|

市場調查報告書

商品編碼

2044037

用於LED基板的藍寶石晶體生長設備:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

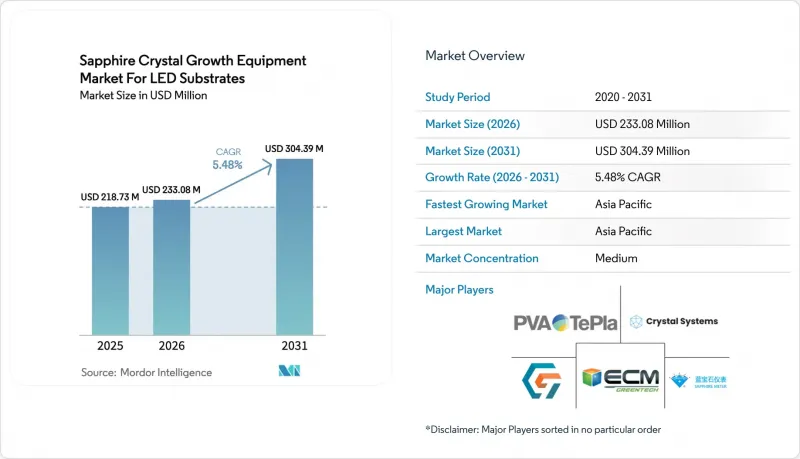

預計到 2031 年,用於 LED基板的藍寶石晶體生長設備的市場規模將達到 3.0439 億美元,在預測期(2026-2031 年)內以 5.48% 的複合年成長率成長,從 2025 年的 2.1873 億美元成長到 20230 億美元。

北美和歐洲通用照明需求的放緩,恰逢Mini-LED背光、汽車抬頭顯示器和擴增實境(AR)設備對規格要求的不斷提高。儘管中國外延代工廠在2024年至2025年間佔據了全球藍寶石晶圓產能擴張的約60%,但其近期的資本投資主要集中在大直徑晶錠和先進自動化領域,導致傳統4英寸生產線的訂單週期緊張。西方熔爐供應商憑藉其取得專利的熱場設計,在300毫米以上的系統中保持著市場佔有率,而中國競爭對手則憑藉價格競爭力和本地化服務,在150-300毫米細分市場迅速崛起。高階顯示器的普及以及美國能源局和歐盟生態設計指令下持續推行的LED維修強制令之間的相互作用,將決定預計的成長曲線能否突破目前個位數的基準增速。

用於LED基板的藍寶石晶體生長設備的市場趨勢與展望

中國外延代工廠積極擴張產能

2024年至2025年間,中國LED晶片製造商已投入運作超過150台新的MOCVD反應爐。其中,三安光電和HC SemiTek引領潮流,後者投資28億元人民幣(約3.92億美元)的揚州計畫旨在生產mini-LED和micro-LED的基板。此舉導致6吋和8吋藍寶石晶圓的短期需求激增,但也促使採購轉向150-300毫米及以上尺寸的爐體,以最佳化單爐產能。國務院撥款500億元人民幣(約70億美元)用於化合物半導體基礎建設,推動了產能擴張。然而,由於2025年第一季晶圓平均售價年減12%,買家被迫優先考慮自動化以縮短生產週期。因此,設備升級週期正在加快,人工智慧驅動的製程控制軟體包的採用率正在提高,能夠將反應器硬體與預測分析相結合的供應商正在從中受益。

高階電視採用迷你LED背光技術的趨勢正在快速成長。

預計2024年,高階電視製造商將出貨約800萬台mini-LED電視,較2023年成長35%。三星電子和LG Display正在坡州及其他地區擴建面板產能。每個mini-LED陣列都依賴高品質的藍寶石基板,以實現數千個發光晶片的品質匹配,雜質容差嚴格控制在1ppm以下。類似的架構也正被考慮用於汽車抬頭顯示器和新興的AR眼鏡,這進一步推動了對無缺陷晶體的需求。設備OEM廠商現在面臨客戶提出的新規格,而這些規格無法透過老舊的Cairopulos製程生產線滿足,除非進行高成本的改造,或完全更換為位錯密度更低的柴可拉斯基法設備。這些高額要求推高了每台熔爐的平均售價(ASP),同時也確保了耗材和軟體升級帶來的生命週期收入。

與碳化矽爐生產線相比,需要更高的資本投資。

承包的200毫米藍寶石生產線造價在800萬美元到1200萬美元之間,而同等尺寸的碳化矽(SiC)昇華系統造價僅為500萬美元到700萬美元。同時,SiC晶圓的價格卻高出30%到40%。政府的獎勵,特別是美國的《晶片技術創新法案》(CHIPS Act),不成比例地偏向SiC和其他寬能隙材料,進一步分散了投資。以目前LED的平均售價計算,藍寶石製造設備的投資回收期為4到5年,這對於尋求更快回報的創業投資參與企業來說是一個障礙。儘管供應商正透過訂閱式設備和基於性能的定價模式來減輕高昂的前期成本負擔,但由於資金籌措,中型晶圓廠的採用速度仍然緩慢。

細分市場分析

預計到2025年,晶體生長爐將佔藍寶石晶體生長設備市場支出的69.87%,凸顯其在LED基板藍寶石晶體生長設備市場中的核心地位。然而,代工廠擴大將晶體生長爐和以軟體為中心的製程控制軟體包作為一套設備進行銷售,預計到2024年,自動化普及率將達到42%。在LED基板藍寶石基板生長設備市場中,受薪資上漲和日益嚴格的顯示器規格的推動,自動化和製程控制系統的市佔率預計將以6.13%的複合年成長率成長至2031年,成長速度最為迅猛。歐美原始設備製造商(OEM)正透過人工智慧驅動的熱場最佳化技術來凸顯自身優勢,而中國供應商則憑藉高產能晶圓廠青睞的整體擁有成本(TCO)保證來展開競爭。

雖然設備的平均更換週期為 8-10 年,但向 300 毫米尺寸的轉變縮短了折舊免稅額期,迫使仍可使用的 6 英寸設備進行折舊。另一方面,自動化平台的更換週期較短,僅為 3-5 年,這創造了持續的收入來源,並保護供應商免受爐訂單波動的影響。石墨坩堝和高純度氧化鋁等耗材進一步將客戶捲入 OEM 生態系統,逐漸將競爭優勢從硬體價格轉移到整體解決方案的性能。

《LED基板用藍寶石晶體生長設備市場》產業報告按設備類型(晶體生長爐、熱場/坩堝系統等)、生長技術(Cairopulos法、邊緣限定薄膜進料生長法、熱交換器法等)、藍寶石晶體直徑處理能力(150mm以下、150-300mm、300mm以上)和地區進行細分。市場預測以美元計價。

區域分析

預計到2025年,亞太地區將佔據LED基板用藍寶石晶體生長設備市場72.68%的佔有率,並將以5.72%的複合年成長率持續成長至2031年。光是中國就佔全球晶圓產量的約55%,這得益於地方政府補貼抵銷了爐體折舊免稅額。台灣地區專注於高利潤率的mini-LED基板,而韓國的三星顯示器和LG顯示正在迅速擴大mini-LED電視的產能,間接推動了對藍寶石基板的需求。日本現有的LED企業正將資本投資轉向SiC和GaN,但日亞化學工業株式會社和豐田合成株式會社的需求仍維持著日本國內設備市場的一個細分領域。

預計2025年,北美和歐洲合計約佔全球銷售額的18%,但受到LED晶片製造地短缺和補貼項目嚴重偏向功率電子領域的限制。美國的《晶片與科學法案》僅將一小部分資金分配給藍寶石,而Wolfspeed向碳化矽(SiC)的策略轉型導致一些以往的主要買家退出市場。同樣,歐洲的《晶片與科學法案》也著重於先進邏輯電路與碳化矽,將藍寶石的需求留給了Monocrystal等專業供應商。然而,該公司對歐盟的供貨受到製裁的影響。儘管相關法規仍在推動LED的普及,但由此產生的基板訂單主要集中在亞洲的代工廠。

儘管2025年「世界其他地區」的銷售額佔比不到10%,但由於沙烏地阿拉伯、阿拉伯聯合大公國和巴西的基礎設施電氣化進程,預計該地區將進一步成長。印度100億美元的「半導體發展計畫」可能會在2028年至2030年間重塑市場格局,儘管截至2026年3月,訂單。設備製造商正在探索合資組裝模式,以滿足潛在的國內採購需求,尤其是在南亞各國政府考慮推出在地採購獎勵的情況下。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高階電視中Mini-LED背光技術的快速普及。

- 中國外延代工廠積極擴張產能

- 根據美國能源局(DOE) 和歐盟生態設計條例,履行節能義務。

- 過渡到 300mm 藍寶石晶錠以減少晶圓 CMP 損耗。

- 將人工智慧驅動的預測控制整合到生長反應器中

- 印度擴大對化合物半導體叢集的資本補貼

- 市場限制因素

- 氧化鋁價格波動給OEM廠商的利潤率帶來了壓力。

- 與碳化矽爐生產線相比,需要更高的資本投資。

- 使用大直徑鑽頭進行岩心鑽探時產量降低。

- 從2024年起,歐洲對LED照明維修的需求將會下滑

- 宏觀經濟因素對市場的影響

- 產業生態系分析

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過裝置

- 晶體生長爐

- 熱場與坩堝系統

- 培訓自動化和製程控制系統

- 訓練技巧

- 脊椎矯正療法

- 邊緣限定薄膜輸送方法(EFG)

- 熱交換器法

- 柴可拉斯基法

- 按直徑和容量分類的藍寶石

- 小於150毫米

- 150~300 mm

- 300毫米或以上

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- GT Advanced Technologies Inc.

- PVA TePla AG

- ECM Greentech SA(Cyberstar)

- Crystal Systems Inc.

- Zhejiang Jingjing Science and Technology Co., Ltd.

- Crystec Technology Trading GmbH

- Monocrystal LLC

- Ferrotec Holdings Corporation

- Castech Inc.

- Linton Crystal Technologies

- Hangzhou Shalom Electro-optics Technology Co., Ltd.

- Advanced Crystal Technology Inc.

- Naura Technology Group Co., Ltd.

- Toyo Tanso Co., Ltd.

- Changchun Up Optotech Co., Ltd.

- Silian Optoelectronics(Chongqing)Co., Ltd.

- Heraeus Noblelight Ltd

第7章 市場機會與未來展望

The sapphire crystal growth equipment market for LED substrates market size was valued at USD 218.73 million in 2025, USD 233.08 million in 2026, and reach USD 304.39 million by 2031, at a CAGR of 5.48% during the forecast period (2026-2031).

Moderating general-illumination demand in North America and Europe coincides with rising specification pressure from mini-LED backlighting, automotive head-up displays and augmented-reality devices. Chinese epitaxy foundries accounted for roughly 60% of global sapphire wafer capacity additions between 2024 and 2025, yet their recent equipment spend skews toward larger-diameter boules and advanced automation, compressing order cycles for legacy 4-inch lines. Western furnace vendors defend share in above-300 mm systems by leveraging patented thermal-field designs, while Chinese peers gain traction in the 150-300 mm segment through price leadership and localized service. The interplay between premium display uptake and continued LED retrofit mandates under the U.S. Department of Energy and European Union Ecodesign directive will determine whether the projected growth curve accelerates beyond today's mid-single-digit baseline.

Insights and Trends of Sapphire Crystal Growth Equipment Market For LED Substrates

Aggressive Capacity Expansion by Chinese Epitaxy Foundries

Chinese LED chipmakers commissioned more than 150 new MOCVD reactors during 2024-2025, spearheaded by San'an Optoelectronics and HC SemiTek, whose CNY 2.8 billion (USD 392 million) Yangzhou project targets mini-LED and micro-LED substrates. This uptick triggered a near-term spike in demand for 6-inch and 8-inch sapphire wafers, yet it also realigned procurement toward 150-300 mm and above-300 mm furnaces that optimize throughput per boule. State Council funding of CNY 50 billion (USD 7 billion) for compound-semiconductor infrastructure reinforces the build-out, although wafer ASPs slipped 12% year-on-year in Q1 2025, compelling buyers to prioritize automation that compresses cycle time. The net effect raises installed base turnover and lifts attach rates for AI-driven process-control packages, benefiting suppliers able to combine furnace hardware with predictive analytics.

Surging Mini-LED Backlighting Adoption in High-End TVs

Premium television manufacturers shipped roughly 8 million mini-LED sets in 2024, a 35% jump over 2023, with Samsung Electronics and LG Display expanding panel capacity at Paju and other hubs. Each mini-LED array relies on a higher-quality sapphire substrate to achieve bin-matching for thousands of emissive chips, tightening impurity tolerances to sub-1 ppm. Automotive head-up displays and emerging AR glasses evaluate similar architectures, further lifting demand for defect-free boules. Equipment OEMs now face customer specifications that older Kyropoulos lines can meet only via costly retrofits or complete replacement with Czochralski tools that deliver lower dislocation densities. These premium requirements raise per-furnace ASPs but also lock in higher lifecycle revenue from consumables and software upgrades.

High Capex Requirement Compared with SiC Furnace Lines

A turnkey 200 mm sapphire line costs USD 8-12 million, versus USD 5-7 million for an equivalently sized silicon-carbide sublimation setup, while SiC wafers sell at 30-40% higher prices. Government incentives, notably the U.S. CHIPS Act, disproportionately favor SiC and other wide-bandgap materials, further diverting investment. Payback for sapphire tools stretches to 4-5 years under current LED ASPs, a hurdle for venture-backed entrants seeking quicker returns. Vendors mitigate sticker shock through equipment-as-a-service offerings and outcome-based pricing, yet financing constraints still delay adoption among second-tier fabs.

Other drivers and restraints analyzed in the detailed report include:

- Transition Toward 300 mm Sapphire Boules to Reduce Wafer CMP Loss

- Energy Savings Mandates from U.S. DOE and EU Ecodesign

- Volatile Alumina Prices Tightening OEM Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystal growth furnaces anchored 69.87% of 2025 spending, underscoring their central role in the sapphire crystal growth equipment market for LED substrates industry market size. Foundries, however, now increasingly bundle furnaces with software-centric process control packages, lifting automation attach rates to 42% in 2024. The sapphire crystal growth equipment market for LED substrates industry market share for automation and process control systems is poised to expand fastest at 6.13% CAGR through 2031 as wage inflation and tighter display specifications converge. Western OEMs differentiate through AI-driven thermal-field optimization, while Chinese vendors compete on total-cost-of-ownership guarantees that resonate with high-throughput fabs.

Replacement cycles average 8-10 years, yet the pivot to 300 mm compresses depreciation schedules, forcing write-offs of serviceable 6-inch tools. Automation platforms enjoy shorter three-to-five-year refresh intervals, creating a recurring revenue stream that cushions suppliers from furnace order volatility. Consumables such as graphite crucibles and high-purity alumina further lock customers into OEM ecosystems, gradually shifting competitive leverage from hardware price to total solution performance.

The Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and More), Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and Above 300 Mm), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 72.68% of the sapphire crystal growth equipment market for LED substrates industry market size in 2025 and is tracking a 5.72% CAGR through 2031. China alone absorbed roughly 55% of global wafer output, fueled by municipal subsidies that offset furnace depreciation. Taiwan specializes in high-margin mini-LED substrates, while South Korea's Samsung Display and LG Display balloon mini-LED TV capacity, indirectly ratcheting up sapphire substrate pull. Japan's LED incumbents divert capex to SiC and GaN, yet demand from Nichia and Toyoda Gosei still sustains a niche domestic equipment market.

North America and Europe collectively represented about 18% of 2025 revenue, constrained by limited LED chip fab footprints and subsidy programs skewed toward power electronics. The U.S. CHIPS and Science Act directed only a fractional slice of funding toward sapphire, and Wolfspeed's strategic pivot to SiC eliminated a major historical buyer. Europe's Chips Act similarly orients toward advanced logic and SiC, leaving sapphire consumption to specialized vendors such as Monocrystal, whose EU shipments face sanctions-related friction. Regulations still spur LED adoption, but the resulting substrate orders largely accrue to Asian foundries.

The Rest of the World accounted for less than 10% of sales in 2025, yet infrastructure electrification in Saudi Arabia, the UAE and Brazil positions the region for incremental gains. India's USD 10 billion Semiconductor Mission could alter the map by 2028-2030, though no sapphire tool orders were booked as of March 2026. Equipment OEMs weigh joint-venture assembly models to satisfy potential domestic-content rules, especially as South Asian governments explore localization incentives.

- GT Advanced Technologies Inc.

- PVA TePla AG

- ECM Greentech S.A. (Cyberstar)

- Crystal Systems Inc.

- Zhejiang Jingjing Science and Technology Co., Ltd.

- Crystec Technology Trading GmbH

- Monocrystal LLC

- Ferrotec Holdings Corporation

- Castech Inc.

- Linton Crystal Technologies

- Hangzhou Shalom Electro-optics Technology Co., Ltd.

- Advanced Crystal Technology Inc.

- Naura Technology Group Co., Ltd.

- Toyo Tanso Co., Ltd.

- Changchun Up Optotech Co., Ltd.

- Silian Optoelectronics (Chongqing) Co., Ltd.

- Heraeus Noblelight Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mini-LED Backlighting Adoption in High-End TVs

- 4.2.2 Aggressive Capacity Expansion by Chinese Epitaxy Foundries

- 4.2.3 Energy Savings Mandates From U.S. DOE and EU Ecodesign

- 4.2.4 Transition Toward 300 mm Sapphire Boules to Reduce Wafer CMP Loss

- 4.2.5 Integration of AI-Enabled Predictive Control in Growth Furnaces

- 4.2.6 Accelerated Capital Subsidies for Compound-Semiconductor Clusters in India

- 4.3 Market Restraints

- 4.3.1 Volatile Alumina Prices Tightening OEM Margins

- 4.3.2 High Cap-Ex Requirement Compared with SiC Furnace Lines

- 4.3.3 Yield Losses During Core-Drilling of Large-Diameter Boules

- 4.3.4 Sluggish LED Lighting Retrofit Demand in Europe Post-2024

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Ecosystem Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Upto 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GT Advanced Technologies Inc.

- 6.4.2 PVA TePla AG

- 6.4.3 ECM Greentech S.A. (Cyberstar)

- 6.4.4 Crystal Systems Inc.

- 6.4.5 Zhejiang Jingjing Science and Technology Co., Ltd.

- 6.4.6 Crystec Technology Trading GmbH

- 6.4.7 Monocrystal LLC

- 6.4.8 Ferrotec Holdings Corporation

- 6.4.9 Castech Inc.

- 6.4.10 Linton Crystal Technologies

- 6.4.11 Hangzhou Shalom Electro-optics Technology Co., Ltd.

- 6.4.12 Advanced Crystal Technology Inc.

- 6.4.13 Naura Technology Group Co., Ltd.

- 6.4.14 Toyo Tanso Co., Ltd.

- 6.4.15 Changchun Up Optotech Co., Ltd.

- 6.4.16 Silian Optoelectronics (Chongqing) Co., Ltd.

- 6.4.17 Heraeus Noblelight Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment