|

市場調查報告書

商品編碼

2073494

中國金融科技:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

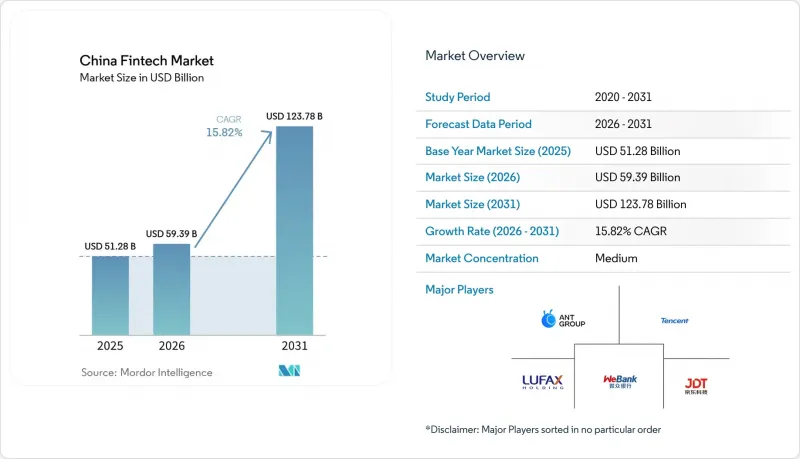

根據 Mordor Intelligence 的數據顯示,2025 年中國金融科技市場價值 512.8 億美元,預計到 2031 年將達到 1237.8 億美元,而 2026 年為 593.9 億美元,預測期(2026-2031 年)的複合年成長率為 15.82%。

本報告按服務類型(數位支付、數位借貸和資金籌措、數位投資、保險科技、新型銀行)、最終用戶(個人、企業)和用戶介面(行動應用、網頁/瀏覽器、POS/物聯網設備)分類。市場預測以美元計價。

中國金融科技市場的趨勢與洞察

中國人民銀行推出電子人民幣,正加速二、三線城市數位支付的普及。

電子人民幣框架將於2026年1月1日過渡到計息存款機制,屆時錢包餘額將納入銀行負債和準備金計算,並對非銀行支付機構實施100%的準備金要求。這將把數位貨幣整合到標準的銀行監管框架中。截至2025年11月,電子人民幣累積交易量將達到34.8億筆,由數億個個人和企業錢包支持,這表明即使在2026年計息存款機制生效之前,電子人民幣也已奠定了堅實的基礎。然而,電子人民幣的廣泛應用仍面臨諸多挑戰,因為用戶仍然傾向於使用目前主導行動支付市場的第三方平台。因此,在未來兩到四年內,提供獎勵並強製商家採用電子人民幣將對彌合普及差距起到至關重要的作用。試點計畫已從最初的區域範圍擴展到數十個城市,其架構設計充分考慮了與商業銀行分銷網路的互通性。這項措施旨在推廣行動支付習慣尚未普及、服務覆蓋範圍較窄的地區,與一線城市相比,這些地區的行動支付服務普及程度較低。此舉將透過儲備機制加強政策溝通,在更接近銀行存款而非數位現金的模式下提升合規性,並透過標準化的錢包設計和商家受理指南促進中國金融科技市場的發展。

強制清算線上工會將促進第三方結算的交易量。

這個集中式支付清算系統處理全國範圍內的大量交易,展現了支持零售和服務業持續使用QR碼和應用內支付所需的技術能力。 2025年第三季度,網聯處理了3,196.7億筆交易,銀聯同期清算了1,000.1億筆銀行間交易。這在核心支付系統中建立了多層冗餘和強大的處理能力。支付整合消除了先前平台與數百家銀行直接連接模式造成的碎片化問題,提高了中央銀行的監管透明度,並簡化了反洗錢工作的風險管理。這些結構性優勢能夠幫助商家和消費者應對節日和大型購物節期間的交易量激增,並有效避免營運瓶頸。這項基礎設施的規模和穩定性為新的金融科技應用場景提供了穩定的基礎。同時,中國的金融科技市場正從支付領域擴展到貸款、保險和資產管理等領域,而這些領域都仰賴高度可靠的支付處理能力。

資料安全法:對SaaS金融科技公司跨境資料傳輸實施更嚴格的監管

中國跨境個人資料架構將於2026年1月1日最終確定。該框架將允許對超過一定數據量的數據採用認證機制,對許多非關鍵資訊基礎設施運營商(CIIO)實施標準契約,強制要求對超過閾值的數據進行安全評估,並為國際數據流動建立運行查核點。針對金融機構的特定行業規則強制要求在本地儲存和處理金融客戶訊息,從而將資料在地化確立為銀行和保險公司的基本義務。網路安全法的修訂提高了嚴重違規行為的最高罰款額度,並擴大了域外適用範圍,這加大了執法部門對危害國內網路安全的境外活動的打擊力度。事件報告措施要求CIIO和網路營運商提供快速通知,增加了事件偵測、優先排序和回應方面的管治負擔。這些要求提高了在中國營運或與中國開展業務的公司在工程、法律和營運團隊中建立合規架構的需求,並將影響整個中國金融科技市場的產品設計和供應商選擇。

細分市場分析

到2025年,數位支付將佔據最大佔有率,達到59.23%。這反映了QR碼支付和應用內支付在中國金融科技市場日常商業中的廣泛應用。集中清算依託於系統的處理能力,網聯在2025年第三季將處理3,196.7億筆交易,銀聯將處理1,000.1億筆交易,這為商戶的接受度和用戶信任提供了保障。由於整體「行動優先」的部署,交易速度仍保持高速。同時,從2026年起,電子人民幣(e-CNY)將透過銀行發行,作為公共選項,以規範錢包設計和準備金管理。憑藉大規模的線上用戶群和消費者熟悉度,私人平台的雙平台格局將繼續在零售支付領域佔據核心地位,從而促進用戶養成使用習慣。這些因素確保了數位支付在中國整個金融科技市場中保持其核心地位,為貸款、保險和資產管理等交叉銷售提供支援。

隨著純數位銀行利用數據和雲端原生核心系統在中國金融科技市場推動低成本營運規模化和人工智慧主導的決策,預計新銀行將迎來最快成長,到2031年複合年成長率將達到19.58%。微眾銀行的用戶基數及其向微型、小型和微企業(MSME)的拓展,展現了該模式的營運槓桿作用和規模化服務長尾客戶的能力,並支持其零售和中小企業業務手續費和利息收入的多元化。數位借貸模式持續受到以往P2P借貸模式衰落的影響,供應鏈金融和持牌消費金融與普惠銀行貸款一道,在彌合信貸缺口方面發揮著主導作用。資產管理平台受益於跨國試點計畫和產品標準化,降低了主導服務的客戶獲取門檻。這些趨勢共同推動了新銀行和數位投資的成長前景,儘管數位支付仍然是最大的收入來源。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國人民銀行推出電子人民幣,正加速二、三線城市數位支付的普及。

- 強制使用 NetsUnion 進行付款導致使用第三方支付系統的交易量增加。

- 中小企業的資金籌措缺口正在推動P2P和供應鏈金融科技借貸平台的成長。

- 財富管理互聯計畫正在促進智慧投顧的普及。

- 針對私人醫療保險的稅收優惠政策正在促進保險科技的發展。

- 股票型銀行對雲端原生核心系統的升級正在推動 BaaS/API 的使用量增加。

- 市場限制因素

- 資料安全法加強了對SaaS和金融科技公司跨境資料傳輸的監管。

- 小額信貸不良債務率的上升加重了維持資本充足率的負擔。

- 行動支付的飽和阻礙了交易量的進一步成長。

- 網路安全威脅與資料隱私問題

- 價值鏈分析

- 監管和技術展望

- 波特五力模型

- 投資和資金籌措分析

第5章 市場規模與成長預測

- 服務方案

- 數位支付

- 數字借貸和資金籌措

- 數位投資

- 保險科技

- 新銀行

- 最終用戶

- 零售

- 商業

- 透過使用者介面

- 行動應用

- 網頁/瀏覽器

- POS/物聯網設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ant Group(Alipay)

- Tencent Holdings(Tenpay)

- WeBank Co. Ltd.

- Lufax Holding Ltd.

- JD Technology(JD Digits)

- Ping An OneConnect Bank

- ZhongAn Online P&C Insurance

- Futu Holdings Ltd.

- Tiger Brokers(UP Fintech)

- 360 DigiTech Inc.

- LexinFintech Holdings Ltd.

- Qudian Inc.

- Xiaomi Finance

- Lakala Payment Corp.

- UnionPay Merchant Services

- LianLian DigiTech

- Huize Holding Ltd.

- Du Xiaoman Financial

- Suning Finance

- Wanda Fintech Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the china fintech market size was valued at USD 51.28 billion in 2025 and is estimated to grow from USD 59.39 billion in 2026 to reach USD 123.78 billion by 2031, at a CAGR of 15.82% during the forecast period (2026-2031).

This report is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, Neobanking), End-User (Retail, Businesses), and User Interface (Mobile Applications, Web/Browser, POS/IoT Devices). The Market Forecasts are Provided in Terms of Value (USD).

China Fintech Market Trends and Insights

PBOC e-CNY Roll-out Accelerating Digital Payments Adoption Across Tier-2/3 Cities

The e-CNY framework shifted to interest-bearing deposit money effective January 1, 2026, folding wallet balances into bank liabilities and reserve calculations, and aligning non-bank payment institutions with 100% reserve requirements, which integrates digital currency into standard banking oversight. By November 2025, cumulative e-CNY transactions reached 3.48 billion, supported by hundreds of millions of personal and corporate wallets, indicating foundational scale before the deposit-bearing pivot takes effect in 2026. The adoption challenge remains material because users still favour incumbent third-party platforms that dominate mobile payments, which makes incentives and merchant acceptance mandates decisive for closing the usage gap over the next two to four years. Pilot coverage has expanded from initial sites to dozens of cities, and the architecture is designed for interoperability with commercial bank distribution, which targets underserved regions where mobile payment habits are less entrenched than in tier-1 hubs. The shift supports policy transmission through reserve mechanics and enhances compliance under a model that sits closer to bank deposits than to digital cash, while bolstering the Chinese fintech market with standardized wallet design and merchant acceptance guardrails.

NetsUnion Clearing Mandate Boosting Third-Party Payment Volumes

The centralized clearing regime processes vast transaction volumes at a national scale, which demonstrates the technical capacity required to support continuous use of QR code-based and in-app transactions across retail and services. NetsUnion handled 319.67 billion transactions in Q3 2025, and UnionPay cleared 100.01 billion interbank transactions in the same period, establishing layers of redundancy and throughput in the core payments stack. Consolidation of clearing reduces fragmentation from the earlier direct-connection model between platforms and hundreds of banks, which improves visibility for the central bank and streamlines risk controls for anti-money-laundering monitoring. These structural gains support merchants and consumers as volumes spike during holiday periods and major shopping festivals, providing a buffer against operational bottlenecks. The scale and consistency of this infrastructure enable new fintech use cases to ride on stable rails while the Chinese fintech market broadens from payments into lending, insurance, and wealth, all of which depend on reliable clearing performance.

Data Security Law Tightening Cross-border Data Transfers for SaaS Fintechs

China's cross-border personal information framework is complete as of January 1, 2026, with certification available for certain volumes, standard contracts for many non-CIIOs, and security assessments required above thresholds, which creates operational checkpoints for international data flows. Sectoral rules for financial institutions require local storage and processing for financial customer information, which anchors data localization as a baseline obligation for banking and insurance entities. Amendments to the Cybersecurity Law raised maximum fines for severe violations and broadened extraterritorial reach, increasing enforcement risk for overseas activities that harm domestic cybersecurity. Incident reporting measures now require fast notification windows for CIIOs and network operators, which increases the governance burden for incident detection, triage, and response. These requirements heighten compliance architecture needs across engineering, legal, and operations teams for firms operating in or with China, and they influence product design and vendor choices throughout the China fintech market.

Other drivers and restraints analyzed in the detailed report include:

- SME Financing Gap Driving P2P & Supply-Chain Fintech Lending Platforms

- Wealth Management Connect Schemes Fuelling Robo-advisor Uptake

- Rising NPL Ratio in Micro-lending Elevating Capital-adequacy Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital payments held the largest position with a 59.23% share in 2025, reflecting the scale of QR-based and in-app payments integrated into everyday commerce within the Chinese fintech market. Centralized clearing confirms system capacity with 319.67 billion transactions processed by NetsUnion in Q3 2025 and 100.01 billion transactions cleared by UnionPay's interbank system, which underpins merchant acceptance and user trust. Mobile-first reach across retail categories keeps transaction velocity high, while e-CNY distribution through banks adds a public option that standardizes wallet design and reserves treatment from 2026. The duopoly of private platforms remains central to retail payments, supported by a large online user base and consumer familiarity that reinforces habitual use. These factors keep digital payments positioned as the anchor segment that supports cross-selling into lending, insurance, and wealth across the Chinese fintech market.

Neobanking is projected to post the fastest growth with a 19.58% CAGR through 2031 as digital-only banks use data and cloud-native cores to scale low-cost operations and AI-driven decisioning within the Chinese fintech market. WeBank's user and MSME footprint demonstrates the model's operating leverage and its ability to serve long-tail customers at scale, which supports fee and interest income diversification across retail and small business books. The digital lending landscape remains shaped by the earlier P2P wind down, with supply chain finance and licensed consumer finance taking the lead in filling credit gaps alongside inclusive bank lending. Wealth platforms gain from cross-boundary pilots and product standardization that lowers onboarding friction for advisory-led experiences. These dynamics collectively lift the growth outlook for neobanking and digital investments even as digital payments continue to carry the largest revenue base.

Complete Report Scope:

- By Service Proposition

- Digital Payments

- Digital Lending and Financing

- Digital Investments

- Insurtech

- Neobanking

- By End-User

- Retail

- Businesses

- By User Interface

- Mobile Applications

- Web / Browser

- POS / IoT Devices

List of Companies Covered in this Report:

- Ant Group (Alipay)

- Tencent Holdings (Tenpay)

- WeBank Co. Ltd.

- Lufax Holding Ltd.

- JD Technology (JD Digits)

- Ping An OneConnect Bank

- ZhongAn Online P&C Insurance

- Futu Holdings Ltd.

- Tiger Brokers (UP Fintech)

- 360 DigITech Inc.

- LexinFintech Holdings Ltd.

- Qudian Inc.

- Xiaomi Finance

- Lakala Payment Corp.

- UnionPay Merchant Services

- LianLian DigITech

- Huize Holding Ltd.

- Du Xiaoman Financial

- Suning Finance

- Wanda Fintech Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 PBOC e-CNY Roll-out Accelerating Digital Payments Adoption Across Tier-2/3 Cities

- 4.2.2 NetsUnion Clearing Mandate Boosting Third-Party Payment Volumes

- 4.2.3 SME Financing Gap Driving P2P & Supply-Chain Fintech Lending Platforms

- 4.2.4 Wealth Management Connect Schemes Fueling Robo-advisor Uptake

- 4.2.5 Commercial Health Insurance Tax Incentives Propelling InsurTech Growth

- 4.2.6 Cloud-native Core Upgrades by Joint-stock Banks Expanding BaaS/API Consumption

- 4.3 Market Restraints

- 4.3.1 Data Security Law Tightening Cross-border Data Transfers for SaaS Fintechs

- 4.3.2 Rising NPL Ratio in Micro-lending Elevating Capital-adequacy Burdens

- 4.3.3 Saturation of Mobile Payments Limiting Incremental Volume Growth

- 4.3.4 Cybersecurity Threats and Data Privacy Concerns

- 4.4 Value Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment & Funding Trend Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Ant Group (Alipay)

- 6.4.2 Tencent Holdings (Tenpay)

- 6.4.3 WeBank Co. Ltd.

- 6.4.4 Lufax Holding Ltd.

- 6.4.5 JD Technology (JD Digits)

- 6.4.6 Ping An OneConnect Bank

- 6.4.7 ZhongAn Online P&C Insurance

- 6.4.8 Futu Holdings Ltd.

- 6.4.9 Tiger Brokers (UP Fintech)

- 6.4.10 360 DigiTech Inc.

- 6.4.11 LexinFintech Holdings Ltd.

- 6.4.12 Qudian Inc.

- 6.4.13 Xiaomi Finance

- 6.4.14 Lakala Payment Corp.

- 6.4.15 UnionPay Merchant Services

- 6.4.16 LianLian DigiTech

- 6.4.17 Huize Holding Ltd.

- 6.4.18 Du Xiaoman Financial

- 6.4.19 Suning Finance

- 6.4.20 Wanda Fintech Group

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

替代投資技術市場預測至2034年-按解決方案、部署模式、投資類型、應用、最終用戶和地區分類的全球分析

替代投資技術市場預測至2034年-按解決方案、部署模式、投資類型、應用、最終用戶和地區分類的全球分析 重塑金融科技2.0的未來汽車金融科技市場預測至2034年:按車輛類型、驅動方式、銷售管道、最終用戶和地區分類的全球分析

重塑金融科技2.0的未來汽車金融科技市場預測至2034年:按車輛類型、驅動方式、銷售管道、最終用戶和地區分類的全球分析 金融科技市場:2026-2032年全球市場預測(按支付方式、部署模式、企業規模、技術、最終用戶和應用分類)

金融科技市場:2026-2032年全球市場預測(按支付方式、部署模式、企業規模、技術、最終用戶和應用分類) 伊斯蘭金融科技市場規模、佔有率和趨勢分析報告:按類型、部署模式、最終用途、地區和細分市場預測(2026-2033 年)金融科技即服務市場:依產品類型、部署模式、組織規模及最終用戶分類-2026-2032年全球預測全球金融科技市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

伊斯蘭金融科技市場規模、佔有率和趨勢分析報告:按類型、部署模式、最終用途、地區和細分市場預測(2026-2033 年)金融科技即服務市場:依產品類型、部署模式、組織規模及最終用戶分類-2026-2032年全球預測全球金融科技市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 金融科技市場商業分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案

金融科技市場商業分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案 2026年金融科技多重雲端全球市場報告

2026年金融科技多重雲端全球市場報告 金融科技產業市場:按金融科技卡、解決方案、技術、最終用戶和地區分類

金融科技產業市場:按金融科技卡、解決方案、技術、最終用戶和地區分類