|

市場調查報告書

商品編碼

2043953

喜來芝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Shilajit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

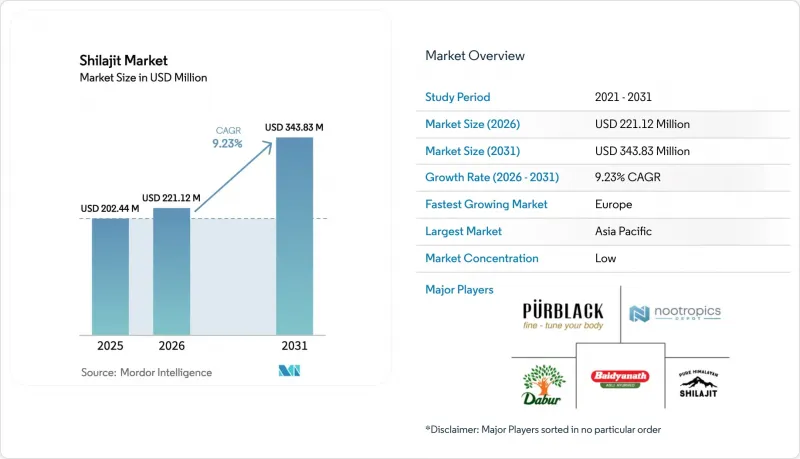

預計喜來芝市場將經歷顯著成長,從 2025 年的 2.0244 億美元成長到 2026 年的 2.2112 億美元,到 2031 年達到 3.4383 億美元。

預計 2026 年至 2031 年的年複合成長率(CAGR)為 9.13%。

這項成長主要受以下因素驅動:消費者對植物來源原的需求不斷成長、富裡酸標準化配方法規結構的逐步明確,以及消費者對健康老化的日益關注。在亞太地區,傳統定位仍然是成長的主要驅動力;而在北美,經證實的臨床療效和潔淨標示聲明是影響產品滲透率的關鍵因素。此外,水溶性粉末和軟糖等創新產品的出現,也拓展了喜來芝的吸引力,使其不再侷限於傳統的樹脂形式。在這些發展趨勢下,市場面臨品管方面的挑戰,凸顯了第三方偵測和可追溯採購系統對於品牌維持競爭優勢的重要性。

全球喜來芝市場趨勢與見解

隨著植物來源和純素食補充劑越來越受歡迎,喜來芝被定位為一種天然替代品。

隨著消費者越來越重視原料來源、生產過程和產品真實性的透明度,植物來源補充劑正在改變健康產業。喜來芝(Shilajit)是一種礦物瀝青樹脂,由植物分解產物經過數百年自然形成,作為一種植物來源品,正逐漸受到關注,成為膠原蛋白和魚油等動物源性補充劑的替代選擇,並成為素食者和純素食者的理想之選。喜來芝富含富裡酸酸、微量元素和抗氧化劑,能夠促進能量生成、增強免疫功能並改善整體健康,其效果堪比合成複合綜合維他命。其源自阿育吠陀的傳統,更使其在傳統和「天然」治療方法備受推崇且價格高昂的市場中更具吸引力。然而,確保產品純度至關重要,因為摻雜填充劑或合成富裡酸會損害消費者信任,並違背「潔淨標示」的承諾。為了應對這些挑戰並在競爭激烈的市場中脫穎而出,由 USDA 有機認證和非基因改造項目認證等第三方機構進行的檢查和認證對於建立消費者的信任和信心至關重要。

產品配方與形體的創新

喜來芝憑藉著軟糖、滴劑和功能飲料等創新產品形式而廣受歡迎,迎合了Z世代的偏好,他們注重便利性、口感以及對特定飲食限制的適應性。 2024年,Blusque和Angel Gummies等品牌推出了添加喜來芝的軟糖,以天然甜味劑和水果萃取物來緩和樹脂的苦味。同時,2025年10月,Purblack推出了一種標準化的“研究級喜來芝樹脂”,其中含有超過60%的富裡酸和超過50%的二苯並-α-吡喃酮,目標客戶是生物駭客和競技運動員。複合產品也備受關注。喜來芝和睡茄的組合產品可以在單一產品中同時解決壓力和能量問題,而喜來芝和薑黃的混合物則針對發炎和關節健康。 Natreon 的取得專利的產品「PrimaVie」是一種經過臨床研究的喜來芝萃取物,是尋求經人體驗證功效的高階品牌的理想成分,符合歐洲食品安全局 (EFSA) 1924/2006 號法規中嚴格的健康標籤規定。雖然脂質奈米顆粒和奈米技術等先進的封裝技術提高了生物利用度,但其高昂的成本限制了其在高級產品中的應用。隨著這些技術的進步使喜來芝成為一種用途廣泛的健康平台,品牌必須在創新和真實性之間取得平衡,才能留住那些偏愛「天然」喜來芝樹脂的傳統消費者。

重金屬和黴菌毒素污染的風險

監管機構正在加強對植物性膳食補充劑中重金屬含量的監測,污染問題被認為是市場成長的主要障礙。近期研究發現,某些喜來芝補充劑中鉈的濃度高達0.5微克/克。長期接觸如此高濃度的鉈會導致嚴重的健康問題,包括潛在的神經系統損傷。美國食品藥物管理局(FDA)的「更接近零排放」(Closer to Zero)舉措旨在減少食品中的重金屬含量,並已製定了嚴格的執法標準。許多喜來芝生產商正努力維持合規性。研究表明,喜來芝含有約65種重金屬,包括鉛、砷、鎘和汞等有害物質。令人擔憂的是,其中一些金屬的含量超過了世界衛生組織(WHO)和FDA設定的允許限值。由於原料品質和重金屬含量因地區而異,區域差異進一步加劇了污染問題。監管力度的加強正推動產業轉型為擁有先進偵測能力和更優採購網路的生產商。另一方面,小規模企業往往缺乏健全的品管體系,面臨巨大的挑戰。

細分市場分析

到2025年,標準級喜來芝將佔據45.32%的市場佔有率,鞏固其在印度、東南亞和中東等價格敏感地區的強勢地位。在這些地區,消費者往往更注重價格而非臨床療效。標準級產品通常含有20-30%的富裡酸,並經過簡單的純化工藝,售價為每30天用量15-25美元。相較之下,優質級喜來芝預計到2031年將以9.51%的複合年成長率成長。這一快速成長主要得益於西方消費者和亞洲富裕城市居民對標準化活性成分濃度、重金屬檢測和臨床驗證的需求。 Natreon公司的取得專利的芝萃取物「PrimaVie」含有超過60%的富裡酸和超過50%的二苯並-α-吡喃酮,正逐漸成為優質配方的黃金標準。 Nootropics Depot和Purblack等知名品牌已在其旗艦產品中使用PrimaVie。此外,PrimaVie 的臨床試驗結果表明,該產品能夠改善粒線體 ATP 的產生和運動表現,符合高階消費者所要求的科學證據,並符合歐洲食品安全局 (EFSA) 法規 (EC) 1924/2006 的健康聲明標準。

在仿冒品氾濫的背景下,高階市場的成長不失為一種策略性解決方案。透過獲得第三方認證(如 NSF、USP、ISO 17025 等)、確保採購流程透明以及採用防篡改包裝,高階品牌正在開闢一個利基市場,其定價也因此比標準等級高出兩到三倍。 Purblack 將於 2025 年 10 月推出的「調查級喜來芝樹脂」正是這項「信任至上」策略的有力支撐,該產品清晰地標明了每批的 ICP-MS 分析結果和採集地點的 GPS 座標。歐洲市場的擴張尤其顯著,隨著傳統草藥(THR)核准流程的推進,預計到 2024 年,英國將有 178 項註冊核准。北美也呈現類似的趨勢,加州「65 號提案」對鉛攝取量的限制(每日 0.5 微克)實際上使得高階純化成為強制性要求。在亞太地區,由於阿育吠陀傳統和口碑傳播,標準等級產品仍將佔據銷售主導地位,但其市場佔有率預計將會萎縮。這項轉變的促進因素是收入成長和健康意識增強,消費者正轉向高階產品。

區域分析

到2025年,亞太地區將佔據61.02%的市場。這主要得益於印度作為喜馬拉雅山脈希拉吉特最大消費和採購中心的地位。隨著印度食品安全標準局(FSSAI)於2025年9月1日推出「阿育吠陀食品」(Ayurveda Ahara)許可類別,希拉吉特被重新歸類為膳食補充劑,從而可以透過超級市場和電商平台進行更廣泛的銷售。一項全國抽樣調查顯示,96%的都市區受訪者和95%的農村受訪者了解AYUSH(阿育吠陀、時代、奧義書、阿育吠陀)體系,約50%的受訪者每年至少花費100印度盧比購買AYUSH產品。中國正在崛起成為一個主要市場,傳統中醫從業者已將希拉吉特納入腎臟保健方案,儘管國家藥品監督管理局(NMPA)的監管障礙仍然存在。在日本,隨著都市區專業擴大尋求益智藥和適應原(如喜來芝)來緩解壓力,這個新興市場正在不斷成長。

預計到2031年,歐洲市場將以11.01%的複合年成長率成長,這主要得益於瑜伽的普及、阿育吠陀療法的被廣泛接受以及傳統草藥(THR)體系的建立。到2024年,英國將有178家註冊企業。德國和英國在推廣應用方面處於領先地位,消費者更傾向於選擇符合歐盟法規(EC) 1881/2006重金屬標準的認證有機和公平貿易的喜來芝。 2026年印度與歐盟的貿易協定將降低阿育吠陀產品的出口關稅,使Double和Vaidhyanath等印度品牌得以與歐洲老牌企業競爭。在義大利市場,將喜來芝納入綜合醫學專業人士的配方中,無疑是一大利好。同時,法國的BELFRIT清單既構成了准入壁壘,也緩解了符合標準的產品的競爭。英國藥品和保健產品監管署 (MHRA) 獨立監管草藥的註冊,這給被迫應對雙重合規要求的品牌帶來了更多複雜性。

受美國和加拿大市場的推動,隨著適應原和益智藥的日益普及,北美市場正在不斷擴張。根據美國FDA的《膳食補充劑健康與教育法案》(DSHEA),喜來芝被視為膳食補充劑,降低了市場准入門檻,但也導致仿冒品氾濫。加州65號提案對鉛含量進行監管,有利於高品質產品的銷售。加拿大天然健康產品管理局(NNHPD)要求上市前進行申報並提供安全證明,雖然減緩了產品進入市場的速度,但提高了其信譽度。南美、中東和非洲仍是新興市場,這主要得益於人們對天然健康解決方案日益成長的興趣以及Mercado Libre和Jumia等電商平台的興起。巴西國家衛生監督局(ANVISA)將喜來芝歸類為“新型食品”,需要上市前核准;而阿拉伯聯合大公國衛生和預防部已核准在杜拜和阿布扎比的藥店銷售部分喜來芝產品。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 隨著植物來源和純素食補充劑越來越受歡迎,喜來芝已成為一種天然替代品。

- 產品配方與形體的創新

- 受社群媒體影響,Z世代男性對健康的興趣日益濃厚。

- 電子商務通路的拓展

- 消費者對符合道德規範且潔淨標示的喜馬拉雅樹脂的需求日益成長。

- 全球整體健康養生實踐的興起以及瑜珈和阿育吠陀的傳播

- 市場限制因素

- 網路市場上假冒樹脂氾濫

- 雜質污染以及不受監管的參與企業市場等問題,都可能導致市場出現問題。

- 原料短缺和地理依賴

- 重金屬和黴菌毒素污染的風險

- 消費者需求分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按品質分級

- 標準級

- 優質級

- 按形式

- 樹脂

- 膠囊/片劑

- 粉末

- 其他

- 透過分銷管道

- 超級市場/大賣場

- 藥局/藥局

- 線上零售

- 其他零售商

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 德國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 亞太其他地區

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pure Himalayan Shilajit

- Purblack

- Dabur

- Baidyanath

- Nootropics Depot

- aSquared Nutrition

- ACTIZEET

- Angel Gummies

- Blisque

- CHOQ LLC

- Vedikroots

- Dorado Nutrition

- Elm & Rye

- Lotus Blooming Herbs

- Natural Shilajit

- Nootrum

- Pahadi Amrut

- Rasayanam Ayurveda

- Upakarma Ayurveda

- Sunfood

第7章 市場機會與未來展望

The Shilajit Market is projected to grow significantly, increasing from USD 202.44 million in 2025 to USD 221.12 million in 2026 and reaching USD 343.83 million by 2031, with a CAGR of 9.13% during 2026-2031.

This growth is fueled by rising demand for plant-based adaptogens, clearer regulatory frameworks for fulvic-acid-standardized formulas, and growing consumer interest in healthy aging. Heritage positioning continues to drive growth in the Asia-Pacific region, while clinical validation and clean-label claims are key factors influencing adoption in North America. Furthermore, innovations such as water-soluble powders and gummies have broadened the appeal of shilajit beyond its traditional resin form. Despite these advancements, the market faces quality-control challenges, highlighting the critical need for third-party testing and traceable sourcing to help brands secure a competitive advantage.

Global Shilajit Market Trends and Insights

Increasing popularity of plant-based and vegan supplements positions Shilajit as a natural alternative

Plant-based supplements are transforming the wellness industry as consumers increasingly prioritize transparency in ingredient sourcing, manufacturing processes, and product authenticity. Shilajit, a mineral-pitch resin naturally formed over centuries from decomposed plant matter, has gained prominence as a preferred option for vegan and vegetarian diets, offering a plant-based alternative to animal-derived supplements like collagen or fish oil. Packed with fulvic acid, trace minerals, and antioxidants, Shilajit supports energy production, immune function, and overall health, delivering benefits comparable to synthetic multivitamins. Its Ayurvedic heritage further enhances its appeal in markets where traditional and "natural" remedies are highly valued and often command a premium price. However, ensuring product purity is crucial, as adulteration with fillers or synthetic fulvic acid can undermine consumer trust and compromise its clean-label promise. To address these challenges and differentiate in a competitive market, third-party testing and certifications such as USDA Organic or Non-GMO Project Verified are becoming indispensable for building consumer confidence and trust.

Innovation in product formulations and formats

Shilajit is gaining popularity through innovative formats like gummies, liquid drops, and functional beverages, appealing to Gen-Z's preference for convenience, taste, and compatibility with their specialty diets. In 2024, brands such as Blisque and Angel Gummies launched Shilajit-infused gummies, masking the resin's bitterness with natural sweeteners and fruit extracts, while Purblack introduced its Research Grade Shilajit Resin in October 2025, standardized to >=60% fulvic acid and >=50% dibenzo-a-pyrones, targeting biohackers and performance athletes. Combination formulations are also gaining traction: Shilajit paired with ashwagandha addresses stress and energy in a single SKU, while Shilajit-turmeric blends target inflammation and joint health. Natreon's PrimaVie-a clinically studied, patented Shilajit extract-has become the ingredient of choice for premium brands seeking to substantiate efficacy claims with human trials, a move that aligns with the European Food Safety Authority's stringent health-claim regulations under Regulation (EC) 1924/2006. Advanced encapsulation technologies like liposomal and nanotechnology are improving bioavailability, though high costs limit their use to premium products. This evolution positions Shilajit as a versatile wellness platform, but brands must balance innovation with authenticity to retain traditional consumers who prefer resin as the authentic form.

Heavy metal and mycotoxin contamination risks

Regulatory agencies are intensifying their scrutiny of heavy metal levels in botanical supplements, spotlighting contamination concerns as a significant barrier to market growth. Recent studies have identified thallium concentrations of up to 0.5 µg/g in certain shilajit supplements. Extended exposure to these levels can lead to severe health repercussions, including potential neurological harm. The FDA's "Closer to Zero" initiative, designed to reduce heavy metals in food products, has introduced stringent enforcement benchmarks. Many manufacturers of shilajit grapple with consistent compliance. Research indicates that shilajit contains approximately 65 heavy metals, with dangerous ones like lead, arsenic, cadmium, and mercury present. Alarmingly, some of these metals exceed the permissible limits established by the WHO and the FDA. The contamination challenge is further complicated by geographic variability, as the quality of raw materials and their heavy metal profiles differ markedly across regions. This escalating regulatory scrutiny is pushing consolidation towards manufacturers with advanced testing capabilities and superior sourcing networks. Meanwhile, smaller players, often devoid of a robust quality control framework, encounter significant challenges.

Other drivers and restraints analyzed in the detailed report include:

- Social-media driven awareness in Gen-Z male wellness

- Expansion of e-commerce channels

- Adulteration and unregulated market players

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Standard Grade Shilajit captured a 45.32% market share, underscoring its stronghold in price-sensitive regions like India, Southeast Asia, and the Middle East. Here, consumers lean towards affordability over clinical validation. Typically, Standard-grade products, containing 20-30% fulvic acid and undergoing minimal purification, retail between USD 15-25 for a 30-day supply. In contrast, the Premium Grade is set to grow at a 9.51% CAGR through 2031. This surge is fueled by Western consumers and affluent urban Asians seeking standardized potency, heavy-metal testing, and clinical backing. Natreon's PrimaVie-a patented Shilajit extract boasting >=60% fulvic acid and >=50% dibenzo-a-pyrones-has emerged as the gold standard for premium formulations. Esteemed brands like Nootropics Depot and Purblack have integrated PrimaVie into their flagship offerings. Furthermore, PrimaVie's clinical trials, showcasing boosts in mitochondrial ATP production and exercise performance, align with the evidence premium consumers demand, meeting the European Food Safety Authority's health-claim standards under Regulation (EC) 1924/2006.

As counterfeit products proliferate, the premium segment's growth is a strategic countermeasure. By securing third-party certifications (like NSF, USP, and ISO 17025), ensuring transparent sourcing, and adopting tamper-evident packaging, premium brands carve out a niche that justifies prices 2-3 times higher than standard grades. Purblack's October 2025 debut of Research Grade Shilajit Resin, featuring batch-specific ICP-MS test results and GPS coordinates of collection sites, underscores this trust-centric strategy. Europe's expansion is notable, with the Traditional Herbal Medicinal Product (THR) pathway granting 178 registrations in the UK by 2024. North America mirrors this trend, as California's Proposition 65 lead limits (set at 0.5 micrograms per day) effectively necessitate premium-grade purification. While Standard grade will continue to lead in volume across Asia Pacific-thanks to Ayurvedic traditions and word-of-mouth endorsements-its market share is poised to dwindle. This shift is driven by rising incomes and heightened health awareness, steering consumers towards premium options.

The Shilajit Market Report is Segmented by Grade/Quality (Standard Grade, Premium Grade), Form (Resin, Capsules/Tablets, Powder, Others), Distribution Channel (Supermarkets/Hypermarkets, Pharmacies and Drugstores, Online Retail, Other Retail Distributors), and Geography (North America, Europe, Asia Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia Pacific held a 61.02% market share, driven by India's role as the largest consumer and sourcing hub for Himalayan Shilajit. The Food Safety and Standards Authority of India's "Ayurveda Aahara" licensing category, introduced on September 1, 2025, reclassified Shilajit as a food supplement, enabling broader distribution through supermarkets and e-commerce. A National Sample Survey revealed that 96% of urban and 95% of rural respondents were aware of AYUSH systems, with nearly 50% spending at least INR 100 annually on AYUSH products. China is emerging as a key market, with traditional Chinese medicine practitioners incorporating Shilajit into kidney health formulations, though regulatory hurdles with the National Medical Products Administration persist. Japan's nascent market is growing as urban professionals seek nootropics and adaptogens like Shilajit to manage stress.

Europe is projected to grow at an 11.01% CAGR through 2031, driven by yoga's mainstreaming, Ayurveda's acceptance, and the Traditional Herbal Medicinal Product (THR) pathway, which enabled 178 registrations in the UK by 2024. Germany and the UK lead adoption, with consumers favoring certified organic, fair-trade Shilajit that meets EU heavy-metal limits under Regulation (EC) 1881/2006. The 2026 India-EU trade agreement reduced tariffs on Ayurvedic exports, allowing Indian brands like Dabur and Baidyanath to compete with European incumbents. Italy's market benefits from integrative medicine practitioners prescribing Shilajit, while France's BELFRIT list creates entry barriers but reduces competition for compliant products. Post-Brexit, the UK's MHRA independently regulates herbal-medicine registrations, adding complexity for brands navigating dual compliance.

North America, led by the U.S. and Canada, is expanding as adaptogens and nootropics gain popularity. The U.S. FDA's DSHEA framework treats Shilajit as a supplement, lowering entry barriers but enabling counterfeit proliferation, while California's Proposition 65 lead limits favor premium-grade products. Canada's NNHPD requires pre-market notification and safety evidence, slowing entry but enhancing trust. South America and the Middle East & Africa remain nascent markets, with growing interest in natural wellness solutions and e-commerce platforms like Mercado Libre and Jumia driving demand. Brazil's ANVISA classifies Shilajit as a novel food requiring pre-market authorization, while the UAE's Ministry of Health and Prevention has approved select products for pharmacy distribution in Dubai and Abu Dhabi.

- Pure Himalayan Shilajit

- Purblack

- Dabur

- Baidyanath

- Nootropics Depot

- aSquared Nutrition

- ACTIZEET

- Angel Gummies

- Blisque

- CHOQ LLC

- Vedikroots

- Dorado Nutrition

- Elm & Rye

- Lotus Blooming Herbs

- Natural Shilajit

- Nootrum

- Pahadi Amrut

- Rasayanam Ayurveda

- Upakarma Ayurveda

- Sunfood

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing popularity of plant-based and vegan supplements positions Shilajit as a natural alternative

- 4.2.2 Innovation in product formulations and formats

- 4.2.3 Social-media driven awareness in Gen-Z male wellness

- 4.2.4 Expansion of e-commerce channels

- 4.2.5 Rising demand for clean-label, ethically sourced Himalayan resins

- 4.2.6 Surge in holistic wellness practices and yoga/Ayurveda adoption worldwide

- 4.3 Market Restraints

- 4.3.1 Counterfeit resin proliferation on online marketplaces

- 4.3.2 Adulteration and unregulated market players

- 4.3.3 Raw material scarcity and geographic dependence

- 4.3.4 Heavy metal and mycotoxin contamination risks

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade/Quality

- 5.1.1 Standard Grade

- 5.1.2 Premium Grade

- 5.2 By Form

- 5.2.1 Resin

- 5.2.2 Capsules/Tablets

- 5.2.3 Powder

- 5.2.4 Others

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Pharmacies and Drugstores

- 5.3.3 Online Retail

- 5.3.4 Other Retail Distributors

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Pure Himalayan Shilajit

- 6.4.2 Purblack

- 6.4.3 Dabur

- 6.4.4 Baidyanath

- 6.4.5 Nootropics Depot

- 6.4.6 aSquared Nutrition

- 6.4.7 ACTIZEET

- 6.4.8 Angel Gummies

- 6.4.9 Blisque

- 6.4.10 CHOQ LLC

- 6.4.11 Vedikroots

- 6.4.12 Dorado Nutrition

- 6.4.13 Elm & Rye

- 6.4.14 Lotus Blooming Herbs

- 6.4.15 Natural Shilajit

- 6.4.16 Nootrum

- 6.4.17 Pahadi Amrut

- 6.4.18 Rasayanam Ayurveda

- 6.4.19 Upakarma Ayurveda

- 6.4.20 Sunfood