|

市場調查報告書

商品編碼

2043884

美國碳酸鈣市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)United States Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

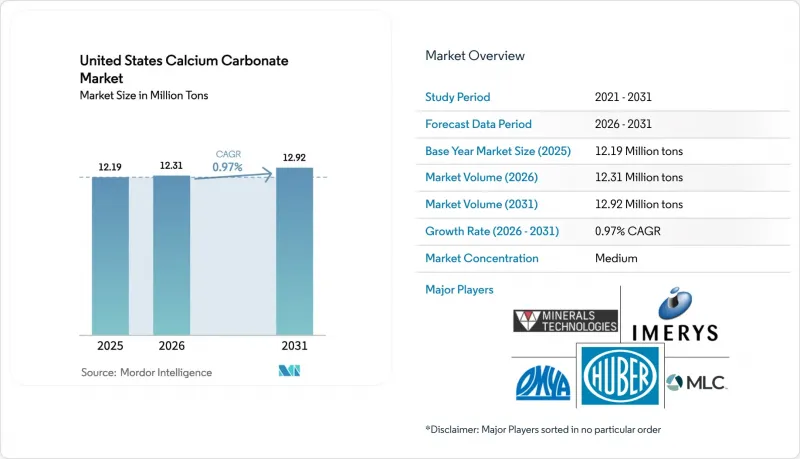

美國碳酸鈣市場預計將從 2025 年的 1,219 萬噸成長到 2026 年的 1,231 萬噸,然後從 2026 年到 2031 年以 0.97% 的複合年成長率成長,到 2031 年達到 1,292 萬噸。

儘管近期銷售成長較為溫和,但就價值創造而言,市場正顯著轉向碳捕獲衍生的沉澱碳酸鈣 (PCC) 和超細特種級產品,這兩類產品均以高價交易。研磨碳酸鈣 (GCC) 仍然主導著大量混凝土和骨材市場。然而,造紙廠安裝的現場 PCC 生產設施以及新興的碳捕獲與利用 (CCU) 設施正在拓展利潤來源,同時減少運輸排放。受聯邦政府《基礎設施投資與就業法案》(IIJA) 的推動,基礎設施項目給石灰石供應鏈帶來了壓力,迫使加工商轉向性能更高的 PCC 產品。在塗料和塑膠產業,混料商正在增加配方中碳酸鈣的用量,以抵消二氧化鈦和聚合物結構性成本的上漲,從而增強需求的韌性。此外,對可吸入結晶二氧化矽監管力度的加大,推動了採石場粉塵控制方面的投資,使無塵合成 PCC 獲得了競爭優勢。

美國碳酸鈣市場趨勢與洞察

油漆和塗料需求不斷成長

為應對二氧化鈦價格持續高企,塗料生產商正在提高油漆和塗料中碳酸鈣填料的比例。這一趨勢的驅動力在於油漆和塗料市場已成為業界成長最快的市場。通貨膨脹控制和就業法案(IIJA)的大部分撥款流向了公路信託基金,這進一步刺激了橋樑、高架公路和機場設施對防護塗料的需求。供應商正在提升其亞微米級研磨能力,並投資於硬脂酸基表面改質技術,以滿足高性能建築塗料嚴格的流變性能要求。超細和表面處理級的填料能夠改善分散性並降低黏度,從而在不影響塗層強度的前提下提高填料含量。這種替代趨勢在經濟型配方中尤其顯著,因為提高填料含量可以降低原料成本。

造紙和包裝產業的成長

數十年來,PCC衛星工廠的整合使造紙業成為最大的消費產業,其中現場PCC生產佔據了普通紙張的很大一部分。 Domtal位於威斯康辛州Nekosa的工廠從一家於2024年運作的衛星工廠獲得原料供應,並通過聯合位置策略,成功降低了年度碳排放,並顯著縮短了卡車運輸距離。雖然印刷用紙的需求正在下降,但箱板紙和EC包裝材料的需求卻在成長,這得益於碳酸鈣塗層增強了瓦楞紙箱的印刷性能。擁有眾多全球衛星工廠的Minerals Technologies公司正在加大對新興亞太市場的投資,顯示北美市場已趨於成熟。然而,國內造紙企業正在加強對PCC粒徑的控制,以贏得高亮度特種包裝材料的訂單,從而確保穩定的需求。

與滑石粉、高嶺土和合成填料的競爭。

由於滑石粉具有優異的耐熱性和尺寸穩定性,因此是聚丙烯汽車零件的首選填料。另一方面,高嶺土因其高白度而在紙張塗料這一細分市場備受青睞。沉澱二氧化矽和氧化鋁填料在高光澤塑膠和耐刮塗料領域也日益普及。複合材料設計師擴大在新塑膠配方中混合滑石粉和碳酸鈣,以提高塑膠的剛性和抗衝擊性。在塗料領域,合成二氧化矽基消光劑在高階木紋塗料的應用中正挑戰碳酸鈣的地位,但由於成本因素,其應用受到限制。區域供應鏈發揮著至關重要的作用。滑石粉主要產自蒙大拿州和德克薩斯州,而碳酸鈣則在全美範圍內均有供應,這使其在許多大規模生產應用中具有運輸成本優勢。

細分市場分析

2025年,磨細碳酸鈣(GCC)佔據市場主導地位,佔總量的75.69%。例如,密西根州的Port Calcite公司每年透過湖上貨輪運輸數百萬噸GCC,為中西部水泥和骨材產業的客戶提供低價產品。同時,沉澱碳酸鈣(PCC)雖然市佔率較小,但其產量呈現上升趨勢,在2026年至2031年的預測期間內,年複合成長率(CAGR)將達到2.26%。這一成長主要得益於造紙廠附近衛星工廠的興起以及各種碳捕獲與利用(CCU)計畫的開展。儘管基數較小,但美國PCC市場正呈現穩定上升的動能。 CarbonFree公司的Gary Works專案不僅捕獲二氧化碳,還將其作為高品質的食品級PCC出售。這項策略符合45Q獎勵,並凸顯了碳捕獲與利用的變革潛力。 Fortera 和 Graymont 的 ReAct夥伴關係正在推出球霰石 PCC,這是一種潛在的水泥水泥熟料替代品,旨在滿足日益成長的綠色混凝土需求。然而,供應鏈面臨許多挑戰。二氧化碳捕獲、純化和液化過程會增加資本投入。幸運的是,聯邦津貼和各州的總量管制與交易額度正在幫助其與開採的綠色水泥熟料 (GCC) 實現公平競爭。

因其粒徑細小、純度高且形態可客製化,商業化生產的聚晶碳酸鹽 (PCC) 價格高於通用型穀蛋白碳酸鹽 (GCC)。這導致食品、製藥和高光塗料等產業對 PCC 的需求旺盛。同時,用於生產超細 GCC 的研磨工藝不斷改進,推高了 GCC 的平均單價,尤其是在霧面建築塗料領域。在數位印刷紙和低 VOC 水性塗料領域,混合填料系統正在興起,其中超細 GCC 提供填充量,而 PCC 則增強遮蓋力和白度。儘管 GCC 預計仍將保持其銷售優勢,但 PCC 的獨特優勢以及碳酸鈣利用率 (CCU) 的提高有望彌合美國碳酸鈣市場傳統的價格性能差距。

《美國碳酸鈣市場報告》按類型(粉狀碳酸鈣和沈澱狀碳酸鈣)和終端用途行業(造紙、塑膠、黏合劑和密封劑、油漆和塗料以及其他終端用途行業)進行細分。市場預測以數量(噸)為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 油漆和塗料行業的需求增加。

- 造紙和包裝產業的成長

- 塑膠產業中碳酸鈣填料的應用

- 美國基礎設施投資(IIJA)正在提振對海灣合作理事會(GCC)的需求。

- 現場生產PCC採用碳捕獲與利用(CCU)

- 市場限制因素

- 吸入碳酸鈣粉塵造成的健康損害

- 與滑石粉、高嶺土和合成填料的競爭

- 美國對採石和排放更嚴格的監管

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

- 礦井位置

第5章 市場規模與成長預測

- 按類型

- 細粉狀碳酸鈣

- 沉澱碳酸鈣

- 按最終用途行業分類

- 紙

- 塑膠

- 黏合劑和密封劑

- 油漆和塗料

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Blue Mountain Minerals

- Carmeuse

- Cerne Calcium Company

- Chememan Public Company Limited.

- CIMBAR RESOURCES, INC.

- Columbia River Carbonates

- GLC Minerals LLC

- Graymont

- ILC Resources

- Imerys

- JM Huber Corporation

- Lhoist

- Minerals Technologies Inc.

- Mississippi Lime Company

- Newpark Resources Inc.

- Omya AG

- Sibelco

- The Cary Company

第7章 市場機會與未來展望

The United States Calcium Carbonate Market size is expected to grow from 12.19 million tons in 2025 to 12.31 million tons in 2026 and is forecast to reach 12.92 million tons by 2031 at 0.97% CAGR over 2026-2031.

Recent growth in volume terms has been modest, but there is a notable shift in value creation towards carbon-capture-derived precipitated calcium carbonate (PCC) and ultrafine specialty grades, both commanding premium pricing. Ground calcium carbonate (GCC) continues to dominate high-tonnage concrete and aggregate outlets. However, on-site PCC satellites at paper mills, along with emerging CCU facilities, are expanding the profit pool while cutting down transport emissions. Infrastructure projects, bolstered by the federal Infrastructure Investment and Jobs Act (IIJA), are tightening limestone supply chains, nudging converters towards higher-performance PCC grades. In the paints and plastics sector, formulators have increased calcium carbonate loadings to offset the structurally elevated costs of titanium dioxide and polymers, thus strengthening demand resilience. Moreover, heightened regulatory scrutiny on respirable crystalline silica is driving dust-suppression investments at quarries, giving a competitive edge to dust-free synthetic PCC.

United States Calcium Carbonate Market Trends and Insights

Rising Demand for Paints and Coatings

Formulators are increasing calcium carbonate extender ratios in paints and coatings to counteract persistently high titanium dioxide prices. This move comes as paints and coatings emerge as the fastest-growing outlet in the industry. A significant portion of the IIJA's allocation is directed to the Highway Trust Fund, boosting demand for protective coatings on bridges, overpasses, and airport facilities. Suppliers are ramping up sub-2 micron grinding capacity and investing in stearic-acid surface modification to achieve stringent rheology targets in high-performance architectural paints. Ultrafine and surface-treated grades enhance dispersion and reduce viscosity, allowing for greater filler loading without compromising film integrity. Notably, this substitution trend is pronounced in value-tier formulations, where increased extender levels lead to reduced raw-material costs.

Growth in the Paper and Packaging Industry

Thanks to decades of integrating PCC satellites, paper remains the dominant consumer, with on-site PCC constituting a substantial portion of a typical sheet. Domtar's Nekoosa Mill in Wisconsin, fed by a satellite launched in 2024, has successfully reduced carbon emissions annually and avoided significant trucking miles through its co-location strategy. While graphic paper has seen a decline, containerboard and e-commerce packaging are on the rise, bolstered by calcium carbonate coatings that enhance printability on corrugated boxes. Minerals Technologies, with numerous satellites globally, is channeling more capital into emerging Asia-Pacific, hinting at a maturing North American base. Yet, domestic mills are enhancing PCC particle-size control to compete for high-brightness specialty packaging orders, ensuring steady demand.

Competition from Talc, Kaolin, and Synthetic Fillers

Thanks to its superior heat resistance and dimensional stability, talc has become the preferred choice for polypropylene automotive parts. Kaolin, with its brightness advantage, is preferred in paper-coating niches. Meanwhile, precipitated silica and alumina fillers are gaining traction in high-gloss plastics and scratch-resistant coatings. Formulators are increasingly blending talc with calcium carbonate in new plastic recipes to enhance stiffness and impact properties. In the coatings sector, while synthetic silica matting agents challenge calcium carbonate in premium wood finishes, cost considerations limit their widespread adoption. Regional supply chains play a pivotal role: talc is mainly sourced from Montana and Texas, while calcium carbonate's nationwide availability offers a freight advantage in numerous high-volume applications.

Other drivers and restraints analyzed in the detailed report include:

- Plastics Industry Adoption of CaCO3 Fillers

- United States Infrastructure Spending (IIJA) Boosting GCC Demand

- Stricter United States Quarrying and Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Ground Calcium Carbonate (GCC) dominated the market, accounting for 75.69% of the total volume. For example, Michigan's Port Calcite ships millions of tons annually via lake freighters, achieving low unit costs for clients in the Midwest cement and aggregate sectors. While Precipitated Calcium Carbonate (PCC) holds a smaller market share, its output is on the rise, growing at a 2.26% CAGR through the forecast period of 2026-2031. This growth is fueled by the emergence of satellite plants near paper mills and various CCU projects. Even though starting from a smaller base, the U.S. market for PCC is on a steady upward trajectory. CarbonFree's Gary Works project is not only capturing CO2 but also marketing it as premium food-grade PCC. This strategy aligns with 45Q incentives and highlights CCU's transformative potential. Fortera and Graymont's ReAct partnership is introducing vaterite PCC, which can serve as a partial substitute for cement clinker, addressing the increasing demand for green concrete. However, the supply chain faces hurdles: the processes of capturing, purifying, and liquefying CO2 elevate capital expenditures. Fortunately, federal grants and state cap-and-trade credits are helping to level the playing field with mined GCC.

Commercial-scale PCC, known for its finer particle size, elevated purity, and customizable morphology, commands a premium over commodity GCC. This makes it highly desirable in sectors such as food, pharmaceuticals, and high-gloss coatings. Meanwhile, upgraded grinding circuits producing ultrafine GCC are enhancing GCC's average unit value, especially in matte architectural coatings. In the realm of digital-print papers and low-VOC water-based paints, hybrid filler systems are emerging. Here, ultrafine GCC provides volume, while PCC contributes opacity or brightness. While GCC is likely to retain its volume leadership, the distinct advantages of PCC and the benefits from CCU are set to bridge the historical price-to-performance gap in the U.S. calcium carbonate market.

The United States Calcium Carbonate Market Report is Segmented by Type (Ground Calcium Carbonate and Precipitated Calcium Carbonate), and End-User Industry (Paper, Plastic, Adhesive and Sealant, Paints and Coatings, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Blue Mountain Minerals

- Carmeuse

- Cerne Calcium Company

- Chememan Public Company Limited.

- CIMBAR RESOURCES, INC.

- Columbia River Carbonates

- GLC Minerals LLC

- Graymont

- ILC Resources

- Imerys

- J.M. Huber Corporation

- Lhoist

- Minerals Technologies Inc.

- Mississippi Lime Company

- Newpark Resources Inc.

- Omya AG

- Sibelco

- The Cary Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rising demand from paints and coatings

- 4.1.2 Growth in paper and packaging industry

- 4.1.3 Plastics industry adoption of CaCO3 fillers

- 4.1.4 United States infrastructure spending (IIJA) boosting GCC demand

- 4.1.5 On-site PCC produced via carbon-capture utilization

- 4.2 Market Restraints

- 4.2.1 Health hazards from respirable CaCO3 dust

- 4.2.2 Competition from talc, kaolin and synthetic fillers

- 4.2.3 Stricter United States quarrying and emission regulations

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

- 4.5 Mine Locations

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Ground Calcium Carbonate

- 5.1.2 Precipitated Calcium Carbonate

- 5.2 By End-user Industry

- 5.2.1 Paper

- 5.2.2 Plastic

- 5.2.3 Adhesive and Sealant

- 5.2.4 Paints and Coatings

- 5.2.5 Other End-User Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Blue Mountain Minerals

- 6.4.2 Carmeuse

- 6.4.3 Cerne Calcium Company

- 6.4.4 Chememan Public Company Limited.

- 6.4.5 CIMBAR RESOURCES, INC.

- 6.4.6 Columbia River Carbonates

- 6.4.7 GLC Minerals LLC

- 6.4.8 Graymont

- 6.4.9 ILC Resources

- 6.4.10 Imerys

- 6.4.11 J.M. Huber Corporation

- 6.4.12 Lhoist

- 6.4.13 Minerals Technologies Inc.

- 6.4.14 Mississippi Lime Company

- 6.4.15 Newpark Resources Inc.

- 6.4.16 Omya AG

- 6.4.17 Sibelco

- 6.4.18 The Cary Company

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

食品級碳酸鈣市場規模、佔有率和成長分析:按類型、應用、終端用戶產業和地區分類-2026-2033年產業預測

食品級碳酸鈣市場規模、佔有率和成長分析:按類型、應用、終端用戶產業和地區分類-2026-2033年產業預測 碳酸鈣市場:依類型、等級、形態、原料、純度、應用及通路分類-2026-2032年全球市場預測

碳酸鈣市場:依類型、等級、形態、原料、純度、應用及通路分類-2026-2032年全球市場預測 碳酸鈣市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

碳酸鈣市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 2026-2030年全球碳酸鈣(CACO3)市場

2026-2030年全球碳酸鈣(CACO3)市場 碳酸鈣市場:按類型、應用和地區分類活性碳酸鈣市場:依等級、形態、應用和最終用途產業分類-2026-2032年全球市場預測

碳酸鈣市場:按類型、應用和地區分類活性碳酸鈣市場:依等級、形態、應用和最終用途產業分類-2026-2032年全球市場預測 碳酸鈣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

碳酸鈣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球碳酸鈣市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球食品級碳酸鈣市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球碳酸鈣市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球食品級碳酸鈣市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 全球農業鈣市場按類型、應用、形態、功能和地區分類-預測(至2030年)

全球農業鈣市場按類型、應用、形態、功能和地區分類-預測(至2030年)