|

市場調查報告書

商品編碼

2044083

專業人脈網路:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Professional Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

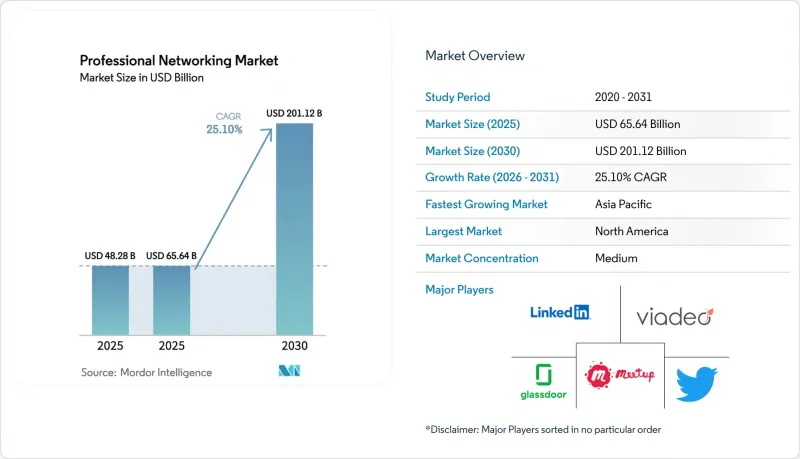

專業人脈市場預計將從 2025 年的 482.8 億美元和 2026 年的 656.4 億美元成長到 2031 年的 2011.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 25.1%。

生成式人工智慧的快速普及、對P2P互動日益成長的需求,以及人們為認證資質付費的意願不斷提高,正推動專業人脈市場從以廣告為中心的模式轉向高利潤的訂閱和交易收入模式。集人脈拓展、學習和認證於一體的平台正逐漸融入企業人才工作流程,而Slack和Discord群組中社群主導的成長正在縮短軟體供應商的銷售週期。監管,特別是歐盟《一般資料保護規則》(GDPR)的監管,推高了合規成本,但這些法規本身也為以隱私為先的替代方案創造了新的市場機會。隨著OpenAI、Salesforce和微軟將專業圖資料整合到其生產力套件中,競爭日益激烈,迫使現有企業透過持續創新和在資料管治的領先地位來捍衛其市場佔有率。

全球專業人脈網路市場趨勢與洞察

由生成式人工智慧驅動的個人化正在推動加值服務的使用。

生成式人工智慧透過提供高度個人化的職位提案、個人資料最佳化和互動式職業指導,將免費用戶轉化為付費用戶,其效果遠超傳統的關鍵字篩選。預計到2025年,LinkedIn Premium的訂閱收入將超過20億美元,約佔總收入的12%。此外,約40%的付費用戶至少使用過一項人工智慧功能。付費用戶在兩年內成長了近50%,顯示人工智慧工具透過簡化繁瑣的個人資料建立流程,降低了用戶升級的門檻。生成式人工智慧軟體供應商目前將12%的數位廣告預算分配給LinkedIn,是業界平均的四倍。這是因為職業意圖資料能夠帶來更高的轉換率。憑藉即時技能差距分析和個人化學習路徑,付費計畫正從可選項轉變為職業投資,迫使競爭對手在人工智慧深度方面迎頭趕上,還是冒著被同質化的風險之間做出選擇。

拓展線上學習與技能發展

隨著平台將認證和同儕推薦相結合,職業人脈拓展和持續學習正在融合。 LinkedIn Learning Career Hub 於 2025 年底推出,它將企業的職位架構映射到 LinkedIn 的經濟圖譜上,視覺化員工技能差距,並推薦課程以支援內部調動。根據七國集團 (G7) 發布的《中小企業人工智慧應用藍圖》,有一半受訪的中小企業缺乏精通生成式人工智慧的人員,導致對微證書的需求激增。 OpenAI 的試驗計畫旨在到 2030 年認證 1000 萬美國工人的技能,該計畫展示了繞過傳統學位要求的替代認證的潛力。在印度,97% 的受訪中小企業已經以某種形式應用了人工智慧,中型企業報告稱,其人工智慧相關技能同比成長了 52%。將學習、認證和社交證明整合到單一工作流程中的平台,比獨立的社交網站擁有更高的用戶參與度和更低的用戶流失率。

資料隱私和安全問題

資料外洩事件的增加和監管力度的加強正在削弱用戶信任,並迫使企業支付巨額遵循成本,從而分散了產品創新資源。 2024年10月,LinkedIn因濫用《歐洲一般資料保護規則》(GDPR)中關於行為導向廣告的法律依據而被罰款3.1億歐元(3.5億美元)。截至2026年2月,GDPR累積罰款金額已達71億歐元(80億美元),光2025年就高達12億歐元(13.5億美元)。同時,2025年歐洲經濟區(EEA)的每日資料外洩報告數量增加至443起。在嚴格監管的地區,使用者越來越不願意共用敏感的商業數據,導致用於驅動建議引擎的輸入數據減少。未能展現出強力的資料管治和透明用戶許可的平台將面臨失去市場准入和用戶流失到注重隱私保護的競爭對手的風險。

細分市場分析

到2025年,社群網路平台將佔據職業社交市場58.13%的佔有率,其中LinkedIn以超過10億會員和3.1億月有效用戶主導。預計到2031年,垂直或細分領域的平台將實現26.92%的複合年成長率,這意味著橫向巨頭在職業社交市場所擁有的規模經濟優勢正在縮小。 GitHub與微軟CoreAI的整合、Discord不斷成長的專業用戶群以及Blind超過900萬匿名工作者的社群都表明,專業化環境正在透過訂閱、招聘費或數據許可等方式實現更深入的用戶互動,從而實現盈利。在這種模式下,開發者、產品經理和創辦人聚集在內容豐富、經過同行檢驗的空間中,而不是向廣泛的受眾進行廣播。這使得垂直產業能夠利用領域數據提供精準的AI建議,並提高轉換率。相反,大規模成熟公司面臨持續響應多樣化用戶需求的挑戰,這需要它們不斷擴展功能,進而導致營運成本的增加。

儘管橫向領域的領導者繼續受益於網路效應,簡化了跨行業搜尋,但如果他們未能整合垂直領域的子社區而不蠶食廣告收入,他們在專業人脈市場的佔有率可能會被稀釋。策略挑戰在於如何取得專業社群——是透過「建構」、「收購」還是「合作」。微軟收購GitHub表明,大型平台將擴大把特定領域的資料圖譜整合到其核心人工智慧模型中,利用專業背景來提升企業生產力解決方案。同時,垂直領域的新興企業可以拓展招聘和教育服務,而無需承擔因廣泛的社會審視而帶來的品牌風險,從而將自身定位為高價值互動中值得信賴的中介機構。

到2025年,廣告平台將佔職業社交市場46.79%的佔有率,這反映了其對贊助內容和展示廣告的傳統依賴。在職業社交市場中,付費訂閱平台收費到2031年將以26.13%的複合年成長率成長,因為用戶付費可享有無廣告環境、人工智慧洞察和認證資格。 LinkedIn的付費用戶在兩年內激增近50%,預計到2025年將超過20億美元。這初步徵兆,訂閱收入已經可以與中型媒體公司相媲美。免費增值模式在基礎社交功能和付費分析及推廣工具之間取得平衡。然而,由於轉換率僅為個位數,LinkedIn不得不每季推出引人注目的新功能以維持用戶升級。

交易平台透過將人才與企業進行配對並收取推薦費或許可費來獲利。這種模式具有很高的終身價值,但也伴隨著較高的實施風險。 HireEZ 和 Loxo 提供企業級許可,價格約為每位使用者每月 199 美元,其定價的合理性在於能夠將招募時間縮短兩位數,並提高候選人品質。擁有從人才搜尋到通訊和應徵者追蹤等端到端工作流程的供應商,會不斷最佳化其人工智慧配對評分,並收集資料以控制轉換成本。因此,現有的以廣告為中心的公司要么被迫轉型為訂閱或交易業務,要么將面臨利潤率下降的困境,因為 cookie 的逐步淘汰和不斷上漲的獲客成本將給廣告商的投資回報率帶來壓力。

區域分析

到2025年,北美將佔據專業社交網路市場35.54%的佔有率,這主要得益於其密集的技術叢集和創業投資的集中。儘管隨著用戶滲透率接近飽和,成長速度有所放緩,但由於企業級整合(例如LinkedIn數據驅動的Microsoft M365 Copilot),每位用戶收入仍在成長。包括Reddit 10億美元股票回購計畫在內的公開市場里程碑事件,凸顯了投資人對社區主導互動模式的信心。加拿大和墨西哥正受益於跨境人才流動,但其本土平台的創新能力仍落後於成熟的美國公司。

亞太地區是成長最快的區域,預計到2031年複合年成長率將達到27.03%。印度擁有1.67億LinkedIn用戶,並以每年20%的速度成長,預計三年內將成為LinkedIn最大的市場。用戶行為反映了創業精神的興起,印度用戶個人資料中「創始人」條目的數量同比成長104%,影片上傳量成長了60%。在日本和韓國,本土企業致力於滿足語言和數據主權方面的需求,這使得全球品牌難以進入市場。東南亞的年輕人口正在推動行動優先技術的普及,但支付方式的去中心化將限制訂閱模式的普及,直到數位錢包成熟為止。

歐洲仍然是重要的收入來源,但由於嚴格的GDPR法規和經濟逆風,成長速度正在放緩。 XING的收入下滑表明,僅靠區域規模不足以支撐業務成長,必須快速交付功能;而LinkedIn被處以3.1億歐元的罰款,則清楚地說明了不一致的同意框架所帶來的成本。中東和非洲地區作為一個新興市場,擁有巨大的成長潛力,各國政府都在資助數位轉型和創投生態系統,但支付基礎設施的匱乏和寬頻網路的不均衡阻礙了其短期獲利能力。南美洲,尤其是巴西和阿根廷,由於貨幣波動和通貨膨脹,面臨複雜的定價問題,但其充滿活力的創業環境孕育了靈活的人才市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 拓展線上學習與技能發展

- 社群媒體在職涯發展中的日益普及

- 遠距辦公和混合辦公模式日益普及。

- 企業加大數位化招募解決方案的投資

- 由生成式人工智慧驅動的個人化正在推動加值服務的使用。

- 垂直SaaS整合到網路平台

- 市場限制因素

- 資料隱私和安全問題

- 跨境資料法規導致合規成本增加

- 創作者疲勞和自然觸達率下降

- 過度集中於單一主導平台的風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按平台

- 社群網路平台

- 利基/垂直平台

- 特定工作平台

- 專業網路社區

- 按收入模式

- 廣告平台

- 免費增值訂閱平台

- 高級訂閱平台

- 基於交易費用的平台

- 最終用戶

- 專家和個人

- 公司和組織

- 負責人和顧問

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- LinkedIn Corporation

- Viadeo SA

- Glassdoor Inc.

- Meetup Inc.

- Twitter Inc.

- XING SE

- Shapr SAS

- Slack Technologies LLC

- GitHub Inc.

- AngelList Holdings LLC

- Polywork Inc.

- Lunchclub Inc.

- Discord Inc.

- Reddit Inc.

- Fishbowl Inc.

- Teamblind Inc.(Blind)

- Kaggle Inc.

- Goodwall SA

- Opportunity Network Srl

- Jobcase Inc.

第7章 市場機會與未來展望

The professional networking market size is projected to expand from USD 48.28 billion in 2025 and USD 65.64 billion in 2026 to USD 201.12 billion by 2031, registering a CAGR of 25.1% between 2026 to 2031.

Rapid penetration of generative artificial intelligence, demand for private peer exchanges, and rising willingness to pay for verified credentials are shifting the professional networking market from an advertising-heavy model toward high-margin subscription and transaction revenue. Platforms that combine networking with learning and credentialing are embedding themselves in enterprise talent workflows, while community-led growth in Slack and Discord groups is compressing sales cycles for software vendors. Regulatory scrutiny, especially under the European General Data Protection Regulation, is elevating compliance costs, yet the same rules create white-space for privacy-first alternatives. Competitive intensity is rising as OpenAI, Salesforce, and Microsoft integrate professional graph data into productivity suites, forcing incumbents to defend share through continuous feature innovation and data-governance leadership.

Global Professional Networking Market Trends and Insights

Generative-AI Based Personalization Boosting Premium Uptake

Generative artificial intelligence is converting free users into paying subscribers by delivering hyper-personalized job suggestions, profile optimization, and conversational career coaching that surpass traditional keyword filters. LinkedIn Premium subscriptions passed USD 2 billion in 2025, equal to roughly 12% of total revenue, with around 40% of premium users engaging at least one AI-powered feature. Premium subscriber counts rose close to 50% in two years, indicating lower friction in upgrading when AI tools remove tedious profile work. Generative-AI software vendors now channel 12% of digital advertising budgets into LinkedIn, quadrupling the cross-industry average because professional intent data yields higher conversion. Real-time skill-gap analysis and personalized learning paths are turning premium plans from discretionary spend into a career investment, pushing rivals to match AI depth or risk commoditization.

Expansion of Online Learning and Skill Development

Professional networking and continuous learning are converging as platforms bundle credentialing with peer endorsement. LinkedIn Learning Career Hub, launched late 2025, maps enterprise job architectures to the LinkedIn Economic Graph, surfaces employee skill shortages, and recommends courses that support internal mobility. The G7 SME AI Adoption Blueprint shows that half of surveyed small and medium enterprises lack staff proficient in generative AI, creating urgent demand for micro-credentials. OpenAI's certification pilot aiming to validate 10 million American workers by 2030 demonstrates that alternative credentialing can bypass legacy degree requirements. In India, 97% of surveyed small businesses already use AI in some capacity, while mid-size firms reported a 52% year-on-year jump in AI-related skills. Platforms that integrate learning, credentialing, and social proof within a single workflow enjoy higher engagement and lower churn than stand-alone networking sites.

Data Privacy and Security Concerns

Escalating breaches and heightened enforcement are eroding user trust and forcing heavy compliance spend that diverts resources from product innovation. LinkedIn incurred a EUR 310 million (USD 350 million) penalty in October 2024 for misusing behavioral-ad legal bases under the European General Data Protection Regulation. Cumulative GDPR fines hit EUR 7.1 billion (USD 8 billion) by February 2026, with EUR 1.2 billion (USD 1.35 billion) levied in 2025 alone, while daily breach notifications in the European Economic Area climbed to 443 in 2025. Users in strict jurisdictions now hesitate to share sensitive professional data, thinning the input that powers recommendation engines. Platforms unable to prove strong data governance and consent transparency risk market-access loss and user flight to privacy-centric rivals.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Private Micro-Communities for Peer Knowledge Exchange

- Increased Use of Social Media for Career Growth

- Mounting Compliance Costs from Cross-Border Data Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Social networking platforms commanded 58.13% professional networking market share in 2025, a position led by LinkedIn's one-billion-plus members and 310 million monthly active users. The professional networking market size advantage of horizontal giants is narrowing as niche or vertical platforms register a 26.92% CAGR through 2031. GitHub's integration into Microsoft's CoreAI unit, Discord's widening professional user base, and Blind's nine-million-strong anonymous workforce community show that specialized environments monetize deeper engagement through subscriptions, hiring fees, or data licenses. In this paradigm, developers, product managers, and founders congregate where discourse is context-rich and peer-validated rather than broadcast to broad audiences, allowing vertical operators to leverage domain data for targeted AI recommendations and higher conversion rates. Conversely, broad-scale incumbents face the challenge of sustaining relevance with heterogeneous user needs, demanding continuous feature sprawl that inflates operating expense.

Horizontal leaders still profit from network effects that simplify cross-industry search, yet their professional networking market share may dilute if they fail to embed vertical sub-communities without cannibalizing advertising revenue. The strategic question is whether to build, buy, or partner for specialty communities. Microsoft's GitHub absorption signals that large platforms will increasingly fold domain-specific data graphs into core AI models, using professional context to enrich enterprise productivity offerings. Vertical challengers, meanwhile, can extend into hiring and education services without accumulating the brand risk linked to broad social discourse, positioning themselves as trusted intermediaries for high-value interactions.

Advertising-based platforms held 46.79% professional networking market size in 2025, reflecting legacy dependence on sponsored content and display units. In the professional networking market, premium subscription platforms are on track for a 26.13% CAGR through 2031 as users pay for ad-free sessions, AI insights, and verified credentials. LinkedIn's premium subscriber pool surged almost 50% in two years, passing USD 2 billion in 2025, an early marker that subscription revenue can already rival mid-tier media properties. Freemium models occupy a balancing act, offering baseline networking free while reserving analytics and outreach tools behind paywalls; however, single-digit conversion rates pressure them to unveil compelling new features quarterly to sustain upgrades.

Transaction-fee platforms generate income by matching talent and earning placement or licensing fees, a route with higher lifetime values but steeper execution risk. HireEZ and Loxo price enterprise seats near USD 199 per user each month, justified by double-digit reductions in time-to-hire and improved candidate quality. Vendors that own the end-to-end workflow-from sourcing through messaging to applicant tracking-capture data exhaust that refines AI match scores and sustains switching costs. Ad-centric incumbents must therefore diversify toward subscriptions and transactions or confront margin compression as cookies deprecate and cost-per-lead inflation eats into advertiser return on investment.

The Professional Networking Market Report is Segmented by Platform (Social Networking, Niche/Vertical, Job-Specific, and Specialized Communities), Revenue Model (Advertising, Freemium, Premium, and Transaction-Fee), End-User (Professionals, Businesses, and Recruiters), Organization Size (Large Enterprises, and SMEs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 35.54% professional networking market share in 2025, driven by dense technology clusters and venture capital concentration. Growth is plateauing as user penetration nears saturation, yet monetization per user rises because of enterprise integrations such as LinkedIn data powering Microsoft M365 Copilot. Public-market milestones including Reddit's USD 1 billion share-repurchase plan highlight investor confidence in community-driven engagement models. Canada and Mexico benefit from cross-border talent liquidity, though domestic platform innovation remains overshadowed by United States incumbents.

Asia-Pacific is the fastest growing region, with a projected 27.03% CAGR through 2031. India's 167 million LinkedIn users are expanding 20% per year, and the country is on pace to become LinkedIn's largest market within three years. User behavior underscores entrepreneurial appetite, as "founder" additions to Indian profiles rose 104% year-over-year while video uploads grew 60%. Local players across Japan and South Korea address language and data-sovereignty needs, complicating entry for global brands. Southeast Asia's youthful demographics fuel mobile-first adoption, though fragmented payments limit subscription uptake until digital wallets mature.

Europe contributes meaningful revenue but lags on growth due to stringent GDPR oversight and economic headwinds. XING's declining revenue shows that regional scale is insufficient without feature velocity, while LinkedIn's EUR 310 million penalty illustrates the cost of misaligned consent frameworks. The Middle East and Africa offer greenfield upside as governments fund digital transformation and venture ecosystems, but payment infrastructure gaps and inconsistent broadband coverage temper near-term revenue conversion. South America, with Brazil and Argentina at the center, faces currency volatility and inflation that complicate pricing yet hosts a vibrant startup scene receptive to flexible talent marketplaces.

- LinkedIn Corporation

- Viadeo SA

- Glassdoor Inc.

- Meetup Inc.

- Twitter Inc.

- XING SE

- Shapr SAS

- Slack Technologies LLC

- GitHub Inc.

- AngelList Holdings LLC

- Polywork Inc.

- Lunchclub Inc.

- Discord Inc.

- Reddit Inc.

- Fishbowl Inc.

- Teamblind Inc. (Blind)

- Kaggle Inc.

- Goodwall SA

- Opportunity Network Srl

- Jobcase Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Online Learning and Skill Development

- 4.2.2 Increased Use of Social Media for Career Growth

- 4.2.3 Growing Remote and Hybrid Work Adoption

- 4.2.4 Rising Employer Investment in Digital Recruitment Solutions

- 4.2.5 Generative-AI Based Personalization Boosting Premium Uptake

- 4.2.6 Vertical SaaS Integration into Networking Platforms

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Security Concerns

- 4.3.2 Mounting Compliance Costs from Cross-Border Data Regulation

- 4.3.3 Creator Fatigue and Declining Organic Reach

- 4.3.4 Concentration Risk Around a Single Dominant Platform

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Social Networking Platforms

- 5.1.2 Niche/Vertical Platforms

- 5.1.3 Job-Specific Platforms

- 5.1.4 Specialized Networking Communities

- 5.2 By Revenue Model

- 5.2.1 Advertising-Based Platforms

- 5.2.2 Freemium Subscription Platforms

- 5.2.3 Premium Subscription Platforms

- 5.2.4 Transaction-Fee Platforms

- 5.3 By End-User

- 5.3.1 Professionals/Individuals

- 5.3.2 Businesses and Organisations

- 5.3.3 Recruiters and Consultants

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 LinkedIn Corporation

- 6.4.2 Viadeo SA

- 6.4.3 Glassdoor Inc.

- 6.4.4 Meetup Inc.

- 6.4.5 Twitter Inc.

- 6.4.6 XING SE

- 6.4.7 Shapr SAS

- 6.4.8 Slack Technologies LLC

- 6.4.9 GitHub Inc.

- 6.4.10 AngelList Holdings LLC

- 6.4.11 Polywork Inc.

- 6.4.12 Lunchclub Inc.

- 6.4.13 Discord Inc.

- 6.4.14 Reddit Inc.

- 6.4.15 Fishbowl Inc.

- 6.4.16 Teamblind Inc. (Blind)

- 6.4.17 Kaggle Inc.

- 6.4.18 Goodwall SA

- 6.4.19 Opportunity Network Srl

- 6.4.20 Jobcase Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

社群網路應用市場規模、佔有率和成長分析:按應用程式類型、獲利模式、平台和地區分類-2026-2033年產業預測

社群網路應用市場規模、佔有率和成長分析:按應用程式類型、獲利模式、平台和地區分類-2026-2033年產業預測 企業社交網路市場:按組件、部署類型、組織規模和最終用戶分類-2026年至2032年全球預測

企業社交網路市場:按組件、部署類型、組織規模和最終用戶分類-2026年至2032年全球預測 2026年全球企業社交網路市場報告2026年全球創作者空間市場報告

2026年全球企業社交網路市場報告2026年全球創作者空間市場報告 企業社交網路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類社交網路應用市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型和最終用戶分類

企業社交網路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類社交網路應用市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、部署類型和最終用戶分類 全球 Mighty Networks 和 Circle 市場:未來預測(至 2032 年)—按產品類型、功能集、用例、技術、最終用戶和地區進行分析

全球 Mighty Networks 和 Circle 市場:未來預測(至 2032 年)—按產品類型、功能集、用例、技術、最終用戶和地區進行分析 全球社交網路應用市場2025年社群網路應用全球市場報告

全球社交網路應用市場2025年社群網路應用全球市場報告