|

市場調查報告書

商品編碼

2044049

北美自動化紙箱組裝機:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Automatic Carton Erector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

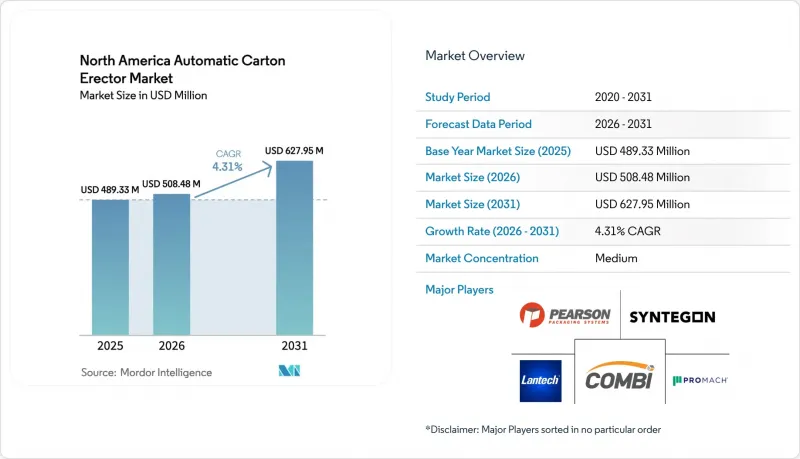

預計北美自動化瓦楞紙箱組裝機市場將從 2025 年的 4.8933 億美元成長到 2026 年的 5.0848 億美元,到 2031 年達到 6.2795 億美元,2026 年至 2031 年的複合年成長率為 4.31%。

電子商務的擴張、倉庫工人兩位數的工資成長以及日益嚴格的食品安全法規,正推動採購預算轉向自動化裝箱機。由於人工成本幾乎佔最終包裝成本的三分之一,財務部門目前預計投資回收期為18-24個月。此外,自2019年以來40-50%的薪資成長也為採用自動化設備提供了依據。隨著視覺引導機器人、伺服運動和模組化框架成為標準配置,供應商面臨的技術壁壘正在降低,競爭優勢正轉向預接線、可快速安裝的成套設備,從而最大限度地縮短工程前置作業時間。同時,由於現有食品工廠對資本支出的審查日益嚴格,整體成長速度正在放緩。這是因為維修一座已有30年歷史的建築,由於電氣升級、地面找平以及消防安全合規維修,安裝成本可能會翻倍。不同細分市場的採用率有顯著差異。標準開槽紙箱(RSC)仍然佔據主導地位,佔瓦楞紙板出貨量的70-80%,但零售商引入的體積重量附加費正在加速托盤成型機和環繞式包裝形式的普及。速度為每分鐘20-40箱(CPM)的中型機器將在2025年佔據五分之二的銷售額,與大多數冷凍食品、藥品和合約包裝生產線的處理能力相當。然而,在季節性高峰期採用三班制運作的飲料和休閒食品生產企業中,速度超過每分鐘40箱的系統正在獲得市場佔有率。全自動平台將在2025年佔據近三分之二的安裝量,但由於能夠維護伺服驅動器、視覺攝影機和PLC代碼的技術人員短缺,其成長受到限制。地區也會影響投資報酬率。到2025年,美國將佔全球銷售額的五分之四以上,但受新建履約中心的推動,加拿大預計在2031年前成為成長最快的市場。此外,墨西哥在近岸外包方面存在不確定性,其成長潛力取決於服務網路的覆蓋範圍和人事費用趨勢。

北美自動化瓦楞紙板組裝機市場趨勢及洞察

電子商務履約中心快速成長

線上零售商透過在新物流中心部署自動化組裝,維持每小時超過1000件的處理能力,取代了耗時8到12秒的人工組裝流程。沃爾瑪加拿大公司位於沃恩和卡加利的65億加元倉庫整合了紙箱成型和高密度儲存系統,而亞馬遜位於YYC4的280萬平方英尺的倉庫運作機器人揀選系統,該系統依賴預組裝紙箱。像Metro Supply Chain這樣的微型倉配專家正在將AutoStore的立方體儲存系統與緊湊型紙板組裝相結合,以將訂單到出貨的週期縮短至30分鐘以內。在分散式網路中,即使單一地點的處理量減少,所需的機器數量也會增加,因此,模組化、即插即用的解決方案更受歡迎,這些解決方案可以用堆高機運送到位,並在數小時內完成佈線,而不是數天。

人事費用上升正在推動自動化技術的普及。

2024年第二季度,倉庫平均時薪達18.99美元,較2019年成長40%至50%。這使得瓦楞紙板組裝機的投資回收期縮短至18至24個月。離職率進一步提升了成本節約。企業每流失一名員工,就要花費3,500美元招募和培訓,而許多物流中心每8至12個月就要重複一次這樣的招募和培訓。將業務從亞洲遷回國內的合約物流供應商正面臨人手不足、失業率接近歷史最高水準的市場,因此自動化成為唯一可擴展的選擇。然而,由於上游工程的托盤堆疊和下游的貼標流程也需要同步進行現代化改造,因此只有13%的受訪倉庫表示實現了全面的包裝自動化。

高初始投資

入門級半自動包裝機的起價約為 15,000 美元,但配備視覺系統的全自動平台價格超過 100,000 美元,這對於利潤率僅為個位數的食品加工企業來說是一筆不小的負擔。加上空白送料器、下游封口機和系統整合等成本,總實施成本將翻倍,而且即使只運作一個班次,投資回報期也超過 36 個月。包裝器材的租賃模式仍處於起步階段,企業必須使用營運資金貸款,而截至 2024 年,利率將超過 7%。生產量波動較大的契約製造製造商不願固定成本,許多公司都在推遲自動化,直到透過私募股權整合公司整合多個生產基地實現規模經濟效益。

細分市場分析

到2025年,標準開槽紙箱組裝將佔據45.32%的市場佔有率,這表明它們在托盤最佳化運輸路線中發揮著重要作用,其成長率與北美自動化瓦楞紙板組裝市場的整體趨勢相符。特殊尺寸的紙箱組裝預計將成長5.34%,高於市場平均水平,這得益於尺寸合適的包裝可以降低體積重量費用,從而減輕數位零售利潤率的壓力。托盤成型機服務於生鮮食品和已調理食品調理食品,這些產業對產品的透氣性和貨架可見度有較高要求。同時,Tablock設計無需使用黏合劑,降低了耗材成本,並提高了作為生活垃圾的可回收性。環繞式包裝可為倉儲式會員商店提供類似標誌的圖形,但對產品精確裝載和SKU差異低接受度的需求,使得整合機器人的重要性日益凸顯。

視覺引導系統可在 10 分鐘內實現無需工具的設定更改,從而降低 500 件以下批量混合規格生產的成本。 Combi 的 Ergopack 2.0 可在幾分鐘內完成瓦楞紙板 (RSC) 和托盤之間的切換,滿足了食品電履約對多 SKU 的需求。藥品和營養補充劑的合約包裝公司正在使用特殊規格的包裝,並在組裝過程中插入防篡改插頁,以滿足合規性和行銷需求。永續性的轉變正在推動這一趨勢,因為環繞式包裝和托盤包裝通常可減少 10-15% 的瓦楞紙板用量,從而有助於提升企業的 ESG(環境、社會和治理)績效。

預計到2025年,每分鐘出貨量為20-40個包裝盒的系統將佔據40.21%的市場。這與北美自動化紙盒組裝機市場中冷凍食品、成藥和合約包裝生產線的需求相符,這些產業需要在保證產量的同時頻繁更換包裝。每分鐘出貨量低於20個包裝盒的機器仍用於小規模生產和臨床試驗場所,因為在這些場所,手動組裝仍然具有成本效益。預計每分鐘出貨量高於40個包裝盒的機器將成長5.53%,這主要得益於飲料、零食和當日達履約中心等行業的成長,這些產業需要自動化成型以提高設備運作的經濟效益。

Schneider電機的伺服驅動平台在面積僅 12 英尺的情況下,實現了每分鐘 60 箱的生產速度,無需額外臨時人員即可滿足勞動節飲料促銷活動的需求。在兩班或三班制工廠中,持續運作可進一步加快投資回報。一台每天運作20 小時、每分鐘 60 箱的組裝機可處理 72,000 箱產品,減少了 4-5 名操作員的需求,從而在 12-15 個月內收回成本。瓶頸在於上游工程,下游的封箱機、包裝機和堆垛機需要匹配速度,這通常會導致系統預算高達 50 萬至 75 萬美元。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人事費用上升正在推動自動化技術的普及。

- 電子商務履約中心快速成長

- 更嚴格的食品安全包裝法規

- 視覺引導機器人的整合

- 引入即插即用的模組化機械

- 過渡到可回收紙板材料

- 市場限制因素

- 大量初始資本投資

- 現有設施建築占地面積的限制

- 熟練維修技師短缺

- 瓦楞紙板供應鏈的波動性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 標準開槽式外殼組裝機

- 塔布洛克箱體組裝機

- 托盤成型組裝機

- 專用箱體組裝機

- 按速度區域(每分鐘瓦楞紙箱數量)

- 每千次展示成本 (CPM) 20 美分或更低

- 20~40 CPM

- 每千次展示成本 (CPM) 40 美分或以上

- 按最終用途行業分類

- 食品/飲料

- 電子商務與零售

- 製藥

- 工業產品

- 其他終端用戶產業

- 按自動化級別

- 半自動

- 全自動

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ProMach Inc.

- Syntegon Technology GmbH

- Combi Packaging Systems LLC

- Pearson Packaging Systems LLC

- Lantech LLC

- Massman Automation Designs LLC

- Schneider Packaging Equipment Company Inc.

- EndFlex LLC

- Douglas Machine Inc.

- Delkor Systems Inc.

- ADCO Manufacturing

- Somic Packaging Inc.

- Econocorp Inc.

- BluePrint Automation BV

- JLS Automation

- Hamrick Manufacturing and Service Inc.

- Texwrap Packaging Systems LLC

- Kliklok-Woodman LLC

- PMI KYOTO Packaging Systems Inc.

第7章 市場機會與未來展望

The North America automatic carton erector market size is expected to increase from USD 489.33 million in 2025 to USD 508.48 million in 2026 and reach USD 627.95 million by 2031, growing at a CAGR of 4.31% over 2026-2031.

Expanding e-commerce footprints, double-digit rises in warehouse wages, and stricter food-safety mandates collectively steer procurement budgets toward automated case forming. Finance teams now calculate 18- to 24-month payback horizons as labor represents nearly one-third of end-of-line packaging cost, while 40%-50% wage inflation since 2019 accelerates automation justification. Vendors face fewer technology barriers because vision-guided robotics, servo motion, and modular frames have become standard offerings, so competitive advantage shifts to pre-wired, quick-install packages that minimize engineering lead time. Deeper capital scrutiny inside legacy food plants tempers the overall growth pace because electrical upgrades, floor-leveling, and fire-code retrofits can double installed cost when retrofitting 30-year-old buildings. Key adoption differentials surface across segments. Regular slotted case (RSC) formats still dominate because they handle 70%-80% of corrugated shipping volume, yet retailers' dimensional-weight surcharges spur faster uptake of tray formers and wraparound styles. Mid-tier 20-40 carton-per-minute (CPM) machines account for two-fifths of 2025 revenue because they match throughput on most frozen food, pharma, and contract-packaging lines; however, >40 CPM systems are gaining share in beverage and snack operations that now run three shifts during seasonal peaks. Fully automatic platforms comprise almost two-thirds of 2025 installations, but their growth is gated by the scarcity of technicians who can maintain servo drives, vision cameras, and PLC code. Geography again shapes ROI; the United States controls more than four-fifths of 2025 sales, Canada emerges as the fastest grower through 2031 on the back of greenfield fulfillment hubs, and Mexico is a nearshoring wild card whose upside depends on service-network reach and wage-cost trajectories.

North America Automatic Carton Erector Market Trends and Insights

Boom in E-Commerce Fulfillment Centers

Online retailers embed automatic erectors inside greenfield distribution hubs to eliminate 8- to 12-second manual case assembly steps, sustaining throughput targets above 1,000 units per hour. Walmart Canada's USD 6.5 billion Vaughan and Calgary nodes integrate carton forming with high-density storage, while Amazon's 2.8 million square-foot YYC4 site runs robotic picking that depends on pre-erected cartons. Micro-fulfillment specialists such as Metro Supply Chain pair AutoStore cubes with compact erectors, pushing order-to-ship cycles under 30 minutes. Distributed networks multiply the number of required machines even when single-site volumes drop, favoring modular, plug-and-play formats that forklift into position and wire up in hours rather than days.

Rising Labor Costs Prompting Automation Adoption

Average warehouse wages reached USD 18.99 per hour in Q2 2024, a 40%-50% jump since 2019, compressing carton-erector payback periods to 18-24 months. High turnover magnifies savings; each replacement costs firms USD 3,500 in recruiting and onboarding, repeating every 8-12 months in many distribution centers. Contract logistics providers reshoring operations from Asia enter labor-scarce markets where unemployment hovers near record lows, leaving automation as the only scalable path. Nonetheless, only 13% of surveyed warehouses report full packaging automation because upstream palletizing and downstream labeling must be modernized in parallel.

High Upfront Capital Expenditure

Entry-level semi-automatic units start near USD 15,000, while fully automatic, vision-equipped platforms exceed USD 100,000, a hurdle for food processors operating on single-digit margins. Total installed cost doubles after accounting for blank feeders, downstream sealers, and system integration, stretching ROI beyond 36 months when plants run only one shift. Leasing models remain nascent in packaging machinery, forcing firms to draw on working-capital lines priced above 7% interest in 2024. Contract manufacturers with variable volume commitments hesitate to lock in fixed costs, and many postpone automation until private-equity consolidators roll up multiple sites to achieve scale.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Food Safety Packaging Regulations

- Integration of Vision-Guided Robotics

- Skilled Technician Shortage for Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Regular slotted case erectors accounted for 45.32% of the market share in 2025, underscoring their entrenched role in pallet-optimized shipping lanes, yet their growth aligns with the overall North America automatic carton erector market. Specialty case erectors is projected to outpace the baseline at 5.34% because right-sized packaging trims dimensional-weight fees that erode digital-retail margins. Tray formers serve fresh produce and ready-meal sectors that need airflow and shelf visibility, while tablock designs remove adhesive, lowering consumables budgets and improving curbside recyclability. Wraparound styles offer billboard-quality graphics for warehouse-club aisles, but they require precision product loading and intolerance for SKU variances, increasing the importance of integrated robotics.

Vision-guided systems now enable sub-10-minute tool-free changeovers, making mixed-format production economical at batch sizes below 500. Combi's Ergopack 2.0, capable of switching between RSC and tray within minutes, answers multi-SKU demands in grocery e-commerce fulfillment. Pharmaceutical and nutraceutical contract packers add tamper-evident inserts during erection, leveraging specialty formats for compliance as well as marketing. The shift toward sustainability reinforces the trend, since wraparounds and trays often reduce corrugated usage by 10%-15%, supporting corporate ESG scorecards.

Systems rated 20-40 CPM captured 40.21% of the market share in 2025, aligning with the North America automatic carton erector market size requirements of frozen food, OTC pharma, and contract-packaging lines that balance volume with frequent changeovers. Sub-20 CPM machines persist in artisan and clinical-trial environments where manual assembly still pencils out. Equipment above 40 CPM is forecast to grow 5.53%, driven by beverage, snack, and same-day-delivery fulfillment centers whose uptime economics demand automated forming.

Schneider's servo-driven platform hits 60 CPM while still fitting a 12-foot footprint, enabling Labor Day beverage promotions without adding temporary workers. The ROI accelerates in continuous 2- or 3-shift plants; a 60 CPM erector running 20 hours daily erects 72,000 cases, eliminating four to five operators and recouping capital in 12-15 months. The constraint lies upstream, and downstream case sealers, packers, and palletizers must match speed, often bumping system budgets toward USD 0.5-0.75 million.

The North America Automatic Carton Erector Market Report is Segmented by Product Type (Regular Slotted Case Erectors, Tablock Case Erectors, Tray Forming Erectors, and Specialty Case Erectors), Speed Band (Up To 20 CPM, 20-40 CPM, and Above 40 CPM), End-Use Industry (Food and Beverage, and More), Automation Level (Semi-Automatic, and Fully Automatic), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ProMach Inc.

- Syntegon Technology GmbH

- Combi Packaging Systems LLC

- Pearson Packaging Systems LLC

- Lantech LLC

- Massman Automation Designs LLC

- Schneider Packaging Equipment Company Inc.

- EndFlex LLC

- Douglas Machine Inc.

- Delkor Systems Inc.

- ADCO Manufacturing

- Somic Packaging Inc.

- Econocorp Inc.

- BluePrint Automation B.V.

- JLS Automation

- Hamrick Manufacturing and Service Inc.

- Texwrap Packaging Systems LLC

- Kliklok-Woodman LLC

- PMI KYOTO Packaging Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Labor Costs Prompting Automation Adoption

- 4.2.2 Boom in E-Commerce Fulfillment Centers

- 4.2.3 Stricter Food Safety Packaging Regulations

- 4.2.4 Integration of Vision-Guided Robotics

- 4.2.5 Adoption of Plug-and-Play Modular Machines

- 4.2.6 Shift Toward Recyclable Corrugated Materials

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure

- 4.3.2 Limited Floor Space in Legacy Facilities

- 4.3.3 Skilled Technician Shortage for Maintenance

- 4.3.4 Supply Chain Volatility of Corrugated Board

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Regular Slotted Case Erectors

- 5.1.2 Tablock Case Erectors

- 5.1.3 Tray Forming Erectors

- 5.1.4 Specialty Case Erectors

- 5.2 By Speed Band (Cartons per Minute)

- 5.2.1 Up to 20 CPM

- 5.2.2 20-40 CPM

- 5.2.3 Above 40 CPM

- 5.3 By End-Use Industry

- 5.3.1 Food and Beverage

- 5.3.2 E-Commerce and Retail

- 5.3.3 Pharmaceuticals

- 5.3.4 Industrial Goods

- 5.3.5 Other End-Use Industries

- 5.4 By Automation Level

- 5.4.1 Semi-Automatic

- 5.4.2 Fully Automatic

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ProMach Inc.

- 6.4.2 Syntegon Technology GmbH

- 6.4.3 Combi Packaging Systems LLC

- 6.4.4 Pearson Packaging Systems LLC

- 6.4.5 Lantech LLC

- 6.4.6 Massman Automation Designs LLC

- 6.4.7 Schneider Packaging Equipment Company Inc.

- 6.4.8 EndFlex LLC

- 6.4.9 Douglas Machine Inc.

- 6.4.10 Delkor Systems Inc.

- 6.4.11 ADCO Manufacturing

- 6.4.12 Somic Packaging Inc.

- 6.4.13 Econocorp Inc.

- 6.4.14 BluePrint Automation B.V.

- 6.4.15 JLS Automation

- 6.4.16 Hamrick Manufacturing and Service Inc.

- 6.4.17 Texwrap Packaging Systems LLC

- 6.4.18 Kliklok-Woodman LLC

- 6.4.19 PMI KYOTO Packaging Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

移動物流機器人市場規模、佔有率和成長分析:按類型、有效載荷能力、電池類型、應用、最終用戶產業、部署模式和地區分類-2026-2033年產業預測

移動物流機器人市場規模、佔有率和成長分析:按類型、有效載荷能力、電池類型、應用、最終用戶產業、部署模式和地區分類-2026-2033年產業預測 物流機器人市場機會、成長要素、產業趨勢分析及2026-2035年預測。

物流機器人市場機會、成長要素、產業趨勢分析及2026-2035年預測。 物流機器人市場:機器人類型、功能、負載容量、動力來源、應用及最終用途-2026-2032年全球市場預測

物流機器人市場:機器人類型、功能、負載容量、動力來源、應用及最終用途-2026-2032年全球市場預測 物流機器人市場報告:按組件、機器人類型、功能、運作領域、最終用戶產業和地區分類(2026-2034 年)

物流機器人市場報告:按組件、機器人類型、功能、運作領域、最終用戶產業和地區分類(2026-2034 年) 全球物流機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)托盤轉移模組市場:按類型、應用、終端用戶產業、自動化程度、負載能力和分銷管道分類-全球預測,2026-2032年自動瓦楞紙板組裝機市場機會、成長要素、產業趨勢分析及2026年至2035年預測。全球箱體安裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球自動化瓦楞紙板組裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球物流機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)托盤轉移模組市場:按類型、應用、終端用戶產業、自動化程度、負載能力和分銷管道分類-全球預測,2026-2032年自動瓦楞紙板組裝機市場機會、成長要素、產業趨勢分析及2026年至2035年預測。全球箱體安裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球自動化瓦楞紙板組裝機市場規模、佔有率、趨勢及成長分析報告(2026-2034) 物流機器人市場:依組件、產業、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

物流機器人市場:依組件、產業、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測