|

市場調查報告書

商品編碼

2035154

日本戶外LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Outdoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

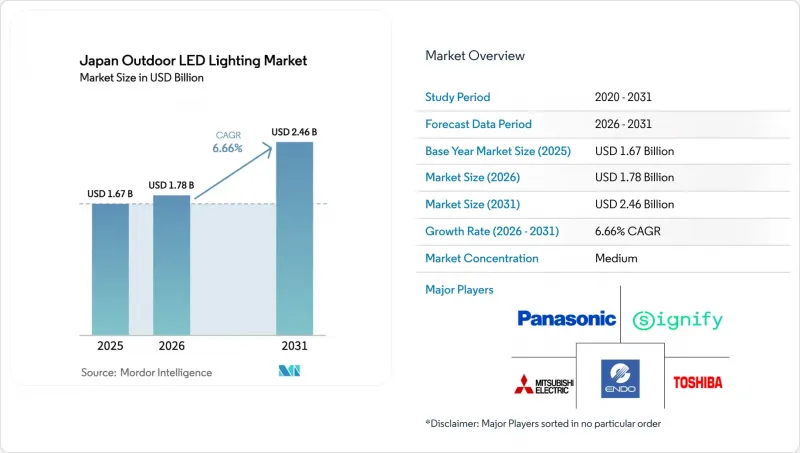

2025年日本戶外LED照明市場價值16.7億美元,預計到2031年將從2026年的17.8億美元成長到24.6億美元,預測期(2026-2031年)複合年成長率為6.66%。

市場規模的擴張主要受以下因素驅動:計畫於2026會計年度逐步淘汰汞燈、日本自然資源能源廳的節能指令以及LED組件價格的下降,這些因素縮短了地方政府的投資回收期。在東京-名古屋-大阪走廊沿線的智慧城市計畫中,透過將5G小型基地台設備和環境感測器整合到照明設備中,使路燈轉變為多功能資產,需求進一步擴大。在注重環保的地區,吸引昆蟲並減少光污染的「以人為本」的琥珀色LED燈正日益普及。另一方面,供應鏈對進口氮化鎵晶片的依賴以及大都會圈以外地方政府預算的縮減,都對短期成長構成挑戰。

日本戶外LED照明市場趨勢與洞察

節能法規正在改變採購方式。

根據日本國家能源效率標準,地方政府有義務達到預定的能源效率目標,因此,改用LED燈已成為法律要求,而非可選項。為了最大限度地獲得補貼,地方政府目前正將路燈、停車場照明和公共交通照明項目合併到單一競標中,從而擴大合約規模並縮短工程工期。透明的報告機制使城市管理者能夠將自身績效與其他城市進行比較,從而形成同儕壓力,並加速那些實施進度緩慢的城市的LED燈推廣。此外,對不遵守標準的處罰措施進一步鼓勵了快速實施,即使在資金預算緊張的情況下也是如此。

禁用汞燈縮短了汞燈的更換週期。

由於到2026年最後期限前約有300萬盞汞燈需要拆除,各市政當局被迫加快升級改造進度,而通常情況下,這一過程需要10年時間。此外,監管規定的最後期限也導致備件進口中斷,迫使各市政當局在全面維修LED燈具和維持現有照明系統不正常運作之間做出選擇。時間的縮短使得需求提前出現,給安裝能力帶來了壓力,尤其是在需要客製化支架的隧道和橋樑維修中。

地方政府預算凍結導致地方計畫延期。

為因應新冠疫情而提供的經濟刺激資金將於2024年到期,迫使許多小城市優先加強醫療保健和災害應變能力建設,而非升級照明設施。漫長的綠色債券津貼申請流程進一步延誤了專案進度,導致日本戶外LED照明市場呈現兩極化的局面:大都會圈發展領先,而農村地區則停滯不前。

細分市場分析

至2025年,照明燈具在日本戶外LED照明市場中佔比高達71.63%。這主要是由於地方政府傾向於更換整套照明系統,以確保覆蓋範圍和均勻的光學性能。由於整合無線控制和模組化感測器組件的普及,日本戶外LED照明市場中照明燈具的市場規模正在不斷擴大,以確保資產的未來相容性。僅更換燈具的市場正以8.02%的複合年成長率成長,高於整體市場成長速度,因為它可以相容於結構完好的老舊電線電線杆。

製造商正透過基於雲端的管理平台來區分其照明設備,這些平台可以發送韌體更新和診斷警報。Panasonic的「LANTERNA」照明設備展示了內容傳送功能,將路燈轉變為用於市政訊息的數位電子看板。由於現場檢查通常與計劃維護同時進行,因此僅更換燈泡仍然是維護週期中的熱門選擇,這樣可以快速更換LED燈泡而無需重新佈線。

預計到2025年,道路和街道項目將佔日本戶外LED照明市場規模的47.10%。這主要是由於監管機構設定了確保公共安全的最後期限。同時,體育設施和體育場館的複合年成長率最高,達到8.78%,這主要得益於為迎接國際賽事而對廣播級亮度和動態調光功能的需求。

場館業主正在安裝可與娛樂系統同步的RGBW照明燈具,這不僅能提升觀眾體驗,也能滿足電視色彩還原標準。停車場、交通樞紐和建築外觀也呈現穩定的需求,而組件成本的下降使得非必要的照明昇級更具經濟可行性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 自然資源和能源署強制執行的節能措施

- 到 2026 會計年度,必須迅速淘汰汞燈路燈。

- LED價格的下降縮短了地方政府投資的回收期。

- 東京、名古屋和大阪超級走廊的智慧城市項目

- 為了控制昆蟲數量,人們對人性化的「琥珀色」LED燈的需求日益成長。

- 利用LED燈桿部署5G小型基地台基礎設施

- 市場限制因素

- 由於應對新冠疫情的財政獎勵策略減少,小規模城鎮的預算被凍結。

- 昭和時代隧道照明燈具維修工程的複雜性。

- 氮化鎵基板進口的供應鏈風險

- 住宅組織就眩光問題提起的訴訟數量增加。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 燈

- 照明燈具/照明設備

- 透過使用

- 街道和道路照明

- 建築與景觀

- 體育場

- 隧道和橋樑

- 停車和交通區域

- 其他用途

- 按安裝類型

- 新安裝

- 維修工程

- 透過分銷管道

- 直銷

- 批發的

- 零售

- 電子商務

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Panasonic Holdings Corporation

- Toshiba Lighting and Technology Corporation

- Mitsubishi Electric Corporation

- Sharp Corporation

- Nichia Corporation

- Citizen Watch Co., Ltd.

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- Iwasaki Electric Co., Ltd.

- Endo Lighting Corporation

- Odelic Co., Ltd.

- Ushio Inc.

- MinebeaMitsumi Inc.

- NEC Lighting, Ltd.

- Signify NV

- OSRAM GmbH

- Acuity Brands, Inc.

- Zumtobel Group AG

- Seoul Semiconductor Co., Ltd.

- Musco Sports Lighting, LLC

第7章 市場機會與未來展望

The Japan outdoor LED lighting market size was valued at USD 1.67 billion in 2025 and estimated to grow from USD 1.78 billion in 2026 to reach USD 2.46 billion by 2031, at a CAGR of 6.66% during the forecast period (2026-2031).

Market size expansion is driven by the mandatory phase-out of mercury-vapor lamps planned for fiscal year 2026, energy-efficiency directives issued by the Agency for Natural Resources and Energy, and declining LED component prices that shorten municipal payback periods. Smart-city programs in the Tokyo-Nagoya-Osaka corridor amplify demand by bundling 5G small-cell equipment and environmental sensors with luminaires, converting lighting poles into multifunctional assets. Human-centric amber LEDs are gaining traction in environmentally sensitive areas because they reduce insect attraction and light pollution. At the same time, supply-chain exposure to imported gallium-nitride wafers and shrinking municipal budgets outside major metros challenge short-term growth.

Japan Outdoor LED Lighting Market Trends and Insights

Energy-efficiency mandates reshape procurement.

Japan's national efficiency standards oblige municipalities to meet predefined energy-intensity targets, making LED conversion a legal requirement rather than a discretionary upgrade. Local governments now bundle street, parking, and transit lighting in a single tender to maximize rebate eligibility, resulting in larger contract sizes and shorter project timelines. Transparent reporting rules enable city managers to benchmark their performance, fueling peer pressure that drives uptake among lagging jurisdictions. Penalties for non-compliance further compel rapid deployment even when capital budgets are tight.

Mercury-vapor ban compresses the replacement cycle.

Approximately 3 million mercury-vapor fixtures must be removed by the FY 2026 deadline, forcing municipalities to accelerate their upgrade schedules, which normally span a decade. The regulatory cut-off also stops the import of spare parts, leaving cities with a binary choice between full LED retrofits or non-functional lighting networks. This compressed window pulls demand forward and strains installation capacity, particularly for tunnel and bridge retrofits that need custom brackets.

Municipal budget freezes slow rural projects

COVID-19 stimulus funding ended in 2024, leaving many small cities with austerity budgets that prioritize healthcare and disaster resilience over lighting upgrades. Lengthy grant-application processes for green bonds further delay projects, resulting in a two-speed Japan outdoor LED lighting market where major metropolitan areas forge ahead while rural areas stall.

Other drivers and restraints analyzed in the detailed report include:

- Price erosion boosts ROI and rural demand.

- Smart-city corridor turns poles into digital assets.

- Retrofit complexity in Showa-era tunnels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires captured 71.63% of the Japan outdoor LED lighting market share in 2025 as municipalities favored complete system replacement for warranty coverage and uniform optical performance. The Japan outdoor LED lighting market size for luminaires benefits from integrated wireless controls and modular sensor bays that future-proof assets. Lamp-only replacements grow at 8.02% CAGR, a pace that outstrips the total market because they fit mixed-vintage poles where structural elements remain sound.

Manufacturers differentiate luminaires through cloud-managed platforms that push firmware updates and diagnostic alerts. Panasonic's LANTERNA fixture demonstrates content broadcasting, converting poles into digital signage for municipal messaging. Lamps remain popular in maintenance cycles where truck rolls coincide with routine inspection, allowing quick LED swaps without rewiring.

Street and roadway projects accounted for 47.10% of the Japan outdoor LED lighting market size in 2025, as regulatory deadlines focus on public safety corridors. Sports and stadium venues, however, post the fastest 8.78% CAGR as broadcast-grade luminance and dynamic dimming drive procurement ahead of global tournaments.

Venue owners install RGBW fixtures that synchronize with entertainment systems, enhancing spectator experience while meeting television color-rendering standards. Parking lots, transit hubs, and architectural facades follow with steady demand as falling component costs broaden the economic case for non-essential illumination upgrades.

The Japan Outdoor LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Application (Street and Roadway Lighting, Architectural and Landscape, and More), Installation Type (New Installation, and Retrofit Installation), Distribution Channel (Direct Sales, Wholesale, Retail, and E-Commerce). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Panasonic Holdings Corporation

- Toshiba Lighting and Technology Corporation

- Mitsubishi Electric Corporation

- Sharp Corporation

- Nichia Corporation

- Citizen Watch Co., Ltd.

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- Iwasaki Electric Co., Ltd.

- Endo Lighting Corporation

- Odelic Co., Ltd.

- Ushio Inc.

- MinebeaMitsumi Inc.

- NEC Lighting, Ltd.

- Signify N.V.

- OSRAM GmbH

- Acuity Brands, Inc.

- Zumtobel Group AG

- Seoul Semiconductor Co., Ltd.

- Musco Sports Lighting, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency mandates from Japan's Agency for Natural Resources and Energy

- 4.2.2 Rapid phasing-out of mercury-vapor street lamps mandated for FY-2026

- 4.2.3 LED price erosion enabling faster municipal ROIs

- 4.2.4 Tokyo-Nagoya-Osaka mega-corridor smart-city projects

- 4.2.5 Growing demand for human-centric "amber" LEDs to curb insect populations

- 4.2.6 Deployment of 5G small-cell infrastructure piggy-backing on LED poles

- 4.3 Market Restraints

- 4.3.1 Budget freezes in smaller municipalities post-COVID fiscal stimulus tapering

- 4.3.2 High retrofit complexity for Showa-era tunnel lighting fixtures

- 4.3.3 Supply-chain exposure to gallium-nitride substrate imports

- 4.3.4 Increasing glare-related litigation from residential groups

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Application

- 5.2.1 Street and Roadway Lighting

- 5.2.2 Architectural and Landscape

- 5.2.3 Sports and Stadium

- 5.2.4 Tunnel and Bridge

- 5.2.5 Parking and Transit Areas

- 5.2.6 Other Applications

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Wholesale

- 5.4.3 Retail

- 5.4.4 E-commerce

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Panasonic Holdings Corporation

- 6.4.2 Toshiba Lighting and Technology Corporation

- 6.4.3 Mitsubishi Electric Corporation

- 6.4.4 Sharp Corporation

- 6.4.5 Nichia Corporation

- 6.4.6 Citizen Watch Co., Ltd.

- 6.4.7 Koito Manufacturing Co., Ltd.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Iwasaki Electric Co., Ltd.

- 6.4.10 Endo Lighting Corporation

- 6.4.11 Odelic Co., Ltd.

- 6.4.12 Ushio Inc.

- 6.4.13 MinebeaMitsumi Inc.

- 6.4.14 NEC Lighting, Ltd.

- 6.4.15 Signify N.V.

- 6.4.16 OSRAM GmbH

- 6.4.17 Acuity Brands, Inc.

- 6.4.18 Zumtobel Group AG

- 6.4.19 Seoul Semiconductor Co., Ltd.

- 6.4.20 Musco Sports Lighting, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

戶外LED照明市場:全球市場預測,2026-2032年

戶外LED照明市場:全球市場預測,2026-2032年 戶外LED照明:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)印度戶外LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

戶外LED照明:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)印度戶外LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球戶外LED照明市場報告

2026年全球戶外LED照明市場報告 太陽能LED路燈市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、照明類型、產品類型、地區和競爭格局分類,2021-2031年)戶外LED照明市場-全球產業規模、佔有率、趨勢、機會與預測:來源、通路、應用、地區和競爭格局(2021-2031年)

太陽能LED路燈市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、照明類型、產品類型、地區和競爭格局分類,2021-2031年)戶外LED照明市場-全球產業規模、佔有率、趨勢、機會與預測:來源、通路、應用、地區和競爭格局(2021-2031年) 戶外LED照明市場規模、佔有率和成長分析(按類型、安裝方式、交付形式、銷售管道、應用和地區分類)—產業預測(2026-2033年)軍用戶外 LED 照明市場(按產品類型、電源、功率輸出、技術、應用、最終用戶和分銷管道)- 2025-2030 年全球預測中國戶外 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

戶外LED照明市場規模、佔有率和成長分析(按類型、安裝方式、交付形式、銷售管道、應用和地區分類)—產業預測(2026-2033年)軍用戶外 LED 照明市場(按產品類型、電源、功率輸出、技術、應用、最終用戶和分銷管道)- 2025-2030 年全球預測中國戶外 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)