|

市場調查報告書

商品編碼

2043882

甲苯二異氰酸酯:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Toluene Diisocyanate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

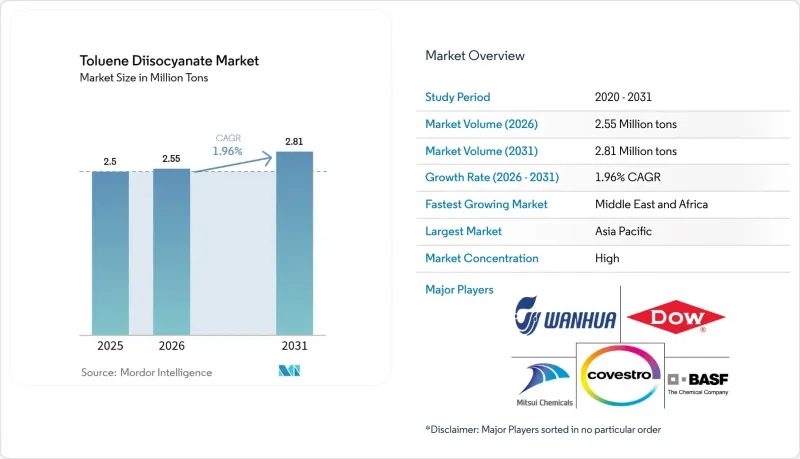

2025 年甲苯二異氰酸酯市場價值為 250 萬噸,預計到 2031 年將從 2026 年的 255 萬噸成長至 281 萬噸,預測期(2026-2031 年)複合年成長率為 1.96%。

目前的成長反映了產業正從快速擴張轉向穩步成熟,這主要得益於更嚴格的勞動安全法規、向無光氣生產流程的轉型以及亞太地區綜合石化中心持續的資本投資。生產商正專注於生產用於軟泡沫的低黏度、高純度等級產品,而下游用戶則需要更輕、更節能的材料用於家具、交通運輸和建築等領域。 2024-2025年區域價格上漲(例如,萬華化學在東協的價格上漲200美元/噸,BASF在南亞的價格上漲300美元/噸)凸顯了原料和物流持續面臨的壓力。沙烏地基礎工業公司(SABIC)在福建投資64億美元建造乙烯聯合裝置等項目,顯示了對聚氨酯需求的長期信心。受加州大學聖地牙哥分校在生物基芳香族二異氰酸酯領域取得的突破性成果啟發,一座無光氣先導工廠標誌著下一個技術前沿的到來。

全球甲苯二異氰酸酯市場趨勢及洞察

家具和床上用品對柔軟性聚氨酯泡棉的需求。

家用和商用家具製造商大量使用TDI,因為柔軟性聚氨酯具有觸感柔軟、回彈性和使用壽命長等優點。 2024年,美國家具和床上用品銷售額超過1,060億美元,發泡體的年需求量超過15億英鎊。與TDI和MDI混合的記憶海綿床墊能夠更好地分散壓力,因此零售價格更高。同時,辦公椅墊的厚度也不斷減小,在不影響舒適度的前提下減少了原料的使用。在亞太地區,都市區住宅的增加、可支配收入的成長以及家具銷售管道的拓展,正推動著TDI需求的穩定成長。中國將於2025年7月生效的家具標準GB 18584-2024對包括甲苯在內的有害物質進行了規範,鼓勵國內加工商採用更清潔的TDI等級。目前,二異氰酸酯、多元醇和添加劑供應商之間的合作研發重點是開發具有終身保固的微孔和低密度泡棉。

汽車座椅和內裝的輕量化

汽車製造商在座椅墊、頂棚和隔音墊中使用TDI基發泡材,以減輕重量並提高乘員舒適度。隨著小型電動車款的減重目標日益嚴格,預計到2030年,TDI的需求將以2.54%的複合年成長率成長。最佳的70:30 TDI:MDI混合比例可增強拉伸強度和透明度,並在高低溫循環中保持一致的觸感。汽車製造商也將TDI用於耐磨耐化學腐蝕的雙組分聚氨酯塗料。然而,較高的MDI比例會導致塗料適用期縮短,因此塗裝車間需要對催化劑配比進行微調,以確保足夠的處理時間。區域籌資策略可以降低供應風險。北美組裝依賴BASF在路易斯安那州不斷擴大的產能,而中國整車製造商則從萬華和科思創等叢集採購。

關於毒性和工人安全的法規

TDI 是強效呼吸道致敏劑,被國際癌症研究機構 (IARC) 列為 2B 類致敏物,監管機構強制要求採用低暴露閾值。美國職業安全與健康管理局 (OSHA) 將 8 小時時間加權平均值 (TWA) 設定為 0.02 ppm,而美國政府工業衛生學家協會 (ACGIH) 建議 TWA 為 0.001 ppm,短期暴露極限 (STEL) 為 0.005 ppm。由於致敏工人在 1-5 ppb 的濃度下即可產生反應,加工企業被迫改善封閉式設施、通風系統和個人防護設備。美國環保署 (EPA) 的《有毒物質控制法》(TSCA) 強制要求對某些含 TDI 的聚合物進行“新用途通知”,這增加了控制成本。在英國,健康與安全局 (HSA)建議致敏人員完全避免接觸未反應的 TDI,這迫使企業採用封閉式混合系統並實施嚴格的洩漏檢測。

細分市場分析

到2025年,發泡體將佔甲苯二異氰酸酯市場佔有率的68.10%,鞏固了該領域作為雙功能芳香族異氰酸酯主要消費領域的長期穩固地位。在發泡體中,軟質泡沫佔據了大部分市場佔有率,這主要得益於亞太和北美地區家具和床上用品需求的強勁成長。隨著中國和東南亞下游產能的提升,發泡體用甲苯二異氰酸酯的市場規模預計將進一步擴大。記憶海綿的創新應用,包括具有黏彈性和透氣性的戶外產品,利用TDI的低黏度和快速固化特性,在不影響回彈性和耐用性的前提下,打造出更輕便的床墊芯材。

除發泡體以外的其他領域的成長前景持續改善。雖然黏合劑和密封劑的銷售量目前較為溫和,但預計到2031年將以2.27%的複合年成長率成長,這主要得益於模組化建築和電動車組裝對黏合性能的嚴格要求。在塗料領域,TDI實現了高交聯密度,為汽車和木材基材提供了光澤亮麗且耐化學腐蝕的塗層。彈性體(例如輥筒和減震墊)正在拓展產品線,其中低酸度和窄異構體比例的特殊等級產品具有卓越的機械性能。

甲苯二異氰酸酯 (TDI) 市場報告按應用領域(發泡體、塗料、黏合劑和密封劑、彈性體及其他)、終端用戶行業(家具及室內裝飾、建築及施工、汽車、電子、包裝及其他)和地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以銷售量(噸)為單位。

區域分析

亞太地區佔47.62%的市場佔有率,凸顯了該地區一體化的供應鏈和具有成本效益的原料組成。中國擁有多條TDI生產線,包括科思創上海工廠(計劃到2025年將其年產能從31萬噸擴大到37萬噸)和福建萬華的年產能36萬噸項目(已通過環境評估)。該地區的甲苯二異氰酸酯市場受益於出口導向型策略,預計2024年平均離岸價(FOB)將達到每噸1700至1800美元,這將支撐其向東南亞地區的出口。在印度,可支配收入的成長和家俱生產的發展推動了需求;而在日本和韓國,高純度產品(用於電子產品和特殊彈性體)的需求尤其突出。

在北美,受家具和汽車產業的支撐,消費保持穩定。BASF位於蓋斯馬的工廠擴建將間接增強芳香族二異氰酸酯價值鏈,到2026年,該地區的MDI年產能將達到60萬噸。 TDI進口主要經由墨西哥灣沿岸地區港口,以彌補國內供應的波動。由於加拿大冷庫設施的維修和墨西哥汽車組裝的擴張,加工商的產運作運轉。

在歐洲,不斷上漲的能源成本和嚴格的脫碳目標正給利潤率帶來壓力,但該地區在低單體殘留等級方面仍保持著技術領先地位。科思創對其位於塔拉戈納的氯工廠進行了維修,引入了氧去極化陰極技術,在確保當地二異氰酸酯生產廠原料供應的同時,降低了25%的電力需求。諸如歐盟床墊生態標章標準等監管措施可能會進一步限制TDI含量,這將促進低排放系統的應用。

中東和非洲地區以2.18%的複合年成長率呈現最高增速,這主要得益於海灣合作理事會(GCC)成員國的投資,例如薩達拉綜合體項目,該地區正準備實現下游聚氨酯產品多元化。南美市場規模較小但較為穩定,巴西建設業的復甦以及阿根廷汽車零件生產的復甦,推動了銷售量的逐步成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 家具和床上用品對柔軟性聚氨酯泡沫的需求。

- 汽車座椅和內裝的輕量化

- 建築隔熱材料(硬質/軟質泡沫)的建築標準

- 電瓶電池用溫度控管泡沫

- 擴大無光氣TDI的生產規模

- 市場限制因素

- 關於毒性和工人安全的法規

- 甲苯/原油價格波動

- TDI的歐盟床墊生態標章標準

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 透過使用

- 發泡體

- 塗層

- 黏合劑和密封劑

- 彈性體

- 其他用途

- 按最終用戶行業分類

- 家具和室內設計

- 建築/施工

- 車

- 電子學

- 包裝

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- BASF SE

- BorsodChem

- Cangzhou Dahua Group Co., Ltd.

- Covestro AG

- Dow

- GNFC Ltd.

- Hanwha Solutions Chemical Division Corporation

- Karoon Petrochemical Company

- KH Chemicals

- Merck KGaA

- Mitsui Chemicals, Inc.

- OCI Company Ltd.

- Simel Chemical Industry Co., Ltd.

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry(India)Pvt., Ltd.

- Wanhua

第7章 市場機會與未來展望

The Toluene Diisocyanate Market size was valued at 2.5 Million tons in 2025 and estimated to grow from 2.55 Million tons in 2026 to reach 2.81 Million tons by 2031, at a CAGR of 1.96% during the forecast period (2026-2031).

Current growth reflects a sector moving from rapid expansion toward steady maturity, shaped by stricter worker-safety rules, a shift toward phosgene-free routes, and sustained capital spending in Asia-Pacific's integrated petrochemical hubs. Producers are emphasizing low-viscosity, high-purity grades for flexible foams, while downstream users seek lighter, more energy-efficient materials for furniture, transportation, and construction applications. Regional price spikes in 2024-2025-such as Wanhua Chemical's USD 200/ton lift in ASEAN and BASF's USD 300/ton rise in South Asia-underscore persistent feedstock and logistics pressures. Investments like SABIC's USD 6.4 billion ethylene complex in Fujian illustrate long-term confidence in polyurethane demand. Phosgene-free pilot plants, inspired by UC San Diego's bio-based aromatic diisocyanate breakthrough, signal the next technology frontier.

Global Toluene Diisocyanate Market Trends and Insights

Flexible PU-Foam Demand in Furniture and Bedding

Household and commercial furniture makers consume large volumes of TDI because flexible polyurethane delivers soft-touch cushioning, high rebound, and long service life. U.S. furniture and bedding sales topped USD 106 billion in 2024, sustaining foam off-take that exceeded 1.5 billion lb annually. Memory-foam mattresses that blend TDI and MDI enhance pressure relief and command premium retail pricing, while thinner office-chair cushions reduce raw-material use without sacrificing comfort. In Asia-Pacific, urban housing growth, rising disposable incomes, and e-commerce furniture channels spur steady TDI uptake. China's GB 18584-2024 furniture standard, effective July 2025, limits hazardous substances including toluene, prompting local converters to adopt cleaner TDI grades. Collaborative R&D among diisocyanate, polyol, and additive suppliers now focuses on smaller-cell, lower-density foams that support lifetime warranties.

Automotive Seat and Interior Lightweighting

Vehicle makers rely on TDI-based foams for seat cushions, headliners, and acoustical pads because the material cuts weight and improves passenger comfort. Light-duty electrified models intensify weight-reduction targets, lifting TDI demand at a 2.54% CAGR to 2030. Optimal 70:30 TDI:MDI blends raise tensile strength and transparency, delivering consistent feel in hot-and-cold cycles. Automakers also apply TDI in two-component polyurethane coatings that withstand abrasion and chemicals. However, higher MDI ratios shorten pot life, so finishing shops fine-tune catalyst packages to keep processing windows open. Regional sourcing strategies limit supply risk: North American assemblers lean on BASF's expanding Louisiana capacity, while Chinese OEMs source from Wanhua and Covestro clusters.

Toxicity And Worker-Safety Regulations

TDI is a potent respiratory sensitizer classified as Group 2B by IARC, prompting regulators to enforce low exposure thresholds. OSHA sets an 8-hour TWA of 0.02 ppm, while ACGIH recommends 0.001 ppm TWA and 0.005 ppm STEL. Sensitized workers can react at 1-5 ppb, which pushes converters to improve enclosure, ventilation, and personal protective equipment. EPA's Toxic Substances Control Act requires significant-new-use notifications for certain TDI-bearing polymers, adding administrative cost. In the United Kingdom, the Health Security Agency advises complete avoidance of unreacted TDI for sensitized individuals, forcing companies to adopt closed-mix systems and rigorous leak detection.

Other drivers and restraints analyzed in the detailed report include:

- Building-Insulation Codes (Rigid/Flexible Foams)

- EV Battery Thermal-Management Foams

- Toluene/Crude-Oil Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Foams represented 68.10% of the Toluene diisocyanates market share in 2025, confirming the segment's long-standing position as the principal consumer of difunctional aromatic isocyanates. Within foams, flexible grades command the majority, backed by robust furniture and bedding demand in Asia-Pacific and North America. The Toluene diisocyanates market size for foams is projected to rise in line with downstream capacity additions in China and Southeast Asia. Memory-foam innovations, including viscoelastic and breathable outdoor variants, build on TDI's low viscosity and fast cure, offering lighter mattress cores without compromising rebound or durability.

Growth prospects outside foams continue to improve. Adhesives and sealants account for a modest volume today but are forecast at a 2.27% CAGR through 2031 thanks to stringent bonding requirements in modular construction and electric-vehicle assembly. In coatings, TDI affords high cross-link density for glossy, chemical-resistant finishes on automotive and wood substrates. Elastomers such as rollers and anti-vibration pads round out the portfolio, with niche grades featuring low acidity and narrow isomer ratios for superior mechanical performance.

The Toluene Diisocyanates (TDI) Market Report is Segmented by Application (Foams, Coatings, Adhesives and Sealants, Elastomers, and Other Applications), End-User Industry (Furniture and Interiors, Building and Construction, Automotive, Electronics, Packaging, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific's 47.62% share underscores its integrated supply chains and cost-advantaged feedstock slate. China hosts multiple TDI lines, including Covestro's Shanghai facility expanding from 310 000 tpa to 370 000 tpa by 2025 and Fujian Wanhua's 360 000 tpa project that cleared environmental review. The Toluene diisocyanates market size in the region benefits from export-oriented strategies, with average 2024 FOB prices of USD 1 700-1 800/ton supporting shipments across Southeast Asia. India's rising disposable income and furniture output add incremental demand, while Japan and South Korea emphasize high-purity grades for electronics and specialty elastomers.

North America shows stable consumption underpinned by furniture and automotive sectors. BASF's Geismar expansion will push regional MDI capacity to 600 000 tpa by 2026, indirectly bolstering aromatic diisocyanate value chains. TDI imports enter primarily through Gulf Coast ports, balancing domestic supply fluctuations. Canadian cold-storage retrofits and Mexican vehicle-assembly growth keep converters operating near capacity.

Europe confronts elevated energy costs and stringent decarbonization targets that pressure margins, yet the region retains technological leadership in low-monomer-residual grades. Covestro's chlorine-plant upgrade in Tarragona deploys oxygen-depolarized-cathode technology that trims power needs 25% and secures feedstock for local diisocyanate units. Regulatory initiatives such as EU Ecolabel criteria for mattresses could further limit TDI content, spurring adoption of lower-emission systems.

Middle East and Africa posts the fastest 2.18% CAGR on the back of GCC investments like the Sadara complex, which positions the region for downstream polyurethane diversification. South America remains a smaller but steady outlet, with Brazil's construction recovery and Argentina's auto-parts output supporting gradual volume gains.

- BASF SE

- BorsodChem

- Cangzhou Dahua Group Co., Ltd.

- Covestro AG

- Dow

- GNFC Ltd.

- Hanwha Solutions Chemical Division Corporation

- Karoon Petrochemical Company

- KH Chemicals

- Merck KGaA

- Mitsui Chemicals, Inc.

- OCI Company Ltd.

- Simel Chemical Industry Co., Ltd.

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry (India) Pvt., Ltd.

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Flexible PU-Foam Demand in Furniture and Bedding

- 4.2.2 Automotive Seat and Interior Lightweighting

- 4.2.3 Building-Insulation Codes (Rigid/Flexible Foams)

- 4.2.4 EV Battery Thermal-Management Foams

- 4.2.5 Phosgene-Free TDI Scale-Up

- 4.3 Market Restraints

- 4.3.1 Toxicity and Worker-Safety Regulations

- 4.3.2 Toluene/Crude-Oil Price Volatility

- 4.3.3 EU Ecolabel Limits for TDI in Mattresses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Foams

- 5.1.2 Coatings

- 5.1.3 Adhesives and Sealants

- 5.1.4 Elastomers

- 5.1.5 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Furniture and Interiors

- 5.2.2 Building and Construction

- 5.2.3 Automotive

- 5.2.4 Electronics

- 5.2.5 Packaging

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 BorsodChem

- 6.4.3 Cangzhou Dahua Group Co., Ltd.

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 GNFC Ltd.

- 6.4.7 Hanwha Solutions Chemical Division Corporation

- 6.4.8 Karoon Petrochemical Company

- 6.4.9 KH Chemicals

- 6.4.10 Merck KGaA

- 6.4.11 Mitsui Chemicals, Inc.

- 6.4.12 OCI Company Ltd.

- 6.4.13 Simel Chemical Industry Co., Ltd.

- 6.4.14 Thermo Fisher Scientific Inc.

- 6.4.15 Tokyo Chemical Industry (India) Pvt., Ltd.

- 6.4.16 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

甲苯市場:全球市場預測,2026-2032年

甲苯市場:全球市場預測,2026-2032年 甲苯市場規模、佔有率和趨勢分析報告:按應用、地區、主要參與者和競爭對手分析以及細分市場預測(2026-2033 年)

甲苯市場規模、佔有率和趨勢分析報告:按應用、地區、主要參與者和競爭對手分析以及細分市場預測(2026-2033 年) 甲苯市場報告:按技術、應用和地區分類(2026-2034 年)

甲苯市場報告:按技術、應用和地區分類(2026-2034 年) 甲苯市場-全球產業規模、佔有率、趨勢、機會、預測:按衍生物、應用、地區和競爭對手分類,2021-2031年

甲苯市場-全球產業規模、佔有率、趨勢、機會、預測:按衍生物、應用、地區和競爭對手分類,2021-2031年 甲苯市場:依衍生物類型、應用、生產製程及地區分類

甲苯市場:依衍生物類型、應用、生產製程及地區分類 甲苯二異氰酸酯市場機會、成長要素、產業趨勢分析及2026-2035年預測。氯甲苯市場機會、成長要素、產業趨勢分析及2026-2035年預測

甲苯二異氰酸酯市場機會、成長要素、產業趨勢分析及2026-2035年預測。氯甲苯市場機會、成長要素、產業趨勢分析及2026-2035年預測 甲苯市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

甲苯市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 甲苯:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031)全球甲苯二異氰酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

甲苯:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031)全球甲苯二異氰酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)