|

市場調查報告書

商品編碼

2035116

CPaaS(通訊平台即服務):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Communication Platform-as-a-Service (CPaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

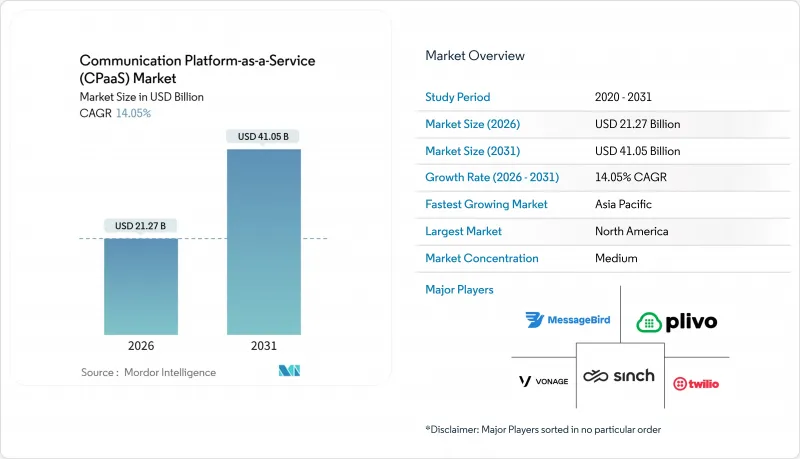

預計到 2026 年,通訊平台即服務 (CPaaS) 市場將達到 212.7 億美元,到 2031 年將達到 410.5 億美元,複合年成長率為 14.05%。

對嵌入式語音、通訊和視訊日益成長的需求正在改變客戶體驗的架構,促使企業從單一的客服中心套件轉向以 API 為先導、可組合的層級結構,以便直接整合到數位化工作流程中。推動這項轉變的三大因素是:嚴格的身份驗證法規,例如歐洲的 PSD2 強制要求可程式設計的動態密碼(OTP) 流程;消費者轉向 OTT 聊天管道,迫使企業在單一供應商的合作關係下進行整合;以及 5G 網路切片技術的出現,使通訊業者能夠為關鍵任務工作負載提供低延遲路徑。儘管競爭日益激烈,但沒有一家供應商的市場佔有率超過 15%,這意味著通訊平台即服務 (CPaaS) 市場仍存在著巨大的商機,等待著那些致力於解決特定產業挑戰和區域數據主權要求的專家企業去發掘。

全球通訊平台即服務 (CPaaS) 市場趨勢與洞察

以OTT聊天為中心的互動

僅 WhatsApp Business API 目前每月處理超過 1000 億條訊息,規模之龐大迫使 Meta 在 2025 年 7 月實施基於對話的收費模式。由於每個管道都有其獨特的核准流程和內容規則,企業紛紛湧向那些能夠與 WhatsApp、Telegram、LINE、微信和 Viber 等平台承包整合的平台。零售商和電商企業正在利用這些整合,在聊天線程中自動完成訂單確認、出貨狀態更新和退貨流程,從而減少對網頁入口網站的依賴。無法支援多個 OTT 平台的 CPaaS 供應商則面臨退守同質化簡訊服務的困境。此外,印度和巴西的資料本地化法規迫使服務提供者維護區域託管節點,這增加了複雜性和成本。

建置低程式碼/無程式碼 CPaaS

像 Twilio Studio 這樣的視覺化流程建立工具,讓不具備技術專長的員工也能在幾分鐘內設計預約提醒電話或購物車放棄挽回宣傳活動,因此無需專門的開發人員。快速原型製作縮短了中小企業的銷售週期,也讓大型企業在分配工程預算之前先試行各種互動方案。例如,醫療機構的工作人員無需 IT 部門的參與,即可設定諮詢後的簡訊跟進。編配工具的普及降低了進入門檻,從而擴大了通訊平台即服務 (CPaaS) 市場,尤其是在新興的亞太國家,這些國家的中小企業面臨著嚴重的開發人員短缺問題。由於仍需採取安全措施來遵守諸如美國《電話隱私法》(TCPA) 等反垃圾郵件許可規則,主要供應商正在其建置工具中整合選擇加入管理功能。

各國A2P簡訊附加費

印度、美國和歐洲許多地區的通訊業者對企業簡訊收取每條0.005美元至0.02美元的費用,這可能導致高流量業務的利潤率下降高達25個百分點。諸如印度基於區塊鏈的分散式帳本技術(DLT)平台和美國的10DLC框架等註冊系統要求所有模板都需預先核准,這延長了時效性強的警報引進週期。供應商正敦促客戶遷移到不產生額外費用的RCS和OTT管道,但低度開發市場設備支援的分散性阻礙了這項轉型。

細分市場分析

到2025年,純粹的專業公司將佔據通訊平台即服務(CPaaS)市場42.44%的營收佔有率。這一成長歸功於快速發布週期、統一API和營運商無關路由所推動的全球部署加速。然而,通訊業者主導服務預計將成為該細分市場中成長最快的領域,到2031年複合年成長率將達到14.67%,這主要得益於與企業行動合約的捆綁銷售以及無需信令路徑中繼的直接網路存取。

在實務中,跨國銀行通常採用雙重採購模式,即利用專業供應商進行全通路創新,並藉助電信業者的子公司提供對延遲敏感的國內身分驗證服務。超大規模雲端平台如今已整合原生通訊和語音功能,進一步降低了切換成本。因此,通訊平台即服務 (CPaaS) 市場正轉向混合使用模式,企業將獨立供應商提供的 API 豐富的創新功能與行動網路營運商提供的標準化工作負載交付相結合。

截至2025年,簡訊和傳統A2P流量仍將佔據39.21%的市場。這部分原因在於,即使資料通訊不穩定,任何設備都能接收文字訊息。然而,隨著蘋果iOS 18在2024年加入原生RCS支持,RCS普及的一大障礙已被消除,預計到2031年,RCS市場將以14.98%的複合年成長率成長。

零售商現在將產品輪播圖和快速回覆按鈕整合到RCS訊息中,與純文字簡訊相比,點擊率提高了三倍。早期採用者無需強制客戶安裝獨立應用程式即可獲得更豐富的互動指標。然而,注重安全性的企業仍保留需要口頭同意的語音和互動式語音應答(IVR)流程,這進一步印證了通路組合而非單一媒介才是通訊平台即服務(CPaaS)市場的基礎。

《通訊平台即服務 (CPaaS) 報告》按 CPaaS 類型(純 CPaaS、企業級 CPaaS 等)、通訊管道(簡訊和 A2P通訊等)、API 服務(通訊等)、部署模式(公共雲端、私有雲端、混合雲端)、企業規模(中小企業和大型企業)、最終用戶(IT 和電信、其他地區)以及工業(IT 和電信市場預測以美元 (USD) 為單位。

區域分析

預計到2025年,北美地區的收入將佔全球總收入的36.01%,這主要得益於該地區較高的雲端滲透率、蓬勃發展的新創企業生態系統以及與超大規模資料中心業者的接近性。該地區的買家優先考慮人工智慧驅動的分析和全通路編配,這有助於提升每位用戶平均收入(ARPU),並提高供應商的盈利。

亞太地區是經濟成長的主要驅動力,預計到2031年將以15.90%的複合年成長率加速成長,這主要得益於印度、中國和東南亞等智慧型手機普及率較高的經濟體正從桌面網路轉向行動端互動。到2025年底,印度的統一支付介面(UPI)每月將處理114億筆交易,每筆交易都會觸發即時警報,從而為該國的支付卡即服務(CPaaS)平台帶來基準流量。

歐洲憑藉PSD2認證保持著穩固的訂單基礎,但隨著初期合規浪潮的消退,成長速度將會放緩。南美、中東和非洲的絕對收入落後於其他地區,但由於公共部門的數位化,沙烏地阿拉伯和阿拉伯聯合大公國的成長正在加速。在非洲,由於網路覆蓋率較低,簡訊在短期內仍將佔據主導地位,這支撐了CPaaS(通訊平台即服務)市場中傳統管道的低階收入。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- OTT聊天互動

- 建置低程式碼/無程式碼 CPaaS

- PSD2主導的可程式通訊

- 通訊業者在基於 5G 的 CPaaS 領域的創新

- 人工智慧驅動的CPaaS自動化與分析

- 物聯網和邊緣整合 CPaaS 工作負載

- 市場限制因素

- 各國A2P簡訊附加費

- 企業資料居住要求

- 更嚴格的反垃圾郵件和同意規定

- 擴展通訊/API 安全性和詐欺風險

- 產業價值鏈分析

- 產業生態系分析

- 監理情勢

- 技術展望

- 無伺服器實現

- 基於機器學習和人工智慧的上下文路由

- 全通路互動式機器人

- 進階安全與隱私範式(零信任、STIR/SHAKEN)

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新參與企業的威脅

- 買方的議價能力

- 供應商議價能力

- 替代品的威脅

- 競爭公司之間的競爭關係

- 定價和經營模式分析

- 比較分析:CPaaS、UCaaS、傳統部署

- 投資分析

第5章 市場規模與成長預測

- CPaaS 的類型

- 純粹的CPaaS

- 企業級 CPaaS

- 通訊業者主導的CPaaS

- 基於服務供應商的CPaaS

- 混合型CPaaS

- 透過通訊管道

- 簡訊/A2P通訊

- 語音通話和互動語音應答

- 影片 WebRTC

- 電子郵件

- 推播通知/應用程式內通知

- RCS(進階通訊服務)通訊

- 透過 API 服務

- 通訊API

- 語音 API

- 影片API

- 身份驗證和安全 API

- RCS(進階通訊服務)API

- 透過部署方法

- 公共雲端

- 私有雲端

- 混合雲端

- 按公司規模

- 中小企業

- 大公司

- 按最終用戶類別

- 資訊科技/通訊

- 銀行、金融服務和保險業 (BFSI)

- 零售與電子商務

- 醫療保健

- 旅遊與飯店

- 物流/運輸

- 政府/公共部門

- 教育

- 其他最終用戶字段

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、資金籌措、合作)

- 市佔率分析

- 公司簡介

- Twilio Inc.

- Vonage Holdings Corp.

- Sinch AB

- Infobip Ltd.

- MessageBird BV

- Bandwidth Inc.

- Plivo Inc.

- 8x8 Inc.

- Voximplant(Zingaya Inc.)

- Voxvalley Technologies

- IntelePeer Cloud Communications

- Wazo Communication Inc.

- Avaya Inc.

- AT&T Inc.

- Mitel Networks Corporation

- Telestax

- CM.com NV

- Kaleyra Inc.

- Route Mobile Ltd.

- Telnyx LLC

- RingCentral Inc.

- Cisco Systems Inc.

- Link Mobility Group ASA

- TeleSign Corp.

第7章 市場機會與未來展望

The Communication Platform-as-a-Service market size is USD 21.27 billion in 2026, and it is projected to reach USD 41.05 billion by 2031, advancing at a 14.05% CAGR.

Heightened demand for embedded voice, messaging, and video is reshaping customer-experience architectures, encouraging firms to swap monolithic contact-center suites for API-first, composable layers that plug directly into digital workflows. Three catalysts drive this shift: stronger authentication rules such as PSD2 in Europe, which require programmable one-time-password flows; the migration of consumers to over-the-top chat channels that enterprises must now unify under a single vendor relationship; and the arrival of 5G network slicing that lets operators carve low-latency lanes for mission-critical workloads. Competitive intensity is rising, yet no vendor controls more than 15%, so the Communication Platform-as-a-Service market still offers white-space opportunities for specialists addressing vertical gaps or regional data-sovereignty requirements.

Global Communication Platform-as-a-Service (CPaaS) Market Trends and Insights

OTT Chat-Centric Engagement

WhatsApp Business API alone now handles more than 100 billion messages per month, a scale that forced Meta to adopt conversation-based pricing in July 2025. Enterprises flock to platforms that maintain turnkey integrations with WhatsApp, Telegram, LINE, WeChat, and Viber because each channel carries unique approval workflows and content rules. Retailers and e-commerce players use these integrations to automate order confirmations, shipping updates, and returns entirely within chat threads, trimming web-portal dependencies. CPaaS vendors incapable of sustaining multi-OTT support risk falling back to commoditized SMS delivery. Even so, data-localization rules in India and Brazil compel providers to keep regional hosting nodes, adding complexity and cost.

Low-Code / No-Code CPaaS Build-Outs

Visual flow builders such as Twilio Studio let non-technical staff design appointment-reminder calls or abandoned-cart campaigns in minutes, removing the need for dedicated developers. Rapid prototyping shortens sales cycles for SMEs and lets large enterprises pilot engagement ideas before allocating engineering budgets. Healthcare clerical workers, for instance, can set up post-consultation SMS follow-ups without IT involvement. The democratization of orchestration tools is broadening the Communication Platform-as-a-Service market by lowering entry barriers, particularly in emerging Asia Pacific where small businesses face acute developer shortages. Compliance with spam-consent rules such as the TCPA in the United States still requires guardrails, so leading vendors embed opt-in management inside their builders.

Country-Level A2P SMS Surcharges

Operators in India, the United States, and much of Europe have imposed fees of USD 0.005-0.02 per message on enterprise SMS, eroding margins by up to 25 percentage points for high-volume traffic. Registration systems such as India's blockchain-based DLT platform and the U.S. 10DLC framework require every template to be pre-approved, lengthening onboarding cycles for time-sensitive alerts. Vendors are nudging customers toward RCS or OTT channels where surcharges do not apply, but fragmented handset support outside developed markets slows migration.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered CPaaS Automation and Analytics

- Telco 5G-Anchored CPaaS Innovation

- Enterprise Data-Residency Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pure-play specialists captured a 42.44% revenue slice of the Communication Platform-as-a-Service market in 2025. Their growth stems from rapid release cadences, unified APIs, and carrier-agnostic routing that speed global expansion. However, telco-driven offerings exhibit the segment's quickest advance at a 14.67% CAGR to 2031, riding bundled enterprise mobility contracts and direct network access that eliminates a hop in the signaling path.

In practice, multinational banks often dual-source, using a pure-play vendor for omnichannel innovation and a carrier subsidiary for latency-critical authentication inside domestic borders. Hyperscale clouds are now embedding native messaging and voice, narrowing switching costs further. Consequently, the Communication Platform-as-a-Service market is tilting toward hybrid consumption, where enterprises mix API-rich innovation from independents with regulated-workload delivery from mobile-network operators.

SMS and traditional A2P traffic retained 39.21% share in 2025, in part because every handset can receive a text even when data connectivity is unreliable. Yet Apple's iOS 18 added native RCS support in 2024, clearing a major adoption hurdle and driving a 14.98% CAGR for RCS through 2031.

Retailers now embed product carousels and quick-reply buttons inside RCS messages, achieving tap-through rates triple that of plain-text SMS. Enterprises that move early gain richer engagement metrics without forcing customers to install standalone apps. Still, security-sensitive organizations retain voice and interactive-voice-response flows where verbal consent remains mandatory, confirming that a channel portfolio rather than a single medium underpins the Communication Platform-as-a-Service market.

The Communication Platform-As-A-Service Report is Segmented by CPaaS Type (Pure-Play, Enterprise-Grade, and More), Communication Channel (SMS and A2P Messaging, and More), API Service (Messaging, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Enterprise Size (SMEs, and Large Enterprises), End-User Vertical (IT and Telecom, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 36.01% of 2025 revenue due to deep cloud penetration, a dense start-up ecosystem, and proximity to hyperscalers. Regional buyers prioritize AI-driven analytics and omnichannel orchestration, translating into premium ARPU that props up vendor profitability.

Asia Pacific is the growth engine, forecast to surge at a 15.90% CAGR to 2031 as smartphone-first economies in India, China, and Southeast Asia leapfrog desktop web to mobile engagement. India's Unified Payments Interface processed 11.4 billion monthly transactions by late 2025, each triggering real-time alerts that inflate baseline traffic on domestic CPaaS platforms.

Europe retains a solid base order flow anchored in PSD2 authentication, but growth moderates after the initial compliance wave. South America, the Middle East and Africa trail in absolute revenue, though Saudi Arabia and the United Arab Emirates are accelerating due to public-sector digitization. In Africa, coverage gaps mean SMS dominates for now, sustaining a revenue floor for legacy channels inside the Communication Platform-as-a-Service market.

- Twilio Inc.

- Vonage Holdings Corp.

- Sinch AB

- Infobip Ltd.

- MessageBird B.V.

- Bandwidth Inc.

- Plivo Inc.

- 8x8 Inc.

- Voximplant (Zingaya Inc.)

- Voxvalley Technologies

- IntelePeer Cloud Communications

- Wazo Communication Inc.

- Avaya Inc.

- AT&T Inc.

- Mitel Networks Corporation

- Telestax

- CM.com N.V.

- Kaleyra Inc.

- Route Mobile Ltd.

- Telnyx LLC

- RingCentral Inc.

- Cisco Systems Inc.

- Link Mobility Group ASA

- TeleSign Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OTT Chat-Centric Engagement

- 4.2.2 Low-Code / No-Code CPaaS Build-Outs

- 4.2.3 PSD2-Driven Programmable Messaging

- 4.2.4 Telco 5G-Anchored CPaaS Innovation

- 4.2.5 AI-Powered CPaaS Automation and Analytics

- 4.2.6 IoT and Edge-Integrated CPaaS Workloads

- 4.3 Market Restraints

- 4.3.1 Country-Level A2P SMS Surcharges

- 4.3.2 Enterprise Data-Residency Mandates

- 4.3.3 Stricter Anti-Spam and Consent Regulations

- 4.3.4 Growing Messaging/API Security and Fraud Risk

- 4.4 Industry Value-Chain Analysis

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.7.1 Serverless Deployments

- 4.7.2 Machine-Learning and AI-Enabled Contextual Routing

- 4.7.3 Omnichannel Conversational Bots

- 4.7.4 Advanced Security and Privacy Paradigms (Zero-Trust, STIR/SHAKEN)

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

- 4.10 Pricing and Business-Model Analysis

- 4.11 Comparative Analysis of CPaaS vs UCaaS vs Traditional Deployments

- 4.12 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By CPaaS Type

- 5.1.1 Pure-Play CPaaS

- 5.1.2 Enterprise-Grade CPaaS

- 5.1.3 Telco-Driven CPaaS

- 5.1.4 Service-Provider-Based CPaaS

- 5.1.5 Hybrid CPaaS

- 5.2 By Communication Channel

- 5.2.1 SMS and A2P Messaging

- 5.2.2 Voice and IVR

- 5.2.3 Video and WebRTC

- 5.2.4 Email

- 5.2.5 Push and In-App Notifications

- 5.2.6 Rich Communication Services (RCS) Messaging

- 5.3 By API Service

- 5.3.1 Messaging APIs

- 5.3.2 Voice APIs

- 5.3.3 Video APIs

- 5.3.4 Authentication and Security APIs

- 5.3.5 Rich Communication Services (RCS) APIs

- 5.4 By Deployment Model

- 5.4.1 Public Cloud

- 5.4.2 Private Cloud

- 5.4.3 Hybrid Cloud

- 5.5 By Enterprise Size

- 5.5.1 Small and Medium Enterprises (SMEs)

- 5.5.2 Large Enterprises

- 5.6 By End-User Vertical

- 5.6.1 IT and Telecom

- 5.6.2 BFSI

- 5.6.3 Retail and E-commerce

- 5.6.4 Healthcare

- 5.6.5 Travel and Hospitality

- 5.6.6 Logistics and Transportation

- 5.6.7 Government and Public Sector

- 5.6.8 Education

- 5.6.9 Other End-User Verticals

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Twilio Inc.

- 6.4.2 Vonage Holdings Corp.

- 6.4.3 Sinch AB

- 6.4.4 Infobip Ltd.

- 6.4.5 MessageBird B.V.

- 6.4.6 Bandwidth Inc.

- 6.4.7 Plivo Inc.

- 6.4.8 8x8 Inc.

- 6.4.9 Voximplant (Zingaya Inc.)

- 6.4.10 Voxvalley Technologies

- 6.4.11 IntelePeer Cloud Communications

- 6.4.12 Wazo Communication Inc.

- 6.4.13 Avaya Inc.

- 6.4.14 AT&T Inc.

- 6.4.15 Mitel Networks Corporation

- 6.4.16 Telestax

- 6.4.17 CM.com N.V.

- 6.4.18 Kaleyra Inc.

- 6.4.19 Route Mobile Ltd.

- 6.4.20 Telnyx LLC

- 6.4.21 RingCentral Inc.

- 6.4.22 Cisco Systems Inc.

- 6.4.23 Link Mobility Group ASA

- 6.4.24 TeleSign Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

通訊平台即服務 (CPaaS) 市場:全球市場預測,2026-2032 年

通訊平台即服務 (CPaaS) 市場:全球市場預測,2026-2032 年 通訊平台即服務 (CPaaS) 市場規模、佔有率和成長分析:按服務類型、企業規模、應用領域、最終用戶產業、銷售管道和地區分類-2026-2033 年產業預測

通訊平台即服務 (CPaaS) 市場規模、佔有率和成長分析:按服務類型、企業規模、應用領域、最終用戶產業、銷售管道和地區分類-2026-2033 年產業預測 通訊平台即服務 (CPaaS) 市場:按最終用戶產業和地區分類

通訊平台即服務 (CPaaS) 市場:按最終用戶產業和地區分類 2026年全球通訊平台(MaaP)市場報告

2026年全球通訊平台(MaaP)市場報告 通訊平台即服務 (CPaaS) 市場預測至 2034 年—按組件、通訊管道、部署模式、企業規模、應用程式、最終用戶和地區分類的全球分析電信平台即服務 (TPaaS) 市場預測至 2034 年—按組件、部署模式、平台類型、企業用例、最終用戶和區域分類的全球分析

通訊平台即服務 (CPaaS) 市場預測至 2034 年—按組件、通訊管道、部署模式、企業規模、應用程式、最終用戶和地區分類的全球分析電信平台即服務 (TPaaS) 市場預測至 2034 年—按組件、部署模式、平台類型、企業用例、最終用戶和區域分類的全球分析 通訊平台即服務 (CPaaS) 市場規模、佔有率、趨勢和預測:按組件、企業規模、行業和地區分類,2026-2034 年2026年全球通訊平台即服務(CPaaS)市場報告

通訊平台即服務 (CPaaS) 市場規模、佔有率、趨勢和預測:按組件、企業規模、行業和地區分類,2026-2034 年2026年全球通訊平台即服務(CPaaS)市場報告 印度通訊平台即服務 (CPaaS) 市場佔有率分析、行業趨勢、統計數據和成長預測 (2026-2031)

印度通訊平台即服務 (CPaaS) 市場佔有率分析、行業趨勢、統計數據和成長預測 (2026-2031) CPaaS(通訊平台即服務)市場規模、佔有率和成長分析(按部署類型、公司規模、垂直產業和地區分類)-2026-2033年產業預測

CPaaS(通訊平台即服務)市場規模、佔有率和成長分析(按部署類型、公司規模、垂直產業和地區分類)-2026-2033年產業預測