|

市場調查報告書

商品編碼

1871274

虛擬可擴展區域網路 (VXLAN) 市場機會、成長促進因素、產業趨勢分析及 2025-2034 年預測Virtual Extensible LAN (VXLAN) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

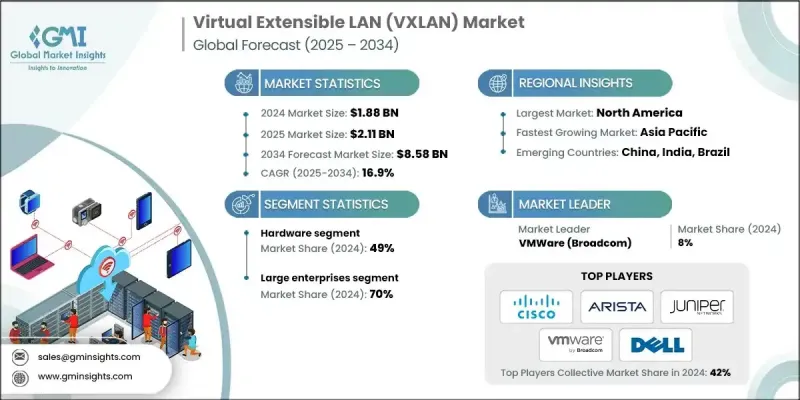

2024 年全球虛擬可擴展區域網路 (VXLAN) 市值為 18.8 億美元,預計到 2034 年將以 16.9% 的複合年成長率成長至 85.8 億美元。

VXLAN 技術正在變革企業和資料中心網路,它實現了跨越二層和三層邊界的可擴展、靈活且高效的網路虛擬化。 VXLAN 透過將二層服務擴展到三層網路來增強敏捷性,從而確保雲端環境中更佳的工作負載遷移和多租戶能力。隨著企業不斷將工作負載遷移到雲端平台,對能夠提供更高可擴展性、安全性和靈活性的虛擬化疊加網路的需求正在加速成長。網路基礎設施供應商正在開發強大的 VXLAN 生態系統,並將其與 SDN 控制器、自動化工具和編排框架整合,以最佳化部署效率。超大規模資料中心和雲端運算的興起推動了 VXLAN 協定的應用,以支援動態、可編程的網路,從而管理高流量的東西向網路並促進虛擬機器遷移。 VXLAN 疊加網路實現了分散式設施之間的無縫互連,提供了彈性擴展和工作負載遷移能力,這是建構彈性企業和雲端原生架構的核心要求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 18.8億美元 |

| 預測值 | 85.8億美元 |

| 複合年成長率 | 16.9% |

2024年,硬體領域佔據49%的市場佔有率,這主要得益於對相容VXLAN封裝和疊加技術的交換器、路由器和閘道器等實體網路元件日益成長的需求。隨著企業和大型資料中心優先考慮能夠管理內部流量和混合雲端環境的高性能硬體,對支援VXLAN的交換器、路由器和網卡的需求持續成長。高速交換技術的創新以及與基於SDN的網路管理系統更緊密的整合也推動了該領域的成長。

由於雲端運算、軟體定義網路 (SDN) 和網路虛擬化技術的廣泛部署,大型企業預計在 2024 年將佔據 70% 的市場佔有率。這些企業利用 VXLAN 疊加網路連接本地和多雲端基礎設施,從而確保全球資料中心之間統一的安全策略、簡化的工作負載遷移和集中式網路管理。在 VXLAN 框架中採用人工智慧驅動的自動化技術,進一步幫助企業提高營運效率並最佳化大規模分散式系統的管理。

美國虛擬可擴展區域網路 (VXLAN) 市場佔據 90.5% 的市場佔有率,預計到 2024 年將創造 6.323 億美元的市場規模。這一主導地位源自於美國對軟體定義網路 (SDN) 的早期採用、雲端優先戰略以及超大規模資料中心和企業的大規模部署。美國受益於其先進的 IT 生態系統、高雲滲透率以及 VXLAN 與 SDN、NFV 和多雲編排平台的整合,這些優勢能夠實現安全、可擴展和自動化的網路虛擬化。

全球虛擬可擴展區域網路 (VXLAN) 市場的主要參與者包括思科系統、瞻博網路、Arista Networks、VMware(博通)、惠普企業 (HPE) / Aruba Networks、華為技術有限公司、Cumulus Networks(英偉達公司)、戴爾科技和 Extreme Networks。領先企業在虛擬可擴展區域網路 (VXLAN) 市場採取的關鍵策略包括:擴展軟體定義網路產品組合、投資高速 VXLAN 相容硬體以及與雲端服務供應商建立合作夥伴關係以增強互通性。各公司也利用人工智慧和自動化技術進行動態網路編排、最佳化延遲並提高可擴展性。持續的研發投入、開放的網路計畫以及對軟體驅動型網路解決方案供應商的收購,使各公司能夠增強產品組合、提高市場滲透率並滿足不斷變化的企業連接需求。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 快速的雲端和資料中心擴張

- 軟體定義網路 (SDN) 的日益普及

- 對網路分段和安全的需求日益成長

- 提高虛擬機器移動性

- 產業陷阱與挑戰

- 複雜的部署與配置

- 不同供應商之間的互通性挑戰

- 市場機遇

- 邊緣與 5G 網路虛擬化

- 人工智慧驅動的網路自動化

- 雲端原生和容器網路

- 新興資料中心市場的擴張

- 成長促進因素

- 成長潛力分析

- 監管環境

- 全球的

- IETF 標準制定與 RFC 演進

- IEEE網路標準及互通性

- NIST網路安全框架與指南

- 開源授權和知識產權

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 全球的

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 下一代 VXLAN 增強功能和標準演進

- 與意圖式網路(IBN)整合

- 人工智慧/機器學習驅動的網路自動化與最佳化

- 邊緣運算與5G網路切片整合

- 新興技術

- 容器網路與 Kubernetes 整合

- 安全性增強與零信任架構

- 效能最佳化和硬體加速

- 多雲和混合雲端網路演進

- 技術採納障礙及緩解策略

- 當前技術趨勢

- 價格趨勢

- 硬體定價趨勢及成本最佳化

- 軟體授權模式演進(永久授權與訂閱授權)

- 專業服務定價及市場價格

- 基於雲端和SaaS的定價模式

- 總擁有成本 (TCO) 分析

- 各廠商的性價比基準測試

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 投資與融資分析

- 創投與私募股權投資趨勢

- 政府資金和基礎設施投資計劃

- 研發投資重點及技術發展

- 市場成熟度評估

- 客戶需求與供應商能力差距分析

- 企業需求評估及未滿足的需求

- 服務提供者的需求與現有服務

- 中小企業市場進入及簡化方面的差距

- 效能與可擴展性預期不符

- 供應商差距縮小策略及路線圖

- 產品開發和功能增強計劃

- 合作夥伴關係和生態系統拓展計劃

- 培訓和認證項目投資

- 開源貢獻與社區建設

- 市場案例研究及實施分析

- 大型企業 VXLAN 部署案例研究

- 雲端服務提供者實施範例

- 政府與國防部署成功案例

- 中小企業採用模式及經驗教訓

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 產品組合分析與差異化策略

- 供應商選擇標準與客戶決策因素

- 通路夥伴及經銷網路分析

- 顧客滿意度與品牌認知分析

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 硬體

- 開關

- 路由器

- 閘道

- 其他

- 軟體

- 支援VXLAN的網路作業系統

- 網路虛擬化軟體

- 網路管理與編排軟體

- 其他

- 服務

- 專業服務

- 諮詢

- 部署與整合

- 支援與維護

- 託管服務

- 專業服務

第6章:市場估算與預測:依企業規模分類,2021-2034年

- 主要趨勢

- 大型企業

- 中小企業

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 多租戶

- 工作負荷流動性

- 軟體定義網路(SDN)疊加層

- 網路功能虛擬化(NFV)

- 災後復原

- 其他

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 製造業

- 衛生保健

- 金融服務業

- 零售

- 媒體與娛樂

- 政府

- 資訊科技與電信

- 其他

第9章:市場估算與預測:依部署模式分類,2021-2034年

- 主要趨勢

- 現場

- 基於雲端的

- 混合

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 俄羅斯

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Global companies

- Arista Networks

- Cisco Systems

- Cumulus Networks (NVIDIA Corporation)

- Hewlett Packard Enterprise (HPE)

- Huawei Technologies

- Juniper Networks

- VMware (Broadcom)

- Hardware Infrastructure Leaders

- Dell Technologies

- Foxconn Technology Group

- Inspur Group

- Lenovo Group

- Quanta Computer

- Supermicro Computer

- Emerging & Disruptive Players

- Forward Networks

- Fungible Inc. (Microsoft)

- Kaloom Inc.

- Netris AI

- Pensando Systems (AMD)

- Veriflow Systems

- 區域性和小眾玩家

- Allied Telesis

- D-Link Corporation

- Extreme Networks

- Netgear

- TP-Link Technologies

- Ubiquiti

The Global Virtual Extensible LAN (VXLAN) Market was valued at USD 1.88 billion in 2024 and is estimated to grow at a CAGR of 16.9% to reach USD 8.58 billion by 2034.

VXLAN technology is transforming enterprise and data center networking by enabling scalable, flexible, and efficient network virtualization across Layer 2 and Layer 3 boundaries. It enhances agility by extending Layer 2 services over Layer 3 networks, ensuring better workload mobility and multi-tenancy in cloud environments. As enterprises continue migrating workloads to cloud platforms, the demand for virtualized overlay networks offering greater scalability, security, and flexibility is accelerating. Network infrastructure providers are developing robust VXLAN ecosystems integrated with SDN controllers, automation tools, and orchestration frameworks to optimize deployment efficiency. The rise of hyperscale data centers and cloud computing fuels the use of VXLAN protocols to support dynamic, programmable networks that manage heavy east-west traffic and facilitate virtual machine mobility. VXLAN overlays enable seamless interconnection between distributed facilities, providing elastic scalability and workload migration, core requirements for resilient enterprise and cloud-native architecture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.88 Billion |

| Forecast Value | $8.58 Billion |

| CAGR | 16.9% |

The hardware segment held a 49% share in 2024, driven by the rising need for physical network components such as switches, routers, and gateways compatible with VXLAN encapsulation and overlay technologies. Demand for VXLAN-enabled switches, routers, and network interface cards continues to grow as enterprises and large-scale data centers prioritize high-performance hardware capable of managing internal traffic and hybrid cloud environments. The segment's growth is being supported by innovations in high-speed switching and stronger integration with SDN-based network management systems.

The large enterprises segment held a 70% share in 2024, owing to the widespread deployment of cloud computing, SDN, and network virtualization technologies. These organizations use VXLAN overlays to connect on-premises and multi-cloud infrastructures, ensuring uniform security policies, streamlined workload migration, and centralized network management across global data centers. The adoption of AI-powered automation within VXLAN frameworks is further helping enterprises improve operational efficiency and optimize management of large-scale distributed systems.

U.S. Virtual Extensible LAN (VXLAN) Market accounted for a 90.5% share, generating USD 632.3 million in 2024. This dominance stems from early adoption of SDN, cloud-first strategies, and large-scale deployments by hyperscale data centers and enterprises. The U.S. benefits from an advanced IT ecosystem, high cloud penetration, and the integration of VXLAN with SDN, NFV, and multi-cloud orchestration platforms that enable secure, scalable, and automated network virtualization.

Major players in the Global Virtual Extensible LAN (VXLAN) Market include Cisco Systems, Juniper Networks, Arista Networks, VMware (Broadcom), Hewlett Packard Enterprise (HPE) / Aruba Networks, Huawei Technologies Co., Cumulus Networks (NVIDIA Corporation), Dell Technologies, and Extreme Networks. Key strategies adopted by leading companies in the Virtual Extensible LAN (VXLAN) Market include expanding software-defined networking portfolios, investing in high-speed, VXLAN-compatible hardware, and forming partnerships with cloud service providers to enhance interoperability. Firms are also leveraging AI and automation for dynamic network orchestration, optimizing latency, and improving scalability. Continuous R&D efforts, open networking initiatives, and acquisitions of software-driven network solution providers are enabling companies to enhance product portfolios, increase market penetration, and meet evolving enterprise connectivity demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021-2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Enterprise size

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Deployment model

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid cloud and data center expansion

- 3.2.1.2 Rising adoption of software-defined networking (SDN)

- 3.2.1.3 Growing need for network segmentation and security

- 3.2.1.4 Increased virtual machine mobility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex deployment and configuration

- 3.2.2.2 Interoperability challenges across vendors

- 3.2.3 Market opportunities

- 3.2.3.1 Edge and 5g network virtualization

- 3.2.3.2 AI-driven network automation

- 3.2.3.3 Cloud-native and container networking

- 3.2.3.4 Expansion in emerging data center markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global

- 3.4.1.1 IETF standards development & RFC evolution

- 3.4.1.2 IEEE networking standards & interoperability

- 3.4.1.3 NIST cybersecurity framework & guidelines

- 3.4.1.4 Open source licensing & intellectual property

- 3.4.2 North America

- 3.4.3 Europe

- 3.4.4 Asia Pacific

- 3.4.5 Latin America

- 3.4.6 Middle East & Africa

- 3.4.1 Global

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Next-generation VXLAN enhancements & standards evolution

- 3.7.1.2 Integration with intent-based networking (IBN)

- 3.7.1.3 AI/ML-driven network automation & optimization

- 3.7.1.4 Edge computing & 5G network slicing integration

- 3.7.2 Emerging technologies

- 3.7.2.1 Container networking & kubernetes integration

- 3.7.2.2 Security enhancement & zero trust architecture

- 3.7.2.3 Performance optimization & hardware acceleration

- 3.7.2.4 Multi-cloud & hybrid cloud networking evolution

- 3.7.3 Technology adoption barriers & mitigation strategies

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 Hardware pricing trends & cost optimization

- 3.8.2 Software licensing model evolution (perpetual vs subscription)

- 3.8.3 Professional services pricing & market rates

- 3.8.4 Cloud-based & saas pricing models

- 3.8.5 Total cost of ownership (TCO) analysis

- 3.8.6 Price-performance benchmarking across vendors

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Investment & funding analysis

- 3.13.1 Venture Capital & Private Equity Investment Trends

- 3.13.2 Government Funding & Infrastructure Investment Programs

- 3.13.3 R&D Investment Priorities & Technology Development

- 3.14 Market maturity assessment

- 3.15 Customer needs vs vendor capability gap analysis

- 3.15.1 Enterprise requirements assessment & unmet needs

- 3.15.2 Service provider demands vs current offerings

- 3.15.3 SME market accessibility & simplification gaps

- 3.15.4 Performance & scalability expectation misalignment

- 3.16 Vendor gap reduction strategies & roadmaps

- 3.16.1 Product development & feature enhancement plans

- 3.16.2 Partnership & ecosystem expansion initiatives

- 3.16.3 Training & certification program investments

- 3.16.4 Open source contribution & community building

- 3.17 Market case studies & implementation analysis

- 3.17.1 Large enterprise VXLAN deployment case studies

- 3.17.2 Cloud service provider implementation examples

- 3.17.3 Government & defense deployment success stories

- 3.17.4 SME adoption patterns & lessons learned

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product portfolio analysis & differentiation strategies

- 4.8 Vendor selection criteria & customer decision factors

- 4.9 Channel partner & distribution network analysis

- 4.10 Customer satisfaction & brand perception analysis

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Switches

- 5.2.2 Routers

- 5.2.3 Gateways

- 5.2.4 Others

- 5.3 Software

- 5.3.1 VXLAN enabled network operating system

- 5.3.2 Network virtualization software

- 5.3.3 Network management and orchestration software

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional services

- 5.4.1.1 Consulting

- 5.4.1.2 Deployment & integration

- 5.4.1.3 Support & maintenance

- 5.4.2 Managed services

- 5.4.1 Professional services

Chapter 6 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Large enterprises

- 6.3 SME

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Multi-tenancy

- 7.3 Workload mobility

- 7.4 Software-defined networking (SDN) overlays

- 7.5 Network function virtualization (NFV)

- 7.6 Disaster recovery

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Manufacturing

- 8.3 Healthcare

- 8.4 BFSI

- 8.5 Retail

- 8.6 Media & entertainment

- 8.7 Government

- 8.8 IT & telecommunications

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 On-premises

- 9.3 Cloud-based

- 9.4 Hybrid

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Arista Networks

- 11.1.2 Cisco Systems

- 11.1.3 Cumulus Networks (NVIDIA Corporation)

- 11.1.4 Hewlett Packard Enterprise (HPE)

- 11.1.5 Huawei Technologies

- 11.1.6 Juniper Networks

- 11.1.7 VMware (Broadcom)

- 11.2 Hardware Infrastructure Leaders

- 11.2.1 Dell Technologies

- 11.2.2 Foxconn Technology Group

- 11.2.3 Inspur Group

- 11.2.4 Lenovo Group

- 11.2.5 Quanta Computer

- 11.2.6 Supermicro Computer

- 11.3 Emerging & Disruptive Players

- 11.3.1 Forward Networks

- 11.3.2 Fungible Inc. (Microsoft)

- 11.3.3 Kaloom Inc.

- 11.3.4 Netris AI

- 11.3.5 Pensando Systems (AMD)

- 11.3.6 Veriflow Systems

- 11.4 Regional & Niche Players

- 11.4.1 Allied Telesis

- 11.4.2 D-Link Corporation

- 11.4.3 Extreme Networks

- 11.4.4 Netgear

- 11.4.5 TP-Link Technologies

- 11.4.6 Ubiquiti