|

市場調查報告書

商品編碼

2073389

德國超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年)Germany Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

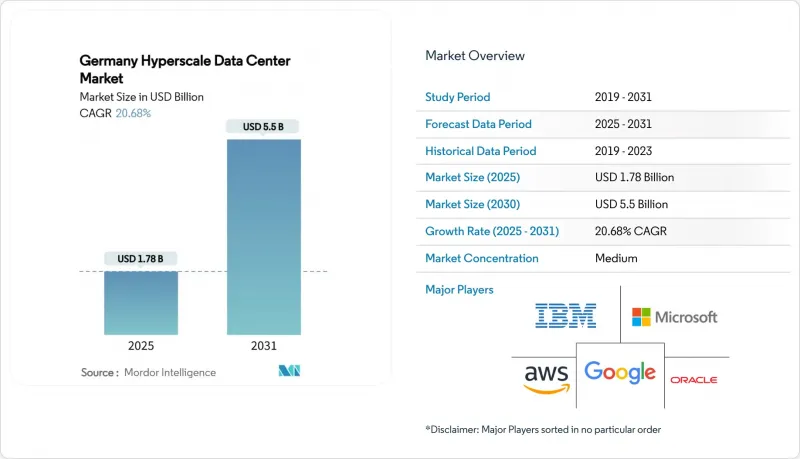

根據 Mordor Intelligence 預測,德國超大規模資料中心市場規模預計將在 2025 年達到 178151 億美元,到 2031 年達到 550328 億美元,複合年成長率為 20.68%。

同時,IT 容量預計將從 2025 年的 2,451.07 兆瓦成長到 2031 年的 3,942.78 兆瓦,複合年成長率為 8.24%。

本報告按資料中心類型(超大規模自建資料中心、超大規模託管資料中心)、元件(IT基礎設施、電力基礎架構等)、等級(Tier III、Tier IV)、最終用戶產業(雲端運算與IT服務、電信等)、資料中心規模(大型、超大型、巨型)以及國家/地區進行細分。市場預測以價值(美元)和規模(兆瓦)表示。

德國超大規模資料中心市場的趨勢與洞察

AI/ML(主要是GPU,功率超過50千瓦)機架密度快速成長

目前,大多數人工智慧訓練叢集的機架功耗超過 50 千瓦,因此對於 NVIDIA H100 的部署而言,風冷已不再實用。微軟斥資 32 億歐元(約 37.3 億美元)的專案凸顯了資料中心建置模式的轉變,即從以儲存為中心的資料中心轉向以運算為導向的資料中心,後者需要採用晶片級直接冷卻或浸沒式冷卻。營運商正在將配電系統維修到 415 伏特三相拓撲結構,而 UPS 供應商則正在部署高速回應模組來應對 GPU 的突發負載。 Northern Data 部署的 19,000 個 H100 GPU 清楚地表明了人工智慧資料中心所需的高額資本支出 (Capex)。雖然高昂的價格和更高的密度帶來了更高的毛利率潛力,但也增加了整個德國超大規模資料中心市場的工程複雜性。

主權雲端合規性(GDPR、BSI C5)正在落實中。

德國的數位主權議程要求公共部門工作負載必須獲得 BSI C5 認證和資料居住保證。 T-Systems 基於 Google Cloud 建構的 Sovereign Cloud 展示了合規性資本投資如何轉化為競爭優勢。 NIS-2 的實施將網路彈性義務擴展到數千家營運商,並加強了營運查核點。雖然獲得認證的成本會延長專案工期,但合規站點可以確保更高的獲利能力,這使得合規性成為德國超大規模資料中心市場日益重要的需求促進因素。

蒸發冷卻用水量的上限

歐盟永續發展法規要求揭露用水量,尤其關注日均用水量,大型設施的每日平均用水量可達500萬加侖。根據DENEFF的一項調查,56%的業者認為熱能再利用需求較低,這限制了水資源利用效率與熱效率之間的綜效。都市區更嚴格的用水量限制迫使營運商轉向封閉回路型絕熱或液冷系統,但這些系統初始成本高且運作難度較大,對德國超大規模資料中心市場構成挑戰。

細分市場分析

預計到2024年,超大規模託管服務將佔總收入的52%,反映出企業尋求具備容錯能力的承包解決方案的趨勢日益成長。然而,在德國超大規模資料中心市場,由於大型雲端公司對人工智慧和主權工作負載的架構控制需求增加,超超大規模資料中心業者營運商的本地自建資料中心目前正以12.8%的複合年成長率快速成長。不斷加速的專案儲備正在推動德國超大規模資料中心市場的發展,AWS、微軟和Oracle公司已在客製化園區建設方面投入數十億美元。

我們自建的設施採用了晶片級直接冷卻、400G 光纖網路和客製化電源路由,這些在託管機房中很少預先安裝。相較之下,現有的託管服務供應商則透過客製化模組、自主雲端環境和靈活的所擁有土地來應對這項挑戰。這兩種發展趨勢正在緩解需求波動,並擴展德國超大規模資料中心產業的服務範圍。

到2024年, IT基礎設施將佔總收入的41.2%,並推動該細分市場以14.6%的複合年成長率成長,這主要得益於GPU伺服器叢集取代了以儲存為中心的機架。在德國超大規模資料中心市場,伺服器節點的市場規模超過了冷卻器和發電機,而訓練工作負載則佔據了大部分資本支出(CAPEX)。

電氣設備也隨之發展。隨著機架密度的提高,對415V母線槽、高速傳輸開關和鋰離子UPS的需求也在成長。機械設備的投資正轉向液冷迴路和後門式熱交換器,儘管傳統的冷水機組仍然是低密度機房的基礎。物料清單(BOM)的演變推高了德國超大規模資料中心市場的平均專案價值,同時供應商的專業化程度也在提高。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AI/ML(主要是GPU,功率超過50千瓦)機架密度快速成長

- 建構主權雲端合規性(GDPR、BSI C5)

- 即時結算和央行數位貨幣延遲要求

- 以城域樞紐為中心的5G邊緣與核心網路融合

- GenAI推理叢集需要水冷

- 基於運轉率的可再生能源購電協議(PPA)用於容量對沖

- 市場限制因素

- 蒸發冷卻用水量的上限

- GPU和光元件供應鏈出現供不應求。

- 因強制餘熱再利用而增加的資本支出(法案草案)

- 二線城市併網容量超過30兆瓦的限制

- 價值供應鏈分析

- 技術展望

第5章:在超大規模資料中心實施人工智慧(AI)(子章節內容可能會根據最新資料而有所變更)

- 人工智慧工作負載的影響:高密度GPU機架的興起與高熱負載管理

- 快速過渡到 400G 和 800G 乙太網路——本地 OEM 廠商的整合和相容性要求

- 液冷技術的創新:浸沒式冷卻和冷板的發展趨勢

- 實施人工智慧驅動的資料中心管理 (DCIM)-雲端提供者的角色

第6章 監理與合規框架

第7章 資料中心關鍵統計數據

- 德國現有超大規模資料中心設施(單位:兆瓦)(超大規模自建資料中心與託管資料中心)

- 德國計劃建造的超大規模資料中心清單

- 德國超大規模資料中心營運商列表

- 德國資料中心資本支出(CAPEX)分析

第8章 市場規模與成長預測

- 依資料中心類型

- 超大規模自建

- 超大規模資料中心託管

- 按組件

- IT基礎設施

- 伺服器基礎架構

- 儲存基礎設備

- 網路基礎設施

- 電力基礎設施

- 配電單元

- 傳輸開關和開關設備

- UPS系統

- 發電機

- 其他電力基礎設施

- 機械基礎設施

- 冷卻系統

- 架子

- 其他機械基礎設施

- 一般建築

- 核心和外殼開發

- 安裝和試運行

- 設計與工程

- 火災偵測和物理安全

- DCIM/BMS解決方案

- IT基礎設施

- 基於層級的標準

- Tier III

- Tier IV

- 按最終用戶行業分類

- 雲端和IT服務

- 溝通

- 媒體與娛樂

- 政府

- BFSI

- 製造業

- 電子商務

- 其他最終用戶

- 按資料中心規模

- 大型(25兆瓦或以下)

- 超大型(超過 25 兆瓦但少於 60 兆瓦)

- 兆瓦級(超過 60 兆瓦)

- 按地區

- 法蘭克福/萊茵-美因

- 柏林/勃蘭登堡

- 慕尼黑/巴伐利亞

- 漢堡/北部

- 北萊茵-威斯特法倫州(杜塞爾多夫-科隆)

第9章 競爭情勢

- 市佔率分析

- 公司簡介

- Amazon Web Services

- Microsoft Corporation

- Alphabet Inc.(Google)

- Meta Platforms Inc.

- Oracle Corporation

- International Business Machines Corp.

- Alibaba Group Holding Ltd.

- Tencent Holdings Ltd.

- Baidu Inc.

- Digital Realty(Interxion)

- Equinix Inc.

- NTT Global Data Centers(e-Shelter)

- CyrusOne Inc.

- Vantage Data Centers

- Quality Technology Services(QTS)

- STACK Infrastructure

- Iron Mountain Data Centers

- Maincubes One GmbH

- Hetzner Online GmbH

- OVHcloud

- Data4 Group

- GDS Holdings Ltd.

- CoreWeave Inc.

- Flexential Corp.

第10章 市場機會與未來展望

- 評估閒置頻段和未滿足的需求

According to Mordor Intelligence, the germany hyperscale data center market size stands at USD 1,781.51 million in 2025 and is projected to reach USD 5,503.28 million by 2031 at a 20.68% CAGR, while installed IT capacity is set to expand from 2,451.07 MW in 2025 to 3,942.78 MW by 2031 at an 8.24% CAGR.

This report is Segmented by Data Center Type (Hyperscale Self-Build, Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, and More), Tier Standard (Tier III, Tier IV), End-User Industry (Cloud and IT Services, Telecom, and More), Data Center Size (Large, Massive, Mega), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (MW).

Germany Hyperscale Data Center Market Trends and Insights

Surging GPU-centric AI/ML rack densities ( Greater than 50 kW)

Rack power envelopes now exceed 50 kW in most AI training clusters, rendering air cooling impractical for NVIDIA H100 deployments. Microsoft's EUR 3.2 billion (USD 3.73 billion) programme underscores the pivot from storage-heavy builds to compute-optimized halls that demand direct-to-chip or immersion cooling. Operators are retrofitting distribution to 415 V three-phase topologies, while UPS vendors introduce fast-response modules to manage GPU burst loads. Northern Data's roll-out of 19,000 H100 GPUs exemplifies the capex premium attached to AI-ready halls Premium price points and density gains widen gross-margin potential but raise engineering complexity across the Germany hyperscale data center market.

Sovereign-cloud compliance (GDPR, BSI C5) builds

Germany's digital-sovereignty agenda makes BSI C5 attestation and data-residency guarantees compulsory for public-sector workloads. T-Systems' Sovereign Cloud powered by Google Cloud shows how compliance capital spend turns into a competitive moat NIS-2 implementation expands cyber-resilience obligations to thousands of operators, tightening operational checkpoints. Certification overheads lengthen project schedules but let compliant sites command higher yields, cementing compliance as a demand driver within the Germany hyperscale data center market.

Water-use caps on evaporative cooling

EU sustainability rules now compel water-use disclosure, spotlighting daily consumption that can hit 5 million gallons at large sites DENEFF's survey shows 56% of operators see weak demand for heat-reuse, limiting synergy between water and thermal efficiency. Urban water caps tighten allowable draw, pushing operators toward closed-loop adiabatic or liquid systems that cost more upfront and lift the operational hurdle in the Germany hyperscale data center market.

Other drivers and restraints analyzed in the detailed report include:

- Real-time payment and CBDC latency mandates

- 5G edge-core consolidation around metro hubs

- GPU/optics supply-chain shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hyperscale colocation controlled 52% revenue in 2024, reflecting entrenched enterprise preference for turnkey resilience. However, the Germany hyperscale data center market now sees hyperscaler self-builds expanding at 12.8% CAGR as cloud majors seek architectural control for AI and sovereignty workloads. The accelerating pipeline lifts the Germany hyperscale data center market as AWS, Microsoft, and Oracle commit multibillion budgets to bespoke campuses.

Self-builds embed direct-to-chip cooling, 400 G fabric and custom power paths that colocation shells seldom pre-install. Colocation incumbents respond with build-to-suit modules, sovereign-cloud enclaves and flexible land banks. This two-track growth cushions demand volatility and broadens service menus across the Germany hyperscale data center industry.

IT infrastructure delivered 41.2% of 2024 revenue, leading segment growth at 14.6% CAGR as GPU server clusters displace storage-centric racks. The Germany hyperscale data center market size for server nodes outpaces chillers and generators as training workloads dominate capex.

Electrical gear follows closely: 415 V busways, fast-transfer switchgear and lithium-ion UPS units rise in tandem with rack density. Mechanical spend migrates toward liquid loops and rear-door exchangers, though legacy chilled-water plants still underpin lower-density halls. The evolving bill-of-materials lifts average project value in the Germany hyperscale data center market while deepening vendor specialization.

Complete Report Scope:

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design and Engineering

- Fire Detection and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT Services

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

- By Geography

- Frankfurt / Rhein-Main

- Berlin / Brandenburg

- Munich / Bavaria

- Hamburg / North

- NRW (Dusseldorf-Cologne)

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Alphabet Inc. (Google)

- Meta Platforms Inc.

- Oracle Corporation

- International Business Machines Corp.

- Alibaba Group Holding Ltd.

- Tencent Holdings Ltd.

- Baidu Inc.

- Digital Realty (Interxion)

- Equinix Inc.

- NTT Global Data Centers (e-Shelter)

- CyrusOne Inc.

- Vantage Data Centers

- Quality Technology Services (QTS)

- STACK Infrastructure

- Iron Mountain Data Centers

- Maincubes One GmbH

- Hetzner Online GmbH

- OVHcloud

- Data4 Group

- GDS Holdings Ltd.

- CoreWeave Inc.

- Flexential Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging GPU-centric AI/ML rack densities (>50 kW)

- 4.2.2 Sovereign-cloud compliance (GDPR, BSI C5) builds

- 4.2.3 Real-time payment and CBDC latency mandates

- 4.2.4 5G edge-core consolidation around metro hubs

- 4.2.5 GenAI inference clusters needing liquid cooling

- 4.2.6 Availability-based renewable PPAs for capacity hedge

- 4.3 Market Restraints

- 4.3.1 Water-use caps on evaporative cooling

- 4.3.2 GPU/optics supply-chain shortages

- 4.3.3 Heat-reuse mandate increasing CapEx (draft law)

- 4.3.4 Grid-connection curtailment greater than 30 MW in Tier-2 cities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-segments are subject to change depending on Data Recency)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet - Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption - Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in Germany (in MW) (Hyperscale Self build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in Germany

- 7.3 List of Hyperscale Data Center Operators in Germany

- 7.4 Analysis on Data Center CAPEX in Germany

8 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Unit

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning

- 8.2.4.3 Design and Engineering

- 8.2.4.4 Fire Detection and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By End-User Industry

- 8.4.1 Cloud and IT Services

- 8.4.2 Telecom

- 8.4.3 Media and Entertainment

- 8.4.4 Government

- 8.4.5 BFSI

- 8.4.6 Manufacturing

- 8.4.7 E-Commerce

- 8.4.8 Other End User

- 8.5 By Data Center Size

- 8.5.1 Large (Less than equal to 25 MW)

- 8.5.2 Massive (Greater than 25 MW and less than equal to 60 MW)

- 8.5.3 Mega (Greater than 60 MW)

- 8.6 By Geography

- 8.6.1 Frankfurt / Rhein-Main

- 8.6.2 Berlin / Brandenburg

- 8.6.3 Munich / Bavaria

- 8.6.4 Hamburg / North

- 8.6.5 NRW (Dusseldorf-Cologne)

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Alphabet Inc. (Google)

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Oracle Corporation

- 9.2.6 International Business Machines Corp.

- 9.2.7 Alibaba Group Holding Ltd.

- 9.2.8 Tencent Holdings Ltd.

- 9.2.9 Baidu Inc.

- 9.2.10 Digital Realty (Interxion)

- 9.2.11 Equinix Inc.

- 9.2.12 NTT Global Data Centers (e-Shelter)

- 9.2.13 CyrusOne Inc.

- 9.2.14 Vantage Data Centers

- 9.2.15 Quality Technology Services (QTS)

- 9.2.16 STACK Infrastructure

- 9.2.17 Iron Mountain Data Centers

- 9.2.18 Maincubes One GmbH

- 9.2.19 Hetzner Online GmbH

- 9.2.20 OVHcloud

- 9.2.21 Data4 Group

- 9.2.22 GDS Holdings Ltd.

- 9.2.23 CoreWeave Inc.

- 9.2.24 Flexential Corp.

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment

超大規模資料中心市場:按組件、電力容量、冷卻方式、所有權類型、部署模式、應用和最終用戶產業分類-2026-2032年全球市場預測

超大規模資料中心市場:按組件、電力容量、冷卻方式、所有權類型、部署模式、應用和最終用戶產業分類-2026-2032年全球市場預測 全球超大規模資料中心市場:機會與策略展望(至2035年)

全球超大規模資料中心市場:機會與策略展望(至2035年) 超級資料中心市場規模、佔有率和趨勢分析報告:按解決方案、資料中心類型、冷卻技術、地區和細分市場預測(2026-2033 年)

超級資料中心市場規模、佔有率和趨勢分析報告:按解決方案、資料中心類型、冷卻技術、地區和細分市場預測(2026-2033 年) 超級資料中心市場分析與預測(至2035年):依類型、產品、服務、技術、元件、應用、部署方式、最終使用者、功能及安裝方式分類

超級資料中心市場分析與預測(至2035年):依類型、產品、服務、技術、元件、應用、部署方式、最終使用者、功能及安裝方式分類 超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季)

超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季) 超級資料中心市場:按組件、最終用戶、行業和地區分類(2026-2034 年)

超級資料中心市場:按組件、最終用戶、行業和地區分類(2026-2034 年) 超大規模資料中心全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

超大規模資料中心全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 超大規模資料中心市場:按IT基礎設施、電氣基礎設施、機械基礎設施、一般建築和區域分類超大規模資料中心市場分析及預測(至2035年):按類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶和解決方案分類

超大規模資料中心市場:按IT基礎設施、電氣基礎設施、機械基礎設施、一般建築和區域分類超大規模資料中心市場分析及預測(至2035年):按類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶和解決方案分類