容器將以4.68%的複合年成長率推動市場結構性成長。

三片式焊接罐在散裝食品、咖啡和工業化學品領域仍然佔據重要地位,因為其高度調節的便利性和成本效益超過了無縫結構的優勢。罐體製造精度的不斷提高使得全表面圖案和霧面飾面成為可能,從而拓展了精釀啤酒和特殊能量飲料的優質化機會。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場促進因素

- 金屬包裝回收率高

- 罐頭食品方便快捷,保存期限長。

- 精釀啤酒和即飲飲料的蓬勃發展帶動了罐裝飲料需求的成長。

- 監理機關推動永續單一材料包裝

- 透過輕量化創新降低單位罐體成本

- 品牌所有者的循環包裝舉措確保了對罐裝食品的需求。

- 市場限制

- 推廣替代包裝形式(PET、軟包裝袋)

- 鋁和鋼鐵等原料價格波動;

- 對雙酚A替代品過渡的擔憂影響了消費者信心

- 由於國內產能限制,罐用鋼板供應面臨風險。

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

- 監管環境

- 技術展望

第5章 市場規模與成長預測

- 依材料類型

- 鋁

- 鋼材

- 透過可結構

- 兩件套

- 三件套

- 單體氣霧劑

- 按容量/尺寸

- ≤250毫升

- 250-500毫升

- 500~1,000 ml

- 1000毫升或更多

- 透過製造程序

- 拉伸和軋延(DandI)

- 再拉伸(DRD)

- 衝擊擠壓

- 按最終用戶行業分類

- 食物

- 飲料

- 個人護理和化妝品

- 製藥

- 油漆和工業化學品

- 汽車用液體/潤滑油

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Crown Holdings, Inc.

- Ball Corporation

- Silgan Holdings Inc.

- Mauser Packaging Solutions Holding Company

- Ardagh Metal Packaging SA

- DS Containers, LLC

- CCL Industries Inc.(CCL Container division)

- Independent Can Company

- Tecnocap SpA

- CAN-PACK SA

- Allstate Can Corporation

- Envases Universales Group

- Trivium Packaging BV

- Greif, Inc.

- Toyo Seikan Group Holdings, Ltd.

- Montebello Packaging Inc.

- Crown Cork and Seal USA, Inc.

- Metal Container Corporation

第7章 市場機會與未來展望

The United States metal cans market is expected to grow from USD 21.38 billion in 2025 to USD 22.04 billion in 2026 and is forecast to reach USD 25.67 billion by 2031 at 3.09% CAGR over 2026-2031.

Growing preference for infinitely recyclable aluminum, combined with brand-owner sustainability pledges, keeps demand ahead of domestic supply and sustains near-maximum plant utilization despite a 25% tariff on empty cans imported from Mexico. Beverage, pharmaceutical, and premium personal-care brands continue to migrate to metal containers to meet durability and circular-economy goals, while lightweighting technology reduces material consumption and shipping costs. Vertical integration strategies by leading producers secure can-sheet supply and reinforce competitive barriers, yet input-price volatility and flexible packaging innovations remain persistent threats. Overall, the United States metal cans market benefits from strong end-use momentum, stable pricing power in high-value niches, and regulatory tailwinds favoring single-material packaging formats.

United States (US) Metal Cans Market Trends and Insights

High Recyclability Rates Drive Packaging Material Substitution

Metal cans contain 75% recycled content on average and can be remelted indefinitely without quality loss, giving them a clear cost and sustainability edge over PET bottles that contain 35% recycled resin on average. Municipal recycling programs earn about USD 1,200 per ton of recovered aluminum versus USD 200 for PET, incentivizing local governments to prioritize can collection infrastructure. Brand-owner mandates such as Coca-Cola's 35-40% recycled-content pledge lock in multiyear purchase volumes, guaranteeing baseline demand even during economic slowdowns. Federal procurement standards now specify recycled-content thresholds, ensuring ongoing institutional demand. As state extended producer-responsibility fees penalize complex laminates, metal cans gain additional market share in shelf-stable food and specialty beverage categories.

Craft-Beer and RTD Beverage Surge Reshapes Demand Patterns

More than 9,000 craft breweries nationwide prefer aluminum because it blocks light, maintains carbonation, and supports vibrant graphics that reinforce brand storytelling. Ready-to-drink alcoholic beverages are the fastest-growing subsegment, spurring demand for sleek 12 oz and 8.4 oz formats that command premium shelf positioning. Hard seltzer producers pay 15-20% above commodity pricing for advanced barrier coatings that avoid flavor pickup. The trend promotes regional co-packing networks to shorten product-to-shelf cycles, opening opportunities for flexible, quick-change can lines. Niche suppliers such as Independent Can Company expand West Coast capacity to meet small-batch orders, underscoring the market's responsiveness to localized beverage trends

Proliferation of Alternate Packaging Formats Intensifies Competitive Pressure

Stand-up pouches with high-barrier films weigh 60-70% less than comparable cans and enable transparent windows that showcase product freshness, appealing to millennial shoppers. Lightweight PET bottles continue to shed grams, lowering cost per unit and challenging cans on price in value-oriented beverage lines. Carton-based containers with aluminum layers undercut metal cans by 15-25% in certain soup categories, enticing cost-sensitive food processors. Rapid material-science innovation cycles and the speed of graphic changes give flexibles a marketing agility advantage. Despite these headwinds, cans maintain dominance where retort processing, carbonation retention, or long shelf life is essential.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates Accelerate Sustainable Packaging Adoption

- Lightweighting Innovations Transform Manufacturing Economics

- Raw Material Price Volatility Creates Supply-Chain Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum accounted for 70.48% of United States metal cans market share in 2025, driven by beverages that demand corrosion resistance and premium shelf appeal. Nevertheless, steel cans regain momentum in large-format foods and pet nutrition because three-piece welded bodies offer cost advantages and withstand retort temperatures.

Lightweighting has trimmed aluminum usage by 13% per can, offsetting metal-price volatility, while tinplate suppliers introduce thinner gauges with improved organosol coatings to reduce steel container weight. Geographic feedstock patterns also shape material choice: aluminum plants cluster near recycled-can streams in the South and Midwest, whereas steel can lines stay close to integrated mills. These locational advantages inform footprint decisions for both incumbent and new entrants.

Two-piece drawn-and-ironed cans captured 53.78% of United States metal cans market size in 2025 owing to high-speed lines that exceed 2,300 cans per minute and deliver superior axial strength for sparkling beverages. Monobloc aerosol bodies, however, lead structural growth at 4.68% CAGR, powered by pharmaceutical spray and dermal-foam demand.

Three-piece welded formats remain relevant in bulk foods, coffee, and industrial chemicals where easy height variation and cost efficiency outweigh seamless construction benefits. Continuous improvement in body maker precision has enabled full-panel graphics and matte finishes, expanding premiumization opportunities across craft beer and specialty energy drinks.

The United States Metal Cans Market Report is Segmented by Material Type (Aluminium, and Steel), Can Structure (Two-Piece, Three-Piece, Monobloc Aerosol), Capacity/Size (<=250 Ml, 250-500 Ml, 500-1, 000 Ml, >1, 000 Ml), Manufacturing Process (Drawn and Ironed, Drawn and Redrawn, Impact Extrusion), End-User Industry (Food, Beverage, Personal Care and Cosmetics and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Crown Holdings, Inc.

- Ball Corporation

- Silgan Holdings Inc.

- Mauser Packaging Solutions Holding Company

- Ardagh Metal Packaging S.A.

- DS Containers, LLC

- CCL Industries Inc. (CCL Container division)

- Independent Can Company

- Tecnocap S.p.A.

- CAN-PACK S.A.

- Allstate Can Corporation

- Envases Universales Group

- Trivium Packaging B.V.

- Greif, Inc.

- Toyo Seikan Group Holdings, Ltd.

- Montebello Packaging Inc.

- Crown Cork and Seal USA, Inc.

- Metal Container Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 High recyclability rates of metal packaging

- 4.1.2 Convenience and extended shelf life offered by canned foods

- 4.1.3 Craft-beer and RTD beverage boom boosting can demand

- 4.1.4 Regulatory push for sustainable, single-material packaging

- 4.1.5 Lightweighting innovations lowering per-unit can cost

- 4.1.6 Brand-owner circular-packaging pledges securing can volumes

- 4.2 Market Restraints

- 4.2.1 Proliferation of alternate packaging formats (PET, pouches)

- 4.2.2 Volatility in aluminum and steel input prices

- 4.2.3 BPA-substitute migration concerns affecting consumer trust

- 4.2.4 Domestic can-sheet capacity constraints creating supply risk

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 The Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Can Structure

- 5.2.1 Two-Piece

- 5.2.2 Three-Piece

- 5.2.3 Monobloc Aerosol

- 5.3 By Capacity / Size

- 5.3.1 <=250 ml

- 5.3.2 250-500 ml

- 5.3.3 500-1,000 ml

- 5.3.4 >1,000 ml

- 5.4 By Manufacturing Process

- 5.4.1 Drawn and Ironed (DandI)

- 5.4.2 Drawn and Redrawn (DRD)

- 5.4.3 Impact Extrusion

- 5.5 By End-User Industry

- 5.5.1 Food

- 5.5.2 Beverage

- 5.5.3 Personal Care and Cosmetics

- 5.5.4 Pharmaceuticals

- 5.5.5 Paints and Industrial Chemicals

- 5.5.6 Automotive Fluids and Lubricants

- 5.5.7 Other End-User Industry

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Crown Holdings, Inc.

- 6.4.2 Ball Corporation

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 Mauser Packaging Solutions Holding Company

- 6.4.5 Ardagh Metal Packaging S.A.

- 6.4.6 DS Containers, LLC

- 6.4.7 CCL Industries Inc. (CCL Container division)

- 6.4.8 Independent Can Company

- 6.4.9 Tecnocap S.p.A.

- 6.4.10 CAN-PACK S.A.

- 6.4.11 Allstate Can Corporation

- 6.4.12 Envases Universales Group

- 6.4.13 Trivium Packaging B.V.

- 6.4.14 Greif, Inc.

- 6.4.15 Toyo Seikan Group Holdings, Ltd.

- 6.4.16 Montebello Packaging Inc.

- 6.4.17 Crown Cork and Seal USA, Inc.

- 6.4.18 Metal Container Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

金屬罐和玻璃瓶市場:2026-2032年全球市場預測(按包裝類型、材料、蓋子類型、容量、最終用戶和分銷管道分類)

金屬罐和玻璃瓶市場:2026-2032年全球市場預測(按包裝類型、材料、蓋子類型、容量、最終用戶和分銷管道分類) 金屬罐市場報告:趨勢、預測及競爭分析(至2035年)

金屬罐市場報告:趨勢、預測及競爭分析(至2035年) 金屬罐市場規模、佔有率、趨勢和預測:按材料類型、製造方法、罐型和地區分類,2026-2034年金屬罐、桶、鼓和桶市場:依材質、產品類型、容量、終端用戶產業和銷售管道分類-2026-2032年全球市場預測

金屬罐市場規模、佔有率、趨勢和預測:按材料類型、製造方法、罐型和地區分類,2026-2034年金屬罐、桶、鼓和桶市場:依材質、產品類型、容量、終端用戶產業和銷售管道分類-2026-2032年全球市場預測 北美金屬罐市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美金屬罐市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 金屬罐市場規模、佔有率和趨勢分析報告:按材料、產品、蓋類型、應用、地區和細分市場預測(2026-2033 年)

金屬罐市場規模、佔有率和趨勢分析報告:按材料、產品、蓋類型、應用、地區和細分市場預測(2026-2033 年) 全球金屬桶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球特種馬口鐵罐罐市場(按產品類型、材料、塗層和最終用途分類)預測(2026-2032)

全球金屬桶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球特種馬口鐵罐罐市場(按產品類型、材料、塗層和最終用途分類)預測(2026-2032) 金屬食品飲料罐市場規模、佔有率及成長分析(依材料、罐型、應用、飲料類型、食品類型及地區分類)-2026-2033年產業預測金屬罐市場-2025-2030年預測

金屬食品飲料罐市場規模、佔有率及成長分析(依材料、罐型、應用、飲料類型、食品類型及地區分類)-2026-2033年產業預測金屬罐市場-2025-2030年預測