|

市場調查報告書

商品編碼

2044097

義大利超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Italy Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

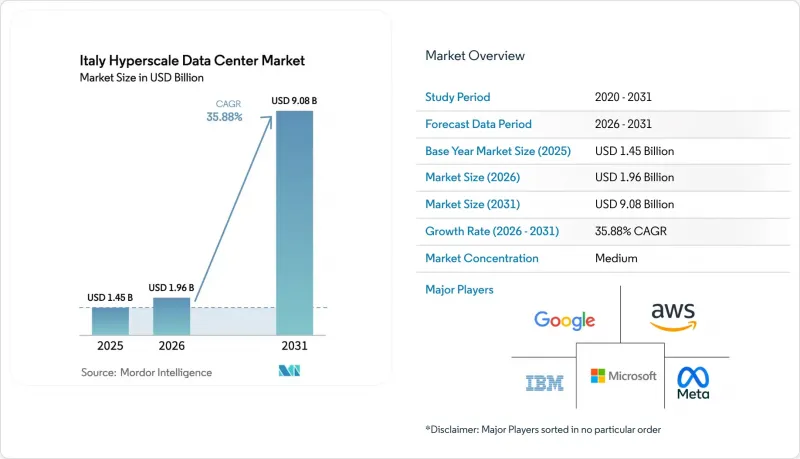

預計義大利超大規模資料中心市場將從 2025 年的 14.5 億美元成長到 2026 年的 19.6 億美元,到 2031 年達到 90.8 億美元,2026 年至 2031 年的複合年成長率為 35.88%。

歐盟的「數位十年」計畫強制要求建設主權雲端基礎設施,義大利國家復甦與韌性計畫提供的巨額津貼,以及美國超大規模資料中心業者加速推出雲端區域,共同推動了米蘭和羅馬新增雲端容量的累積。隨著海底光纜在西西里島的登陸,義大利南部正被重新定位為通往北非的低延遲門戶,而生成式人工智慧叢集的激增正推動機架密度超過40kW,並加速向晶片級液冷(DTC)技術的過渡。開發商在施工前兩年就鎖定電網容量,以規避Lombardia的電力供應限制,並通常同時簽訂長期可再生能源購電協議,將電價控制在每兆瓦時50歐元以下。符合Gaia-X和Tier IV標準的未開發空間的預租競爭日益激烈,使得承包託管園區比自建項目擁有提前前置作業時間的優勢。

義大利超大規模資料中心市場的趨勢與洞察

AWS、微軟 Azure 和谷歌雲端的雲端區域正在快速擴張

為了滿足GDPR的地理位置要求和DORA的彈性規則,各大雲端服務供應商正在加速在米蘭和羅馬建造多可用區。 AWS計畫在2029年向其米蘭區域投資12億歐元,而微軟則在義大利北部投資43億歐元。每個項目將新增三個或更多區域,並透過低於10毫秒的光纖連接進行互連。 Oracle在Oracle的第二個雲端區域已於2025年底啟用,這拓寬了競爭格局,並產生了生態系統效應,例如託管服務供應商預租了毗鄰超大規模資料中心業者中心入口的機房。這種整合縮短了開關設備、發電機和預製液冷迴路的採購週期,部分機械設備包的前置作業時間甚至縮短至40週以內。 DATA4的MIL02園區也體現了租戶的迫切需求,園區首期15兆瓦裝置容量的60%在基礎工程開始前就已經完成了預租。

部署一條新的海底電纜,該電纜將在西西里島登陸。

Sparkle公司的Unitirreno系統於2025年10月投入運作,該系統包含24對光纖電纜。這使得米蘭和突尼斯之間的往返延遲從45毫秒降低到15毫秒以內,使巴勒莫只需一次躍點即可接入北非的交通流。該電纜與Terna公司1000兆瓦的「第勒尼安連接線」高壓直流互連線路平行,為西西里島基地提供充足的頻寬和清潔能源。卡塔尼亞附近的邊緣節點已能在20毫秒的嚴格要求下處理海洋感測器資料和無人機影像,而這些應用場景如果走米蘭線路則無法實現。開發商如果能在巴勒莫登陸站附近的150千伏變電站獲得20-30兆瓦的電力,即可利用太陽能支援的購電協議(PPA)來維持營運成本不變,同時也能將Lombardia的土地價格控制在一半以下。

Lombardia和Lazio電網可用容量的限制

Telna警告稱,到2028年,當資料中心累積需求超過500兆瓦時,米蘭和羅馬周邊變電站可能出現150兆瓦的電力缺口。目前,開發商會在開工前18至24個月鎖定配電容量,在某些情況下,預付併網費用會使土地成本上漲10%至15%。 Vantage Data Centers已在其MXP2資料中心預購了96兆瓦的容量,以確保分階段擴容,從而承擔了這部分額外成本。錯過配電容量分配的業者將不得不投資建造現場電池儲能系統,或接受限電處罰,這將影響服務水準保證。

細分市場分析

截至2025年,自建園區佔據了義大利超大規模資料中心市場佔有率的絕大部分(61.73%)。然而,承包閒置頻段的高資本效率正促使超大規模資料中心業者轉向第三方機房,這些機房能夠在不增加其資產負債表負擔的情況下提供同等的安全環境。預計到2031年,義大利託管機房的超大規模資料中心市場將以36.73%的複合年成長率成長。 MXP2第一期計畫(裝置容量32兆瓦)的啟動為這一成長趨勢提供了支撐,該計畫甚至在基礎建設開始前就吸引了兩家大型雲端公司和一家政府機構進駐。與自建待開發區設施相比,這些早期合約將產品上市時間縮短了一年,使企業能夠更快地部署人工智慧推理工作負載。

在需要客製化熱通道配置或專用光纖網路的場景中,本地部署仍然普遍存在。例如, Oracle位於都靈的資料中心就直接與 TIM 的骨幹網路整合,從而實現了穩定的吞吐量。儘管如此,託管服務供應商仍承擔著液冷系統的高昂前期成本,這使得租戶無需額外投資即可擴展 60kW 機架。這種轉變刺激了金融科技和 SaaS 公司的需求,這些公司原本會將培訓業務遷至法蘭克福,從而擴大了它們在義大利超大規模資料中心市場叢集中的地理覆蓋範圍。

預計到2025年,受高密度GPU伺服器的影響, IT基礎設施將佔據52.88%的市場佔有率;而機械系統預計將以36.84%的複合年成長率快速成長,因為運營商會用浸沒式水箱替換精密空調機組,以將PUE值維持在1.15以下。每個GB200 NVL72機架會散發132千瓦的熱量,因此需要設施部署480伏主幹網、2N+1 UPS串聯配置以及能夠處理45度C進水溫度的冷凍水循環系統。這些升級預計將提高開關設備和水泵的市場佔有率。

此外,液冷技術可提高冷通道周圍送風溫度,進而降低風扇功耗,提升整體設施效率。預計到2028年,這些優勢將使液冷相關機械設備在義大利超大規模資料中心市場的支出超過傳統精密空調(CRAC)設備。電力基礎設施也呈現類似趨勢,各資料中心園區正在增設30兆瓦容量的母線槽和靜態傳輸交換機,以支援分階段部署的雲端可用區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AWS、微軟 Azure 和谷歌雲端的雲端區域正在快速擴張

- 鋪設一條新的海底電纜,將在西西里島登陸。

- 歐盟的數位主權和對 Gaia-X 的遵守正在推動現場建設。

- 企業購電協議(PPA)正在推動義大利太陽能和風能的激增。

- GenAI推理叢集需要液冷邊緣區域

- 米蘭-都靈走廊的四級金融科技與即時支付中心

- 市場限制因素

- Lombardia和Lazio輸電網過剩容量的限制

- 高壓 (HV) 和中壓 (MV) 工程人員短缺,無法處理 24/7 全天候運作和維護 (O&M)。

- 波河流域蒸發冷卻受水資源壓力限制。

- AI 級 GPU 和光纖組件優先分配給 FLAP-D 中心。

- 產業價值鏈分析

- 技術展望

- 宏觀經濟因素對市場的影響

第5章:在超大規模資料中心實施人工智慧(AI)(子章節可能會根據資料可用性而有所變化)

- 人工智慧工作負載的影響:高密度GPU機架的興起與高熱負載管理

- 快速過渡到 400G 和 800G 乙太網路 / 本地 OEM 廠商對整合和相容性的需求

- 液冷技術的創新:浸沒式冷卻和冷板的發展趨勢

- 實施基於人工智慧的資料中心管理 (DCIM) / 雲端供應商的角色

第6章 監理與合規框架

第7章 資料中心關鍵統計數據

- 義大利現有超大規模資料中心設施(單位:兆瓦)(超大規模自建資料中心與託管資料中心)

- 義大利計畫建置的超大規模資料中心清單

- 義大利超大規模資料中心營運商列表

- 義大利資料中心資本支出(CAPEX)分析

第8章 市場規模與成長預測

- 依資料中心類型

- 超大規模自建

- 超大規模機房託管

- 按組件

- IT基礎設施

- 伺服器基礎架構

- 儲存基礎設備

- 網路基礎設施

- 電力基礎設施

- 配電單元

- 傳輸開關和開關設備

- UPS系統

- 發電機

- 其他電力基礎設施

- 機械設備

- 冷卻系統

- 架子

- 其他機械和設備

- 一般建築

- 核心和外殼開發

- 安裝和試運行服務

- 設計工程

- 火災偵測、消防和物理安全

- DCIM/BMS解決方案

- IT基礎設施

- 等級標準

- Tier III

- Tier IV

- 按資料中心規模

- 大型(25兆瓦或以下)

- 超大型(25兆瓦至60兆瓦)

- 兆瓦級(超過 60 兆瓦)

第9章 競爭情勢

- 市佔率分析

- 公司簡介

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Oracle Corporation

- IBM Corporation

- Equinix Inc.

- Digital Realty Trust Inc.

- STACK Infrastructure

- DATA4 Group

- Vantage Data Centers

- Compass Datacenters LLC

- Iron Mountain Inc.(Data Centers)

- Green DC Italy Srl

- Aruba SpA

- Rai Way SpA(Data Centers)

- Irideos SpA(Avalon)

- CyrusOne(KKR and GIP)

- Colt Data Centre Services

- Telecom Italia Sparkle SpA

- Retelit SpA

- Aligned Data Centers

- SuperNAP Italia Srl

第10章 市場機會與未來展望

- 評估未開發領域和未滿足的需求

The Italy hyperscale data center market size is expected to increase from USD 1.45 billion in 2025 to USD 1.96 billion in 2026 and reach USD 9.08 billion by 2031, growing at a CAGR of 35.88% over 2026-2031.

Sovereign-cloud mandates under the EU Digital Decade program, sizable grants from Italy's National Recovery and Resilience Plan, and stepped-up cloud-region launches by U.S. hyperscalers are pulling new capacity toward Milan and Rome. Subsea cable landings in Sicily are repositioning southern Italy as a low-latency gateway to North Africa, while generative-AI clusters are pushing rack densities above 40 kW and accelerating the shift to direct-to-chip liquid cooling. Developers are reserving grid capacity two years ahead of construction to avoid Lombardy's head-room constraints, and many are pairing those allocations with long-term renewable power purchase agreements that cap electricity costs below EUR 50 per MWh. Competitive intensity is further magnified by the rush to pre-lease white space that meets Gaia-X and Tier IV requirements, giving turnkey colocation campuses a time-to-market edge over self-build projects.

Italy Hyperscale Data Center Market Trends and Insights

Rapid Cloud-Region Roll-Outs by AWS, Microsoft Azure and Google Cloud

Cloud majors are accelerating multi-availability-zone builds in Milan and Rome to satisfy GDPR location clauses and DORA resilience rules. AWS has earmarked EUR 1.2 billion for its Milan region through 2029, while Microsoft is injecting EUR 4.3 billion into Italy North, each project adding three or more zones interconnected by sub-10-millisecond fiber paths. Oracle's second cloud region in Turin, opened in late 2025, widened the competitive field and created an ecosystem effect in which colocation providers pre-lease shells next door to hyperscaler on-ramps. The clustering compresses procurement cycles for switchgear, generators and prefabricated liquid-cooling loops, pulling lead times below 40 weeks for some mechanical packages. Tenant urgency is further evident in DATA4's MIL02 campus where 60% of the first 15 MW phase was pre-committed before foundations were poured.

Deployment of New Subsea Cables Landing in Sicily

Sparkle's Unitirreno system went live in October 2025 with 24 fiber pairs, cutting round-trip latency between Milan and Tunis from 45 milliseconds to under 15 milliseconds and bringing Palermo within one hop of North African traffic flows. The cable coincides with Terna's 1,000 MW Tyrrhenian Link HVDC interconnector, giving Sicilian sites both bandwidth and clean-power head-room. Edge nodes near Catania are already processing maritime sensor feeds and drone video within strict 20-millisecond budgets, use cases that would be unviable over Milan-routed paths. Developers able to secure 20-30 MW at 150 kV substations near the Palermo landing station can under-cut Lombardy's land prices by half while using solar-backed PPAs to keep operating costs flat.

Grid-Capacity Head-Room Constraints in Lombardy and Lazio

Terna warns that substations around Milan and Rome could face a 150 MW shortfall by 2028 as cumulative data-center demand breaches 500 MW. Developers now secure allocations 18-24 months before breaking ground and, in some cases, pre-pay grid-access charges that raise land costs by 10-15%. Vantage Data Centers absorbed this premium at its MXP2 site, buying 96 MW capacity upfront to guarantee phased expansion. Operators that miss the queue must invest in on-site battery energy storage or accept curtailment penalties that erode service-level guarantees.

Other drivers and restraints analyzed in the detailed report include:

- EU Digital-Sovereignty and Gaia-X Compliance Boosting Local Builds

- Corporate PPAs Tapping Italy's Solar and Wind Surge

- AI-Grade GPU and Optics Preferentially Allocated to FLAP-D Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-build campuses held the majority Italy hyperscale data center market share at 61.73% in 2025, but the capital-light appeal of turnkey white space is steering hyperscalers toward third-party halls that achieve the same security envelope without tying up balance sheets. The Italy hyperscale data center market size for colocation halls is projected to expand at a 36.73% CAGR through 2031, a trajectory underpinned by MXP2's 32 MW first phase that attracted two cloud majors and one sovereign tenant before slab pour. Such early commitments shave a year off time-to-market compared with green-field self-builds, giving enterprises faster on-ramps for AI inference workloads.

Self-build remains entrenched in scenarios requiring bespoke hot-aisle geometry or proprietary optical fabrics, as seen in Oracle's Turin region that integrates directly with TIM's backbone for deterministic throughput. Even so, colocation operators are absorbing the steep entry cost of liquid cooling, letting tenants scale 60 kW racks without single-client outlay. That shift unlocks demand from fintechs and SaaS firms that would otherwise push training jobs to Frankfurt, enhancing geographic stickiness inside Italy hyperscale data center market clusters.

IT infrastructure accounted for 52.88% of the share in 2025 due to GPU-dense servers, while mechanical systems are projected to grow the fastest at a 36.84% CAGR as operators replace CRAC units with immersion tanks to maintain PUE below 1.15. Each GB200 NVL72 rack dissipates 132 kW, requiring facilities to implement 480 V backbones, 2N+1 UPS strings, and chilled-water loops rated for 45 °C inlet. These upgrades are expected to increase wallet share for switchgear and pumps.

Immersion cooling also allows higher supply-air temperatures in surrounding cold aisles, trimming fan energy and lifting overall facility efficiency. These gains explain why the Italy hyperscale data center market share for mechanical packages tied to liquid cooling is expected to eclipse legacy CRAC spend by 2028. Electrical infrastructure follows the same curve, as campuses add bus ducts and static transfer switches sized for 30 MW blocks to support staggered cloud availability zones.

The Italy Hyperscale Data Center Market Report is Segmented by Data Center Type (Hyperscale Self-Build, and Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction), Tier Standard (Tier III, and Tier IV), and Data Center Size (Large, Massive, and Mega). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Oracle Corporation

- IBM Corporation

- Equinix Inc.

- Digital Realty Trust Inc.

- STACK Infrastructure

- DATA4 Group

- Vantage Data Centers

- Compass Datacenters LLC

- Iron Mountain Inc. (Data Centers)

- Green DC Italy S.r.l.

- Aruba S.p.A.

- Rai Way S.p.A. (Data Centers)

- Irideos S.p.A. (Avalon)

- CyrusOne (KKR and GIP)

- Colt Data Centre Services

- Telecom Italia Sparkle S.p.A.

- Retelit S.p.A.

- Aligned Data Centers

- SuperNAP Italia S.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Cloud-Region Roll-Outs by AWS, Microsoft Azure and Google Cloud

- 4.2.2 Deployment of New Subsea Cables Landing in Sicily

- 4.2.3 EU Digital-Sovereignty and Gaia-X Compliance Boosting Local Builds

- 4.2.4 Corporate PPAs Tapping Italy's Solar and Wind Surge

- 4.2.5 GenAI Inference Clusters Requiring Liquid-Cooled Edge Zones

- 4.2.6 Tier IV Fintech And Instant-Payments Hubs in Milan-Turin Corridor

- 4.3 Market Restraints

- 4.3.1 Grid-Capacity Head-Room Constraints in Lombardy and Lazio

- 4.3.2 Scarcity of HV/MV Engineering Talent for 24x7 O & M

- 4.3.3 Water-Stress Curbs on Evaporative Cooling in Po Valley

- 4.3.4 AI-Grade GPU and Optics Preferentially Allocated to FLAP-D Hubs

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-Segments are Subject to Change Depending on Availability of Data)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in Italy (in MW) (Hyperscale Self-Build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in Italy

- 7.3 List of Hyperscale Data Center Operators in Italy

- 7.4 Analysis on Data Center CAPEX in Italy

8 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Units

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning Services

- 8.2.4.3 Design Engineering

- 8.2.4.4 Fire Detection, Suppression and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By Data Center Size

- 8.4.1 Large ( Less than or equal to 25 MW)

- 8.4.2 Massive (Greater than 25 MW and Less than equal to 60 MW)

- 8.4.3 Mega (Greater than 60 MW)

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Google LLC

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Oracle Corporation

- 9.2.6 IBM Corporation

- 9.2.7 Equinix Inc.

- 9.2.8 Digital Realty Trust Inc.

- 9.2.9 STACK Infrastructure

- 9.2.10 DATA4 Group

- 9.2.11 Vantage Data Centers

- 9.2.12 Compass Datacenters LLC

- 9.2.13 Iron Mountain Inc. (Data Centers)

- 9.2.14 Green DC Italy S.r.l.

- 9.2.15 Aruba S.p.A.

- 9.2.16 Rai Way S.p.A. (Data Centers)

- 9.2.17 Irideos S.p.A. (Avalon)

- 9.2.18 CyrusOne (KKR and GIP)

- 9.2.19 Colt Data Centre Services

- 9.2.20 Telecom Italia Sparkle S.p.A.

- 9.2.21 Retelit S.p.A.

- 9.2.22 Aligned Data Centers

- 9.2.23 SuperNAP Italia S.r.l.

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment

超大規模資料中心市場:按組件、電力容量、冷卻方式、所有權類型、部署模式、應用和最終用戶產業分類-2026-2032年全球市場預測

超大規模資料中心市場:按組件、電力容量、冷卻方式、所有權類型、部署模式、應用和最終用戶產業分類-2026-2032年全球市場預測 德國超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年)

德國超大規模資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年) 全球超大規模資料中心市場:機會與策略展望(至2035年)

全球超大規模資料中心市場:機會與策略展望(至2035年) 超級資料中心市場規模、佔有率和趨勢分析報告:按解決方案、資料中心類型、冷卻技術、地區和細分市場預測(2026-2033 年)

超級資料中心市場規模、佔有率和趨勢分析報告:按解決方案、資料中心類型、冷卻技術、地區和細分市場預測(2026-2033 年) 超級資料中心市場分析與預測(至2035年):依類型、產品、服務、技術、元件、應用、部署方式、最終使用者、功能及安裝方式分類

超級資料中心市場分析與預測(至2035年):依類型、產品、服務、技術、元件、應用、部署方式、最終使用者、功能及安裝方式分類 超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季)

超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季) 超級資料中心市場:按組件、最終用戶、行業和地區分類(2026-2034 年)

超級資料中心市場:按組件、最終用戶、行業和地區分類(2026-2034 年) 超大規模資料中心全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

超大規模資料中心全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 超大規模資料中心市場:按IT基礎設施、電氣基礎設施、機械基礎設施、一般建築和區域分類

超大規模資料中心市場:按IT基礎設施、電氣基礎設施、機械基礎設施、一般建築和區域分類