|

市場調查報告書

商品編碼

2035113

機器人割草機:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Robotic Lawn Mower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

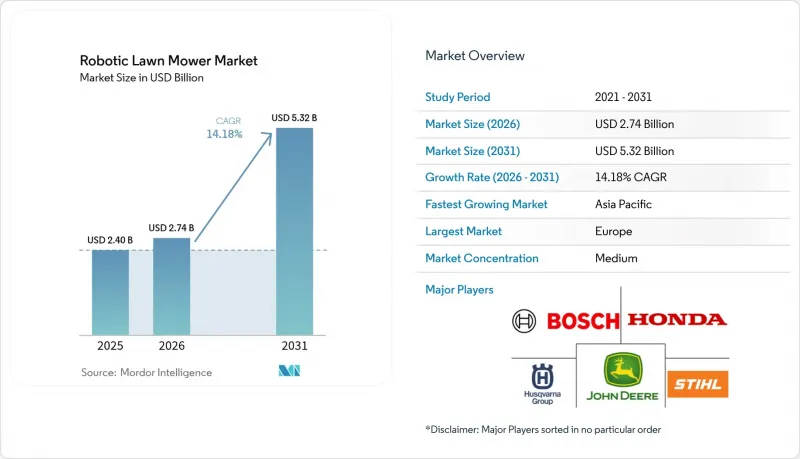

預計機器人割草機市場將從 2025 年的 24 億美元成長到 2026 年的 27.4 億美元,然後在 2031 年達到 53.2 億美元,2026 年至 2031 年的複合年成長率為 14.18%。

這一成長主要得益於電池驅動的自動割草機系統的日益普及。園林綠化產業的人手不足、日益嚴格的環境法規、充電技術的進步以及無需邊界的先進視覺導航系統,都為市場擴張提供了支撐。製造商正透過訂閱服務和現有設備的遠端軟體更新來增強其收入來源。零售商專注於高利潤的智慧家庭設備,這對市場產生了積極影響,而住宅對自動割草服務的使用也不斷增加。在商業領域,尤其是體育設施管理人員和維護公司,為了解決人手不足並確保大面積草坪的割草品質始終如一,對機器人割草機的投資也在增加。

全球機器人割草機市場趨勢及洞察

住宅草坪維護外包業務增加

在住宅草坪護理市場,外包給專業人士的趨勢日益成長,這主要受雙薪家庭優先考慮休閒時間以及人口老齡化導致體力勞動減少的雙重影響。園林綠化公司正透過引進機器人割草機來解決長期存在的人手不足,從而在不增加員工的情況下維持服務進度。這種自動化使工人能夠專注於利潤更高的服務,例如景觀設計和硬景觀施工。由於機器人割草機在夜間運作,因此可以在保證割草高度均勻的前提下,增加每條路線的服務次數,而不會受到人手不足的影響。頻繁且精準的割草能夠改善草坪健康狀況,減少肥料用量,進而提高服務提供者的投資報酬率。在北美郊區和西歐市場,這種草坪護理外包的趨勢正在加速發展,這些地區以獨棟住宅為主,家庭收入水平也允許人們使用專業服務。

過渡到電池驅動的戶外設備

加州和歐盟對汽油動力手持設備的政府監管正在加速向電池動力產品的轉型,電動驅動正逐漸成為標配而非可選升級。 STIHL報告稱,2023年電池動力產品佔其總銷量的24%,併計劃到2027年達到35%,這表明該行業正朝著電氣化方向發展。機器人設備的噪音和振動降低,使其能夠在夜間運作,從而最大限度地提高每日割草效率,同時避免打擾居民,並騰出白天時間用於澆水和休閒活動。電池能量密度的提高使中階機器人單次充電即可運作超過150分鐘,而快速充電功能則將停機時間減少到運作週期的20%以下。政府獎勵,例如德國對零排放園藝設備提供的200歐元(約215美元)補貼,正在縮短投資回收期,並在經濟波動的情況下維持穩定的需求。

與傳統割草機的初始成本比較

機器人割草機的價格差異很大,從 800 美元到 5000 美元不等,遠高於汽油動力手推式割草機的 300 美元到 800 美元。 500 美元的專業安裝費用對首次購買者來說是一筆不小的開支,尤其是在新興市場。在已開發市場,住宅會權衡機器人割草機 3 到 5 年的投資回收期與搭乘用割草機更短的融資方案之間的利弊。雖然零售貸款和訂閱模式可以降低初始成本,但這些選擇大多僅限於高階品牌,限制了入門級市場的銷售量。在南美,貨幣貶值推高了以美元計價的進口價格,導致消費者選擇購買二手汽油動力割草機。雖然電池成本的降低和本地組裝未來可能會縮小價格差距,但目前市場成長仍受到價格親民的限制。

細分市場分析

到2025年,涵蓋範圍積在501至2000平方公尺之間的中型機器人割草機將佔據42.85%的市場。這一主導地位反映了歐洲和北美典型的郊區用地面積。這些機型在價格、涵蓋範圍積和電池續航時間之間實現了最佳平衡,既滿足了普通住宅庭院的需求,又最大限度地節省了儲存空間。隨著製造商引入系統化的割草模式,與隨機導航系統相比,割草均勻性得到提升,該細分市場持續成長。此外,退貨率的下降也印證了該細分市場的穩定性,顯示這些機型符合消費者的性能預期。

涵蓋範圍積達2,000平方公尺以上的高階機型以17.1%的複合年成長率呈現最高成長。這一成長主要歸功於高爾夫球場、體育設施和教育機構等尋求降低人事費用的機構對這類產品的日益青睞。無線導航系統的引入降低了大面積區域的安裝成本,而集中式管理系統則允許透過單一設備介面管理多個單元。涵蓋範圍積小於平方公尺的低價機器人則在日本和英國人口稠密的都市區保持一定的市場佔有率。隨著價格下降並影響利潤率,製造商正在為產品添加諸如庭院邊緣修剪等附加功能。為了提高客戶維繫,業界的重心正從硬體創新轉向軟體增強,例如灌溉和同步調度管理系統。

2025年,邊界引導系統在機器人割草機市場仍維持64.75%的市佔率。這是因為安裝人員和住宅認可其即使在雨天和落葉嚴重的季節也能保持穩定的性能。現有的線路基礎設施透過品牌忠誠度支撐著更換需求,但由於庭院維修和維修成本較高,一些用戶正在探索其他替代技術。

預計到2031年,基於視覺/攝影機的平台將以18.9%的複合年成長率成長。這些系統對於管理多處物業的商業承包商尤其有利,因為它們無需開挖溝渠,並可在多個地點快速部署。混合系統結合了RTK-GPS廣域定位和光學邊緣偵測,可在花壇附近實現精確導航,在運動設施中可達到厘米級精度。僅配備全球導航衛星系統(GNSS)的設備在晴朗的開放區域表現良好,但由於訊號干擾,在樹木茂密的郊區環境中其有效性會降低。製造商正日益重視軟體開發,不斷改進人工智慧演算法,以提高對常見花園障礙物(例如彈跳床、車道和戶外家具)的偵測精度。

區域分析

預計到2025年,歐洲將佔據機器人割草機市場44.80%的佔有率。這主要得益於歐洲居民根深蒂固的園藝習慣、高昂的人事費用以及排放氣體法規,這些因素共同推動了機器人割草機的普及。德國、英國和法國擁有廣泛的分銷網路,而斯堪地那維亞市場在獨棟住宅領域的滲透率更高。歐洲的機械法規簡化了安全認證流程,促進了跨境產品發布,並實現了跨區域的整合行銷。製造商正利用區域供應鏈規避中美之間的關稅,從而在北美出口市場中獲得競爭優勢。

預計到2031年,亞太地區將成長13.2%,這主要得益於中國服務型機器人產業的蓬勃發展。該產業預計到2024年市場規模將達到737.55億元人民幣(約104億美元)。國內服務型機器人產業大規模供應鋰離子電池和相機模組。在日本,勞動人口減少;在韓國,都市區草坪覆蓋率上升,都推動了對噪音低於60分貝的緊湊型機器人的需求。澳洲市政當局正在公共場所開展機器人試點項目,以應對不斷上漲的工資水準。大洋洲地區正被定位為商業機器人車隊營運的試驗場。

儘管北美擁有廣大的草坪面積,但其機器人割草機的普及率卻低於歐洲。此外,貿易趨勢也更傾向於從歐洲進口而非中國產品,這影響了市場佔有率的分佈。根據《通貨膨脹控制法案》,2026年提案的電動戶外設備消費者補貼政策可望促進機器人割草機的普及。雖然目前南美、中東和非洲的市場佔有率僅為個位數,但墨西哥和海灣國家中產階級財富的成長預示著未來耐高溫防塵的高階機型將迎來發展機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 住宅草坪維護外包的趨勢日益成長。

- 過渡到電池驅動的戶外設備

- 園林綠化服務業人手不足

- 零售商推廣高利潤率的智慧家居產品。

- 基於視覺的無邊界導航的出現。

- 面向自主割草機的OEM訂閱模式

- 市場限制因素

- 與傳統割草機相比,初始成本較高

- 在不平坦的地形和長滿高草的區域,性能會受到限制。

- 網路安全和資料隱私問題

- 因鋰離子園藝設備有火災風險,現召回。

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按範圍

- 小規模(小於500平方公尺)

- 中型(501-2000平方公尺)

- 大型(2000平方公尺或以上)

- 導航技術

- Boundary-Wire

- 視覺/攝影機

- GNSS/RTK-GPS

- 最終用戶

- 住宅

- 商業的

- 透過分銷管道

- 線上(直銷、電商平台)

- 線下(家居建材商店、專賣店)

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 伊朗

- 阿曼

- 其他中東國家

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Husqvarna AB

- ANDREAS STIHL AG & Co. KG

- Honda Motor Co., Ltd.

- Deere & Company

- Robert Bosch GmbH

- Positec Technology Co., Ltd.

- The Toro Company

- Stanley Black & Decker, Inc.

- STIGA SpA(3i Group plc)

- Globe Tools Group Co., Ltd.

- Segway Inc.(Ninebot Ltd.)

- Shenzhen Mammotion Technologies Co., Ltd.

- EcoFlow Technology Inc.

- FJDynamics International Ltd.

- Yamabiko Corporation

第7章 市場機會與未來展望

The robotic lawn mower market size is expected to grow from USD 2.4 billion in 2025 to USD 2.74 billion in 2026 and is forecast to reach USD 5.32 billion by 2031 at 14.18% CAGR over 2026-2031.

The increasing adoption of battery-powered autonomous mowing systems drives this growth. The market expansion is supported by labor shortages in the landscaping industry, enhanced environmental regulations, improvements in charging technology, and advanced vision-based navigation systems that eliminate the need for boundary wires. Manufacturers are strengthening their revenue streams through subscription services and remote software updates for existing equipment. The market benefits from retailers' focus on smart-home devices with higher profit margins, while homeowners increasingly opt for automated mowing services. The commercial segment, particularly sports field managers and facility maintenance contractors, is increasing investments in robotic mowers to address workforce shortages and maintain consistent mowing quality across extensive areas.

Global Robotic Lawn Mower Market Trends and Insights

Rising Residential Lawn-Care Outsourcing

The residential lawn care market shows increasing preference for professional services over self-maintenance, driven by dual-income households prioritizing leisure time and an aging population less inclined toward physical labor. Landscape companies address persistent labor shortages by implementing robotic mowing fleets to maintain service schedules without increasing workforce. This automation enables crews to focus on higher-margin services such as landscape design and hardscaping. The robotic mowers operate nightly, increasing the number of properties serviced per route while ensuring uniform cutting heights independent of labor constraints. The frequent, precise mowing patterns improve lawn health and reduce fertilizer requirements, enhancing the return on investment for service providers. This trend of outsourced lawn maintenance accelerates adoption across North American suburbs and Western European markets, where single-family homes predominate and household income levels support professional service fees.

Shift Toward Battery-Electric Outdoor Equipment

Government restrictions on gasoline-powered handheld equipment in California and the European Union accelerate the transition to battery-powered products, establishing electric propulsion as a standard rather than an optional upgrade. STIHL reported that battery-powered units comprised 24% of its 2023 sales and aims to reach 35% by 2027, demonstrating the industry's shift toward electrification. The reduced noise and vibration of robotic units enable overnight operation, maximizing daily mowing cycles without disrupting residents while leaving daylight hours available for watering or recreational activities. Improvements in battery energy density now enable mid-range robots to operate for over 150 minutes per charge, while rapid charging capabilities reduce downtime to less than 20% of the operational cycle. Government incentives, such as Germany's EUR 200 (USD 215) rebate on zero-emission garden equipment, reduce the investment recovery period and maintain steady demand during economic fluctuations.

High Upfront Cost versus Conventional Mowers

The cost of robotic lawn mowers ranges from USD 800 to USD 5,000, significantly higher than gas-powered push mowers priced between USD 300 and USD 800. Professional installation costs of USD 500 create barriers for first-time buyers, particularly in emerging economies. In developed markets, homeowners compare the three to five-year payback period against shorter financing terms available for riding tractors. While retail financing and subscription models reduce initial costs, these options are primarily available for premium brands, limiting sales volume in entry-level segments. In South America, currency depreciation increases dollar-denominated import prices, causing consumers to opt for used gas-powered units. Although battery cost reductions and local assembly may eventually reduce the price difference, current market growth remains constrained by affordability challenges.

Other drivers and restraints analyzed in the detailed report include:

- Labor Shortages in Landscaping Services

- Retailer Push for High-Margin Smart-Home SKUs

- Fire-Risk Recalls of Li-ion Garden Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium units covering 501-2,000 m2 accounted for 42.85% of the robotic lawn mower market in 2025. This dominance reflects the typical suburban lot sizes in Europe and North America. These models offer an optimal balance of price, coverage area, and battery life, meeting average residential yard requirements while requiring minimal storage space. The segment's growth continues as manufacturers implement systematic cutting patterns, improving grass cutting uniformity compared to random navigation systems. The segment's stability is evident in reduced return rates, indicating these models meet consumer performance expectations.

High-range models covering areas above 2,000 m2 demonstrate the highest growth rate at 17.1% CAGR. This growth stems from increased adoption by golf courses, sports facilities, and educational institutions seeking to reduce labor costs. The implementation of wire-free navigation systems reduces installation costs for large areas, while centralized control systems enable management of multiple units through single-device interfaces. Low-range robots covering under 500 m2 maintain market presence in dense urban areas of Japan and the United Kingdom. Declining prices affect profit margins, leading manufacturers to include additional features like patio-edge trimming capabilities. The industry focus has shifted from hardware innovations to software enhancements, such as irrigation-synchronized scheduling systems, to strengthen customer retention.

Boundary-wire guidance maintained a 64.75% market share in robotic lawn mowers in 2025, as installers and homeowners value its consistent performance during rainy conditions and heavy debris seasons. The established wire infrastructure supports replacement sales through brand loyalty, though yard renovation and repair expenses motivate some users to explore alternative technologies.

Vision/camera-based platforms are projected to grow at a 18.9% CAGR through 2031. These systems eliminate trenching requirements and enable quick deployment across multiple locations, particularly benefiting commercial contractors managing multiple properties. Hybrid systems combine RTK-GPS for broad positioning with optical edge detection for precise navigation near flower beds, delivering centimeter-level accuracy for sports facilities. While Global Navigation Satellite System (GNSS) only units perform well in open areas with clear sky views, their effectiveness decreases in suburban environments with dense tree coverage due to signal interference. Manufacturers continue to enhance AI algorithms to improve the detection of common yard obstacles, including trampolines, driveways, and outdoor furniture, indicating increased focus on software development.

The Robotic Lawn Mower Market Report is Segmented by Range (Low (Less Than 500 M2), and More), by Navigation Technology (Boundary-Wire, and More), by End-User (Residential, and Commercial), by Distribution Channel (Online, and Offline), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe held 44.80% of the robotic lawn mower market share in 2025, driven by established gardening practices, high labor costs, and emissions regulations that support robotic lawn mower adoption. Germany, the United Kingdom, and France maintain extensive dealer networks, while Scandinavian markets show high penetration in detached housing segments. European machinery regulations streamline safety certification processes, facilitating cross-border product launches and enabling consolidated marketing across multiple regions. Manufacturers leverage regional supply chains to avoid U.S.-China tariffs, providing a competitive advantage for North American exports.

Asia-Pacific demonstrates 13.2% growth through 2031, supported by China's RMB 73.755 billion (USD 10.4 billion) service-robot industry in 2024, which provides domestic lithium-ion cells and camera modules at scale. Japan's declining workforce and South Korea's concentrated urban lawns increase demand for compact models operating below 60 dB. Australian municipalities test robots in public spaces to address wage inflation, positioning Oceania as an evaluation ground for commercial fleet operations.

North America shows lower penetration compared to Europe despite extensive lawn areas, while trade dynamics favor European imports over Chinese products, affecting market share distribution. The Inflation Reduction Act's proposed consumer rebate on electric outdoor equipment may increase robotic mower adoption if implemented in 2026. South America, the Middle East, and Africa currently represent single-digit market shares, though increasing middle-class wealth in Mexico and Gulf nations indicates future opportunities for premium models designed for high temperatures and sand exposure.

- Husqvarna AB

- ANDREAS STIHL AG & Co. KG

- Honda Motor Co., Ltd.

- Deere & Company

- Robert Bosch GmbH

- Positec Technology Co., Ltd.

- The Toro Company

- Stanley Black & Decker, Inc.

- STIGA S.p.A. (3i Group plc)

- Globe Tools Group Co., Ltd.

- Segway Inc. (Ninebot Ltd.)

- Shenzhen Mammotion Technologies Co., Ltd.

- EcoFlow Technology Inc.

- FJDynamics International Ltd.

- Yamabiko Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Residential Lawn-Care Outsourcing

- 4.2.2 Shift Toward Battery-Electric Outdoor Equipment

- 4.2.3 Labor Shortages in Landscaping Services

- 4.2.4 Retailer Push for High-Margin Smart-Home SKUs

- 4.2.5 Advent of Vision-Based, Perimeter-Free Navigation

- 4.2.6 Original Equipment Manufacturer Subscription Models for Autonomous Mowing

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost versus Conventional Mowers

- 4.3.2 Limited Performance on Uneven and Tall-Grass Terrains

- 4.3.3 Cyber-Security and Data-Privacy Concerns

- 4.3.4 Fire-Risk Recalls of Li-ion Garden Equipment

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Range

- 5.1.1 Low (Less Than 500 m2)

- 5.1.2 Medium (501-2,000 m2)

- 5.1.3 High (More Than 2,000 m2)

- 5.2 By Navigation Technology

- 5.2.1 Boundary-Wire

- 5.2.2 Vision / Camera

- 5.2.3 GNSS / RTK-GPS

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 Online (Direct, Marketplaces)

- 5.4.2 Offline (DIY Stores, Specialty Dealers)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Australia

- 5.5.3.6 New Zealand

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Iran

- 5.5.5.4 Oman

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Husqvarna AB

- 6.4.2 ANDREAS STIHL AG & Co. KG

- 6.4.3 Honda Motor Co., Ltd.

- 6.4.4 Deere & Company

- 6.4.5 Robert Bosch GmbH

- 6.4.6 Positec Technology Co., Ltd.

- 6.4.7 The Toro Company

- 6.4.8 Stanley Black & Decker, Inc.

- 6.4.9 STIGA S.p.A. (3i Group plc)

- 6.4.10 Globe Tools Group Co., Ltd.

- 6.4.11 Segway Inc. (Ninebot Ltd.)

- 6.4.12 Shenzhen Mammotion Technologies Co., Ltd.

- 6.4.13 EcoFlow Technology Inc.

- 6.4.14 FJDynamics International Ltd.

- 6.4.15 Yamabiko Corporation

7 Market Opportunities and Future Outlook

機器人割草機市場:按類型、動力來源、草坪面積、刀片類型、電壓、銷售管道和最終用戶分類-2026-2032年全球市場預測

機器人割草機市場:按類型、動力來源、草坪面積、刀片類型、電壓、銷售管道和最終用戶分類-2026-2032年全球市場預測 歐洲機器人割草機:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

歐洲機器人割草機:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球人工智慧(AI)割草機市場報告

2026年全球人工智慧(AI)割草機市場報告 機器人割草機市場機會、成長要素、產業趨勢分析及2026-2035年預測無線割草機器人市場:按類型、電源、最終用戶和銷售管道,全球預測,2026-2032年

機器人割草機市場機會、成長要素、產業趨勢分析及2026-2035年預測無線割草機器人市場:按類型、電源、最終用戶和銷售管道,全球預測,2026-2032年 機器人割草機市場規模、佔有率和趨勢分析報告:按電池容量、銷售管道、最終用途、地區和細分市場預測(2026-2033 年)2026年全球機器人割草機市場報告

機器人割草機市場規模、佔有率和趨勢分析報告:按電池容量、銷售管道、最終用途、地區和細分市場預測(2026-2033 年)2026年全球機器人割草機市場報告 全球機器人割草機市場-產業規模、佔有率、趨勢、機會與預測:電池容量、草坪面積、連結性、分銷管道、最終用戶、地區和競爭格局(2021-2031)

全球機器人割草機市場-產業規模、佔有率、趨勢、機會與預測:電池容量、草坪面積、連結性、分銷管道、最終用戶、地區和競爭格局(2021-2031) 機器人割草機市場-2026-2031年預測

機器人割草機市場-2026-2031年預測 按產品類型和地區分類的機器人割草機市場規模、佔有率和成長分析 - 2026-2033 年產業預測

按產品類型和地區分類的機器人割草機市場規模、佔有率和成長分析 - 2026-2033 年產業預測