|

市場調查報告書

商品編碼

2044116

甲苯:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031)Toluene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

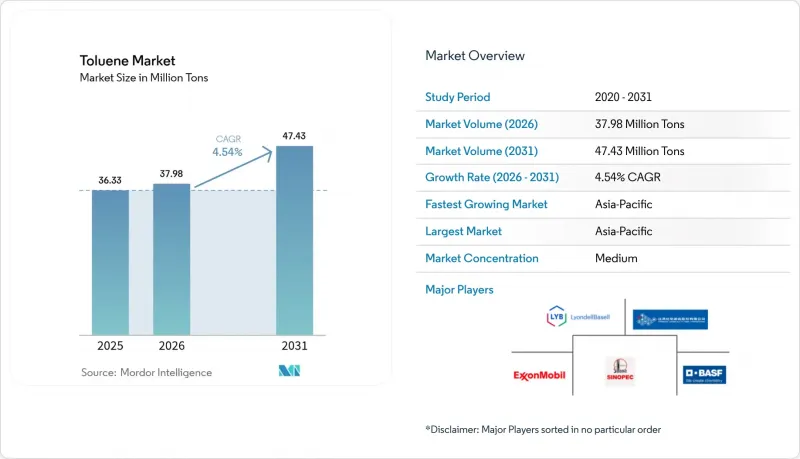

預計甲苯市場將從 2025 年的 3,633 萬噸成長到 2026 年的 3,798 萬噸,然後在 2031 年達到 4,743 萬噸,2026 年至 2031 年的複合年成長率為 4.54%。

需求成長反映了這種化學品作為芳香烴的多功能性,它可用於生產苯、二甲苯和甲苯二異氰酸酯 (TDI) 等下游產品,這些產品供應給從建築到電子等眾多行業。旨在減少排放的監管措施正在加速製程改進,從而提高能源效率並減少揮發性有機化合物 (VOC) 的排放,進而增強企業的長期競爭力。這些趨勢共同凸顯了向一體化、以永續性發展為中心的供應鏈的轉變,這種轉變有利於那些能夠在成本領先優勢和清潔製程技術投資之間取得平衡的生產商。

全球甲苯市場趨勢與洞察

東協地區聚氨酯泡棉的強勁成長正在推動TDI的消費。

家具、寢具和汽車座椅用軟泡材料的產量激增,推動了馬來西亞、越南和泰國對甲苯二異氰酸酯(TDI)的需求成長。區域內對甲苯市場的投資,例如馬來西亞國家石油公司(Petronas)的RAPID綜合設施,正在擴大當地獲取甲苯基中間體的管道,並降低對進口的依賴。生產商正在提高原油到化學品的轉化率,以擴大芳香族化合物的產量,而甲苯則被定位為區域聚氨酯供應的核心成分。

印度和中國對辛烷值等級的限制將提振對重整油衍生甲苯的需求。

印度的第六階段排放標準(Bharat Stage VI)和中國的國六排放標準(China 6)對爆震抑制組分的要求更高,促使煉油廠增加富含甲苯的重整油的產量。努馬裡加爾煉油廠的產量提高至每年900萬噸,因而增強了印度國內的甲苯供應;同時,中國的綜合煉油廠也正在向汽油調和池供應更多的芳烴化合物。這些措施吸收了原本會導致供應過剩的額外甲苯供應,從而為煉油廠創造了更大的利潤空間,並推高了亞太地區溶劑級甲苯的價格。

加強歐盟REACH法規中關於芳香族化合物的揮發性有機化合物(VOC)規定

歐盟提高了揮發性有機化合物(VOC)的閾值,並敦促油漆、塗料和黏合劑生產商修改配方,以消除芳香族溶劑。 [2] 由於需要投資排放控制設備以及改用更昂貴的低VOC載體,因此合規成本不斷增加。跨國配方生產商正在精簡產品線以符合歐盟和英國的法規,這進一步加劇了甲苯市場的分散化,並減緩了消費者應用領域對甲苯的區域需求。

細分市場分析

到2025年,苯和二甲苯將佔衍生性商品消費量的37.70%,凸顯其在聚酯、尼龍和特種化學品供應鏈中的穩固地位。這一主導地位確保了改質劑和芳烴萃取劑的加工量穩定,即使利潤率有所波動。同時,與TDI相關的甲苯市場規模預計將在2026年至2031年間以5.37%的複合年成長率成長,反映出新興經濟體對家具和床上用品的強勁需求。

苯甲醛、苯甲酸、TNT及其一些特殊衍生物各有其特定的應用領域,但即使加起來,它們在整個甲苯市場中所佔的佔有率也相對較小。一體化生產商透過平衡產品組合併利用規模經濟,為客戶提供通用和特種產品。

本甲苯市場報告按以下類別對行業進行細分:衍生物(苯和二甲苯、汽油添加劑、甲苯二異氰酸酯 (TDI) 等)、應用(油漆和塗料、黏合劑和油墨、化工行業等)、終端用戶行業(汽車、建築、石油和天然氣等)以及地區(亞太地區、北美地區、歐洲地區等)。市場預測以噸為單位。

區域分析

到2025年,亞太地區將佔全球總量的54.70%,其5.48%的複合年成長率鞏固了其作為甲苯市場主要成長引擎的地位。都市化、建築業的蓬勃發展以及汽車保有量的不斷成長,正在推動東協和南亞地區對甲苯衍生產品的需求。

北美是一個成熟且充滿創新活力的市場,該地區的監管決策會對全球產生影響。美國正主導高毒性溶劑的淘汰,導致某些產品重組過程中甲苯成為首選溶劑。歐洲面臨最嚴格的揮發性有機化合物(VOC)法規,儘管溶劑需求正在下降,但低排放製程化學的研究和開發卻在加速進行。

在中東,沙烏地阿拉伯和阿拉伯聯合大公國新建了全球規模的混合二甲苯生產設施,使該地區成為亞洲多元化的供應來源。儘管南美洲的佔有率較小,但巴西工業的復甦正在提振全部區域的需求,而與重大事件相關的建築需求和基礎設施建設也推動了甲苯行業的成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 東協對聚氨酯泡棉的強勁需求正在推動TDI的消費。

- 印度和中國強制提高辛烷值等級,刺激了對重整甲苯的需求。

- 台灣和韓國對電子產品溶劑的需求

- 美國黏合劑產業中甲苯替代二氯甲烷

- 海灣合作理事會地區芳香植物產能快速擴張

- 市場限制因素

- 加強歐盟REACH法規中關於芳香族化合物的揮發性有機化合物(VOC)法規

- 石腦油與原油價差的波動給利潤率帶來了壓力。

- 北美地區生物基溶劑的應用日益廣泛

- 價值鏈分析

- 原料分析

- 科技趨勢

- 監管分析

- 貿易分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格指數

第5章 市場規模與成長預測

- 導數

- 苯和二甲苯

- 汽油添加劑

- 甲苯二異氰酸酯(TDI)

- 其他衍生物(苯甲酸、三硝基甲苯(TNT)、苯甲醛)

- 透過使用

- 油漆和塗料

- 黏合劑和油墨

- 化工

- 霹靂

- 其他用途(藥品、溶劑和脫脂劑、染料和顏料)

- 按最終用戶行業分類

- 車

- 建造

- 石油和天然氣

- 軍事/國防

- 其他終端用戶產業(電子產品、消費品)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- CPC Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- Indian Oil Corporation Ltd

- INEOS

- LyondellBasell Industries Holdings BV

- Mangalore Refinery and Petrochemicals Limited

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- Reliance Industries Limited

- SABIC

- Shell plc

- SK innovation Co., Ltd

- TotalEnergies

- Valero

第7章 市場機會與未來展望

The Toluene Market size is expected to grow from 36.33 Million Tons in 2025 to 37.98 Million Tons in 2026 and is forecast to reach 47.43 Million Tons by 2031 at 4.54% CAGR over 2026-2031.

Demand growth reflects the chemical's versatility as an aromatic hydrocarbon used in downstream products such as benzene, xylene, and toluene diisocyanate (TDI), which feed diverse sectors from construction to electronics. Regulatory initiatives to reduce emissions accelerate process upgrades that improve energy efficiency and cut volatile organic compound (VOC) releases, supporting long-term competitiveness. Together, these trends underscore a shift toward integrated, sustainability-oriented supply chains that favor producers able to balance cost leadership with technology investments in cleaner processes.

Global Toluene Market Trends and Insights

Robust Polyurethane Foam Build-out in ASEAN Elevates TDI Consumption

Surging output of flexible foam for furniture, bedding, and vehicle seats is driving incremental TDI demand in Malaysia, Vietnam, and Thailand. Toluene market regional investments, such as Petronas' RAPID complex, increase local access to toluene-based intermediates, limiting import reliance. Producers are elevating crude-to-chemicals yields to expand aromatics output, placing toluene at the heart of regional polyurethane supply.

Octane-Boost Mandates in India and China Boost Reformate Toluene Intake

India's Bharat Stage VI and China 6 fuel norms demand higher anti-knock components, prompting refiners to raise reformate volumes enriched with toluene. Numaligarh Refinery's upgrade to 9 MTPA consolidates local supply, while Chinese integrated complexes channel more aromatics into gasoline blending pools. These moves absorb incremental toluene streams that might otherwise face oversupply, creating a cushion for refinery margins and lifting solvent-grade prices across the toluene market in Asia Pacific.

Tightening EU REACH VOC Restrictions on Aromatics

The European Union has intensified VOC thresholds, prompting paint, coating, and adhesive producers to reformulate away from aromatic solvents[2]. Compliance costs rise through investment in abatement equipment and substitution with higher-priced low-VOC carriers. Toluene market fragmentation emerges as multinational formulators rationalize product lines to accommodate EU and the United Kingdom limits, dampening regional toluene demand in consumer-facing applications.

Other drivers and restraints analyzed in the detailed report include:

- Electronics-Grade Solvents Demand in Taiwan and South Korea

- Substitution of Methylene Chloride by Toluene in US Adhesives

- Volatility in Naphtha and Crude Spreads Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Benzene and xylene retained a 37.70% share of derivative consumption in 2025, underscoring their entrenched role in polyester, nylon, and specialty chemical chains. That leadership secures steady throughput for reformers and aromatics extractors even as margins fluctuate. Meanwhile, the toluene market size tied to TDI is projected to expand at a 5.37% CAGR from 2026-2031, reflecting robust furniture and bedding demand across emerging economies.

Benzaldehyde, benzoic acid, TNT, and niche derivatives carve specialized outlets, but collectively they account for a modest share of the toluene market volumes. Integrated producers balance this portfolio, leveraging economies of scale to supply both commodity and specialty customers.

The Toluene Market Report Segments the Industry by Derivative (Benzene and Xylene, Gasoline Additives, Toluene Diisocyanates (TDI), and Others), Application (Paints and Coatings, Adhesives and Inks, Chemical Industry, and Others), End-User Industry (Automotive, Construction, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons)

Geography Analysis

Asia Pacific controlled 54.70% of global volumes in 2025, and the region's 5.48% CAGR cements its status as the primary growth engine for the toluene market. Urbanization, construction booms, and rising vehicle penetration sustain derivative demand throughout ASEAN and South Asia.

North America is a mature yet innovative arena where regulatory decisions ripple globally. The United States is spearheading the phaseout of high-toxicity solvents, inadvertently favoring toluene in specific reformulations. Europe grapples with the strictest VOC rules, trimming solvent demand but stimulating research and development toward low-emission process chemistry.

The Middle East adds new barrels through world-scale mixed-xylene facilities in Saudi Arabia and the United Arab Emirates, positioning the region as a swing supplier for Asia. South America accounts for a smaller slice, yet Brazil's industrial recovery lifts regional appetite, especially for construction windows tied to major events and infrastructure drives growth in toluene industry.

- BASF

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- CPC Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- Indian Oil Corporation Ltd

- INEOS

- LyondellBasell Industries Holdings B.V.

- Mangalore Refinery and Petrochemicals Limited

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- Reliance Industries Limited

- SABIC

- Shell plc

- SK innovation Co., Ltd

- TotalEnergies

- Valero

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Polyurethane Foam Build-out in ASEAN Elevates TDI Consumption

- 4.2.2 Octane-Boost Mandates in India and China Boost Reformate Toluene Intake

- 4.2.3 Electronics?Grade Solvents Demand in Taiwan and South Korea

- 4.2.4 Substitution of Methylene Chloride by Toluene in US Adhesives

- 4.2.5 Rapid Capacity Addition of Aromatics Units in GCC Region

- 4.3 Market Restraints

- 4.3.1 Tightening EU REACH VOC Restrictions on Aromatics

- 4.3.2 Volatility in Naphtha and Crude Spreads Compressing Margins

- 4.3.3 Growing Bio-Based Solvent Adoption in North America

- 4.4 Value Chain Analysis

- 4.5 Feedstock Analysis

- 4.6 Technological Snapshot

- 4.7 Regulatory Analysis

- 4.8 Trade Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Degree of Competition

- 4.10 Price Index

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Derivative

- 5.1.1 Benzene and Xylene

- 5.1.2 Gasoline Additives

- 5.1.3 Toluene Diisocyanates (TDI)

- 5.1.4 Other Derivatives (Benzoic Acid, Trinitrotoluene (TNT), Benzaldehyde)

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Inks

- 5.2.3 Chemical Industry

- 5.2.4 Explosives

- 5.2.5 Other Applications (Pharmaceuticals, Solvents and Degreasers, Dyes and Pigments)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Oil and Gas

- 5.3.4 Military and Defense

- 5.3.5 Other End-user Industries (Electronics, Consumer Products)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Braskem

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 China Petrochemical Corporation

- 6.4.5 CNPC

- 6.4.6 CPC Corporation

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Formosa Chemicals & Fibre Corp

- 6.4.9 Indian Oil Corporation Ltd

- 6.4.10 INEOS

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 Mangalore Refinery and Petrochemicals Limited

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 Mitsui Chemicals, Inc.

- 6.4.15 Reliance Industries Limited

- 6.4.16 SABIC

- 6.4.17 Shell plc

- 6.4.18 SK innovation Co., Ltd

- 6.4.19 TotalEnergies

- 6.4.20 Valero

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

甲苯市場:全球市場預測,2026-2032年

甲苯市場:全球市場預測,2026-2032年 甲苯市場規模、佔有率和趨勢分析報告:按應用、地區、主要參與者和競爭對手分析以及細分市場預測(2026-2033 年)

甲苯市場規模、佔有率和趨勢分析報告:按應用、地區、主要參與者和競爭對手分析以及細分市場預測(2026-2033 年) 甲苯市場報告:按技術、應用和地區分類(2026-2034 年)

甲苯市場報告:按技術、應用和地區分類(2026-2034 年) 甲苯市場-全球產業規模、佔有率、趨勢、機會、預測:按衍生物、應用、地區和競爭對手分類,2021-2031年

甲苯市場-全球產業規模、佔有率、趨勢、機會、預測:按衍生物、應用、地區和競爭對手分類,2021-2031年 甲苯市場:依衍生物類型、應用、生產製程及地區分類

甲苯市場:依衍生物類型、應用、生產製程及地區分類 甲苯二異氰酸酯市場機會、成長要素、產業趨勢分析及2026-2035年預測。氯甲苯市場機會、成長要素、產業趨勢分析及2026-2035年預測

甲苯二異氰酸酯市場機會、成長要素、產業趨勢分析及2026-2035年預測。氯甲苯市場機會、成長要素、產業趨勢分析及2026-2035年預測 甲苯市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

甲苯市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 甲苯二異氰酸酯:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)全球甲苯二異氰酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

甲苯二異氰酸酯:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)全球甲苯二異氰酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)