|

市場調查報告書

商品編碼

2043966

終端和雲端管理安全:市場佔有率分析、行業趨勢和統計數據以及成長預測(2025-2030 年)Endpoint And Cloud Managed Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

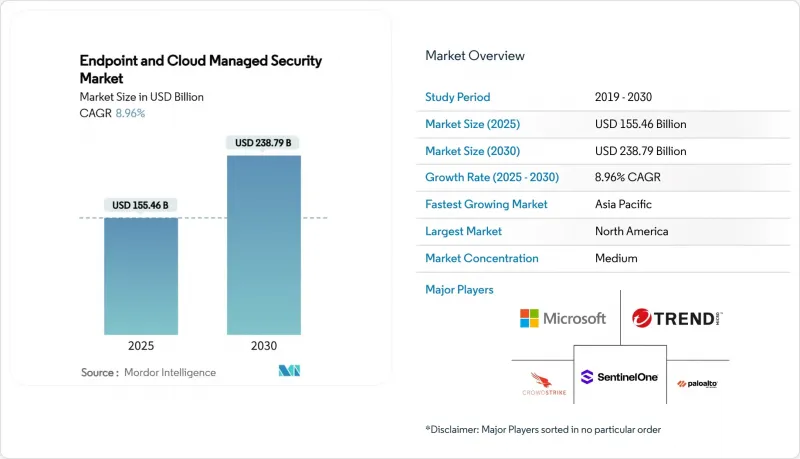

預計到 2025 年,終端和雲端管理安全市場規模將達到 1,554.6 億美元,到 2030 年將達到 2,387.9 億美元,同期複合年成長率為 8.96%。

企業網路安全營運外包的快速成長、混合辦公模式的普及以及雲端原生應用的興起,正在推動這一成長趨勢。更嚴格的網路保險要求、人工智慧驅動的威脅狩獵以及地緣政治供應鏈事件也增加了對託管偵測與回應 (MDR) 的需求。儘管平台供應商之間的整合正在重塑服務提供者的策略,但統一的安全堆疊正在幫助買家減少工具的氾濫,並降低整體擁有成本 (TCO)。

全球終端及雲端託管安全市場趨勢及洞察

混合辦公室終端數量的激增

與 2020 年之前相比,企業管理的終端設備數量增加了兩倍,這加劇了攻擊面的複雜性。整合和監控企業、個人和物聯網硬體給企業內部資源帶來了巨大壓力,促使企業將支出轉向託管安全合作夥伴。微軟的 Security Copilot 和 Intune 整合展示了人工智慧主導的管理如何幫助企業大規模保持可見度。企業報告稱,由於混合模式,網路安全複雜性增加了 40%,只有 23% 的企業承認自身擁有足夠的內部能力。因此,託管服務透過提供一致的措施、身分檢驗和合規性,而無需大幅增加人員配置,正在推動終端和雲端託管安全市場的成長。

雲端原生應用程式的普及率正在迅速提高。

目前,78% 的企業運行混合雲或多重雲端環境,容器、無伺服器和微服務工作負載激增。根據 Fortinet 預測,到 2027 年,雲端安全預算將以每年 25% 的速度成長,其中大部分將流向託管服務供應商,因為技能缺口正在擴大。 DevSecOps 的整合需要涵蓋從傳統終端到最新雲端平台的專業知識,這推動了包含持續工作負載狀態管理的整合外包合約的出現。

宏觀經濟逆風導致預算緊張

由於經濟放緩,儘管威脅日益加劇,許多企業的安全預算卻停滯不前。企業董事會質疑是否需要增加支出,認為現有措施已足夠。諸如NIS2之類的監管要求仍然要求最低投資額,這導致市場兩極化:在合規至關重要的行業,支出得以維持;而在非必要行業,項目則被推遲。隨著買家更加重視價值而非廣度,能夠量化投資回報率並整合各種工具的託管安全供應商正成為他們的首選。

細分市場分析

受強制網路保險和即時遙測技術普及的推動,託管式端點偵測與回應 (EDR) 服務在 2024 年佔據了端點和雲端託管安全市場 28.3% 的主導佔有率。合規性主導的普及確保了其收入的穩定,即便其他非必需消費類別的成長放緩。託管式整合端點管理服務以 14.8% 的複合年成長率 (CAGR) 成長,反映了企業對跨筆記型電腦、行動裝置和物聯網端點的單一介面裝置管治的需求。

功能融合正在模糊終端管理和安全之間的界線。供應商現在將設備管理、威脅偵測和策略合規性打包到整合訂閱服務中,這減少了供應商的總數。傳統的防毒服務正變得商品化,供應商越來越關注行為分析和客製化的回應策略。隨著客戶擴展其防護層級,身分管理、資料防洩漏 (DLP) 和新興的行動威脅防禦服務正在豐富其產品組合。

預計到2024年,基於雲端的交付模式將佔據終端和雲端管理安全市場66.1%的佔有率,並持續以10.6%的複合年成長率成長至2030年。企業更傾向於採用彈性、API驅動的控制方案,而非固定硬體,尤其是在需要持續更新模型的AI分析工作負載方面。儘管本地部署在監管嚴格的行業仍然普遍存在,但許多企業正在採用混合架構,將本地感測器的資料傳送到雲端進行分析。

保全服務邊緣的採用進一步加速了向雲端的遷移,將網路存取控制和威脅掃描整合到託管服務中。總體擁有成本 (TCO) 研究表明,在考慮基礎設施折舊免稅額、人事費用和與修補程式相關的間接成本後,與同等本地部署相比,可節省 40% 至 60% 的成本。

《端點和雲端託管安全市場報告》按服務類型(託管端點檢測和回應服務、其他)、部署模式(本地部署、雲端部署、混合部署)、安全類型(端點安全、雲端工作負載安全、其他)、組織規模(中小企業和大型企業)、最終用戶行業(銀行、金融服務和保險、IT 和電信、醫療保健、其他)以及地區進行細分。

區域分析

2024年,北美將佔據終端和雲端託管安全市場38.7%的佔有率,這得益於雲端安全的早期普及、成熟的網路保險市場以及大規模的政府外包體系。美國財政部簽署的200億美元支援合約表明,聯邦政府希望建立長期的管理夥伴關係。加拿大企業遵循美國標準,跨境提供者正利用通用的語言和監管環境的相似性來簡化服務交付流程。

亞太地區預計將以14.2%的複合年成長率成長,受益於數位服務的爆炸性成長和法規結構的不斷改進。谷歌雲端在印尼推出的「BerdAIa」舉措,在本地資料中心部署了人工智慧驅動的安全營運中心(SOC)功能,是服務供應商在地化策略的典範。日益猖獗的網路犯罪和技能短缺正在推動東協和南亞國家對承包託管服務的需求。

在歐洲,受NIS2、GDPR以及即將到來的人工智慧法規的影響,合規性外包業務持續成長。根據歐盟網路安全與資訊安全局(ENISA)的數據,安全支出目前佔歐盟IT預算的9%,且逐年成長。那些擁有本地資料處理、多語言安全營運中心(SOC)支援以及歐盟認證託管服務的供應商,正吸引那些尋求在主權和營運靈活性之間取得平衡的企業。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合工作終端數量的激增

- 雲端原生應用程式的採用率正在激增。

- MDR中網路保險的要求

- 對XDR平台整合的需求

- 人工智慧驅動的威脅狩獵技術取得進展

- 地緣政治因素導致供應鏈攻擊事件加劇

- 市場限制因素

- 警覺性過高導致的疲勞加劇以及技能不足

- 與資料主權相關的合規性挑戰

- 宏觀經濟逆風導致預算緊張

- 對MSP供應商鎖定問題的擔憂

- 價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按服務類型

- 託管端點偵測與回應服務

- 託管式防毒/反惡意軟體服務

- 託管身分和存取管理服務

- 託管預防資料外泄服務

- 託管式移動威脅防禦

- 託管整合端點管理服務

- 其他

- 部署模式

- 現場

- 基於雲端的

- 混合

- 按安全類型

- 端點安全

- 雲端工作負載安全

- 雲端存取安全仲介(CASB)

- 雲端電子郵件安全

- 雲端網路安全

- 雲端身份驗證安全

- 按組織規模

- 小型企業

- 大公司

- 按最終用戶行業分類

- BFSI

- 資訊科技和通訊

- 衛生保健

- 零售與電子商務

- 製造業

- 政府/國防

- 能源與公共產業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CrowdStrike Holdings, Inc.

- Palo Alto Networks, Inc.

- Trend Micro Incorporated

- Sophos Group plc

- SentinelOne, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Secureworks, Inc.

- Arctic Wolf Networks, Inc.

- AT&T Cybersecurity(AT&T Inc.)

- Kaspersky Lab

- ESET, spol. s ro

- VMware, Inc.(Broadcom Inc.)

- Rapid7, Inc.

- Cybereason Inc.

- F-Secure Corporation

- Bitdefender SRL

- NCC Group plc

- Trustwave Holdings, Inc.(Singtel)

- Qualys, Inc.

- Elastic NV

- Darktrace plc

- Trellix

- Malwarebytes Inc.

第7章 市場機會與未來展望

The Endpoint and Cloud Managed Security Market reached a current market size of USD 155.46 billion in 2025 and is forecast to attain USD 238.79 billion by 2030, registering an 8.96% CAGR over the period.

Rapid enterprise migration to outsourced cyber-operations, hybrid workforce expansion, and cloud-native application growth are steering this trajectory. Heightened cyber-insurance conditions, AI-driven threat-hunting, and geopolitical supply-chain incidents are also intensifying demand for managed detection and response. Consolidation among platform vendors is reshaping provider strategies, while unified security stacks are helping buyers curb tool sprawl and lower total cost of ownership.

Global Endpoint And Cloud Managed Security Market Trends and Insights

Proliferation of Hybrid-Work Endpoints

Organizations now manage triple the endpoint devices compared to pre-2020 levels, increasing attack-surface complexity. Unified monitoring over corporate, personal, and IoT hardware is stretching in-house resources, steering spending toward managed security partners. Microsoft's Security Copilot integration with Intune shows how AI-guided administration helps sustain visibility at scale. Enterprises report a 40% jump in cybersecurity complexity from hybrid models and admit only 23% possess adequate internal capabilities. Managed services thus deliver consistent policies, identity validation, and compliance without ballooning headcount, reinforcing the Endpoint and Cloud Managed Security Market's growth arc.

Surging Cloud-Native Application Adoption

Seventy-eight percent of enterprises now operate hybrid or multi-cloud environments, with container, serverless, and microservice workloads proliferating. Fortinet indicates cloud security budgets are expanding 25% annually to 2027, and managed providers are capturing the lion's share as skills gaps widen. DevSecOps convergence demands expertise spanning legacy endpoints and modern clouds, driving unified outsourcing contracts that embed continuous workload posture management.

Budget Squeeze from Macro Headwinds

Economic slowdowns have stalled many security budgets even as threat volume rises. Corporate boards question incremental spend, believing existing controls should suffice. Regulatory mandates such as NIS2 still force minimum investments, creating a split market where compliance-bound sectors sustain spending while discretionary sectors defer projects. Managed security vendors that quantify ROI and consolidate tools earn preference as buyers seek value over breadth.

Other drivers and restraints analyzed in the detailed report include:

- Cyber-Insurance Prerequisites for MDR

- XDR Platform Unification Demand

- MSP Vendor Lock-in Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed Endpoint Detection and Response Services held a commanding 28.3% share of the Endpoint and Cloud Managed Security market size in 2024, anchored by cyber-insurance mandates and real-time telemetry gains. Compliance-driven uptake supports steady revenue even when other discretionary categories decelerate. Managed Unified Endpoint Management Services, expanding at 14.8% CAGR, reflect enterprise appetites for single-pane device governance spanning laptops, mobiles, and IoT endpoints.

Functional convergence is blurring the lines between endpoint management and security. Providers now package device administration, threat detection, and policy compliance in a unified subscription, reducing the total vendor count. Traditional antivirus services have commoditized, prompting vendors to emphasize behavioral analytics and tailored response playbooks. Identity, DLP, and emerging mobile-threat defense services round out portfolios as clients broaden protection layers.

Cloud-based delivery captured 66.1% Endpoint and Cloud Managed Security market share in 2024 and is on track for a 10.6% CAGR to 2030. Organizations favor elastic, API-driven controls over fixed hardware, particularly as AI analytics workloads need continuous model refreshes. On-premise installations persist in highly regulated sectors, yet many adopt hybrid overlays where local sensors feed cloud analytics.

Security service edge adoption further tilts uptake toward cloud, combining network access control and threat inspection within managed offerings. Total cost of ownership studies show 40-60% savings compared with equivalent in-house setups after factoring in infrastructure depreciation, staff, and patching overheads.

Endpoint and Cloud Managed Security Market Report is Segmented by Service Type (Managed Endpoint Detection and Response Services, and More), Deployment Mode (On-Premise, Cloud-Based, and Hybrid), Security Type (Endpoint Security, Cloud Workload Security, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), and Geography.

Geography Analysis

North America accounted for 38.7% of the Endpoint and Cloud Managed Security market size in 2024, buoyed by early cloud-security adoption, mature cyber-insurance markets, and sizable government outsourcing frameworks. The U.S. Treasury's USD 20 billion support contract illustrates federal appetite for long-term managed partnerships. Canadian organizations align with U.S. standards, while cross-border providers leverage shared language and regulatory commonalities to streamline service delivery.

Asia-Pacific, forecast to expand at a 14.2% CAGR, benefits from explosive digital-service uptake and widening regulatory frameworks. Google Cloud's Indonesia BerdAIa initiative, which deploys AI-enabled SOC capabilities within local data centers, demonstrates provider localization strategies. Rising cybercrime and skill shortages amplify demand for turnkey managed offerings across ASEAN and South Asian economies.

Europe sustains growth through NIS2, GDPR, and upcoming AI regulations, driving compliance-centric outsourcing. ENISA notes that security now consumes 9% of EU IT budgets, reflecting year-on-year elevation. Providers boasting local-data processing, multi-language SOC support, and EU-certified hosting attract enterprises balancing sovereignty with operational agility.

- CrowdStrike Holdings, Inc.

- Palo Alto Networks, Inc.

- Trend Micro Incorporated

- Sophos Group plc

- SentinelOne, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Secureworks, Inc.

- Arctic Wolf Networks, Inc.

- AT&T Cybersecurity (AT&T Inc.)

- Kaspersky Lab

- ESET, spol. s r.o.

- VMware, Inc. (Broadcom Inc.)

- Rapid7, Inc.

- Cybereason Inc.

- F-Secure Corporation

- Bitdefender SRL

- NCC Group plc

- Trustwave Holdings, Inc. (Singtel)

- Qualys, Inc.

- Elastic N.V.

- Darktrace plc

- Trellix

- Malwarebytes Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of hybrid-work endpoints

- 4.2.2 Surging cloud-native application adoption

- 4.2.3 Cyber-insurance prerequisites for MDR

- 4.2.4 XDR platform unification demand

- 4.2.5 AI-driven threat-hunting advances

- 4.2.6 Geo-political supply-chain attacks escalation

- 4.3 Market Restraints

- 4.3.1 High alert-fatigue and skill shortage

- 4.3.2 Data-sovereignty compliance hurdles

- 4.3.3 Budget squeeze from macro headwinds

- 4.3.4 MSP vendor lock-in concerns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Managed Endpoint Detection and Response Services

- 5.1.2 Managed Antivirus/Antimalware Services

- 5.1.3 Managed Identity and Access Management Services

- 5.1.4 Managed Data Loss Prevention Services

- 5.1.5 Managed Mobile Threat Defense

- 5.1.6 Managed Unified Endpoint Management Services

- 5.1.7 Others

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Security Type

- 5.3.1 Endpoint Security

- 5.3.2 Cloud Workload Security

- 5.3.3 Cloud Access Security Broker (CASB)

- 5.3.4 Cloud Email Security

- 5.3.5 Cloud Web Security

- 5.3.6 Cloud Identity Security

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing

- 5.5.6 Government and Defense

- 5.5.7 Energy and Utilities

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CrowdStrike Holdings, Inc.

- 6.4.2 Palo Alto Networks, Inc.

- 6.4.3 Trend Micro Incorporated

- 6.4.4 Sophos Group plc

- 6.4.5 SentinelOne, Inc.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Check Point Software Technologies Ltd.

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 Secureworks, Inc.

- 6.4.10 Arctic Wolf Networks, Inc.

- 6.4.11 AT&T Cybersecurity (AT&T Inc.)

- 6.4.12 Kaspersky Lab

- 6.4.13 ESET, spol. s r.o.

- 6.4.14 VMware, Inc. (Broadcom Inc.)

- 6.4.15 Rapid7, Inc.

- 6.4.16 Cybereason Inc.

- 6.4.17 F-Secure Corporation

- 6.4.18 Bitdefender SRL

- 6.4.19 NCC Group plc

- 6.4.20 Trustwave Holdings, Inc. (Singtel)

- 6.4.21 Qualys, Inc.

- 6.4.22 Elastic N.V.

- 6.4.23 Darktrace plc

- 6.4.24 Trellix

- 6.4.25 Malwarebytes Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球終端安全市場

2026-2030年全球終端安全市場 終端安全市場:2026-2032年全球市場預測(依產品、作業系統、應用程式、最終用戶、部署類型及企業規模分類)

終端安全市場:2026-2032年全球市場預測(依產品、作業系統、應用程式、最終用戶、部署類型及企業規模分類) 終端安全市場報告:按組件、部署模式、組織規模、產業和地區分類(2026-2034 年)

終端安全市場報告:按組件、部署模式、組織規模、產業和地區分類(2026-2034 年) 終端安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

終端安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球終端安全市場報告

2026年全球終端安全市場報告 終端安全市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

終端安全市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 終端安全市場:依組件、應用點(工作站、行動裝置、伺服器、POS終端)、部署類型、產業規模和最終用戶(航空航太與國防、政府、銀行與金融保險、醫療保健、製造業) - 至2036年的全球預測

終端安全市場:依組件、應用點(工作站、行動裝置、伺服器、POS終端)、部署類型、產業規模和最終用戶(航空航太與國防、政府、銀行與金融保險、醫療保健、製造業) - 至2036年的全球預測 端點安全市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球終端安全市場規模、佔有率、趨勢和成長分析報告(2026-2034)

端點安全市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類全球終端安全市場規模、佔有率、趨勢和成長分析報告(2026-2034) 終端安全市場 - 全球產業規模、佔有率、趨勢、機會和預測(按解決方案、部署模式、組織規模、最終用戶、地區和競爭格局分類,2021-2031 年)

終端安全市場 - 全球產業規模、佔有率、趨勢、機會和預測(按解決方案、部署模式、組織規模、最終用戶、地區和競爭格局分類,2021-2031 年)