|

市場調查報告書

商品編碼

2044102

光照上網技術(Li-Fi):市佔率分析、產業趨勢與統計、成長預測(2026-2031)Light Fidelity (Li-Fi) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

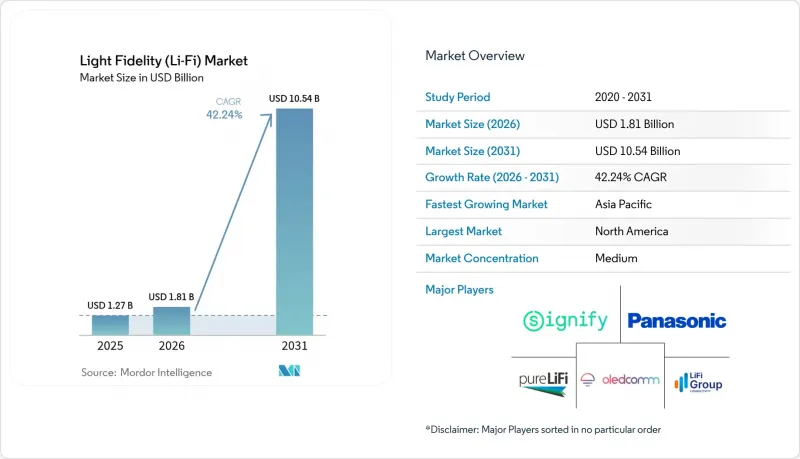

預計光照上網(Li-Fi)市場將從 2025 年的 12.7 億美元成長到 2026 年的 18.1 億美元,到 2031 年達到 105.4 億美元,2026 年至 2031 年的複合年成長率為 42.24%。

IEEE 802.11bb互通性標準消除了廠商鎖定風險,加速了商業性進程。此外,美國陸軍的大規模部署也證明了其在實際環境中的穩健性。如今,企業將光纖無線技術視為 Wi-Fi 的安全補充,尤其是在頻寬擁塞、電磁干擾或間諜威脅等無線解決方案易受攻擊的環境中。醫療、航空航太和工業自動化領域的早期採用者報告稱,網路中斷減少、延遲降低,數據安全性也得到提升,由此產生的同行主導需求超越了傳統的照明維修週期。因此,試點活動的活性化正在推動一系列維修和新計畫的順利開展,這些項目計劃於 2026 年至 2028 年間啟動。

全球光照上網技術(Li-Fi)市場趨勢與洞察

LED照明維修浪潮

在2020年至2025年間將螢光具更換為LED燈具的機構,如今將Li-Fi視為分階段升級而非新建設。 Wieland Electric公司在2025年透過將光調變器整合到現有照明燈具中,展示了這一模式。此舉避免了鋪設新電纜,並在短短幾天內運作250 Mbps的通訊鏈路。由於設施管理人員正在整合照明和網路預算,與單獨部署無線系統相比,節能和連接性的提升使得投資回收期更短。隨著越來越多的照明供應商提供「支援Li-Fi」的燈具,採購團隊正在積極地明確相關功能,以確保未來的需求。因此,這種維修趨勢正在將日常維護週期轉變為龐大且前景看好的光無線市場。

IEEE 802.11bb互通性標準

2023年IEEE 802.11bb標準的正式核准,以及隨後政府採購公告強制要求使用符合該標準的硬體,消除了此前阻礙試點部署的多供應商風險。企業現在正將Li-Fi網路基地台整合到現有的IP安全和QoS(服務品質)架構中,無需再建置並行的IT架構。晶片組製造商正在製定明確的設計規則,以支援大規模生產並縮小與Wi-Fi的成本差距。標準化也促進了全球認證,使製造商能夠向全球銷售單一產品系列。因此,可靠性得到提升,銷售週期縮短,短期出貨量預測也得到了上調。

與Wi-Fi相比,設備成本更高

Li-Fi網路基地台和USB接收器的價格仍然是同類Wi-Fi設備的3到5倍,這種價格差異阻礙了它們在學校、新創公司和家庭中的普及。 Oledcomm的LiFiMAX Compact套件降低了進入門檻,但其價格仍使其更適合安全設施而非大眾市場。由於需要雙硬體——燈具和客戶端設備都需要收發器——組件成本加倍。在整合晶片組成為筆記型電腦和平板電腦的主流之前,每個用戶的適配器成本將居高不下,總擁有成本(TCO)也將居高不下。儘管供應商正在嘗試引入租賃和訂閱模式,但短期內能否普及仍取決於那些因安全性和避免干擾的需求而需要額外成本的應用場景。

細分市場分析

預計到2025年,室內網路和企業部署將佔光照上網(Li-Fi)市場佔有率的39.21%,證實了安全會議室、負責人和交易大廳目前是最大的收入來源。醫院、工廠和機場的試點部署正在穩步推進,這增強了人們對Li-Fi在實驗室外可靠運作的信心。目前小規模的水下和海事領域預計到2031年將以43.66%的複合年成長率成長,因為海軍和海上運營商正在用藍綠雷射系統取代衰減嚴重的無線鏈路。由於光訊號不會干擾維生設備,因此在醫療機構的部署持續獲得支持,使得患者照護區域能夠轉變為可靠的高頻寬區域。總而言之,Li-Fi在關鍵任務環境中出色的初步表現凸顯了其在更廣泛的企業部署中的有效性。

國防領域的支援正在產生連鎖反應,加速民用產業的採購。軍事領域的實地測試表明,光鏈路具有極強的抗干擾能力,且不會發射可偵測的無線電波。這些結果引起了金融服務和關鍵基礎設施營運商的共鳴,他們一直擔憂間諜活動。航空領域的測試表明,乘客可以接收Gigabit級內容,而不會給航空電子設備增加射頻噪聲,這進一步擴大了這項技術的吸引力。雖然智慧家庭領域目前仍處於小眾階段,但遊戲玩家和在家工作已經開始為低延遲光鏈路支付高價,這表明消費者正在逐步接受這項技術。總而言之,這些多樣化的部署管道降低了風險,並支撐了光照上網(Li-Fi)市場規模的穩健前景,而這與其廣泛的應用領域密切相關。

到2025年,LED佔組件銷售額的47.38%。這是因為許多機構選擇維修現有照明設備,而不是投資獨立的LED發光元件。這項優點反映了辦公室和工廠天花板照明已十分普及的現實情況,只需少量額外硬體即可增加數據調製功能。同時,光電探測器預計將實現最快成長,2026年至2031年的複合年成長率將達到43.26%,因為崩光二極體和矽光電倍增器擴展了通訊範圍並實現了多Gigabit的吞吐量。光學濾波器和精密透鏡透過增強光束聚焦和阻擋環境光來完善新型接收器,這在陽光充足的中庭和玻璃幕牆工廠中至關重要。隨著企業需要控制面板來協調Li-Fi和Wi-Fi之間的漫遊,軟體和服務收入也同步成長。

尤其是在需要確定性延遲的製造環境中,基於雷射的垂直腔面共振器(VCSO)發送器正日益普及。雖然雷射在光照上網 (Li-Fi) 市場中所佔佔有率仍然較小,但其高達 10 Gbps 的傳輸能力正在支援即時機器視覺和機器人技術,從而催生了對先進檢測器的新需求。為了在不斷變化的光照條件下透過自適應編碼來穩定通訊鏈路,微控制器和調製器變得越來越複雜,導致每個燈具的半導體元件用量增加。隨著供應商不再只是追求亮度,而是致力於實現人眼安全限值,提高接收器靈敏度正成為擴大覆蓋範圍的主要手段。這種轉變正將價值從通用 LED 轉移到利潤更高的光電和訊號處理元件上。

區域分析

預計到2025年,北美將佔LightFitness銷售額的38.42%,位居市佔率榜首。由於聯邦網路安全法規和持續的國防預算,政府和金融服務業的需求仍然強勁。 LED的廣泛應用也使供應商受益,加速了Li-Fi在企業園區的部署。本地製造業投資縮短了供應鏈,滿足了國內採購需求,進一步增強了買家信心。儘管該地區的預期成長率不如亞太地區,但仍保持強勁勢頭。

預計到2031年,亞太地區的Li-Fi市場將以43.29%的複合年成長率成長,創下該地區Li-Fi市場有史以來的最高成長率。中國、印度、日本和韓國政府主導的試點項目,以及對智慧工廠和智慧城市走廊的津貼,正在為國內供應商帶來首批關鍵訂單。各國國防部正在資助安全的艦隊通訊,以繞過擁擠的無線電頻寬;教育機構也在研究實驗室中採用Li-Fi技術來保護智慧財產權。以VCSEL陣列和檢測器為核心的新興組件生態系統可望降低成本,並實現大規模商業部署。隨著標準的不斷完善,跨境部署將使亞洲供應商能夠出口承包解決方案。

在嚴格的電磁相容性 (EMC) 標準和鼓勵光控的隱私法規的推動下,歐洲也緊隨其後。航空公司正在為其飛機加裝 Li-Fi 照明系統,辦公大樓業主也在安裝安全會議室以吸引優質租戶。中東和非洲各國政府正在關鍵基礎設施中試行這項技術,而拉丁美洲的物流業者則在高挑的倉庫中進行測試,因為無線電波反射會影響 Wi-Fi 的可靠性。儘管這些地區目前的市場佔有率小規模,但成功的試點計畫有望刺激潛在需求,並在預測期內推動全球 Li-Fi 市場規模的進一步成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- LED照明維修熱潮

- 國防和醫療領域中安全的無射頻通訊鏈路

- IEEE 802.11bb互通性標準

- 機上互聯互通實施現狀

- 基於VCSEL的工業鏈路,傳輸速率超過10Gbps

- 強制性射頻限制無塵室

- 市場限制因素

- 與Wi-Fi相比,設備成本更高

- 能見度受阻且距離短

- 碎片化的頻譜調節

- 混合Li-Fi/Wi-Fi的安全挑戰

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過使用

- 室內網路和企業

- 醫療保健和醫療設備

- 汽車和交通運輸

- 水下/海洋

- 航太/國防

- 智慧家庭和家用電子電器

- 工業自動化和倉儲

- 按組件

- LED

- 檢測器

- 微控制器和調變器

- 光學濾光片和透鏡

- 軟體和服務

- 按外形規格

- Li-Fi 燈/照明設備

- Li-Fi 加密狗和存取金鑰

- LiFi模組/晶片組

- 整合式Li-Fi照明燈具

- 最終用戶

- 公司

- 政府/國防

- 住宅

- 運輸/物流

- 工業製造

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- pureLiFi Ltd

- Oledcomm SAS

- LiFi Group

- Panasonic Holdings Corp

- Lucibel SA

- Zero1 Pte Ltd

- LumEfficient LLC

- KYOCERA SLD Laser Inc

- Acuity Brands Lighting Inc

- Qualcomm Technologies Inc

- Broadcom Inc

- Lite-On Technology Corp

- Renesas Electronics Corp

- Velmenni OU

- Getac Technology Corp

- Honeywell International Inc

- PureLifi France SAS

- Firefly LiFi Ltd

- Fraunhofer HHI

第7章 市場機會與未來展望

The Light Fidelity (Li-Fi) market size is expected to increase from USD 1.27 billion in 2025 to USD 1.81 billion in 2026 and reach USD 10.54 billion by 2031, growing at a CAGR of 42.24% over 2026-2031.

Commercial momentum accelerated after the IEEE 802.11bb interoperability standard removed vendor-lock risk, while large-scale U.S. Army deployments validated field resilience. Enterprises now view optical wireless as a secure overlay that complements Wi-Fi, especially in environments where spectrum congestion, electromagnetic interference, or espionage threats undermine radio solutions. Early adopters in healthcare, aviation, and industrial automation report fewer network outages, lower latency, and greater confidence in data security, creating peer-driven demand that extends beyond traditional lighting refurbishment cycles. The resulting uptick in pilot activity supports a robust pipeline of retrofit and green-field projects scheduled to start during 2026-2028.

Global Light Fidelity (Li-Fi) Market Trends and Insights

LED-Lighting Retrofit Wave

Organizations that replaced fluorescent fixtures with LEDs during 2020-2025 now view Li-Fi as an incremental upgrade rather than a green-field build. Wieland Electric demonstrated the model in 2025 by embedding optical modulators into existing luminaires, avoiding new cable pulls and bringing 250 Mbps links online in days. Facility managers merge lighting and networking budgets, so the combined energy savings and connectivity gains shorten payback periods compared with separate wireless rollouts. As more lighting vendors ship "Li-Fi-ready" fixtures, procurement teams specify the capability up front, locking in future demand. The retrofit dynamic, therefore, converts a routine maintenance cycle into a large, addressable funnel for optical wireless.

IEEE 802.11bb Interoperability Standard

Formal ratification of IEEE 802.11bb in 2023, followed by government procurement notices that require compliant hardware, removed the multi-vendor risk that once stalled pilots. Enterprises now integrate Li-Fi access points into existing IP security and quality-of-service frameworks, eliminating the need for parallel IT stacks. Chipset makers have clear design rules that support volume production and narrow the cost gap with Wi-Fi. Standards alignment also eases global certification, enabling manufacturers to ship a single product family worldwide. The resulting confidence compresses sales cycles and lifts near-term shipment forecasts.

High Device Cost Versus Wi-Fi

Li-Fi access points and USB receivers still cost three to five times as much as comparable Wi-Fi gear, a premium that deters schools, start-ups, and homeowners. Oledcomm's LiFiMAX Compact kit reduces installation friction but remains priced for security-sensitive sites rather than mass adoption. The dual-hardware requirement transceivers in both lamps and client devices double the bill of materials. Until integrated chipsets appear in mainstream laptops and tablets, per-user dongle costs will keep total ownership high. Vendors are experimenting with leasing and subscription models, yet near-term uptake still hinges on applications where security or interference avoidance justifies the added spend.

Other drivers and restraints analyzed in the detailed report include:

- Secure RF-Free Links for Defense and Healthcare

- In-Flight Cabin Connectivity Adoption

- Line-of-Sight Blockage and Short Range

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Indoor networking and enterprise deployments accounted for 39.21% of the Light Fidelity (Li-Fi) market share in 2025, confirming that secure conference rooms, executive suites, and trading floors form the largest current revenue pool. Hospitals, factories, and airports added steady pilot volume, boosting confidence that Li-Fi performs reliably outside laboratories. The underwater and maritime niche, although small today, is projected to expand at a 43.66% CAGR through 2031 as navies and offshore operators replace attenuated radio links with blue-green laser systems. Healthcare installations continue to gain favor because optical signals do not interfere with life-support equipment, enabling patient-care areas to become reliable, high-bandwidth zones. Overall, strong early performance in mission-critical settings validates Li-Fi for broader enterprise rollouts.

Defense endorsements create a ripple effect that speeds procurement in civilian industries. Military field tests demonstrated that optical links remain jam-resistant and free of detectable emissions, a finding that resonates with financial services and critical infrastructure operators who fear espionage. Aviation trials show passengers can receive gigabit content without adding RF noise to avionics, further widening the technology's appeal. Smart home interest remains niche, yet gamers and home-office users already pay premiums for low-latency optical links, hinting at a gradual trickle-down to consumers. Taken together, diverse adoption paths diversify risk and underpin a strong outlook for the Light Fidelity (Li-Fi) market size tied to application breadth.

LEDs accounted for 47.38% of 2025 component revenue, as most organizations retrofit existing fixtures rather than invest in stand-alone emitters. Their dominance reflects the practical reality that ceiling lights already blanket offices and factories, so adding data modulation demands minimal extra hardware. Photodetectors, however, are on track to deliver the fastest growth, with a 43.26% CAGR from 2026 to 2031, as avalanche photodiodes and silicon photomultipliers extend range and unlock multi-gigabit throughput. Optical filters and precision lenses complement the new receivers by sharpening beam focus and blocking ambient light, essential for sunlit atria and glass-walled factories. Software and services revenue rises in tandem as enterprises need dashboards that orchestrate roaming between Li-Fi and Wi-Fi.

A transition toward laser-based vertical-cavity surface-emitting transmitters is underway, particularly in manufacturing environments that demand deterministic latency. While lasers still account for only a small share of the Light Fidelity (Li-Fi) market, their ability to reach 10 Gbps supports real-time machine vision and robotics, creating new demand for advanced detectors. Micro-controllers and modulators become more complex because adaptive coding keeps links stable during lighting variations, thereby increasing semiconductor content per fixture. As vendors chase eye-safety limits rather than raw brightness, receiver sensitivity improvements become the primary lever for coverage gains. This shift redirects value from commodity LEDs toward higher-margin photonics and signal-processing components.

The Light Fidelity Market Report is Segmented by Application (Underwater and Maritime, Aerospace and Defense, and More), Component (LEDs, Photodetectors, and More), Form Factor (Li-Fi Lamps/Luminaires, Li-Fi Dongles and Access Keys, Li-Fi Modules/Chipsets, Integrated Li-Fi Fixtures), End-User (Enterprises, Residential, Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.42% of 2025 revenue, placing the region at the top of the light fidelity market share leaderboard. Federal cybersecurity mandates and sustained defense funding continue to anchor demand in government and financial services. Vendors also benefit from wide LED penetration, which speeds Li-Fi retrofits across corporate campuses. Local manufacturing investments shorten supply chains and satisfy domestic-content rules, further reinforcing buyer confidence. The region's growth outlook remains solid even though its forecast expansion trails that of the Asia-Pacific.

Asia-Pacific is projected to grow at a 43.29% CAGR through 2031, the highest regional growth rate recorded for the light fidelity market. Government-backed pilots in China, India, Japan, and South Korea channel grants into smart factories and smart city corridors, creating early anchor orders for domestic suppliers. Defense ministries fund secure fleet communications that avoid congested radio bands, and educational institutions install Li-Fi in research labs to protect intellectual property. Component ecosystems emerging around VCSEL arrays and photodetectors are expected to bring down costs and enable large-scale commercial launches. As standards alignment improves, cross-border deployments will allow Asian vendors to export turnkey solutions.

Europe follows closely behind, driven by stringent electromagnetic-compatibility codes and privacy regulations that favor optical confinement. Airlines retrofit cabins with Li-Fi lighting harnesses, while office landlords install secure meeting rooms to attract blue-chip tenants. Middle East and African governments pilot the technology at critical infrastructure sites, and Latin American logistics operators test it in high-bay warehouses where radio reflections degrade Wi-Fi reliability. Although these regions currently hold modest shares, successful trials could unlock pent-up demand, adding incremental volume to the global light fidelity market size during the forecast window.

- Signify N.V.

- pureLiFi Ltd

- Oledcomm SAS

- LiFi Group

- Panasonic Holdings Corp

- Lucibel SA

- Zero1 Pte Ltd

- LumEfficient LLC

- KYOCERA SLD Laser Inc

- Acuity Brands Lighting Inc

- Qualcomm Technologies Inc

- Broadcom Inc

- Lite-On Technology Corp

- Renesas Electronics Corp

- Velmenni OU

- Getac Technology Corp

- Honeywell International Inc

- PureLifi France SAS

- Firefly LiFi Ltd

- Fraunhofer HHI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED-Lighting Retrofit Wave

- 4.2.2 Secure RF-Free Links for Defense and Healthcare

- 4.2.3 IEEE 802.11bb Interoperability Standard

- 4.2.4 In-Flight Cabin Connectivity Adoption

- 4.2.5 VCSEL-Based Above 10 Gbps Industrial Links

- 4.2.6 RF-Restricted Clean-Room Mandates

- 4.3 Market Restraints

- 4.3.1 High Device Cost versus Wi-Fi

- 4.3.2 Line-of-Sight Blockage and Short Range

- 4.3.3 Fragmented Optical-Spectrum Rules

- 4.3.4 Hybrid Li-Fi/Wi-Fi Security Gaps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Indoor Networking and Enterprise

- 5.1.2 Healthcare and Medical Devices

- 5.1.3 Vehicle and Transportation

- 5.1.4 Underwater and Maritime

- 5.1.5 Aerospace and Defense

- 5.1.6 Smart Home and Consumer Electronics

- 5.1.7 Industrial Automation and Warehouse

- 5.2 By Component

- 5.2.1 LEDs

- 5.2.2 Photodetectors

- 5.2.3 Micro-Controllers and Modulators

- 5.2.4 Optical Filters and Lenses

- 5.2.5 Software and Services

- 5.3 By Form Factor

- 5.3.1 Li-Fi Lamps/Luminaires

- 5.3.2 Li-Fi Dongles and Access Keys

- 5.3.3 Li-Fi Modules/Chipsets

- 5.3.4 Integrated Li-Fi Fixtures

- 5.4 By End-User

- 5.4.1 Enterprises

- 5.4.2 Government and Defense

- 5.4.3 Residential

- 5.4.4 Transportation and Logistics

- 5.4.5 Industrial Manufacturing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 pureLiFi Ltd

- 6.4.3 Oledcomm SAS

- 6.4.4 LiFi Group

- 6.4.5 Panasonic Holdings Corp

- 6.4.6 Lucibel SA

- 6.4.7 Zero1 Pte Ltd

- 6.4.8 LumEfficient LLC

- 6.4.9 KYOCERA SLD Laser Inc

- 6.4.10 Acuity Brands Lighting Inc

- 6.4.11 Qualcomm Technologies Inc

- 6.4.12 Broadcom Inc

- 6.4.13 Lite-On Technology Corp

- 6.4.14 Renesas Electronics Corp

- 6.4.15 Velmenni OU

- 6.4.16 Getac Technology Corp

- 6.4.17 Honeywell International Inc

- 6.4.18 PureLifi France SAS

- 6.4.19 Firefly LiFi Ltd

- 6.4.20 Fraunhofer HHI

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

Li-Fi技術市場-全球及區域分析:按應用、組件和地區分類-分析與預測,2026-2035年

Li-Fi技術市場-全球及區域分析:按應用、組件和地區分類-分析與預測,2026-2035年 Li-Fi市場規模、佔有率、趨勢和預測:按組件、應用、傳輸方式、最終用戶和地區分類,2026-2034年

Li-Fi市場規模、佔有率、趨勢和預測:按組件、應用、傳輸方式、最終用戶和地區分類,2026-2034年 2026年全球光學相機通訊市場報告

2026年全球光學相機通訊市場報告 光照上網技術市場:按應用和地區分類

光照上網技術市場:按應用和地區分類 Li-Fi全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)Li-Fi(光照上網)/可見光通訊全球市場報告(2026 年)

Li-Fi全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)Li-Fi(光照上網)/可見光通訊全球市場報告(2026 年) 光學保真市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、最終用途、地區和競爭格局分類,2021-2031年)

光學保真市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、最終用途、地區和競爭格局分類,2021-2031年) Li-Fi市場規模、佔有率和成長分析(按組件、應用、最終用戶、傳輸方式和地區分類)—產業預測(2026-2033年)

Li-Fi市場規模、佔有率和成長分析(按組件、應用、最終用戶、傳輸方式和地區分類)—產業預測(2026-2033年) 全球Li-Fi市場(至2035年):依組件、硬體、傳輸方式、應用、公司規模、商業模式、最終用戶和地區劃分

全球Li-Fi市場(至2035年):依組件、硬體、傳輸方式、應用、公司規模、商業模式、最終用戶和地區劃分 FSO 與 VLC/Li-Fi 的全球市場

FSO 與 VLC/Li-Fi 的全球市場