|

市場調查報告書

商品編碼

2043987

南美金融科技:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

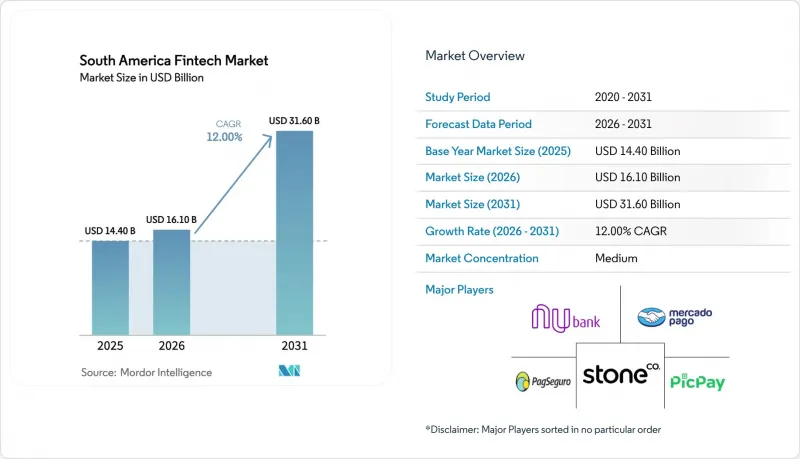

預計南美金融科技市場規模將從 2025 年的 144 億美元成長到 2026 年的 161 億美元,然後在 2031 年達到 316 億美元,2026 年至 2031 年的複合年成長率為 12%。

儘管數位支付以 45.0% 的市場佔有率佔據主導地位,消費信貸和中小企業貸款也在持續擴張,但數位貸款預計將以 21.3% 的複合年成長率 (CAGR) 實現最快成長。到 2025 年,個人用戶將佔 68.6% 的使用率,行動應用程式將佔介面互動的 74.7%,這凸顯了以行動端為中心的新客戶獲取和互動管道的建立。短期內仍存在一些不利因素,尤其是在巴西和阿根廷,互換費上限、利率上升和外匯管制正在對費率和結算盈利構成壓力。隨著新興銀行和嵌入式金融平台交叉銷售信貸、保險和投資產品,競爭日益激烈。 Nubank 在該地區擁有 1.27 億客戶,Mercado Pago在全部區域擁有 7,200 萬月有效用戶。

南美洲金融科技市場趨勢與分析

RTP的擴展和增強正在推動交易量的成長。

即時支付如今已成為整個南美金融科技市場交易成長的基石,其中巴西的Pix處於領先地位。 Pix在幾乎整個地區的成年人中廣泛普及,2024年交易量達到634億筆。 Pix全天候可用且支付處理速度快,使其註冊用戶數量在2024年底激增至1.63億。同時,「Pix Automatico」和非接觸式輕觸支付等新功能拓展了其在訂閱和銷售點(POS)支付方面的應用場景。秘魯以Yape和PLIN為核心的互通支付基礎設施正在推動都市區零售和微型電商商家採用即時支付。連結Pix與鄰近市場的早期跨境試點計畫正在縮短結算時間,並縮小整個南美金融科技市場匯款和電子商務領域的外匯價差。大規模的生態系統正在推動平台普及,Mercado Pago 為 7,200 萬月有效用戶提供即時轉帳服務,而 StoneCo 則報告稱,2025 年初其面向微企業(MSME) 客戶的 Pix 交易量同比成長 95%。監管政策的明確化也為業務擴張提供了支持。這包括巴西的互通性要求、智利和哥倫比亞計劃於 2026 年年中推出的即時支付舉措,以及為應對日益增多的應用程式詐騙舉報而加強的 KYC(了解您的客戶)和生物識別驗證。

開放金融資料可攜性為信貸和諮詢服務打開了大門。

巴西的開放金融系統已獲得超過4,300萬有效用戶的授權,每週處理超過15億次API調用,使其成為全球交易量最大的舉措之一。根據巴西央行指令,符合資格的金融機構必須共用交易、信貸和投資領域的數據,使第三方能夠利用檢驗的帳戶資訊和薪資資料流來評估無擔保貸款、薪資關聯貸款和擔保貸款的利率。 Nubank的擔保貸款組合在2025年年增133%,這主要歸功於透過基於授權的收入和帳戶資料存取方式,提高了信貸評估和催收效率。智利金融市場委員會(CMF)於2024年7月發布了第514號通用規則,強制要求在2026年7月前實施標準化API。哥倫比亞也於2025年6月發布了一項法令草案,將適用範圍從銀行業擴展到保險和退休金產業。阿根廷2025年第353號行政法令正式建立了一個開放金融體系,該體系在阿根廷中央銀行(BCRA)的監管下,採用基於用戶同意的數據共用機制,進一步降低了南美金融科技市場提供多產品金融諮詢的門檻。儘管這一發展勢頭持續,但資料欄位標準的差異以及仍在發展中的跨境互通性,增加了小規模服務提供者的整合成本和複雜性。

高昂的客戶獲取成本和較低的金融素養:成長的結構性障礙

高昂的客戶獲取成本,加上南美洲多個市場普遍存在的金融素養低問題,持續限制金融科技的擴充性。儘管數位化進程飛速發展,但客戶註冊仍需要大量的行銷投入、離線身分驗證以及以教育為導向的互動。這推高了平均客戶獲取成本 (CAC),並降低了客戶終身價值 (LTV),尤其是在銀行服務匱乏的地區和農村地區。這項挑戰具有結構性和長期性,迫使金融科技公司加強對金融教育、代理商支持的註冊流程以及數據主導的個人化服務的投資,以提高轉換率和客戶維繫。

細分市場分析

2025年,數位支付在南美金融科技市佔率中佔比達到45.1%。這得益於巴西的Pix和阿根廷的Transferencias 3.0等支付基礎設施的建設,這些基礎設施降低了消費者和商家的支付成本。在該領域,數位借貸預計將在2026年至2031年間以21.3%的複合年成長率成長,隨著信用評估範圍透過開放金融數據和嵌入式信貸管道擴展到信用記錄有限的人群,南美金融科技市場的加速發展尤為顯著。目前,貸款機構正在將經授權的銀行數據與市場和物流歷史記錄相結合,以評估消費者和微企業借款人的還款行為,從而縮短核准時間,提高以往服務不足群體的核准率。 Nubank的擔保貸款組合在2025年年增133%。這主要歸功於貸款品質和回收率的提升,而這得益於對檢驗的工資存款和帳戶資金流的獲取。 Mercado Libre 的金融科技部門利用市場交易數據和交付接點來最佳化循環信貸餘額、違約率和定價,使其信貸發行量在 2025 年第三季擴大到 110 億美元。

投資和保險相關行業的強勁勢頭正推動面向個人和微企業用戶的更全面的提案。 Mercado Pago 的資產管理規模在 2025 年第三季同比成長一倍,達到 151 億美元,這得益於其將具有吸引力的基準掛鉤收益率的貨幣市場產品整合到日常錢包體驗中。新興銀行和付款管道正透過推出針對中小企業的定向保險產品,並將保險選項整合到註冊和結帳流程中,逐步提高其附加率。隨著服務提供者進軍大規模貸款業務,與資料保護和反洗錢 (AML) 相關的合規標準正在增加固定成本,這有利於那些擁有強大管治和資本的企業,並加速了南美金融科技市場的整合。總體而言,南美金融科技業正持續從單一支付服務向多元化金融服務轉型,以信貸主導的貨幣化將推動下一階段的成長,因為基於用戶同意的數據支持信用評估和債務催收。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- RTP 擴充性和功能

- 開放金融資料可攜性

- 平台上的嵌入式金融

- 實施軟體POS系統和低成本支付解決方案。

- 透過金融科技實現與美元掛鉤的儲蓄

- 代幣化存款和央行數位貨幣

- 市場限制因素

- 高客戶獲取成本和低金融素養

- 佣金上限導致收入壓力

- 即時支付中的應用程式詐騙

- 外匯管制、結算摩擦

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 即時支付基礎設施的現狀

- 目前QR碼互通性的現狀

- 現金流入/流出 (CICO) 和代理網路覆蓋範圍

- 波特五力分析

- 新參與企業的威脅

- 買方的議價能力

- 供應商議價能力

- 替代品的威脅

- 競爭公司之間的競爭關係

第5章:預測市場規模與成長率

- 按服務

- 數位支付

- 數位借貸和金融

- 數位投資

- 保險科技

- 新銀行

- 最終用戶

- 零售

- 公司

- 透過使用者介面

- 行動應用

- 網頁/瀏覽器

- POS/物聯網設備

- 按地區

- 巴西

- 秘魯

- 智利

- 阿根廷

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nubank(Nu Holdings)

- Mercado Pago(Mercado Libre)

- PagSeguro(PagBank)

- StoneCo

- PicPay

- Inter&Co(Banco Inter)

- EBANX

- dLocal

- Uala

- C6 Bank

- Creditas

- Neon

- XP Inc.

- BTG Pactual(digital platforms)

- Getnet Brasil(Santander)

- Prisma Medios de Pago(阿根廷)

- 納蘭哈十號(阿根廷)

- 布魯班克(阿根廷)

- MACH(Banco de Chile)

- 奇普(智利)

- FPay(Falabella)

- Transbank(智利)

- 亞佩(秘魯)

- 普林(秘魯)

- RecargaPay(巴西)

- SumUp(巴西)

- 碼頭(巴西)

- 皮斯莫(巴西)

第7章 市場機會與未來展望

The South America Fintech Market size is expected to grow from USD 14.40 billion in 2025 to USD 16.10 billion in 2026 and is forecast to reach USD 31.60 billion by 2031 at 12% CAGR over 2026-2031.

Digital payments led activity with a 45.0% share, while digital lending is set to expand at the fastest pace, with a 21.3% CAGR, as consumer credit and SME financing continue to scale. Retail users drove 68.6% of usage in 2025, and mobile applications accounted for 74.7% of interface interactions, underscoring a mobile-centric pathway for onboarding and engagement. Short-term headwinds persist from interchange caps, elevated interest rates, and FX controls that compress take rates and settlement economics, particularly in Brazil and Argentina. Competitive intensity is high as neobanks and embedded-finance platforms cross-sell credit, insurance, and investment products, illustrated by Nubank's 127 million customers and Mercado Pago's 72 million monthly active users across the region.

South America Fintech Market Trends and Insights

RTP Scale-Up and Features Propel Volume Growth

Real-time payments now anchor transaction growth across the South America fintech market, led by Brazil's Pix, which handled 63.4 billion transactions in 2024 as adoption approaches ubiquity among adults. Pix's 24/7 availability and rapid settlement underpinned a surge to 163 million registered users by late 2024, while new features such as Pix Automatico and contactless tap-to-pay expanded use cases for subscriptions and point-of-sale payments. Peru's interoperable rails, anchored by Yape and PLIN, support merchant acceptance in urban retail and micro-commerce. Early cross-border pilots linking Pix with neighboring markets are shortening settlement windows and reducing FX spreads for remittance and e-commerce corridors in the South America fintech market. Platform adoption has been reinforced by large ecosystems, with Mercado Pago enabling instant disbursements to its 72 million monthly active users and StoneCo reporting a 95% year-over-year increase in Pix transactions among MSMB clients in early 2025. Regulatory clarity supports scale, including Brazil's interoperability mandates and ongoing instant payment initiatives in Chile and Colombia for mid-2026 timelines, as well as enhanced KYC and biometric checks in response to elevated APP fraud reports.

Open Finance Data Portability Unlocks Credit and Advisory

Brazil's open finance system records more than 43 million active user consents and processes over 1.5 billion API calls weekly, placing it among the largest initiatives globally by transaction volume. Central bank directives require data sharing across transactional, credit, and investment domains for qualifying institutions, enabling third parties to price unsecured, payroll-linked, and secured credit using verified account and salary flows. Nubank's secured-lending portfolio rose 133% year over year in 2025, assisted by consented access to income and account data that tightened underwriting and collection performance. Chile's CMF issued General Rule No. 514 in July 2024 to require standardized APIs by July 2026, and Colombia published a draft decree in June 2025 to extend coverage beyond banking into insurance and pensions. Argentina's Executive Decree No. 353 of 2025 formalized an open finance system with BCRA oversight and consent-based data sharing, further lowering barriers to multi-product financial advice in the South America fintech market. Despite momentum, differing data field standards and nascent cross-border interoperability raise integration costs and complexity for smaller providers.

High Customer Acquisition Costs and Low Financial Literacy as Structural Growth Barriers

High customer acquisition costs, coupled with persistently low financial literacy across several South American markets, continue to constrain fintech scalability. Despite rapid digital adoption, consumer onboarding still requires significant marketing spend, offline verification, and education-driven engagement. This raises blended CAC and depresses lifetime value economics, particularly in underbanked and rural segments. The challenge is structural and long-duration, pushing fintechs to invest in financial education, agent-assisted onboarding, and data-led personalization to improve conversion and retention.

Other drivers and restraints analyzed in the detailed report include:

- Embedded Finance in E-Commerce and Super Apps

- Dollar-Linked Savings and Stablecoin Adoption

- FX Controls, Settlement Frictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital payments captured 45.1% of the South American fintech market share in 2025, underpinned by rails such as Brazil's Pix and Argentina's Transferencias 3.0, which have lowered acceptance costs for consumers and merchants. Within the segment mix, digital lending is forecast to expand at a 21.3% CAGR between 2026 and 2031, highlighting acceleration in the South American fintech market as thin-file underwriting scales through open-finance data and embedded-credit channels. Lenders now combine consented bank data with marketplace and logistics histories to assess repayment behaviour for consumer and MSMB borrowers, compressing approval times while lifting acceptance rates for previously underserved cohorts. Nubank's secured-lending portfolio grew 133% year over year in 2025, aided by access to verified salary deposits and account flows that strengthened origination quality and collections. Mercado Libre's fintech arm scaled credit issuance to USD 11 billion by Q3 2025, using marketplace transaction data and delivery touchpoints to calibrate revolving balances, delinquency, and pricing.

Momentum in investment and insurance adjacencies has supported a more complete proposition for retail and MSMB users. Mercado Pago's assets under management doubled year over year to USD 15.1 billion in Q3 2025 as money-market products were bundled into daily-wallet experiences with attractive benchmark-linked yields. Neobanks and payments platforms have introduced targeted protection products for small businesses, embedding coverage options into onboarding and checkout flows to increase attach rates over time. As providers expand into lending at scale, compliance standards linked to data protection and AML have increased fixed costs and favoured players with robust governance and capital, reinforcing consolidation dynamics in the South American fintech market. On balance, the South America fintech industry continues to shift from single-product payments toward multi-product financial services, with credit-led monetization driving the next leg of growth, where consented data support underwriting and collections.

The South America Fintech Market Report is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, Neobanking), End-User (Retail, Businesses), User Interface (Mobile Applications, Web/Browser, POS/IoT Devices), and Geography (Brazil, Peru, Chile, Argentina, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nubank (Nu Holdings)

- Mercado Pago (Mercado Libre)

- PagSeguro (PagBank)

- StoneCo

- PicPay

- Inter&Co (Banco Inter)

- EBANX

- dLocal

- Uala

- C6 Bank

- Creditas

- Neon

- XP Inc.

- BTG Pactual (digital platforms)

- Getnet Brasil (Santander)

- Prisma Medios de Pago (Argentina)

- Naranja X (Argentina)

- Brubank (Argentina)

- MACH (Banco de Chile)

- Khipu (Chile)

- FPay (Falabella)

- Transbank (Chile)

- Yape (Peru)

- Plin (Peru)

- RecargaPay (Brazil)

- SumUp (Brazil)

- Dock (Brazil)

- Pismo (Brazil)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RTP scale-up and features

- 4.2.2 Open finance data portability

- 4.2.3 Embedded finance in platforms

- 4.2.4 SoftPOS and low-cost acceptance

- 4.2.5 Dollar-linked savings via fintech

- 4.2.6 Tokenized deposits and CBDC

- 4.3 Market Restraints

- 4.3.1 High Customer Acquisition Costs and Low Financial Literacy

- 4.3.2 Fee caps squeeze economics

- 4.3.3 APP fraud on instant rails

- 4.3.4 FX controls, settlement frictions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Real-time payments infrastructure status

- 4.8 Merchant acceptance & QR interoperability landscape

- 4.9 Cash-in/Cash-out (CICO) and agent network coverage

- 4.10 Porter's Five Forces Analysis

- 4.10.1 Threat of New Entrants

- 4.10.2 Bargaining Power of Suppliers

- 4.10.3 Bargaining Power of Buyers

- 4.10.4 Threat of Substitutes

- 4.10.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Peru

- 5.4.3 Chile

- 5.4.4 Argentina

- 5.4.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Nubank (Nu Holdings)

- 6.4.2 Mercado Pago (Mercado Libre)

- 6.4.3 PagSeguro (PagBank)

- 6.4.4 StoneCo

- 6.4.5 PicPay

- 6.4.6 Inter&Co (Banco Inter)

- 6.4.7 EBANX

- 6.4.8 dLocal

- 6.4.9 Uala

- 6.4.10 C6 Bank

- 6.4.11 Creditas

- 6.4.12 Neon

- 6.4.13 XP Inc.

- 6.4.14 BTG Pactual (digital platforms)

- 6.4.15 Getnet Brasil (Santander)

- 6.4.16 Prisma Medios de Pago (Argentina)

- 6.4.17 Naranja X (Argentina)

- 6.4.18 Brubank (Argentina)

- 6.4.19 MACH (Banco de Chile)

- 6.4.20 Khipu (Chile)

- 6.4.21 FPay (Falabella)

- 6.4.22 Transbank (Chile)

- 6.4.23 Yape (Peru)

- 6.4.24 Plin (Peru)

- 6.4.25 RecargaPay (Brazil)

- 6.4.26 SumUp (Brazil)

- 6.4.27 Dock (Brazil)

- 6.4.28 Pismo (Brazil)

7 Market Opportunities & Future Outlook

- 7.1 Cross-border instant-payment corridors (e.g., Pix-enabled international flows and merchant-of-record use cases)

- 7.2 SME embedded finance for B2B trade (real-time FX, invoice financing, supply-chain payments)

金融科技市場:2026-2032年全球市場預測(以支付方式、技術、最終用戶、應用、部署模式和組織規模分類)

金融科技市場:2026-2032年全球市場預測(以支付方式、技術、最終用戶、應用、部署模式和組織規模分類) 汽車金融科技市場規模、佔有率和成長分析:按服務類型、技術、最終用戶、分銷管道和地區分類-2026-2033年產業預測

汽車金融科技市場規模、佔有率和成長分析:按服務類型、技術、最終用戶、分銷管道和地區分類-2026-2033年產業預測 中國金融科技:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中國金融科技:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 替代投資技術市場預測至2034年-按解決方案、部署模式、投資類型、應用、最終用戶和地區分類的全球分析

替代投資技術市場預測至2034年-按解決方案、部署模式、投資類型、應用、最終用戶和地區分類的全球分析 重塑金融科技2.0的未來汽車金融科技市場預測至2034年:按車輛類型、驅動方式、銷售管道、最終用戶和地區分類的全球分析

重塑金融科技2.0的未來汽車金融科技市場預測至2034年:按車輛類型、驅動方式、銷售管道、最終用戶和地區分類的全球分析 伊斯蘭金融科技市場規模、佔有率和趨勢分析報告:按類型、部署模式、最終用途、地區和細分市場預測(2026-2033 年)全球金融科技市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

伊斯蘭金融科技市場規模、佔有率和趨勢分析報告:按類型、部署模式、最終用途、地區和細分市場預測(2026-2033 年)全球金融科技市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 金融科技市場商業分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案

金融科技市場商業分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案 2026年金融科技多重雲端全球市場報告

2026年金融科技多重雲端全球市場報告