|

市場調查報告書

商品編碼

1939008

碳酸鈣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

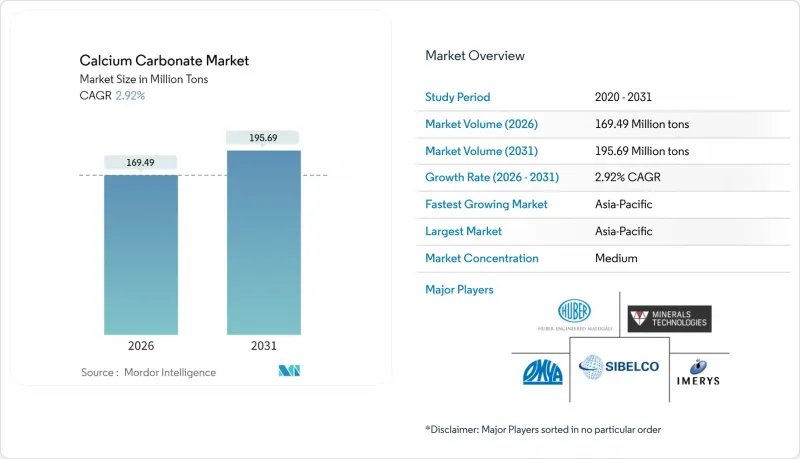

預計到 2026 年,碳酸鈣市場規模將達到 1.6949 億噸,高於 2025 年的 1.6468 億噸。

預計到 2031 年產量將達到 1.9569 億噸,2026 年至 2031 年的複合年成長率為 2.92%。

銷售持續成長證實了該礦物作為塑膠、造紙、建築材料、製藥和農業等領域中節省成本的填料和性能增強劑的既定地位。新興市場基礎設施投資的增加、電子商務驅動的包裝和紙製品需求的持續成長,以及消費者對添加鈣補充劑的保健和營養產品的不斷成長的需求,進一步推動了市場需求。擁有從礦山到應用一體化生產能力的製造商受益於有利的物流條件,並能夠根據最終用途的規格客製化產品等級。同時,日益嚴格的環境法規正在加速對節能破碎設施、低碳沉降線和再生石灰石原料的投資,從而重塑全部區域的成本結構。

全球碳酸鈣市場趨勢及展望

加速建設和基礎設施開發

亞太地區公共工程支出的激增推動了碳酸鈣市場的發展,建商們正在尋求經濟高效的礦物填料,用於水泥、聚合物改質混凝土、建築塗料和密封劑。綜合生產商正在擴大產能以滿足這一需求:伊梅里斯公司將其位於阿拉巴馬州錫拉卡加的工廠產能加倍,以供應建築級材料並縮短北美客戶的前置作業時間。城市負責人對低碳建築材料的推動也增加了對ReMined(100%消費前回收碳酸鈣)等產品的需求,該產品在保持強度和耐久性標準的同時,降低了產品的隱含碳含量。這些與永續性相關的細分市場使經銷商能夠在銷售穩定成長的同時獲得更高的利潤率。

塑膠和聚合物應用範圍的擴大

奈米級研磨技術和表面處理化學的快速發展,大大提升了薄膜、母粒和工程塑膠的性能。奈米碳酸鈣能夠增強包裝材料的拉伸強度、阻隔性和熱穩定性,同時保持透明度,使加工商能夠減少高達5%(重量比)的樹脂用量。中國製造商湖北微晶新材料有限公司已證明,分散在可生物分解聚合物中的亞100奈米顆粒能夠同時增強薄膜強度並精確調控其分解速率,從而直接滿足循環經濟包裝的要求。汽車製造商和電子品牌正擴大採用這些功能性填料,以滿足輕量化、耐熱性和可回收性的目標。

與碳酸鈣相關的健康危害

工人接觸碳酸鈣粉塵(可能導致吸入)引發的危害,促使監管機構加強審查,要求降低工廠和下游加工廠的允許接觸限值,並制定更嚴格的防護標準。奈米顆粒的毒理學研究仍在進行中,目前食品和藥品用途的核准通常需要進行全面的風險評估,這可能會延長商業化進程並增加合規成本。資金有限的小規模生產商往往難以實施閉合迴路加工和高效過濾設備,從而限制了供應的柔軟性。

細分市場分析

由於石灰石礦床豐富且研磨製程能耗低,粉狀碳酸鈣仍將是碳酸鈣市場的核心,預計到2025年將佔市場需求的76.92%。粉狀碳酸鈣優異的成本績效是其在原紙、聚烯薄膜和預拌混凝土等大批量應用領域的關鍵因素。然而,沉澱碳酸鈣(PCC)預計到2031年將以3.31%的複合年成長率加速成長,因為客戶願意為其窄粒徑分佈、高亮度和可客製化的表面化學性質支付溢價。研究人員成功利用大豆尿素酶來實現酵素沉澱,凸顯了這一轉變,這表明PCC可能透過降低成本來擴大其應用範圍。

成熟的碳酸鈣生產商正在對其工廠進行改造,加裝分級研磨系統和乾式塗層設備,以期在無需碳化反應器所需高額資本投入的情況下,達到與碳酸鈣相當的性能。同時,碳酸鈣供應商也正在擴大其內部碳二氧化碳捕集設施和可再生能源投入,以減少碳足跡——這對跨國客戶而言,正日益成為一項重要的採購考量。儘管這些策略的趨同加劇了競爭,但鑑於建築、塑膠和生命科學產業的需求差異,預計這兩個細分市場的碳酸鈣市場規模都將穩定成長。

本碳酸鈣市場報告按類型(細磨碳酸鈣、沉澱碳酸鈣)、應用(建築材料原料、營養補充劑、熱塑性添加劑、填料和顏料等)、終端用戶行業(造紙、塑膠、黏合劑和密封劑、建築等)以及地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。

區域分析

預計到2025年,亞太地區將佔全球碳酸鈣市場佔有率的48.25%,並在2031年之前以3.62%的複合年成長率持續成長。中國是該地區的主要需求來源,伊梅里斯在蕪湖、青陽和岳陽均設有工廠,為包裝、建築和生命科學行業的客戶提供產品。東南亞國家也正在擴大塗佈紙和PVC管材的產能,進一步擴大了該地區的需求基礎。

北美擁有強大的先進塑膠和醫藥供應鏈基礎,其特點是偏好技術級產品並實施嚴格的品管。近期在阿拉巴馬州和喬治亞的投資凸顯了該地區對在地採購的重視,這不僅減少了運輸排放,也確保了及時的技術支援。在歐洲,嚴格的碳減排和採石場修復法規促使人們更加重視再生原料和節能型沉澱設備。在南美洲,巴西和阿根廷的建築熱潮以及農業綜合企業的蓬勃發展推動了土壤處理化學品的消費。預計中東地區將因石化聯合企業和大型基礎設施計劃而保持穩定的需求。同時,非洲尚未開發的採石潛力也十分可觀,尤其是在埃及、奈及利亞和南非。儘管優質石灰石礦床的地理分佈將繼續影響貿易流量和區域價格,但本地化沉澱設備和先進破碎設施的建設正在逐步減輕全球碳酸鈣市場的運輸負擔。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速建設和基礎設施開發

- 塑膠和聚合物應用範圍的擴大

- 紙張和包裝產業的需求不斷成長

- 在醫療和製藥領域應用日益廣泛

- 市場限制

- 與碳酸鈣相關的健康危害

- 環境和採礦法規

- 物流和供應鏈挑戰

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

- 進出口貿易統計數據

第5章 市場規模與成長預測

- 類型

- 細磨碳酸鈣(GCC)

- 沉澱碳酸鈣(PCC)

- 應用

- 建築材料

- 營養補充品

- 熱塑性塑膠添加劑

- 填料和顏料

- 黏合劑組件

- 燃料氣脫硫

- 土壤中的中和劑

- 其他用途

- 終端用戶產業

- 紙

- 塑膠

- 黏合劑和密封劑

- 建造

- 油漆和塗料

- 製藥

- 車

- 農業

- 橡皮

- 其他終端用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

- 伊拉克

- 科威特

- 卡達

- 其他中東國家

- 非洲

- 南非

- 其他非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- ACCM

- GCCP Resources Limited

- Gulshan Polyols Ltd.

- Huber Engineered Materials

- Imerys

- Jordan Carbonate Company

- Manaseer Group

- Minerals Technologies Inc.

- Nigtas

- OKUTAMA KOGYO CO.,LTD.

- Omya International AG

- Provencale SA

- SaudiCarbonate

- SCHAEFER KALK GmbH & Co. KG

- Shiraishi Group

- Sibelco

- SigmaRoc Plc

- VMPC Joint Stock Company.

- Zantat Sdn. Bhd.

第7章 市場機會與未來展望

Calcium Carbonate market size in 2026 is estimated at 169.49 million tons, growing from 2025 value of 164.68 million tons with 2031 projections showing 195.69 million tons, growing at 2.92% CAGR over 2026-2031.

This steady volume-based growth underscores the mineral's entrenched role as both a cost-saving filler and a performance enhancer in plastics, paper, construction materials, pharmaceuticals, and agriculture. Demand is reinforced by rising infrastructure outlays in emerging economies, sustained packaging and paper requirements tied to e-commerce, and a steady pivot toward health-and-nutrition products that incorporate calcium supplements. Producers with integrated mine-to-application capabilities are benefiting from favorable logistics and the ability to tailor grades to end-use specifications. Meanwhile, environmental regulations are accelerating investment in energy-efficient grinding, low-carbon precipitation lines, and recycled limestone feedstocks, reshaping cost structures across every major region.

Global Calcium Carbonate Market Trends and Insights

Accelerating Construction and Infrastructure Development

Surging public-works spending across Asia-Pacific is boosting the calcium carbonate market as builders seek cost-effective mineral fillers for cement, polymer-modified concrete, architectural coatings, and sealants. Integrated producers have ramped up capacity to meet this requirement: Imerys doubled output at its Sylacauga, Alabama unit to supply construction-grade material and improve lead times for North American customers. Urban planners' push for low-carbon building materials is also raising demand for products such as ReMined, a 100% pre-consumer recycled calcium carbonate that reduces embodied carbon while maintaining strength and durability benchmarks. These sustainability-linked niches allow sellers to command higher margins even as bulk volumes grow steadily.

Expanding Plastic and Polymer Applications

Rapid advances in nano-scale grinding and surface-treatment chemistries have shifted the performance ceiling for film, masterbatch, and engineered-plastic grades. Nano-calcium carbonate enhances tensile strength, barrier properties, and thermal stability in packaging while preserving clarity, letting converters cut resin intensity by up to 5% on a weight basis. Chinese producer Hubei Micro Crystal New Materials demonstrated how sub-100 nm particles dispersed in biodegradable polymers can both toughen films and fine-tune degradation rates, directly supporting circular-economy packaging mandates. Automotive OEMs and electronics brands are increasingly specifying these functional fillers to meet lightweighting, heat-resistance, and recyclability targets.

Health Hazards Associated with Calcium Carbonate

Worker exposure to respirable calcium carbonate dust has sharpened regulatory oversight, prompting lower permissible exposure limits and more stringent containment norms in mills and downstream plants. Nanoparticle toxicology remains under study, and approvals for food or pharma applications now routinely require extensive risk assessments, which can prolong commercialization timelines and inflate compliance costs. Small producers with limited capital often struggle to install closed-loop handling and high-efficiency filtration, constraining supply flexibility.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand from the Paper and Packaging Industry

- Rising Healthcare and Pharmaceutical Usage

- Environmental and Mining Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ground calcium carbonate continues to anchor the calcium carbonate market, claiming 76.92% of 2025 demand thanks to abundant limestone deposits and low-energy milling routes. In volume-driven sectors such as basic paper, polyolefin film, and ready-mix concrete, GCC's favorable price-performance ratio remains decisive. Yet precipitated calcium carbonate is setting the pace with a 3.31% CAGR through 2031 as customers pay premiums for narrow particle-size distribution, higher brightness, and customizable surface chemistry. This shift was underscored when researchers achieved enzyme-induced precipitation using soybean urease, signaling cost-reduction paths that could widen PCC's reach.

Mature GCC producers are therefore retooling plants with classified grinding systems and dry-coating units to edge closer to PCC performance without incurring the steep capex of carbonation reactors. Meanwhile, PCC suppliers are scaling captive carbon-dioxide recovery and renewable-energy inputs to shrink their carbon footprint, an increasingly important procurement criterion for multinational customers. As these strategies converge, competitive intensity is rising, but the calcium carbonate market size for both sub-segments is projected to expand steadily, given differentiated demand profiles across construction, plastics, and life-science industries.

The Calcium Carbonate Report is Segmented by Type (Ground Calcium Carbonate and Precipitated Calcium Carbonate), Application (Raw Substance for Construction Material, Dietary Supplement, Additive for Thermoplastics, Filler and Pigment, and More), End-User Industry (Paper, Plastic, Adhesives and Sealants, Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East, and Africa).

Geography Analysis

Asia-Pacific dominated the calcium carbonate market with a 48.25% share in 2025 and is projected to advance at a 3.62% CAGR through 2031. China accounts for the lion's share of regional demand; Imerys operates facilities in Wuhu, Qingyang, and Yueyang to supply packaging, construction, and life-science customers. Southeast Asian economies are also adding coated-board and PVC-pipe capacity, broadening the regional demand base.

North America maintains a solid foothold owing to advanced plastics and pharmaceutical supply chains that prioritize technical grades and stringent quality control. Recent investments in Alabama and Georgia underscore the region's appetite for localized supply that cuts freight emissions and ensures rapid technical support. Europe's stringent carbon-reduction and quarry-rehabilitation rules make recycled feedstocks and energy-efficient precipitation plants critical. South America is leveraging construction booms in Brazil and Argentina alongside agribusiness growth that lifts soil-treatment consumption. The Middle East sees steady demand from petrochemical complexes and large-scale infrastructure projects, while Africa's quarrying potential remains underdeveloped but promising, particularly in Egypt, Nigeria, and South Africa. Geographic dispersion of high-grade limestone deposits will continue to influence trade flows and regional pricing, but localized precipitation units and upgraded grinding hubs are gradually trimming transport intensity across the global calcium carbonate market.

- ACCM

- GCCP Resources Limited

- Gulshan Polyols Ltd.

- Huber Engineered Materials

- Imerys

- Jordan Carbonate Company

- Manaseer Group

- Minerals Technologies Inc.

- Nigtas

- OKUTAMA KOGYO CO.,LTD.

- Omya International AG

- Provencale SA

- SaudiCarbonate

- SCHAEFER KALK GmbH & Co. KG

- Shiraishi Group

- Sibelco

- SigmaRoc Plc

- VMPC Joint Stock Company.

- Zantat Sdn. Bhd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Construction and Infrastructure Development

- 4.2.2 Expanding Plastic and Polymer Applications

- 4.2.3 Growing Demand from the Paper and Packaging Industry

- 4.2.4 Rising Healthcare and Pharmaceutical Usage

- 4.3 Market Restraints

- 4.3.1 Health Hazards Associated with Calcium Carbonate

- 4.3.2 Environmental and Mining Regulations

- 4.3.3 Logistics and Supply Chain Challenges

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

- 4.6 Import/Export Trade Statistics

5 Market Size and Growth Forecasts (Volume)

- 5.1 Type

- 5.1.1 Ground Calcium Carbonate (GCC)

- 5.1.2 Precipitated Calcium Carbonate (PCC)

- 5.2 Application

- 5.2.1 Raw Substance for Construction Material

- 5.2.2 Dietary Supplement

- 5.2.3 Additive for Thermoplastics

- 5.2.4 Filler and Pigment

- 5.2.5 Component of Adhesives

- 5.2.6 Desulfurization of Fuel Gas

- 5.2.7 Neutralizing Agent in Soil

- 5.2.8 Other Applications

- 5.3 End-user Industry

- 5.3.1 Paper

- 5.3.2 Plastic

- 5.3.3 Adhesives and Sealants

- 5.3.4 Construction

- 5.3.5 Paints and Coatings

- 5.3.6 Pharmaceutical

- 5.3.7 Automotive

- 5.3.8 Agriculture

- 5.3.9 Rubber

- 5.3.10 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Australia and New Zealand

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Iran

- 5.4.5.4 Iraq

- 5.4.5.5 Kuwait

- 5.4.5.6 Qatar

- 5.4.5.7 Rest of the Middle-East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Rest of Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ACCM

- 6.4.2 GCCP Resources Limited

- 6.4.3 Gulshan Polyols Ltd.

- 6.4.4 Huber Engineered Materials

- 6.4.5 Imerys

- 6.4.6 Jordan Carbonate Company

- 6.4.7 Manaseer Group

- 6.4.8 Minerals Technologies Inc.

- 6.4.9 Nigtas

- 6.4.10 OKUTAMA KOGYO CO.,LTD.

- 6.4.11 Omya International AG

- 6.4.12 Provencale SA

- 6.4.13 SaudiCarbonate

- 6.4.14 SCHAEFER KALK GmbH & Co. KG

- 6.4.15 Shiraishi Group

- 6.4.16 Sibelco

- 6.4.17 SigmaRoc Plc

- 6.4.18 VMPC Joint Stock Company.

- 6.4.19 Zantat Sdn. Bhd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Importance of Green Applications

- 7.3 Advancements in High-Performance Plastics and Polymers

食品級碳酸鈣市場規模、佔有率和成長分析:按類型、應用、終端用戶產業和地區分類-2026-2033年產業預測

食品級碳酸鈣市場規模、佔有率和成長分析:按類型、應用、終端用戶產業和地區分類-2026-2033年產業預測 碳酸鈣市場:依類型、等級、形態、原料、純度、應用及通路分類-2026-2032年全球市場預測

碳酸鈣市場:依類型、等級、形態、原料、純度、應用及通路分類-2026-2032年全球市場預測 碳酸鈣市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

碳酸鈣市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 2026-2030年全球碳酸鈣(CACO3)市場

2026-2030年全球碳酸鈣(CACO3)市場 碳酸鈣市場:按類型、應用和地區分類活性碳酸鈣市場:依等級、形態、應用和最終用途產業分類-2026-2032年全球市場預測

碳酸鈣市場:按類型、應用和地區分類活性碳酸鈣市場:依等級、形態、應用和最終用途產業分類-2026-2032年全球市場預測 美國碳酸鈣市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國碳酸鈣市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球碳酸鈣市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球食品級碳酸鈣市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球碳酸鈣市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球食品級碳酸鈣市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 全球農業鈣市場按類型、應用、形態、功能和地區分類-預測(至2030年)

全球農業鈣市場按類型、應用、形態、功能和地區分類-預測(至2030年)