|

市場調查報告書

商品編碼

2043960

浸沒式冷卻液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Immersion Cooling Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

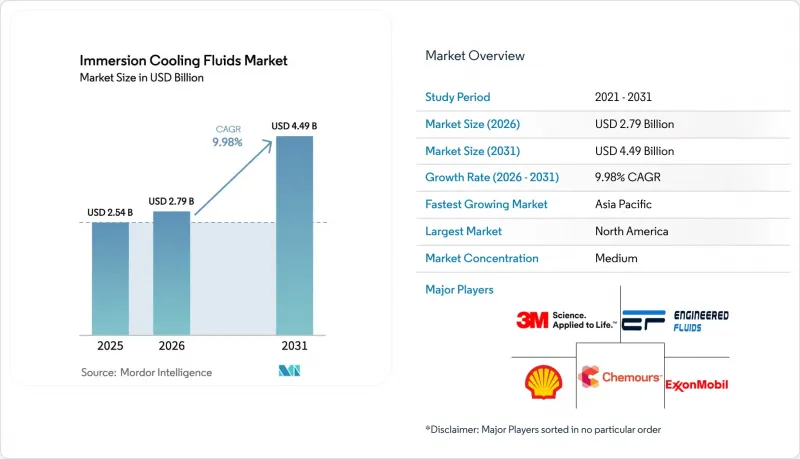

預計浸沒式冷卻劑市場將從 2025 年的 25.4 億美元和 2026 年的 27.9 億美元成長到 2031 年的 44.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.98%。

機架密度不斷攀升,超過30千瓦;超大規模營運商紛紛轉向單園區超過400兆瓦的人工智慧叢集;以及利用廢熱進行商業化的區域供熱項目,正在重塑資料中心的經濟格局。儘管北美和歐洲逐步淘汰PFAS化合物的監管期限促使買家轉向不含PFAS的合成油和酯類,但英特爾對殼牌和埃克森美孚潤滑油的2025年認證,掃清了超大規模部署的一大障礙。因此,目前成本為每公升2-5美元的單相礦物油系統仍佔據已部署容量的大部分,但不含PFAS的氟化替代品已成為成長最快的化學品。競爭依然激烈,沒有一家供應商的市佔率超過12%,但擁有煉油規模和晶片製造商支持的供應商的影響力正在不斷增強。

全球浸沒式冷卻液市場趨勢及洞察

能源效率和PUE最佳化面臨的壓力日益增大

對於目標是將PUE值控制在1.15以下的運營商而言,當機架密度超過30kW時,風冷會帶來顯著的性能損失。單相浸沒式冷卻可以降低風扇和冷卻器的負荷,將PUE值控制在1.05到1.15之間,而雙相冷卻則能達到1.02到1.08。微軟計劃於2025年7月在其所有資料中心部署直接液冷技術,而Colovore公司也獲得了9.25億美元的資金籌措,以確保每個機架擁有200kW的容量,這些都表明液冷技術正從試點階段轉向標準工程。根據Dell'Oro Group的研究,液冷市場在2025年實現了85%的年成長,但浸沒式冷卻技術的發展仍落後於晶片直接冷卻(DTC)維修。歐洲資料中心協會(EDCA)的研究表明,2024年浸沒式冷卻技術的採用率僅為5.6%,這意味著這項轉變還需要5到10年的時間。英特爾和殼牌進行的測試證實,節能高達 48%,二氧化碳排放量減少 30%,用水量減少 99%,這與兩家公司以科學為導向的目標相符。

永續性和碳中和目標正在加速其普及應用。

在區域供熱項目中,供熱價格設定為每兆瓦時12-22歐元,比燃氣鍋爐便宜約50%。 AWS Talat在2024年滿足了都柏林聖三一學院92%的供熱需求,減少了704噸二氧化碳排放。這證明了供熱的盈利。微軟和Fortum在芬蘭的一項計畫預計到2026年將為25萬居民提供服務。在新加坡,取消禁令、強制要求PUE值低於1.3、採購可再生能源,正在推動STT GDC採用液冷技術。 Meta投資650億美元的人工智慧設施建設項目和谷歌投資400億美元的德克薩斯州項目都明確規定採用液冷技術,這將為託管運營商帶來每千瓦20-40%的價格優勢。

人們對 PFAS 法規相關的材料合規性和安全性問題感到擔憂

碳氫化合物冷卻劑會腐蝕某些彈性體,因此針對特定零件檢驗至關重要。嘉吉公司的FR3雖然可生物分解,但會造成高溫區域,可能縮短低利潤率產品的使用壽命。兩相儲槽需要氣密密封。即使是微小的洩漏也會顯著降低性能,如果冷卻液易燃,還會增加火災風險。由於缺乏長期現場數據,殼牌和埃克森美孚的產品直到2025年才通過英特爾的測試。規避風險的銀行、金融和保險(BFSI)用戶正在推遲轉換。歐盟和美國不同的法規要求進行區域性混合,這增加了產品種類和成本。

細分市場分析

2025年,在英特爾對殼牌和埃克森美孚配方的支持下,合成烴佔據了浸沒式冷卻液市場37.12%的佔有率。由科慕、索爾維和陶氏重新推出的不含PFAS的氫氟醚類氟化液,預計在預測期(2026-2031年)內將以10.22%的複合年成長率成長。礦物油因其每公升2-5美元的價格和6-12個月的投資回收期,繼續受到加密貨幣礦工的青睞。同時,天然酯類混合物雖然符合IEC 62770標準,但由於其高熱值,在高效能運算(HPC)領域的應用受到限制。 Dynaleen和Engineered Fluids等工程供應商透過滿足客戶的客製化需求,獲得了高利潤率。

預計到2025年,單相系統在浸沒式冷卻劑市場將佔據64.44%的佔有率,並以10.36%的複合年成長率成長。這主要得益於其較低的初始投資成本(無需氣密密封)、更簡單的流體管理(無需蒸發控制)以及與可處理50–60 度C入口溫度的區域供熱網路的兼容性。對於超過100 kW的機組,雙相系統仍然至關重要,Accelsius的管道系統和DarkNX位於安大略省的300 MW園區證明了這一點,它們的PUE值達到了1.02–1.08。然而,由於密封設計的複雜性和冷媒管理的難度,目前雙相系統的應用仍處於小眾領域。

區域分析

北美市場引領市場,預計到2025年將佔全球收入的41.18%,這主要得益於Meta公司650億美元的人工智慧基礎設施建設以及谷歌在德克薩斯州投資400億美元的項目。亞太地區預計將以10.45%的複合年成長率成長,這主要得益於新加坡的綠色資料中心法規、日本9.6%的市場複合年成長率以及印度200kW機架的引入。在歐洲,廢熱的有效利用正在取得進展,AWS Talat在2024年減少了704噸二氧化碳排放,微軟和Fortum計劃到2026年為25萬芬蘭人供暖,預計將使運營商的投資回報率提高15-25%。拉丁美洲和中東地區正保持兩位數的成長,但面臨危險材料法規和勞動力短缺的問題,減緩了水冷伺服器的普及速度。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 能源效率和PUE最佳化面臨的壓力日益增大

- 永續發展和碳中和目標正在加速其普及應用。

- 更嚴格的 PFAS 淘汰期限將改變流體化學的研究方式。

- 新興市場邊緣微型資料中心的成長

- 熱能再利用舉措正在推動區域供熱系統的整合。

- 市場限制因素

- 對 PFAS 法規下材料的合規性和安全性的擔憂

- 整個OEM生態系缺乏標準和互通性。

- 3M退出後,合成基礎油供應鏈出現波動

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按流體類型

- 合成烴油

- 礦物油

- 含氟液體

- 酯類/生物基和可生物分解液體

- 其他流體類型

- 透過冷卻法

- 單相液體浸沒冷卻

- 兩相浸沒式冷卻

- 透過使用

- 資料中心 - 超大規模

- 資料中心託管

- 資料中心 - 企業

- 加密貨幣挖礦/區塊鏈

- 高效能運算和人工智慧訓練叢集

- 電力電子與工業計算

- 電動車快速充電和電池溫度控管

- 其他

- 按最終用戶行業分類

- 資訊科技和通訊

- BFSI

- 製造業和工業

- 能源與公共產業

- 汽車和交通運輸

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 新加坡

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 荷蘭

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- AGC Inc.

- Cargill

- Castrol Limited(BP)

- Chevron Oronite

- DOW

- Dynalene Inc.

- Engineered Fluids

- ExxonMobil Corporation

- FUCHS

- Lubrizol

- M&I Materials Ltd

- Shell plc

- Solvay

- The Chemours Company

- TotalEnergies

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The Immersion Cooling Fluids Market size is projected to expand from USD 2.54 billion in 2025 and USD 2.79 billion in 2026 to USD 4.49 billion by 2031, registering a CAGR of 9.98% between 2026 and 2031. Growing rack densities that exceed 30 kilowatts, hyperscale operators' shift toward AI clusters above 400 MW per campus, and district-heating programs that monetize waste heat are redefining data-center economics. Regulatory deadlines phasing out PFAS compounds in North America and Europe are steering buyers toward PFAS-free synthetics and esters, while Intel's 2025 certification of Shell and ExxonMobil fluids removed a key hurdle for hyperscale adoption. As a result, single-phase systems priced at USD 2-5 per liter for mineral oils dominate installed capacity, yet fluorinated alternatives, now PFAS-free, are the fastest-growing chemistry. Competitive intensity remains high because no vendor holds more than 12% share, but suppliers that combine refining scale with chip-maker endorsements are consolidating influence.

Global Immersion Cooling Fluids Market Trends and Insights

Rising Energy-Efficiency and PUE Optimization Pressures

Operators pushing PUE below 1.15 face steep air-cooling penalties once rack densities top 30 kW. Single-phase immersion reduces fan and chiller loads, delivering a PUE of 1.05-1.15, while two-phase achieves 1.02-1.08. Microsoft's fleetwide rollout of direct liquid cooling in July 2025 and Colovore's USD 925 million financing for 200 kW-per-rack capacity mark a shift from pilot to baseline engineering. Dell'Oro Group recorded 85% year-over-year liquid-cooling growth in 2025, although immersion still trails direct-to-chip retrofits. The European Data Centre Association measured only 5.6% immersion adoption in 2024, underscoring a five-to-ten-year conversion window. Intel-Shell tests confirmed up to 48% energy savings, 30% CO2 reduction, and 99% lower water use, aligning with corporate science-based targets.

Sustainability and Carbon-Neutral Targets Accelerate Adoption

District-heating programs price delivered heat at EUR 12-22 per MWh, undercutting gas boilers by roughly 50%. AWS Tallaght supplied 92% of Trinity College Dublin's heating and cut 704 tons of CO2 in 2024, proving revenue-positive heat export. Microsoft-Fortum's Finland scheme will reach 250,000 residents by 2026. Singapore's moratorium lift now mandates PUE less than 1.3 and renewable sourcing, stimulating liquid cooling at STT GDC. Meta's USD 65 billion AI build and Google's USD 40 billion Texas plan both specify liquid cooling, giving colocation operators pricing power premiums of 20-40% per kilowatt.

Material Compatibility and Safety Concerns Amid PFAS Regulation

Hydrocarbon coolants can attack certain elastomers, forcing component-by-component validation. Cargill FR3 is biodegradable but creates hotter spots, potentially shortening lifecycle in tight-margin designs. Two-phase tanks demand hermetic sealing; micro-leaks slash performance and raise fire risk when fluids are flammable. Absent long-term field data, Shell and ExxonMobil only cleared Intel tests in 2025; risk-averse BFSI users defer conversion. Divergent EU and U.S. rules oblige region-specific blends, inflating SKUs and cost.

Other drivers and restraints analyzed in the detailed report include:

- Stricter PFAS-Phase-Out Deadlines Reshape Fluid Chemistries

- Growing Edge-Micro-Data-Centers in Untapped Emerging Markets

- Limited Standards / Inter-Operability Across OEM Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic hydrocarbons captured 37.12% of the Immersion Cooling Fluids market share in 2025, buoyed by Intel's endorsement of Shell and ExxonMobil formulas. Fluorinated fluids, relaunched as PFAS-free hydrofluoroethers by Chemours, Solvay, and DOW, are forecast for a 10.22% CAGR during the forecast period (2026-2031). Mineral oils keep crypto miners loyal thanks to USD 2-5 per-liter pricing and 6-12 month paybacks, while natural-ester blends meet IEC 62770 yet run hotter, curbing HPC uptake. Engineered suppliers such as Dynalene and Engineered Fluids fill customization gaps at premium margins.

Single-phase accounted for 64.44% of the Immersion Cooling Fluids market size in 2025 and should grow at a 10.36% CAGR, reflecting their lower capital cost (no hermetic sealing required), simpler fluid management (no evaporation control), and compatibility with district-heating networks that accept 50-60°C inlet temperatures. Two-phase remains essential for racks above 100 kW, demonstrated by Accelsius pipelines and DarkNX's 300 MW Ontario campus hitting PUE 1.02-1.08. However, hermetic design complexity and refrigerant management keep the two-phase adoption niche today.

The Immersion Cooling Fluids Market Report is Segmented by Fluid Type (Synthetic Hydrocarbon Oils, and More), Cooling Type (Single-Phase Immersion Cooling and More), Application (Data Centers - Hyperscale, and More), End-User Industry (IT and Telecom, BFSI, and Mores), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 41.18% of 2025 revenue owing to Meta's USD 65 billion AI build and Google's USD 40 billion Texas project. Asia-Pacific shows a 10.45% forecast CAGR, catalyzed by Singapore's green-data-center rules, Japan's 9.6% market CAGR, and India's 200 kW-rack deployments. Europe monetizes waste heat, AWS Tallaght cut 704 tons of CO2 in 2024, and Microsoft-Fortum will heat 250,000 Finns by 2026, creating 15-25% better ROI for operators. Latin America and the Middle East record double-digit growth but struggle with hazmat regulations and skills shortages, slowing immersion ramp.

List of Companies Covered in this Report:

- 3M

- AGC Inc.

- Cargill

- Castrol Limited (BP)

- Chevron Oronite

- DOW

- Dynalene Inc.

- Engineered Fluids

- ExxonMobil Corporation

- FUCHS

- Lubrizol

- M&I Materials Ltd

- Shell plc

- Solvay

- The Chemours Company

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising energy-efficiency and PUE optimization pressures

- 4.2.2 Sustainability and carbon-neutral targets accelerate adoption

- 4.2.3 Stricter PFAS-phase-out deadlines reshape fluid chemistries

- 4.2.4 Growing edge-micro-data-centers in untapped emerging markets

- 4.2.5 Heat-to-heat-re-use initiatives driving district-heating integration

- 4.3 Market Restraints

- 4.3.1 Material compatibility and safety concerns amid PFAS regulation

- 4.3.2 Limited standards/inter-operability across OEM ecosystems

- 4.3.3 Volatility in synthetic base-oil supply chain post-3M exit

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fluid Type

- 5.1.1 Synthetic Hydrocarbon Oils

- 5.1.2 Mineral Oils

- 5.1.3 Fluorinated Fluids

- 5.1.4 Esters / Bio-based and Biodegradable Fluids

- 5.1.5 Other Fluid Types

- 5.2 By Cooling Type

- 5.2.1 Single-phase Immersion Cooling

- 5.2.2 Two-phase Immersion Cooling

- 5.3 By Application

- 5.3.1 Data Centers - Hyperscale

- 5.3.2 Data Centers - Colocation

- 5.3.3 Data Centers - Enterprise

- 5.3.4 Crypto-mining/Blockchain

- 5.3.5 HPC and AI Training Clusters

- 5.3.6 Power Electronics and Industrial Computing

- 5.3.7 EV Fast-charging and Battery Thermal Management

- 5.3.8 Other Applications

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing and Industrial

- 5.4.4 Energy and Utilities

- 5.4.5 Automotive and Transportation

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 Singapore

- 5.5.1.5 South Korea

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Cargill

- 6.4.4 Castrol Limited (BP)

- 6.4.5 Chevron Oronite

- 6.4.6 DOW

- 6.4.7 Dynalene Inc.

- 6.4.8 Engineered Fluids

- 6.4.9 ExxonMobil Corporation

- 6.4.10 FUCHS

- 6.4.11 Lubrizol

- 6.4.12 M&I Materials Ltd

- 6.4.13 Shell plc

- 6.4.14 Solvay

- 6.4.15 The Chemours Company

- 6.4.16 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

浸沒式冷卻液市場-2026-2032年全球市場預測

浸沒式冷卻液市場-2026-2032年全球市場預測 浸沒式冷卻液市場-全球及區域分析:按應用、產品與國家分類-分析與預測(2025-2035 年)

浸沒式冷卻液市場-全球及區域分析:按應用、產品與國家分類-分析與預測(2025-2035 年) 浸沒式冷卻液市場商機、成長要素、產業趨勢分析及2026-2035年預測

浸沒式冷卻液市場商機、成長要素、產業趨勢分析及2026-2035年預測 浸沒式冷卻液市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、設備、部署及最終用戶分類

浸沒式冷卻液市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、設備、部署及最終用戶分類 全球浸沒式冷卻液市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球浸沒式冷卻液市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球浸沒式冷卻液市場:預測(至2034年)-按類型、冷卻技術、部署方式、應用、最終用戶和地區進行分析

全球浸沒式冷卻液市場:預測(至2034年)-按類型、冷卻技術、部署方式、應用、最終用戶和地區進行分析 2026年全球浸沒式冷卻液市場報告

2026年全球浸沒式冷卻液市場報告 浸沒式冷卻液市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

浸沒式冷卻液市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 亞太地區浸入式冷卻液市場(按應用、產品和國家)分析與預測(2024 年至 2034 年)

亞太地區浸入式冷卻液市場(按應用、產品和國家)分析與預測(2024 年至 2034 年) 歐洲浸沒式冷卻液市場(按應用、產品和國家分類)分析與預測(2024 年至 2034 年)

歐洲浸沒式冷卻液市場(按應用、產品和國家分類)分析與預測(2024 年至 2034 年)