|

市場調查報告書

商品編碼

2044041

日本LED基板用藍寶石晶體生長設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

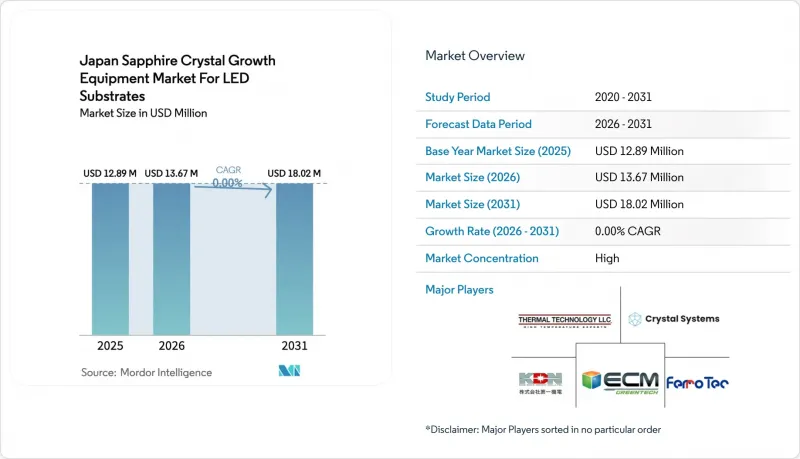

日本用於 LED基板的藍寶石晶體生長設備的市場預計將從 2025 年的 1,289 萬美元成長到 2026 年的 1,367 萬美元,到 2031 年達到 1,802 萬美元,2026 年至 2031 年的複合年成長率為 5.68%。

儘管通用照明需求停滯不前,但受mini-LED和micro-LED背光顯示面板強勁需求的推動,國內對大直徑、低缺陷藍寶石爐的訂單正在成長。柴可拉斯基法。同時,整合測量技術和人工智慧驅動的控制模組正在提高良率並降低對人事費用的依賴。雖然能源成本波動和銥、鉬供應鏈緊張仍然是小規模外延製造商的負擔,但政府補貼和國內元件製造商的垂直整合正在縮短新設備的實際投資回收期。

日本藍寶石晶體生長設備(用於LED基板)市場趨勢及展望

高解析度顯示器對Mini-LED和Micro-LED背光的需求日益成長

高階電視、筆記型電腦和汽車OEM廠商正計劃在2025年前從側入式LED架構轉向mini-LED架構,這將使每個面板的晶片級發光元件數量翻倍,並迫使藍寶石晶圓製造商延長生產宣傳活動。目前,商用micro-LED先導計畫的目標是在6吋c面藍寶石基板上生長尺寸小於100µm的晶片,透過省去彩色濾光片和厚封裝,實現更薄、對比度更高的顯示器。大阪大學已展示了在藍寶石基板上生長的摻銪GaN紅色LED,其外部量子效率接近10%,無需晶片轉移製程即可實現單片全彩堆疊。 Orbray公司正積極回應,提供總厚度偏差小於10µm的高平整度6英寸基板,加速其位於德島和山口的工廠的生產。電動車駕駛座對汽車等級可靠性的需求(這些駕駛艙配備多個高解析度顯示器)進一步支撐了國內藍寶石的需求。

政府獎勵國內LED供應鏈本地化。

2024年,東京撥款約8.7億美元用於化合物半導體研發中心,並建立了一條專門用於藍寶石基板上生長寬頻隙裝置的生產線。這些補貼將把小規模外延企業的晶體生長爐的恢復期從七年縮短至約四年,同時人才培養計畫將重建因2010年代境外外包浪潮而流失的人才儲備。 2023年中國暫時限制鎵和鍺出口後,安全的擔憂加劇,進一步凸顯了這個迫切性。政策制定者目前的目標是到2030年實現藍寶石晶圓國內30%的自給率,這意味著晶體生長爐的年部署率將比歷史平均高出15%至20%。

中小企業外延製造設施的資本密集爐體採購週期

高階的開羅普洛斯(Cairopulos)和柴可拉斯基法設備造價在30萬至150萬美元之間,而客製化的大型藍寶石熔煉爐系統則超過200萬美元,這使得許多國內專業製造商難以負擔。每台熔煉爐單次出晶需要10至20天,除非運轉率超過85%,否則年產量只能達到約18次出晶,導致投資回收期超過五年。日本缺乏成熟的藍寶石製造設備租賃市場,迫使中小企業自行融資或依賴高利專案貸款,這兩種方式都會加劇營運資金緊張。一些工廠透過將晶圓製造外包給低成本的中國供應商來應對,但這犧牲了前置作業時間管理和客製化服務。這種限制直接延緩了向最先進的自動化熔煉爐升級換代的進程,而升級換代本可以提高良率並降低電力消耗。

細分市場分析

預計到2025年,晶體生長爐將佔據日本藍寶石晶體生長設備(用於LED基板)市場67.91%的佔有率,凸顯其作為最大單一資本財的地位。加熱場和坩堝組件是第二大成本項目,其中鉬基替換件每個售價約為500美元,而純度要求高達99.99%的銥坩堝價格也居高不下。生長自動化和製程控制系統雖然佔地面積小,但由於其能夠透過人工智慧視覺和腔內測量技術減少廢料和操作人員的工作量,預計其複合年成長率將達到6.17%。大型積體電路製造商正在採購整合式晶體生長爐和自動化系統的承包工程,以提高無塵室每平方公尺的生產效率,而小規模的專業製造商通常仍使用手動抽屜來減少資金消耗。

競爭對手的趨勢因買家類型而異。歐美供應商主導對直徑公差要求嚴格的高階項目,而注重成本的中國供應商則瞄準周邊地區,價格低30-40%。儘管由於勞動力短缺加劇,新爐的絕對數量略有增加,但預計自動化方面的投入將逐步擴大日本LED基板用藍寶石晶體生長設備的市場佔有率。在預測期內,軟體和感測器升級預計將比單純的硬體輸出改進帶來更大的附加價值,從而重塑供應商的選擇標準。

《日本藍寶石晶體生長設備市場報告(適用於LED基板產業)》依設備類型(晶體生長爐、熱場/坩堝系統等)、生長技術(Cairopulos法、邊緣限定薄膜進料生長法、熱交換器法等)以及藍寶石晶體直徑處理能力(150mm及以下、150-300mm、300mm以上)進行分類。市場預測以美元計價。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高解析度顯示器對Mini-LED和Micro-LED背光的需求日益成長

- 政府獎勵促進國內LED供應鏈本地化。

- 日本LED IDM公司正將6吋晶圓生產線納入主流生產流程

- 透過反應器自動化和基於人工智慧的過程控制提高效率。

- 家用電子電器閃光燈LED過渡到8吋藍寶石晶圓

- 藍寶石基板氮化鎵功率元件在電動車充電器中的崛起

- 市場限制因素

- 中小型外延製造商的資本密集型反應器採購週期

- 2025年照明維修高峰過後,LED最終市場需求的波動性

- 日本2000 度C以上高溫區的能源成本高昂

- 鉬和銥坩堝材料的供應風險

- 工業生態系分析

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過裝置

- 晶體生長爐

- 熱場與坩堝系統

- 成長自動化和製程控制系統

- 透過成長技術

- 基洛普洛斯法

- 邊緣限定薄膜輸送方法(EFG)

- 熱交換器法

- 柴可拉斯基法

- 按直徑和容量分類的藍寶石

- 小於150毫米

- 150~300 mm

- 超過 300 毫米

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ferrotec Holdings Corporation

- Dai-ichi Kiden Co., Ltd.

- Crystal Systems Corporation

- ECM Greentech SA

- Thermal Technology LLC

- GT Advanced Technologies Inc.

- PVA TePla AG

- Luoyang Kunsheng Instrument Equipment Co., Ltd.

- Shanghai Xinkehui New Material Co., Ltd.

- ATTL Advanced Materials Co., Ltd.

- TechSapphire LLC

- EZAN-ERIE Ltd.

- Rostoks-N Ltd.

- APEKS Co., Ltd.

- Apollo Crystal LLC

- Ferrotec Material Technologies Corporation

- FAMETEC GmbH

第7章 市場機會與未來展望

The Japan sapphire crystal growth equipment market for LED substrates industry size is expected to increase from USD 12.89 million in 2025 to USD 13.67 million in 2026 and reach USD 18.02 million by 2031, growing at a CAGR of 5.68% over 2026-2031.

Strong display-panel demand for mini-LED and micro-LED back-lighting is widening the domestic order book for large-diameter, low-defect sapphire furnaces, even as general-lighting demand plateaus. Equipment spending is heavily skewed toward Kyropoulos and Czochralski furnaces that can yield 6-inch and 8-inch boules with stable thermal gradients, while integrated metrology and AI-driven control modules push yields higher and labor dependency lower. Energy-cost volatility and tight iridium and molybdenum supply chains still weigh on smaller epitaxial houses, but government subsidies and vertical-integration moves by local component makers are trimming effective payback horizons for new tool installs.

Insights and Trends of Japan Sapphire Crystal Growth Equipment Market For LED Substrates

Rising Demand for Mini- and Micro-LED Back-lighting in High-Resolution Displays

Premium television, notebook, and automotive OEMs moved from edge-lit to mini-LED architectures during 2025, multiplying the number of die-level emitters per panel and pushing sapphire-wafer pullers to run longer campaigns. Commercial micro-LED pilots now target sub-100 µm die sizes grown on 6-inch c-plane sapphire, eliminating color filters and thick encapsulants for thinner displays with higher contrast. Osaka University demonstrated europium-doped GaN red LEDs on sapphire that approach 10% external quantum efficiency, allowing monolithic full-color stacks without die-transfer steps. Orbray responded with high-flatness 6-inch substrates that show total-thickness variation below 10 µm, accelerating adoption at Tokushima and Yamaguchi fabs. Electric-vehicle cockpits, which house multiple high-resolution displays, add an auto-grade reliability requirement that further anchors domestic sapphire demand.

Government Incentives for Domestic LED Supply-Chain Localization

Tokyo earmarked roughly USD 870 million in 2024 for compound-semiconductor R&D hubs, with dedicated lines for wide-band-gap devices grown on sapphire. Subsidies lower crystal-growth furnace payback from seven to about four years for small epitaxial houses, while workforce programs rebuild a talent pool hollowed out during the 2010s offshoring wave. Security concerns heightened urgency when China briefly restricted gallium and germanium exports in 2023; policymakers now target 30% local sapphire-wafer self-sufficiency by 2030, implying annual furnace installations 15-20% above historical norms.

Capital-Intensive Furnace Procurement Cycle for SME Epi-Houses

Premium Kyropoulos and Czochralski tools carry list prices ranging from USD 300,000 to USD 1.5 million, and custom large-boule systems exceed USD 2 million, placing them out of reach for many domestic specialty producers. Each furnace needs 10-20 days per pull, capping annual output near 18 runs and stretching payback horizons beyond five years unless utilization stays above 85%. Japan lacks a mature leasing market for sapphire equipment, so smaller firms must either self-fund or rely on high-interest project loans, both of which constrain working capital. Some plants respond by outsourcing wafers to low-cost Chinese suppliers, sacrificing lead-time control and custom orientation options. This restraint directly slows the refresh cycle for modern, automation-ready furnaces that could lift yields and cut power use.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Adoption of 6-Inch Wafer Lines by Japanese LED IDMs

- Volatility in LED End-Market Demand Post-2025 Lighting Retrofit Peak

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystal growth furnaces commanded 67.91% of the Japan sapphire crystal growth equipment market for LED substrates industry market share in 2025, underscoring their position as the largest single capital item. Thermal-field and crucible kits form the next cost block, with molybdenum replacements priced near USD 500 per piece and iridium containers fetching premium quotes on 99.99% purity needs. Growth-automation and process-control systems, while starting from a smaller base, are projected at a 6.17% CAGR because AI vision and in-chamber metrology cut scrap and operator minutes. Large integrated device manufacturers buy turnkey furnace-plus-automation bundles to raise throughput per clean-room square meter, whereas small specialty houses often continue with manual pullers to contain cash burn.

Competitive dynamics vary by buyer profile. Western vendors dominate high-end projects that demand tight diameter tolerances, while cost-focused Chinese suppliers court peripheral prefectures with 30-40% lower ticket prices. As labor shortages deepen, automation spending should capture an incrementally larger slice of the Japan sapphire crystal growth equipment market for LED substrates industry market size, even if the absolute number of new furnaces rises only modestly. Over the forecast horizon, software and sensor upgrades are expected to deliver more incremental value than hardware wattage alone, reshaping vendor qualification criteria.

The Japan Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and More), and Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and Above 300 Mm). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ferrotec Holdings Corporation

- Dai-ichi Kiden Co., Ltd.

- Crystal Systems Corporation

- ECM Greentech S.A.

- Thermal Technology LLC

- GT Advanced Technologies Inc.

- PVA TePla AG

- Luoyang Kunsheng Instrument Equipment Co., Ltd.

- Shanghai Xinkehui New Material Co., Ltd.

- ATTL Advanced Materials Co., Ltd.

- TechSapphire LLC

- EZAN-ERIE Ltd.

- Rostoks-N Ltd.

- APEKS Co., Ltd.

- Apollo Crystal LLC

- Ferrotec Material Technologies Corporation

- FAMETEC GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Mini- and Micro-LED Backlighting in High-Resolution Displays

- 4.2.2 Government Incentives for Domestic LED Supply-Chain Localization

- 4.2.3 Mainstream Adoption of 6-inch Wafer Lines by Japanese LED IDMs

- 4.2.4 Efficiency Gains from Furnace Automation and AI-Based Process Control

- 4.2.5 Shift Toward 8-inch Sapphire Wafers in Consumer Electronics Flash LEDs

- 4.2.6 Emergence of GaN-on-Sapphire Power Devices in EV Chargers

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Furnace Procurement Cycle for SME Epi-Houses

- 4.3.2 Volatility in LED End-Market Demand Post 2025 Lighting Retrofit Peak

- 4.3.3 High Energy Costs for Above 2000 °C Thermal Fields in Japan

- 4.3.4 Supply Risk of Molybdenum and Iridium Crucible Materials

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Up to 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ferrotec Holdings Corporation

- 6.4.2 Dai-ichi Kiden Co., Ltd.

- 6.4.3 Crystal Systems Corporation

- 6.4.4 ECM Greentech S.A.

- 6.4.5 Thermal Technology LLC

- 6.4.6 GT Advanced Technologies Inc.

- 6.4.7 PVA TePla AG

- 6.4.8 Luoyang Kunsheng Instrument Equipment Co., Ltd.

- 6.4.9 Shanghai Xinkehui New Material Co., Ltd.

- 6.4.10 ATTL Advanced Materials Co., Ltd.

- 6.4.11 TechSapphire LLC

- 6.4.12 EZAN-ERIE Ltd.

- 6.4.13 Rostoks-N Ltd.

- 6.4.14 APEKS Co., Ltd.

- 6.4.15 Apollo Crystal LLC

- 6.4.16 Ferrotec Material Technologies Corporation

- 6.4.17 FAMETEC GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment