|

市場調查報告書

商品編碼

2044027

通訊網數位雙胞胎:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Telecom Network Digital Twin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

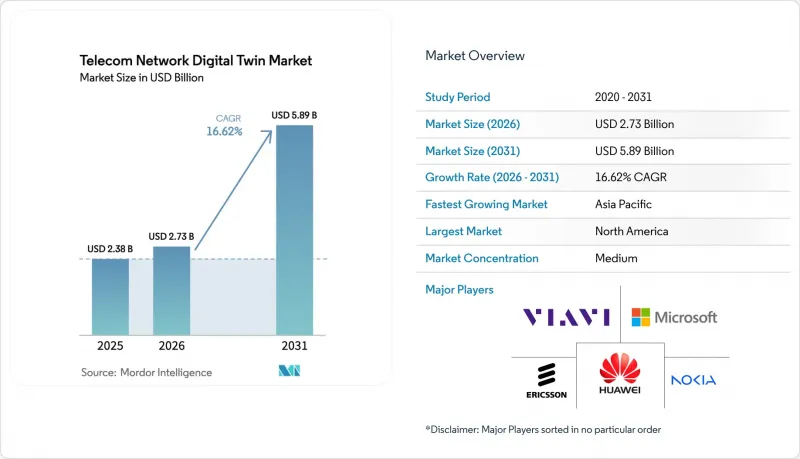

2025 年通訊網數位雙胞胎市場價值為 23.8 億美元,預計到 2031 年將達到 58.9 億美元,而 2026 年為 27.3 億美元,預測期(2026-2031 年)複合年成長率為 16.62%。

這種加速成長反映了電信服務供應商現在如何在運作環境中進行更改之前,先在軟體中模擬無線接入、核心和邊緣資產,從而減少現場部署並縮短升級週期。軟體供應商不斷提高射線追蹤精度和人工智慧驅動的最佳化能力,而超大規模資料中心業者則將通訊模板整合到橫向平台中,從而無需耗時的程式碼客製化。計量型的定價模式推動了雲端技術的日益普及,這種模式將資本成本重新分配到營運預算中。這使得通訊業者能夠將5G和6GHz頻段的投資轉向產生收入應用,成為極具吸引力的選擇。不斷上漲的能源價格和歐洲新的碳排放法規加劇了這種緊迫性,迫使通訊業者利用孿生技術來安排休眠模式,以在不影響服務品質的前提下降低電力成本。同時,O-RAN的開放介面正在擴展合作夥伴生態系統,使小規模分析公司能夠透過通訊業者的應用市場發布專門設計的孿生應用。

全球通訊網數位雙胞胎市場趨勢與洞察:5G RAN 高密度部署需要即時虛擬副本以實現抗干擾規劃

隨著都市區5G部署的增加,大型基地台和小型基地台的數量也隨之增加,如果負責人僅依賴路測,可能會導致吞吐量下降20%至30%。數位雙胞胎能夠擷取地形、障礙物和即時訊號數據,從而對能夠減少同頻道干擾的電線杆位置進行排序。 Verizon利用數位雙胞胎識別並消除重疊波瓣和雨致衰減區域,在紐約和芝加哥將站點購置成本降低了18%。 AT&T正在利用諾基亞的AVA平台對達拉斯的毫米波回程傳輸連結進行預調優。同時,沃達豐德國公司在2025年慕尼黑啤酒節期間應用了愛立信的數位孿生技術,將小區邊緣吞吐量提高了12%。在O-RAN的2026年參考架構中,虛擬副本將與RAN智慧控制器協同工作,透過參數提案在毫秒內實現閉迴路。

將 CSP 遷移到雲端原生核心需要沙箱孿生環境進行 CI/CD 迴歸測試。

容器化的獨立核心每週都會進行軟體部署,任何一個錯誤都可能導致全國範圍的服務中斷。西班牙電信(Telefónica)透過整合 Azure數位雙胞胎作為自動化閘道器,並在推送 Helm Charts 之前重現合成峰值流量,在 2025 年將故障事件減少了 34%。中國移動也在 3GPP研討會上報告了類似的結果,而德國電信正在使用華為的 ICNMaster數位雙胞胎對網路切片隔離進行建模,然後再向企業客戶推廣。 TM Forum 的《2026 年自治網路指南》將基於孿生的測試列為三級自最佳化運行的強制性要求。

高傳真射頻射線追蹤孿生體需要 GPU叢集,這構成了資本支出障礙。

要達到毫米波精度,需要數十億條光線,而NVIDIA的Sionna框架建議至少使用8個H100加速器,這意味著為單一城市建立一個孿生模型的成本超過500萬美元。二級運營商對此持謹慎態度,他們更傾向於使用忽略邊緣干擾的低保真度網格模型。 AWS在2026年透過以模擬次數收費的共用GPU池模式解決了這個問題,但通訊業者仍然擔心網路主權和即時延遲。 Keysight的混合方案結合了粗略規劃和按需高清突發處理,已為巴西和沙烏地阿拉伯的早期採用者降低了40%的前期成本。

細分市場分析

在2025年的電信網路數位雙胞胎市場中,軟體佔比高達67.49%。這主要是因為通訊業者傾向於採用永久授權模式,使其內部團隊能夠在無需重新協商訂閱條款的情況下調整傳播模型。從整合和培訓到託管分析等各類服務正以16.92%的複合年成長率快速成長,直至2031年。這是因為通訊業者缺乏足夠的精通TensorFlow和Python的射頻工程師。諾基亞將現成的3GPP連接器與AVA捆綁銷售,但大多數部署仍需要6-12個月的校準支援。愛立信的託管模式更進一步,其分析團隊會根據數位孿生模型的輸出結果,每週提案參數調整建議。對於希望精簡工程架構的二線營運商而言,這是一個極具吸引力的選擇。

年度維護成本平均佔許可價格的18%至22%,隨著頻寬的擴展,需要提供更新和新的AI模型來維持模型精度。儘管軟體仍是電信網路數位雙胞胎市場的主要主導來源,但由於其服務驅動的特性,市場規模仍在穩定成長。技能提升計畫正在進行中,對外部專家的需求也不斷增加。沃達豐透露,其網路員工中只有不到15%的人具備擴展孿生演算法所需的編碼知識。

到 2025 年,由於低延遲和資料主權政策的需要,企業需要接近性私有資料中心,本地部署的孿生模型將佔總收入的 45.32%。然而,隨著超大規模資料中心超大規模資料中心業者將通訊業專用模組整合到其通用平台中,預計到 2031 年,雲子細分市場將以 18.78% 的複合年成長率成長。微軟和西班牙電信 (Telefónica) 採用了混合模式,將高度敏感的用戶資料儲存在西班牙的資料中心,而 Azure 則用於託管運算密集型模擬。 2026 年,AWS 發布了專為通訊業最佳化的 TwinMaker。它可以自動讀取 3GPP 小區配置,並根據衛星影像產生覆蓋範圍地圖,從而將 Dish Network 和 Rakuten Mobile 等公司的部署時間縮短至 90 天以內。

混合模式的採用凸顯了通訊網數位雙胞胎市場的規模,同時也兼顧了安全性和彈性計算。歐洲依賴混合模式來遵守GDPR,而中國移動則堅持採用本地部署的孿生架構,其300萬個基地台每50毫秒同步一次。付費使用制模式將高峰資本轉化為可預測的營運成本,而由此帶來的會計效益正促使財務長轉向雲端技術。

區域分析

2025年,北美地區的營收佔比達到29.87%。這主要得益於Verizon、AT&T和T-Mobile對開放式無線存取網(Open RAN)數位雙胞胎技術的投資,以簡化聯邦通訊委員會(FCC)要求的6GHz頻段自動頻率調節流程。數位雙胞胎技術減少了路測次數,避免了因都市區規劃而導致的部署延誤,從而幫助通訊業者減輕預算負擔。此外,雲端技術的應用也在持續推進,AWS和微軟的資料中心為通訊業者提供了低延遲環路。

亞太地區到2031年將以16.98%的複合年成長率成長,這主要得益於中國行動平台的推動。該平台每天接收Terabyte的遙測數據,並將基地台停機時間減少了19%。 NTT正在將Twins技術融入其IOWN光子學計畫中,以便在商用服務推出前模擬端到端延遲,並吸引了SONY和豐田等公司作為工業案例。印度通訊部正在鼓勵將Twins技術應用於農村規劃,加速Bharti Airtel和Reliance Jio在服務不足村莊的升級改造。

預計到2025年,歐洲的市佔率將維持在25%左右,但它在能源最佳化領域的創新方面處於主導。 Orange、沃達豐和德國電信正在應用睡眠模式調度孿生技術,以符合歐洲綠色交易的碳排放目標。歐洲電信標準化協會(ETSI)於2026年初發布了同步安全指南草案,以應對歐盟網路安全局(ECA)確定的網路風險。這使得擁有增強型憑證管理的供應商在合規性方面具有優勢。預計到2025年,南美洲和中東及非洲地區的銷售額合計約佔全球總銷售額的五分之一。巴西電信(TIM)和沙烏地阿拉伯電信(stc)正在其5G計畫中部署利用愛立信和華為孿生技術的試點項目,這展現出的發展勢頭有望從2027年起縮小區域差距。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對於密集型 5G RAN,即時虛擬副本對於考慮干擾的規劃至關重要。

- 將 CSP 遷移到雲端原生核心需要沙箱孿生環境進行 CI/CD 迴歸測試。

- 能源成本不斷上漲,促使通訊業者採用基於孿生架構的架構來最佳化其無線存取網睡眠模式。

- O-RAN 的開放介面加速了第三方孿生應用程式的採用。

- 人工智慧產生的合成交通資料集為服務不足的農村地區的城市規劃開闢了新的可能性。

- 6GHz頻段競標之後,利用數位雙胞胎的頻譜共用市場已經出現。

- 市場限制因素

- 高解析度射頻射線追蹤孿生體需要 GPU叢集,這給資本投資帶來了障礙。

- 由於多供應商使用導致模型和模式碎片化,延緩了互通性。

- 從孿生環境到生產環境的同步/網路風險導致監管機構採取謹慎態度。

- 缺乏具備領域知識的機器學習專業人員正在延長引進週期。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 透過網路域

- 無線接取網路(RAN)

- 核心網路

- 運輸/回程傳輸

- Edge/MEC

- 其他網路域(OSS/BSS)

- 最終用戶

- 電信服務供應商(CSP)

- 行動網路營運商(MNO)

- 塔樓公司

- 網際服務供應商(ISP)

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- ASEAN

- 亞太其他地區

- 中東和非洲

- GCC

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- VIAVI Solutions Inc.

- VMware, Inc.

- NEC Corporation

- Samsung Electronics Co., Ltd.

- Amazon Web Services, Inc.

- International Business Machines Corporation(IBM)

- Siemens AG

- Dassault Systemes SE

- PTC Inc.

- Oracle Corporation

- Keysight Technologies, Inc.

- Spirent Communications plc

- Hexagon AB

- Mavenir Systems, Inc.

- Ansys, Inc.

- Cohere Technologies Inc.

第7章 市場機會與未來展望

The Telecom Network Digital Twin Market size was valued at USD 2.38 billion in 2025 and is estimated to grow from USD 2.73 billion in 2026 to reach USD 5.89 billion by 2031, at a CAGR of 16.62% during the forecast period (2026-2031). Accelerated growth reflects how communication service providers now simulate radio-access, core, and edge assets in software before making live changes, trimming truck rolls, and shortening upgrade cycles. Software vendors continue to improve ray-tracing accuracy and AI-driven optimization, while hyperscalers bundle telecom templates into horizontal platforms that eliminate lengthy code customization. Cloud adoption is climbing because consumption-based pricing shifts capital costs into operating budgets, an attractive lever as operators steer 5G and 6 GHz outlays toward revenue-generating apps. Rising energy prices and new carbon caps in Europe add urgency, pushing carriers to use twins for sleep-mode scheduling that cuts electricity bills without harming quality of service. At the same time, O-RAN's open interfaces broaden the partner ecosystem, letting smaller analytics firms release purpose-built twin applications through operator marketplaces.

Global Telecom Network Digital Twin Market Trends and Insights 5G RAN Densification Mandates Real-Time Virtual Replicas for Interference-Aware Planning

Urban 5G rollouts add macro and small cells, which can cause 20%-30% throughput loss when planners rely solely on drive tests. Digital twins ingest terrain, clutter, and live signal data to rank pole locations that lower co-channel interference. Verizon trimmed site-acquisition costs by 18% in New York and Chicago, once its twin-flagged overlapping lobes and rain-fade pockets were removed. AT&T uses Nokia's AVA platform to pre-tune Dallas millimeter-wave backhaul paths, while Vodafone Germany applied Ericsson's twin to boost cell-edge throughput 12% during Oktoberfest 2025. O-RAN's 2026 reference architecture now ties virtual replicas to RAN Intelligent Controllers, enabling parameter proposals to close the loop in milliseconds.

CSP Shift to Cloud-Native Cores Requires Sandbox Twins for CI/CD Regression

Containerized standalone cores bring weekly software drops, and a single misstep can cascade into national outages. Telefonica integrated Azure Digital Twins as an automated gate that replays synthetic peak traffic before every Helm-chart push, cutting incident counts by 34% in 2025. China Mobile reported similar gains in a 3GPP workshop, and Deutsche Telekom models slice isolation in Huawei's ICNMaster twin before onboarding enterprise customers. The TM Forum's 2026 autonomous-network guide positions twin-driven testing as table stakes for Level 3 self-optimizing operations.

High-Fidelity RF Ray-Tracing Twins Demand GPU Clusters, CAPEX Barrier

Millimeter-wave accuracy needs billions of rays, and NVIDIA's Sionna framework recommends at least eight H100 accelerators, pushing a single-city twin above USD 5 million. Tier 2 carriers hesitate, opting for lower-fidelity meshes that skip edge interference. AWS responded in 2026 with per-simulation pricing that rents shared GPU pools, yet operators worry about sovereignty and real-time latency. Keysight's hybrid approach combines coarse planning with on-demand, high-detail bursts, reducing up-front spend by 40% for early adopters in Brazil and Saudi Arabia.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Cost Inflation Pushes Operators to Twin-Based RAN Sleep-Mode Optimization

- O-RAN's Open Interfaces Accelerate Third-Party Twin Apps

- Multi-Vendor Model-Schema Fragmentation Delays Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 67.49% of the telecom network digital twin market in 2025, as carriers favored perpetual licenses that let internal teams tweak propagation models without renegotiating subscription terms. Services spanning integration, training, and managed analytics are pacing ahead at a 16.92% CAGR through 2031 because operators lack sufficient RF engineers with TensorFlow and Python fluency. Nokia bundles ready-made 3GPP connectors with AVA, yet most deployments still require 6 to 12 months of calibration support. Ericsson's managed model goes further, with its analytics squad proposing weekly parameter adjustments based on twin output, an attractive option for Tier 2 carriers that run lean engineering benches.

Annual maintenance averages 18%-22% of license value, providing updates and new AI models that preserve model accuracy as frequency bands expand. The telecom network digital twin market size is tied to services, therefore rises steadily, even though software retains volume leadership. Upskilling programs continue as Vodafone disclosed that fewer than 15% of network staff have the coding knowledge needed to extend twin algorithms, reinforcing external-expert demand.

On-premise twins accounted for 45.32% of revenue in 2025 because low latency and data-sovereignty policies demand proximity to private data centers. The cloud sub-segment, however, grows at an 18.78% CAGR through 2031 as hyperscalers integrate telecom-specific modules into their generic platforms. Microsoft and Telefonica ran a hybrid scheme in which sensitive subscriber data remains within Spanish data centers while Azure hosts compute-intensive simulations. AWS launched a telecom-tuned TwinMaker in 2026 that can automatically load 3GPP cell configurations and generate coverage maps from satellite imagery, reducing deployment time to below 90 days for Dish Network and Rakuten Mobile.

Hybrid adoption shows the size of the telecom network digital twin market, balancing security with elastic compute. Europe leans on hybrid models to comply with GDPR, while China Mobile sticks to on-premises twins that sync every 50 milliseconds with 3 million base stations. Consumption pricing shifts capital peaks into predictable operating lines, and that accounting benefit is nudging CFOs toward cloud commitments.

The Telecom Network Digital Twin Market Report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Network Domain (Radio Access Network (RAN), Core Network, and More), End-User (Communication Service Providers (CSPs), Tower Companies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 29.87% of revenue in 2025 as Verizon, AT&T, and T-Mobile invested in Open RAN digital twins to streamline automated frequency coordination in the 6 GHz band required by the Federal Communications Commission. Carriers gain budget relief when twins cut drive tests and avert deployment delays linked to urban zoning. Cloud adoption also continues to advance, with AWS and Microsoft data centers providing operators with short latency loops.

Asia-Pacific climbs at a 16.98% CAGR toward 2031, fueled by China Mobile's platform that ingests 500 terabytes of telemetry daily to trim base-station downtime by 19%. NTT ties twins into its IOWN photonic program to model end-to-end latency before commercial launch, attracting Sony and Toyota for industrial cases. India's Department of Telecommunications encourages twins for rural planning, accelerating upgrades by Bharti Airtel and Reliance Jio across underserved villages.

Europe hovered near a 25% share in 2025, yet commands innovation leadership on energy optimization. Orange, Vodafone, and Deutsche Telekom apply sleep-mode scheduling twins to align with European Green Deal carbon targets. ETSI issued draft synchronization security guidelines in early 2026, addressing cyber risks flagged by the EU Agency for Cybersecurity, and vendors with hardened credential management now carry a compliance edge. South America and the Middle East and Africa together held roughly one-fifth of 2025 sales. Brazil's TIM and Saudi Arabia's stc run pilots that use Ericsson and Huawei twins for 5G planning, showcasing momentum that could narrow the regional gap post-2027.

List of Companies Covered in this Report:

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- VIAVI Solutions Inc.

- VMware, Inc.

- NEC Corporation

- Samsung Electronics Co., Ltd.

- Amazon Web Services, Inc.

- International Business Machines Corporation (IBM)

- Siemens AG

- Dassault Systemes SE

- PTC Inc.

- Oracle Corporation

- Keysight Technologies, Inc.

- Spirent Communications plc

- Hexagon AB

- Mavenir Systems, Inc.

- Ansys, Inc.

- Cohere Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G RAN Densification Mandates Real-Time Virtual Replicas for Interference-Aware Planning

- 4.2.2 CSP Shift to Cloud-Native Cores Requires Sandbox Twins for CI/CD Regression

- 4.2.3 Energy-Cost Inflation Pushes Operators to Twin-Based RAN Sleep-Mode Optimization

- 4.2.4 O-RAN's Open Interfaces Accelerate Third-Party Twin Apps

- 4.2.5 AI-Curated Synthetic Traffic Datasets Unlock Under-Served Rural Planning

- 4.2.6 Digital-Twin-Enabled Spectrum-Sharing Marketplaces Emerge Post-6 GHz Auctions

- 4.3 Market Restraints

- 4.3.1 High-Fidelity RF Ray-Tracing Twins Demand GPU Clusters, CAPEX Barrier

- 4.3.2 Multi-Vendor Model-Schema Fragmentation Delays Interoperability

- 4.3.3 Twin-to-Live Synchronisation Cyber-Risks Drive Regulatory Caution

- 4.3.4 Scarcity of Domain-Trained ML Talent Lengthens Deployment Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Network Domain

- 5.3.1 Radio Access Network (RAN)

- 5.3.2 Core Network

- 5.3.3 Transport/Backhaul

- 5.3.4 Edge/MEC

- 5.3.5 Other Network Domains (OSS/BSS)

- 5.4 By End-User

- 5.4.1 Communication Service Providers (CSPs)

- 5.4.2 Mobile Network Operators (MNOs)

- 5.4.3 Tower Companies

- 5.4.4 Internet Service Providers (ISPs)

- 5.4.5 Other End-users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Nigeria

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nokia Corporation

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Microsoft Corporation

- 6.4.5 VIAVI Solutions Inc.

- 6.4.6 VMware, Inc.

- 6.4.7 NEC Corporation

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Amazon Web Services, Inc.

- 6.4.10 International Business Machines Corporation (IBM)

- 6.4.11 Siemens AG

- 6.4.12 Dassault Systemes SE

- 6.4.13 PTC Inc.

- 6.4.14 Oracle Corporation

- 6.4.15 Keysight Technologies, Inc.

- 6.4.16 Spirent Communications plc

- 6.4.17 Hexagon AB

- 6.4.18 Mavenir Systems, Inc.

- 6.4.19 Ansys, Inc.

- 6.4.20 Cohere Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions

通訊網路虛擬化市場預測至2034年-按組件、技術、部署模式、網路功能類型、應用、最終用戶和地區分類的全球分析

通訊網路虛擬化市場預測至2034年-按組件、技術、部署模式、網路功能類型、應用、最終用戶和地區分類的全球分析 虛擬擴展區域網路市場:按元件、運作模式、應用、部署模式、產業和組織規模分類-2026年至2032年全球預測

虛擬擴展區域網路市場:按元件、運作模式、應用、部署模式、產業和組織規模分類-2026年至2032年全球預測 2026年全球虛擬可擴展區域網路(VXLAN)市場報告

2026年全球虛擬可擴展區域網路(VXLAN)市場報告 網路虛擬化市場 - 2026-2031年預測

網路虛擬化市場 - 2026-2031年預測 虛擬可擴展區域網路 (VXLAN) 市場機會、成長促進因素、產業趨勢分析及 2025-2034 年預測

虛擬可擴展區域網路 (VXLAN) 市場機會、成長促進因素、產業趨勢分析及 2025-2034 年預測 全球虛擬可擴展區域網路 (VXLAN) 市場

全球虛擬可擴展區域網路 (VXLAN) 市場 虛擬擴展 LAN(VXLAN)市場:成長、未來前景、競爭分析,2024-2032年

虛擬擴展 LAN(VXLAN)市場:成長、未來前景、競爭分析,2024-2032年 全球虛擬可擴展 LAN (VXLAN) 市場:按產品、按應用、按行業、按地區 - 預測至 2029 年

全球虛擬可擴展 LAN (VXLAN) 市場:按產品、按應用、按行業、按地區 - 預測至 2029 年