|

市場調查報告書

商品編碼

2043911

歐洲塑合板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Particle Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

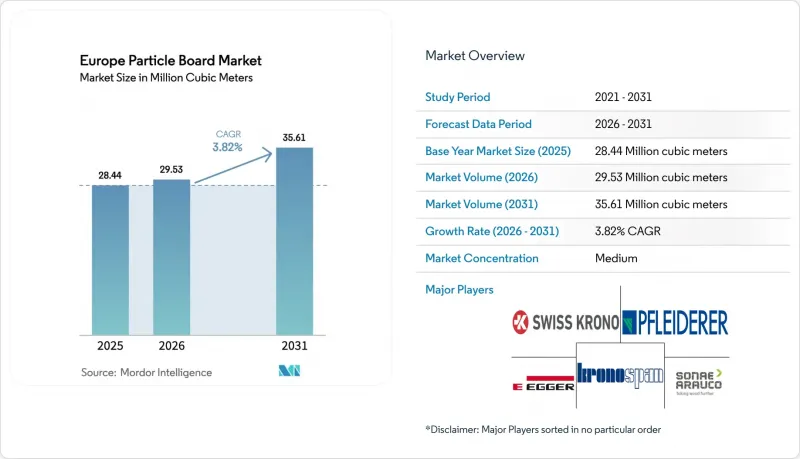

歐洲塑合板市場預計將從 2025 年的 2,844 萬立方米和 2026 年的 2,953 萬立方米成長到 2031 年的 3,561 萬立方米,2026 年至 2031 年的年複合成長率(CAGR)為 3.82%。

強制性低揮發性有機化合物(VOC)法規、強制使用再生木材以及對尿素基黏合劑徵收碳稅,正在重塑成本結構,促使大型垂直整合企業加快開發回收設施並試點部署生物基黏合劑。在德國,一系列木造住宅計畫正在推動需求成長,而斯堪的納維亞半島的鋸木廠則利用森林所有權和熱電聯產電廠來降低原料和能源風險。西姆巴坎普和迪芬巴赫的AI最佳化壓機生產線帶來了兩位數的效率提升,但對於那些自動化預算不足1000萬至1500萬歐元的鋸木廠而言,運營成本差距正在擴大。由於顆粒廠的需求以及CLT(交錯層壓木材)廢料的再利用,鋸末供應嚴重短缺,導致奧地利現貨價格居高不下,超過每噸120歐元,這刺激了人們嘗試使用農業殘餘物作為替代纖維。

歐洲塑合板市場趨勢與洞察

歐盟更嚴格的甲醛法規正在推動超低VOC板材的發展。

歐盟法規2023/1464規定,木質板材的排放上限為0.062毫克/立方米,該法規將於2026年8月6日生效,迫使製造商更改其黏合劑配方或退出市場。德國於2020年採納了DIN EN 16516標準,並給予國內鋸木廠六年的檢驗期。與此同時,南歐和東歐的許多競爭對手正爭相建立實驗室並獲得EN 717-1認證。歐洲化學品管理局(ECHA)於2025年5月發布的指南強制要求進行實驗室測試,而非供應商聲明,這將使中小企業每條產品線的合規成本增加5萬至8萬歐元。在 Metsä Fiber 的 Arnekoski 示範工廠進行試點的木質素改質樹脂,雖然比脲醛樹脂貴 15-20%,但其作為無甲醛板材的潛力繼續吸引研發資金。

利用再生木材作為原料擴大生產能力

2024年,Sonae Arauco使用了80.9萬噸再生木材,再生木材含量達33%。該公司還計劃在2025年底,在部分工廠將再生木材含量提升至75%。 EGGER投資2億歐元的Markt Bibart回收中心,由Timberpak的都市區回收網路供料,於2025年夏季開始營運。同時,Kronospan Luxembourg於2024年6月生產了首批100%再生木板。在德國和奧地利,市政當局對拆除木材的競標日益激烈,而由於甲蟲災害和乾旱導致本地雲杉供應減少,沒有合約的工廠面臨材料短缺的風險。

能源價格波動給印刷生產線的利潤率帶來了壓力。

2025年2月,德國顆粒燃料價格較上季上漲19%,達到每噸363.21歐元。這進一步推高了板材壓製過程中的能源成本,該過程每立方公尺板材的耗電量已達150-200千瓦時。目前,能源成本佔生產成本的比例高達18%,對於無法透過合約對沖這部分成本的鋸木廠而言,這將使其息稅折舊攤提前利潤(EBITDA)下降2-3個百分點。

細分市場分析

儘管到2025年,木質原料仍佔歐洲塑合板產量的57.83%,但歐洲塑合板市場正轉向使用再生材料。 Sonae Arauco公司2024年33%的再生材料使用率以及EGGER公司位於Markt Bibad的工廠都反映了這一成長趨勢。甘蔗渣(甘蔗殘渣)目前仍屬於小眾產品,但地中海地區的鋸木廠正在試驗將甘蔗殘渣在低於150 度C的壓榨溫度下進行混合,預計在預測期(2026-2031年)內將實現4.23%的複合年成長率。每年約640萬噸的釀酒廢穀物供應提供了更多選擇,但其高含水量和物流方面的挑戰仍然存在。由於大規模的樹皮甲蟲災害加劇了本地雲杉的短缺,奧地利鋸末價格已超過每噸120歐元,從而支撐了再生木材的溢價。

隨著歐洲塑合板市場擴張,廢料供應日益緊張,那些擁有可靠廢木材來源的生產商正獲得對沖價值。弗勞恩霍夫應用物理研究所 (Fraunhofer IAP) 的 ReSpan 計畫表明,完全使用廢木材生產塑合板無需粘合劑,這預示著未來鋸木廠可以徹底擺脫原木纖維和尿素。隨著循環經濟配額的日益嚴格,那些在都市區競標拆除木材採購或將農業纖維混合物商業化的企業將能夠獲得利潤優勢。

《歐洲塑合板市場報告》依原料(木材、甘蔗渣及其他原料)、應用領域(家具、建築、基礎設施、包裝及其他)和地區(德國、英國、法國、義大利、西班牙、俄羅斯、北歐國家及其他歐洲國家)進行細分。市場預測以體積(立方米)為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟更嚴格的甲醛法規(EN 16516)推動了對超低 VOC 板材的需求增加。

- 利用再生木材作為原料擴大生產能力

- 預製住宅和異地建造的普及

- 歐盟的CBAM積分制度有利於碳含量較低的太陽能板。

- 人工智慧最佳化後的沖壓生產線可降低 20% 的能耗並提高生產能力。

- 市場限制因素

- 能源價格波動給印刷生產線的利潤率帶來了壓力。

- 由於對 CLT/LVL 的需求,用於自有品牌 (PB) 的木材殘渣正在被使用。

- 強制揭露 EPD(費用百分比)增加了中小企業的合規成本。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按成分

- 木頭

- 渣

- 其他原料

- 透過使用

- 家具

- 建造

- 基礎設施

- 包裝

- 其他

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Action TESA Europe

- arauco

- Boise Cascade

- CFP

- EGGER Group

- FALCO

- Finsa

- Kastamonu Entegre

- Kronospan Ltd.

- Norbord Europe Ltd.

- Orlimex UK Ltd.

- Peter Benson(Plywood)Ltd.

- Pfleiderer

- SAUERLAND Spanplatte

- Sonae Arauco(UK)Ltd

- SWISS KRONO Group

- Swiss Krono Holding AG

- Unilin Division Panels

- Wanhua Ecoboard Co. Ltd.

- West Fraser

第7章 市場機會與未來展望

The Europe Particle Board Market size is projected to expand from 28.44 million cubic meters in 2025 and 29.53 million cubic meters in 2026 to 35.61 million cubic meters by 2031, registering a CAGR of 3.82% between 2026 to 2031.

Mandatory low-VOC (Volatile Organic Compound) rules, recycled-wood mandates, and carbon-pricing of urea adhesives are redefining cost structures, prompting vertically integrated leaders to accelerate recycling hubs and bio-based binder pilots. Germany anchors demand with serial timber-housing programs, while Nordic mills leverage forest ownership and combined-heat-and-power plants to cushion feedstock and energy risk. AI-optimized press lines from Siempelkamp and Dieffenbacher deliver double-digit efficiency gains, but mills lacking EUR 10-15 million automation budgets face widening operating-cost gaps. Tight sawdust supply, exacerbated by pellet-mill demand and CLT (Cross-Laminated Timber) off-cut diversion, continues to lift Austria's spot price above EUR 120/ton, spurring experiments with agricultural residues as substitute fibers.

Europe Particle Board Market Trends and Insights

Tightening EU Formaldehyde Limits Driving Ultra-Low-VOC Boards

EU Regulation 2023/1464 fixes a 0.062 mg/m3 ceiling for emissions from wood-based panels effective August 6, 2026, compelling adhesive reformulations or market exit. Germany adopted DIN EN 16516 back in 2020, giving domestic mills a six-year validation lead time, whereas many Southern and Eastern counterparts now rush to install test chambers and attain EN 717-1 certification. ECHA (European Chemicals Agency) guidelines published in May 2025 mandate chamber testing over supplier declarations, adding EUR 50,000-80,000 to SME (Small and Medium Enterprises) compliance per product line. Lignin-modified resins piloted at Metsa Fibre's Aanekoski demo plant remain 15-20% costlier than urea-formaldehyde, yet the promise of formaldehyde-free boards continues to attract R&D (research and development) budgets.

Capacity Expansions Using Recycled-Wood Feedstock

Sonae Arauco valorised 809,000 tons of recycled wood in 2024, achieving 33% incorporation, and targets 75% in selected mills by end-2025. EGGER's EUR 200 million Markt Bibart hub, supplied by Timberpak's urban-collection network, started recycling operations in summer 2025, while Kronospan Luxembourg produced the first 100% recycled-wood board in June 2024. Municipal tenders for demolition wood across Germany and Austria intensify competition; mills without contracts risk shortages as beetle damage and drought curb virgin spruce supply.

Energy-Price Volatility Squeezing Press-Line Margins

German pellet prices climbed 19% month-on-month to EUR 363.21 t in February 2025, raising press energy cost on boards that already consume 150-200 kWh/m3. Energy now accounts for up to 18% of production cost, trimming EBITDA by two to three points for mills unable to hedge contracts.

Other drivers and restraints analyzed in the detailed report include:

- Prefabricated Timber Housing and Off-Site Construction Uptake

- EU CBAM Credits Favouring Low-Embodied-Carbon Panels

- CLT/LVL Demand Diverting Wood Residues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood-based feedstock retained 57.83% of volume in 2025, but the Europe Particle Board market is pivoting toward recycled streams. Sonae Arauco's 33% recycled share in 2024 and EGGER's Markt Bibart hub demonstrate scaling momentum. Bagasse occupies a niche yet is forecast at 4.23% CAGR during the forecast period (2026-2031), as Mediterranean mills trial sugarcane residue blends at press temperatures below 150°C. Brewer's spent grain volumes near 6.4 million tons/year offer further optionality, although high moisture and logistics hurdles persist. Virgin spruce scarcity, exacerbated by bark-beetle outbreaks, keeps Austria's sawdust above EUR 120 per ton, underpinning recycled-wood premiums.

Producers capturing post-consumer wood streams gain hedge value as Europe Particle Board market size expansion tightens residue supply. Fraunhofer IAP's ReSpan project proved binder-free, 100% waste-wood boards feasible, hinting at a future in which mills decouple from virgin fiber and urea entirely. Operators that secure municipal demolition-wood tenders or commercialize agri-fiber recipes will lock in a margin advantage as circular-economy quotas tighten.

The Europe Particle Board Market Report is Segmented by Raw Material (Wood, Bagasse, and Other Raw Materials), Application (Furniture, Construction, Infrastructure, Packaging, and Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, NORDIC Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Cubic Meters).

List of Companies Covered in this Report:

- Action TESA Europe

- arauco

- Boise Cascade

- CFP

- EGGER Group

- FALCO

- Finsa

- Kastamonu Entegre

- Kronospan Ltd.

- Norbord Europe Ltd.

- Orlimex UK Ltd.

- Peter Benson (Plywood) Ltd.

- Pfleiderer

- SAUERLAND Spanplatte

- Sonae Arauco (UK) Ltd

- SWISS KRONO Group

- Swiss Krono Holding AG

- Unilin Division Panels

- Wanhua Ecoboard Co. Ltd.

- West Fraser

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening European Union formaldehyde limits (EN 16516) driving ultra-low-VOC boards

- 4.2.2 Capacity expansions using recycled-wood feedstock

- 4.2.3 Prefabricated timber housing and off-site construction uptake

- 4.2.4 EU CBAM credits favouring low-embodied-carbon panels

- 4.2.5 AI-optimised press lines cutting energy 20 % and boosting capacity

- 4.3 Market Restraints

- 4.3.1 Energy-price volatility squeezing press-line margins

- 4.3.2 CLT/LVL demand diverting wood residues from PB

- 4.3.3 Mandatory EPD disclosure raising SME compliance cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Wood

- 5.1.2 Bagasse

- 5.1.3 Other Raw Materials

- 5.2 By Application

- 5.2.1 Furniture

- 5.2.2 Construction

- 5.2.3 Infrastructure

- 5.2.4 Packaging

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Action TESA Europe

- 6.4.2 arauco

- 6.4.3 Boise Cascade

- 6.4.4 CFP

- 6.4.5 EGGER Group

- 6.4.6 FALCO

- 6.4.7 Finsa

- 6.4.8 Kastamonu Entegre

- 6.4.9 Kronospan Ltd.

- 6.4.10 Norbord Europe Ltd.

- 6.4.11 Orlimex UK Ltd.

- 6.4.12 Peter Benson (Plywood) Ltd.

- 6.4.13 Pfleiderer

- 6.4.14 SAUERLAND Spanplatte

- 6.4.15 Sonae Arauco (UK) Ltd

- 6.4.16 SWISS KRONO Group

- 6.4.17 Swiss Krono Holding AG

- 6.4.18 Unilin Division Panels

- 6.4.19 Wanhua Ecoboard Co. Ltd.

- 6.4.20 West Fraser

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

塑合板市場規模、佔有率、趨勢和預測:按應用、行業和地區分類,2026-2034年日本塑合板市場規模、佔有率、趨勢和預測:按應用、行業和地區分類,2026-2034年

塑合板市場規模、佔有率、趨勢和預測:按應用、行業和地區分類,2026-2034年日本塑合板市場規模、佔有率、趨勢和預測:按應用、行業和地區分類,2026-2034年 2026年全球塑合板市場報告

2026年全球塑合板市場報告 塑合板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

塑合板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 塑合板市場規模、佔有率和成長分析(按原料、產品類型、安裝方式、應用、最終用途產業和地區分類)-2026-2033年產業預測

塑合板市場規模、佔有率和成長分析(按原料、產品類型、安裝方式、應用、最終用途產業和地區分類)-2026-2033年產業預測 塑合板市場-全球產業規模、佔有率、趨勢、機會和預測,按原料(木材、甘蔗渣、其他)、應用(建築、家具、基礎設施、其他)、地區、競爭細分,2020-2030 年預測

塑合板市場-全球產業規模、佔有率、趨勢、機會和預測,按原料(木材、甘蔗渣、其他)、應用(建築、家具、基礎設施、其他)、地區、競爭細分,2020-2030 年預測 塑合板市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測

塑合板市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測 全球塑合板市場

全球塑合板市場 全球塑合板市場(2024-2028)

全球塑合板市場(2024-2028) 塑合板市場(產品類型:裸板和層壓塑合板;最終用途:住宅、商業和工業)- 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢和預測

塑合板市場(產品類型:裸板和層壓塑合板;最終用途:住宅、商業和工業)- 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢和預測