|

市場調查報告書

商品編碼

2044098

南美洲超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

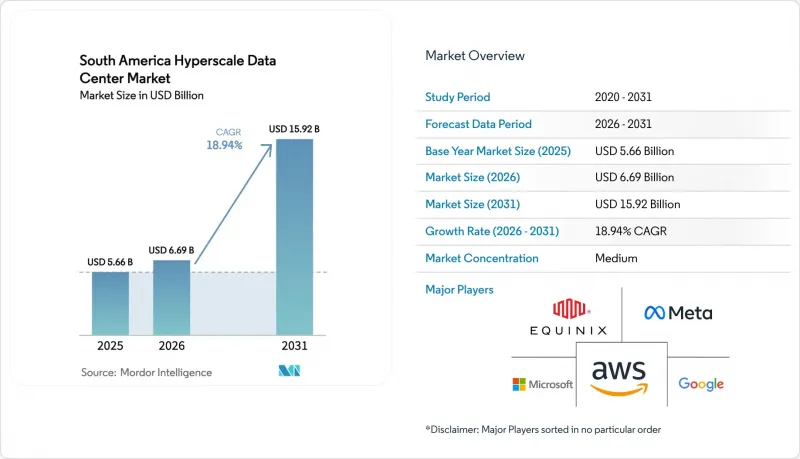

預計南美超大規模資料中心市場將從 2025 年的 56.6 億美元成長到 2026 年的 66.9 億美元,到 2031 年達到 159.2 億美元,2026 年至 2031 年的複合年成長率為 18.94%。

雲端區域的快速擴張、新型海底光纜的鋪設以及大量可再生能源合約的簽訂,正在加速各大大都會圈的資本投資。超大規模資料中心業者資料中心營運商持續建造自有園區,而託管服務供應商則透過分散對電網的依賴來獲取更多電力,以滿足客戶對更快運作速度和不間斷服務的需求。巴西、阿根廷和哥倫比亞實施的資料主權法規要求個人和公共部門資料必須保留在各自國家境內,這有效地提升了南美超大規模資料中心市場的工作負載佔有率。同時,GPU密集型人工智慧叢集正將每個機架的功率密度推高至30千瓦以上,迫使營運商大力投資水冷系統和熱交換器維修,從而調整其機械基礎設施預算。推動營收成長的關鍵因素包括超大規模資料中心業者的自有建設項目、營運商中立園區內以交叉連接為中心的經營模式,以及與監管價格相比可享有12%或更高折扣的可再生能源購買協議。挑戰依然存在,包括電網不可靠、高壓工程師短缺,以及某些地區因缺水導致蒸發冷卻受限而造成的臨時停電。儘管如此,裝置容量超過60兆瓦的大型園區正透過將變電站、冷水機組和光纖環網整合到大規模的容量基礎中,從而發揮營運槓桿作用。由於前五名供應商佔據了約62%的總裝置容量,競爭仍然處於適度水平,這為區域專家和專注於邊緣運算的新興參與企業提供了充足的空間,讓他們可以透過與當地公用事業公司建立合作關係、組建雙語支援團隊以及部署下一代液冷系統來脫穎而出。

南美洲超大規模資料中心市場趨勢與洞察

超大規模資料中心業者服務商推出的雲端區域數量激增。

積極的雲端區域部署是推動南美洲超大規模資料中心市場發展的最強勁動力。亞馬遜雲端服務 (AWS) 正在投資 40 億美元建造其聖地牙哥雲端區域,該區域將擁有 12 個可用區,容量可擴展至 40 至 80 兆瓦,旨在吸引那些需要毫秒延遲才能運行支付引擎和擴增實境(AR) 購物車的軟體供應商。微軟也採取了類似的舉措,在同一都會區部署了一個 Azure 可用區。同時,谷歌在聖保羅推出基於 M8g ARM 的實例後,將每核心成本降低了 22%。這些大規模部署刺激了對鄰近託管設施的需求,因為獨立軟體供應商需要將其應用伺服器部署在同一可用區域內,以滿足嚴格的服務等級目標。當企業簽署交叉連接協議,連接超超大規模資料中心業者時,這項循環便得以完成,使聖保羅的維拉叢集和聖地牙哥的基利庫拉走廊等叢集的運轉率超過 85%。巴西新推出的主權工作負載分類法規將進一步加強對國內託管的依賴,確保雲端建設的勢頭在中期內得以持續。

海底電纜登陸可以改善延遲並提高冗餘度。

第二個驅動力是對跨太平洋和南北向海底光纜的投資,這將降低延遲並實現容錯移轉路徑的多樣化。谷歌的14,800公里長的洪堡海底光纜將於2026年底在瓦爾帕萊索卸載,屆時聖地亞哥和悉尼之間的往返延遲將減少30毫秒,使智利礦業公司能夠在澳大利亞的分析平台上運行預測性維護模型,而不會出現任何可見的延遲。 2025年初,Cirion Technologies公司運作了一條連接巴西和美國的72Terabit/秒的SAC-2鏈路,將內容傳遞網路的傳輸成本降低了18%。 Meta公司的沃特沃斯計畫在2024年底前實現了巴西境內路徑的多樣化,降低了錨鏈拖曳和地震期間困擾營運商的單點故障(SPOF)風險。新增的頻寬使雲端服務供應商能夠在聖保羅和聖地牙哥等城市部署大規模快取節點,為用戶提供延遲低於 50 毫秒的服務,並將洲際幹線的尖峰時段流量降低約 40%。金融服務公司已為其雙路徑網路配備了容錯能力,以滿足業務永續營運要求,現在可以將其演算法交易引擎遷移到區域性位置。

電網不穩定和電費高企

電力不穩定和收費系統波動仍然是南美超大規模資料中心市場面臨的最嚴峻的短期障礙。 2024年11月,聖保羅的Enel電力公司停電影響了210萬用戶,持續長達72小時,觸發了不可抗力條款,讓租戶暫時中止支付託管費用。同年,阿根廷工業電費在補貼削減後飆升了38%,影響了未簽訂對沖協議的設施的營運利潤率。智利的定價體系雖然更為穩定,但仍比區域平均高出9%,促使運營商協商“可中斷負荷合約”,以15%的折扣換取限制供電的權利。為了維持合約規定的運轉率,聖保羅一個典型的20兆瓦資料中心現在需要安裝25兆瓦的備用發電設施,這需要300萬美元的初始投資和40萬美元的年度維護成本。這種額外的成本阻礙了對延遲敏感的工作負載(例如即時競價引擎)的部署,這些應用程式往往會遷移到北美,因為北美的運轉率是 99.999% 的常態。

細分市場分析

預計2026年至2031年間,超大規模託管市場將以19.54%的年均成長率成長,超過本地資料中心18.94%的預期成長率。這種差異凸顯了南美洲超大規模資料中心市場的結構性變化。超大規模資料中心業者傾向於垂直整合,以便針對人工智慧工作負載對冷卻拓撲進行精細調整,從而導致2025年,本地資料中心支出佔比將達到55.76%。然而,巴西和阿根廷較長的電力供應前置作業時間和價格衝擊正促使大型雲端公司避開長達18個月的待開發區建設週期,轉而透過租賃可在90天內運作的整塊電力資源來規避風險。亞馬遜網路服務(AWS)正是這種策略的體現,該公司在Equinix SP11中租用了5兆瓦電力,用於在維護期間備份其聖保羅雲區域,這表明即使是資金雄厚的公司也優先考慮敏捷性。金融服務公司正在推動託管資料中心的發展。這是因為巴西中央銀行(Banco Central do Brasil)的業務永續營運法規要求主資料中心和災害復原資料中心在地理位置上必須分離,而透過多園區租賃來滿足這項要求比擁有重複的資料中心更具經濟效益。

互連密度的提高增強了託管服務的優勢,將租戶伺服器集中在多個雲端入口、網際網路交換中心和營運商對接機房附近。 Scala 資料中心的一份報告顯示,其 2025 年 42% 的收入將來自交叉連接和對等互聯服務,而非單純的機架租賃,這反映出網路效應如何帶來高入住率和高收入。相較之下,本地部署設施通常選擇房地產成本低 30% 的郊區土地,但有限的光纖線路可能會限制對延遲敏感、需要多重雲端連接的 AI 推理管道。隨著工作負載演變為需要同時存取多個公共雲端的聯邦學習模型,營運商中立的園區互連帶來的溢價將支撐其成長,使其超越託管服務的市場平均水平。因此,南美超大規模資料中心市場似乎正在轉向混合採購模式,將自有容量和租賃容量相結合,即使在超大規模資料超大規模資料中心業者之間也是如此,以便在資本投資紀律和容量獲取速度之間取得平衡。

到2025年,IT硬體仍將維持42.18%的最大支出佔有率,但由於功率密度結構性成長,機械系統預計將以19.62%的複合年成長率位居榜首。 NVIDIA H100等GPU陣列已將機櫃負載推高至30千瓦以上,而能夠處理每個機架45千瓦功率的晶片級冷板和後門式熱交換器如今已成為維修項目的必備設備。電氣設備支出將成長18.7%,因為一個20兆瓦的機房需要25兆瓦的電源連接才能確保N+1冗餘,這將需要對變電站進行升級,費用很容易超過200萬美元。由於營運商擴大從工業地產所有者租賃現有廠房(建築外殼)並安裝模組化閒置頻段套件,而不是開發未開發的土地,因此一般建築成本的成長被限制在18.3%。Schneider Electric最新的預測分析層可最佳化冷卻器運作,以應對人工智慧工作負載的激增,從而減少 12% 的能源浪費。同時,Arista 的 800Gigabit乙太網路脊葉式架構可處理與模型訓練週期相關的東-西向流量高峰。

隨著機架高度從 52U 增加到 60U,機械成本也在上升。這是因為更高的機架需要工程加固、更複雜的線纜管理以及更堅固的氣流控制門。網路升級也是一個重要議題,因為超大規模資料中心業者正在採用Gigabit和Gigabit光纖連接訓練節點。這使得每個機架的光纖數量增加了兩倍,並需要更高靜壓的冷卻風扇。儲存架構向 NVMe over Fabrics 的轉型實現了快閃記憶體池的集中化,並將每Terabyte的成本降低了 18%,但東西向網路負載的增加給冷卻迴路帶來了更大的壓力。機械供應商的定價權越來越大,尤其是在熱交換器核心的前置作業時間延長至 16 週,以及由於全球人工智慧需求,有限的銅和鋁庫存優先供應給一級供應商的情況下。因此,機械設備支出的成長曲線現在已經超過了伺服器更換週期,這與南美洲超大規模資料中心市場的傳統趨勢相反。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模資料中心業者服務商推出的雲端區域數量激增。

- 海底電纜登陸可以改善延遲並提高冗餘度。

- 利用豐富的水力、太陽能和風能資源的可再生能源購電協議

- 《數位主權法案》強制要求本地託管

- 5G開放式無線存取網的部署帶來了微規模和超大規模邊緣技術。

- 鋰礦開採所需的 AI 和 HPC 工作負載需要本地容量

- 市場限制因素

- 電網不穩定和電費高企

- 高壓電氣和機械設備的維護和操作方面缺乏熟練人員。

- 由於缺水,暫停使用蒸發冷卻技術

- 過度依賴一級地區的GPU和光纖通訊資源

- 產業價值鏈分析

- 技術展望

- 宏觀經濟因素對市場的影響

第5章:在超大規模資料中心實施人工智慧(AI)(子章節可能會根據資料可用性而有所變化)

- 人工智慧工作負載的影響:高密度GPU機架的興起與高熱負載管理

- 快速過渡到 400G 和 800G 乙太網路 / 本地 OEM 廠商對整合和相容性的需求

- 液冷技術的創新:浸沒式冷卻和冷板的發展趨勢

- 實施基於人工智慧的資料中心管理 (DCIM) / 雲端供應商的角色

第6章 監理與合規框架

第7章:主要資料中心統計數據

- 南美洲現有超大規模資料中心設施(單位:兆瓦)(超大規模自建資料中心與託管資料中心)

- 南美洲計劃建設的超大規模資料中心列表

- 南美洲超大規模資料中心營運商列表

- 南美洲資料中心資本支出(CAPEX)分析

第8章 市場規模與成長預測

- 依資料中心類型

- 超大規模自建

- 超大規模資料中心託管

- 按組件

- IT基礎設施

- 伺服器基礎架構

- 儲存基礎設備

- 網路基礎設施

- 電力基礎設施

- 配電單元

- 傳輸開關和開關設備

- UPS系統

- 發電機

- 其他電力基礎設施

- 機械設備

- 冷卻系統

- 架子

- 其他機械和設備

- 一般建築

- 核心和外殼開發

- 安裝和試運行服務

- 設計工程

- 火災偵測、消防和物理安全

- DCIM/BMS解決方案

- IT基礎設施

- 等級標準

- Tier III

- Tier IV

- 按資料中心規模

- 大型(25兆瓦或以下)

- 大型(25兆瓦至60兆瓦以上)

- 兆瓦級(超過 60 兆瓦)

- 國家

- 巴西

- 智利

- 哥倫比亞

- 阿根廷

- 秘魯

- 南美洲其他地區

第9章 競爭情勢

- 市佔率分析

- 公司簡介

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Digital Realty(Ascenty)

- Equinix Inc.

- Scala Data Centers

- ODATA

- EdgeConneX

- Cirion Technologies

- NTT Global Data Centers

- Vantage Data Centers LLC

- Kio Networks

- Lumen Technologies

- IBM(Kyndryl)

- Oracle Corporation

- Tencent Holdings Ltd.

- Alibaba Group Holding Ltd.

- TIVIT

- Sonda SA

- Ativy Data Centers

- InterNexa

第10章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

The South America hyperscale data center market size is expected to increase from USD 5.66 billion in 2025 to USD 6.69 billion in 2026 and reach USD 15.92 billion by 2031, growing at a CAGR of 18.94% over 2026-2031.

Rapid cloud-region roll-outs, new sub-sea cables, and abundant renewable-energy contracts combine to accelerate capital deployment across every major metro. Hyperscalers continue to build proprietary campuses, yet colocation providers are winning incremental megawatts by shortening time-to-production and diversifying grid exposure for clients that demand uninterrupted service. Data-sovereignty rules introduced in Brazil, Argentina, and Colombia require personal and public-sector data to remain on domestic soil, which effectively locks a rising share of workloads inside the South America hyperscale data center market. Simultaneously, GPU-rich artificial-intelligence clusters are lifting rack power densities beyond 30 kilowatts, forcing operators to invest aggressively in liquid-cooling and heat-exchanger retrofits that reshape mechanical-infrastructure budgets. Key drivers of revenue growth include hyperscaler self-build programs, cross-connect-centric business models inside carrier-neutral campuses, and renewable power purchase agreements that offer 12%-plus discounts relative to regulated tariffs. Challenges remain in the form of grid unreliability, a shortage of high-voltage technicians, and water-stress moratoria that restrict evaporative cooling in certain jurisdictions. Even so, mega campuses above 60 megawatts unlock operating leverage by centralizing substations, chilled-water plants, and fiber rings across a larger denominator of capacity. Competitive intensity sits at a moderate level because the top five providers account for about 62% of total installed megawatts, leaving meaningful headroom for regional specialists and edge-focused entrants to differentiate through local utility relationships, bilingual support teams, and next-generation liquid-cooling deployments.

South America Hyperscale Data Center Market Trends and Insights

Surge in Cloud-Region Launches by Hyperscalers

Aggressive cloud-region roll-outs anchor the strongest single catalyst for the South America hyperscale data center market. Amazon Web Services committed USD 4 billion to a Santiago cloud region that opens with 12 availability zones and an expandable 40-to-80-megawatt footprint, drawing software vendors that need single-digit-millisecond latency to operate payment engines and augmented-reality shopping carts. Microsoft mirrored the move with Azure zones in the same metro, while Google cut per-core pricing by 22% after enabling its M8g Arm-based instances in Sao Paulo. These flagship deployments trigger demand for adjacent colocation because independent software vendors must install application servers inside identical availability spheres to meet stringent service-level objectives. The loop closes when enterprises sign cross-connects to hyperscaler on-ramps, which in turn drives occupancy rates above 85% in Sao Paulo's Vila Olimpia cluster and Santiago's Quilicura corridor. Newly issued Brazilian regulations that classify sovereign workloads further lock in domestic hosting, ensuring the cloud-build momentum sustains through the medium term.

Sub-Sea Cable Landings Enhancing Latency and Redundancy

A second catalyst flows from trans-Pacific and north-south sub-sea fiber investments that drop latency and diversify fail-over paths. Google's 14,800-kilometer Humboldt cable will reduce Santiago-Sydney round-trip delay by 30 milliseconds when it lands in Valparaiso during late 2026, enabling Chilean mining firms to run predictive-maintenance models on Australian analytics platforms with no perceptible lag. Cirion Technologies activated the 72-terabit-per-second SAC-2 link between Brazil and the United States in early 2025, cutting transit charges for content-delivery networks by 18%. Meta's Project Waterworth diversified Brazilian routes in late 2024, reducing single-point-of-failure risk that previously plagued operators during anchor drag or seismic events. The new bandwidth lets cloud providers place larger cache nodes inside Sao Paulo and Santiago, serving consumers with sub-50-millisecond latency and stripping nearly 40% of peak-hour traffic from transcontinental trunks. Financial-services firms now gain dual-path network resilience that fulfils business-continuity mandates and nudges algorithmic-trading engines into regional halls.

Grid Unreliability and High Electricity Tariffs

Power instability and volatile tariffs remain the most acute short-term drag on the South America hyperscale data center market. Enel's November 2024 outage in Sao Paulo left 2.1 million customers without electricity for up to 72 hours, invoking force-majeure clauses that allowed tenants to suspend colocation payments. Industrial tariffs in Argentina jumped 38% during the same year after subsidy reductions, squeezing operating margins for facilities lacking hedged contracts. Chile's tariff regime is more stable, yet still commands a 9% premium over regional averages, prompting operators to negotiate interruptible-load deals that trade curtailment rights for 15% discounts. To maintain contractual uptime, a typical 20-megawatt hall in Sao Paulo now deploys 25 megawatts of on-site generation, which adds USD 3 million in up-front capex and USD 400,000 in recurring annual maintenance. The added expense deters latency-sensitive workloads such as real-time bidding engines, nudging those applications toward North American regions where five-nines uptime is standard.

Other drivers and restraints analyzed in the detailed report include:

- Renewable PPAs Leveraging Abundant Hydro-Solar-Wind

- Digital-Sovereignty Laws Mandating Local Hosting

- Skilled-Talent Shortage in HV Electrical and Mechanical O&M

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hyperscale colocation is forecast to expand at 19.54% during 2026-2031, surpassing the 18.94% pace set for self-build campuses, and this divergence underpins a structural shift inside the South America hyperscale data center market. Self-build designs captured 55.76% of 2025 spending because hyperscalers prefer vertical integration that lets them fine-tune cooling topologies for AI workloads. Even so, extended utility lead times and tariff shocks in Brazil and Argentina have persuaded cloud majors to hedge with leased hall blocks that can be activated within 90 days, sidestepping the 18-month greenfield timeline. Amazon Web Services exemplified this approach by reserving 5 megawatts within Equinix SP11 to backstop its Sao Paulo cloud region during maintenance windows, demonstrating that even capital-rich players value agility. Financial-services firms bolster colocation growth because Banco Central do Brasil's operational-resilience rules stipulate geographic separation between primary and disaster-recovery footprints, a requirement most economically met through multi-campus leasing rather than proprietary duplication.

Interconnection density amplifies colocation's edge by clustering tenant servers near multiple cloud on-ramps, internet exchanges, and carrier meet-me rooms. Scala Data Centers reported that 42% of 2025 revenue originated from cross-connects and peering services rather than pure rack rental, reflecting how network effects create sticky occupancy and premium yields. By contrast, self-build estates often select ex-urban land parcels where real-estate costs are 30% lower but fiber routes limited, which can constrain latency-sensitive AI inference pipelines that require multi-cloud federation. As workloads evolve toward federated learning models demanding simultaneous access to multiple public clouds, the interconnection premium inside carrier-neutral campuses will likely sustain colocation's above-market growth. Consequently, the South America hyperscale data center market appears to be tilting toward a hybrid procurement mix in which even hyperscalers blend owned and leased capacity to balance capex discipline with speed-to-capacity.

IT hardware retained the largest 42.18% share of 2025 expenditure, yet mechanical systems are positioned for the fastest 19.62% CAGR because power density continues its structural climb. GPU arrays such as NVIDIA H100 already drive cabinet loads beyond 30 kilowatts, and direct-to-chip cold plates or rear-door heat exchangers capable of 45 kilowatts per rack are now mandatory for retrofit projects. Electrical outlays rise at 18.7% because a 20-megawatt hall needs a 25-megawatt utility connection to guarantee N+1 redundancy, which requires substation upgrades that easily exceed USD 2 million. General construction lags at 18.3% because operators increasingly lease pre-built shells from industrial landlords, deploying modular white-space kits rather than breaking raw ground. Schneider Electric's latest predictive-analytics layer synchronizes chiller sequencing with AI workload surges, trimming energy waste by 12%, while Arista's 800-gigabit Ethernet spine-leaf fabrics handle east-west traffic bursts that accompany model training cycles.

Rising rack heights to 52U and even 60U further shift mechanical bills because taller frames require engineered bracing, expanded cable management, and heavier-duty airflow doors. Network upgrades form an allied theme as hyperscalers adopt 400-gigabit and 800-gigabit optics to link training nodes, which triples fiber count per rack and necessitates higher static-pressure cooling fans. Storage architecture transformation toward NVMe-over-Fabrics has centralized flash pools, reducing per-terabyte cost by 18%, yet the heavier east-west network load places added stress on cooling loops. Mechanical suppliers gain pricing power as lead times for heat-exchanger cores stretch to 16 weeks, particularly when global AI demand funnels limited copper and aluminum inventory into Tier-1 regions first. The overall result is a mechanical-spend growth curve that now exceeds server refresh trajectories, a reversal of historic patterns inside the South America hyperscale data center market.

The South America Hyperscale Data Center Market Report is Segmented by Data Center Type (Hyperscale Self-Build, and Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction), Tier Standard (Tier III, and Tier IV), Data Center Size (Large, Massive, and Mega), and Country(Brazil, Chile, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Digital Realty (Ascenty)

- Equinix Inc.

- Scala Data Centers

- ODATA

- EdgeConneX

- Cirion Technologies

- NTT Global Data Centers

- Vantage Data Centers LLC

- Kio Networks

- Lumen Technologies

- IBM (Kyndryl)

- Oracle Corporation

- Tencent Holdings Ltd.

- Alibaba Group Holding Ltd.

- TIVIT

- Sonda S.A.

- Ativy Data Centers

- InterNexa

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Cloud-Region Launches by Hyperscalers

- 4.2.2 Sub-Sea Cable Landings Enhancing Latency and Redundancy

- 4.2.3 Renewable PPAs Leveraging Abundant Hydro-Solar-Wind

- 4.2.4 Digital-Sovereignty Laws Mandating Local Hosting

- 4.2.5 5G Open-RAN Roll-Outs Spawning Micro-Hyperscale Edge

- 4.2.6 Lithium-Mining AI and HPC Workloads Needing Local Capacity

- 4.3 Market Restraints

- 4.3.1 Grid Unreliability and High Electricity Tariffs

- 4.3.2 Skilled-Talent Shortage in HV Electrical and Mechanical O&M

- 4.3.3 Water-Stress Moratoria on Evaporative Cooling

- 4.3.4 GPU or Optic Allocation Bias Toward Tier-1 Regions

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-Segments are Subject to Change Depending on Availability of Data)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in South America (in MW) (Hyperscale Self-Build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in South America

- 7.3 List of Hyperscale Data Center Operators in South America

- 7.4 Analysis on Data Center CAPEX in South America

8 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Units

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning Services

- 8.2.4.3 Design Engineering

- 8.2.4.4 Fire Detection, Suppression and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By Data Center Size

- 8.4.1 Large ( Less than or equal to 25 MW)

- 8.4.2 Massive (Greater than 25 MW and Less than equal to 60 MW)

- 8.4.3 Mega (Greater than 60 MW)

- 8.5 By Country

- 8.5.1 Brazil

- 8.5.2 Chile

- 8.5.3 Colombia

- 8.5.4 Argentina

- 8.5.5 Peru

- 8.5.6 Rest of South America

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Google LLC

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Digital Realty (Ascenty)

- 9.2.6 Equinix Inc.

- 9.2.7 Scala Data Centers

- 9.2.8 ODATA

- 9.2.9 EdgeConneX

- 9.2.10 Cirion Technologies

- 9.2.11 NTT Global Data Centers

- 9.2.12 Vantage Data Centers LLC

- 9.2.13 Kio Networks

- 9.2.14 Lumen Technologies

- 9.2.15 IBM (Kyndryl)

- 9.2.16 Oracle Corporation

- 9.2.17 Tencent Holdings Ltd.

- 9.2.18 Alibaba Group Holding Ltd.

- 9.2.19 TIVIT

- 9.2.20 Sonda S.A.

- 9.2.21 Ativy Data Centers

- 9.2.22 InterNexa

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment

超大規模資料中心市場:按組件、電力容量、冷卻方式、所有權類型、部署模式、應用和最終用戶產業分類-2026-2032年全球市場預測

超大規模資料中心市場:按組件、電力容量、冷卻方式、所有權類型、部署模式、應用和最終用戶產業分類-2026-2032年全球市場預測 德國超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年)

德國超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年) 全球超大規模資料中心市場:機會與策略展望(至2035年)

全球超大規模資料中心市場:機會與策略展望(至2035年) 超級資料中心市場規模、佔有率和趨勢分析報告:按解決方案、資料中心類型、冷卻技術、地區和細分市場預測(2026-2033 年)

超級資料中心市場規模、佔有率和趨勢分析報告:按解決方案、資料中心類型、冷卻技術、地區和細分市場預測(2026-2033 年) 超級資料中心市場分析與預測(至2035年):依類型、產品、服務、技術、元件、應用、部署方式、最終使用者、功能及安裝方式分類

超級資料中心市場分析與預測(至2035年):依類型、產品、服務、技術、元件、應用、部署方式、最終使用者、功能及安裝方式分類 超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季)

超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季) 超級資料中心市場:按組件、最終用戶、行業和地區分類(2026-2034 年)

超級資料中心市場:按組件、最終用戶、行業和地區分類(2026-2034 年) 超大規模資料中心全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

超大規模資料中心全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 超大規模資料中心市場:按IT基礎設施、電氣基礎設施、機械基礎設施、一般建築和區域分類

超大規模資料中心市場:按IT基礎設施、電氣基礎設施、機械基礎設施、一般建築和區域分類