|

市場調查報告書

商品編碼

2035058

聚聚丁烯對苯二甲酸酯(PBT):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)Polybutylene Terephthalate (PBT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

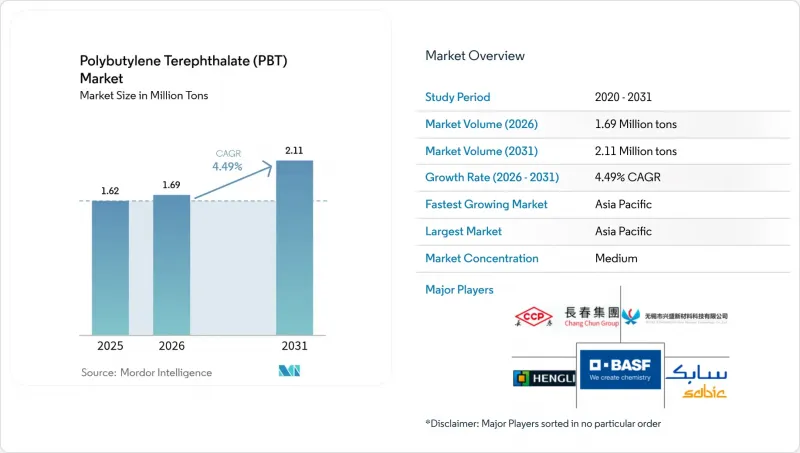

預計到 2026 年,聚聚丁烯對苯二甲酸酯(PBT) 的市場規模將達到 169 萬噸,高於 2025 年的 162 萬噸,預計到 2031 年將達到 211 萬噸。

預計從 2026 年到 2031 年,其複合年成長率將達到 4.49%。

這一前景鞏固了聚丁烯對苯二甲酸酯)在工程熱塑性塑膠市場的主導地位,這得益於其尺寸穩定性、耐濕性和可添加多種添加劑的特性。這項發展動能源自於四大宏觀經濟因素的綜效:(1) 全球汽車平台積極的電氣化目標;(2) 工廠自動化資料傳輸速率的指數級成長;(3) 消費性電子產品領域更嚴格的阻燃法規;(4) 鼓勵使用再生工程樹脂的公共政策獎勵。這四大因素共同作用,使得聚對聚丁烯對苯二甲酸酯(PBT)市場的重要性從傳統的引擎室應用擴展到高性能電池組、高速連接器和精密工業齒輪箱等領域。製造商正致力於垂直整合1,4-丁二醇和玻璃纖維的供應,而原始設備製造商(OEM)則優先考慮可靠的本地化配混,以降低物流風險。儘管亞太地區新增產能,但此趨勢仍使區域價格差異維持在較低水準。

全球聚聚丁烯對苯二甲酸酯(PBT)市場趨勢及洞察

工業自動化領域高速數據連接器的快速普及

工業自動化設備正從串列現場現場匯流排架構向多Gigabit確定性乙太網路過渡,這一轉變使得每條生產線上的高頻銅纜和光纖介面數量加倍。連接器外殼必須確保在接近 80 度C 的持續環境溫度下保持介電完整性,能夠承受機油污染,並能承受反覆的高低溫循環。玻璃纖維增強的 UL 94 V-0 級聚聚丁烯對苯二甲酸酯)提供了必要的尺寸穩定性,從而製造出即插即用的 IP67 連接器,降低了機器停機的風險。日本和德國的機器製造商正在將無鹵 PBT 外殼標準化,以符合 IEC 61076 互連規則,這使得聚對聚丁烯對苯二甲酸酯市場成為下一代機器人線束的預設材料。隨著預測性維護感測器被引入到每個機器人關節中,需求進一步加速成長,需要小型、包覆成型的 PBT 連接器,這些連接器能夠承受超過 10,000 次扭轉循環而不產生微裂紋。

亞洲電動車電池組組件中從 PA66 向 PBT 的過渡正在加速。

由於PBT具有低吸濕性、優異的電解耐受性以及在125 度C快速充電過程中尺寸變化極小等優點,中國、韓國和越南的電動汽車電池製造商目前已開始在模組框架、冷卻液歧管和電壓感測連接器等部件中選用PBT而非PA66。在單體電池封裝設計中,由於外殼更靠近高能量密度的電芯,這些要求顯得特別重要。美國的一級供應商也紛紛效仿,將電池組件的生產轉移到墨西哥以滿足跨太平洋地區的需求,從而降低亞洲生產商受國內價格波動的影響。電動摩托車平台的快速更新換代進一步推動了PBT配方的持續改進,並使其在更廣泛的出行領域中得到應用。

1,4-丁二醇的價格波動與生物基琥珀酸的供應有關。

聚聚丁烯對苯二甲酸酯(PBT) 的聚合依賴於丁二醇的穩定供應。雖然生物基生產路線屬於低碳生產,但其產能仍集中在少數幾家發酵廠,原料糖純度的下降可能導致工廠停產數週,進而引發現貨市場價格飆升。 2024 年,中國 PBT 生產商為保障利潤率而降低了反應器運轉率,但恰逢電動車射出成型訂單高峰期,樹脂供應卻出現緊張。沒有自有丁二醇 (BDO) 生產線的通用加工商面臨交貨延遲,其影響波及電子設備的生產計劃。預計到 2026 年,中東地區石化企業新增的丁二醇產能將緩解價格壓力,但短期內的價格波動將使聚對聚丁烯對苯二甲酸酯市場的複合年成長率 (CAGR) 預測值下調 0.8 個百分點。

細分市場分析

改質級聚對苯二甲酸丁二醇酯(PET)佔總產量的68.15%,預計到2031年將以4.87%的複合年成長率成長,鞏固了其在聚丁烯對苯二甲酸酯玻璃含量為30%,拉伸模量超過10 GPa,熱變形溫度接近210 度C,使其能夠應用於電動車引擎室內的逆變器蓋,在95 度C的冷卻液衝擊下保持性能穩定。這種磷基阻燃化合物在0.4mm厚度下即可達到UL 94 V-0阻燃等級,且流動性損失極小。這是一項突破性的成就,將型腔填充速度提升至0.25秒,並將澆口壓力降低12 MPa。因此,改性級聚對聚丁烯對苯二甲酸酯鞏固了其在高密度闆對板連接器領域作為首選材料的地位,推動了該細分市場PET的擴張。

未改質PBT在某些領域仍佔據重要地位,這些領域對食品接觸所需的光學透明度和純度要求高於機械強度。醫用注射器活塞利用其低萃取率,積層製造絲材則利用其緩慢的結晶速率來生產無翹曲的原型。然而,隨著OEM技術規範日益嚴格,其市場佔有率正在逐漸下降,而對改性等級的需求正在不斷成長。為了應對這一變化,混料商通過在未改性等級中添加生物基BDO琥珀酸酯來提升其永續性,從而在更廣泛的聚聚丁烯對苯二甲酸酯市場中鞏固了小規模但穩定的細分市場。

聚對聚丁烯對苯二甲酸酯(PBT) 市場報告按產品類型(未改質 PBT 和改質 PBT)、終端用戶產業(汽車、電氣電子、工業機械及其他)和地區(亞太、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以數量(噸)和價值(美元)兩種單位呈現。

區域分析

亞太地區佔全球消費量的68.30%,預計到2031年將以4.84%的最高複合年成長率成長。這反映了該地區單體、聚合物和化合物生產能力無與倫比的整合。重慶工廠近期擴建的目標是生產可生物分解共聚物,以開拓包裝終端市場。如此規模確保了成本優勢,而接近性電子和電動車供應鏈則保證了本地市場的快速發展,從而鞏固了該地區在聚聚丁烯對苯二甲酸酯市場的主導地位。

在北美,由於半導體生產回流和電動汽車電池本地化生產,供應鏈正在縮短,從而推高了需求。生產商正利用豐富的頁岩氣衍生產品作為具有成本競爭力的原料,其中美國和墨西哥的汽車原始設備製造商 (OEM) 推動了連接器需求的持續成長。加拿大對再生材料含量的監管壓力正在推動對化學回收的投資,預計在 2027 年前打造北美首個閉合迴路對聚丁烯對苯二甲酸酯酯 (PBT) 供應鏈。這將進一步增強聚對聚丁烯對苯二甲酸酯市場的差異化優勢。

儘管歐洲內燃機汽車的回收速度放緩,但該地區仍然是生物基原料和廢樹脂(PCR)計畫的重要試驗場。歐洲的複合材料生產商正在試驗溶劑溶解回收技術,該技術能夠保持分子量,目標是2028年回收30%的工業廢棄物。即使在整體生產低迷的情況下,這些永續性措施也正在提升該地區在高檔產品中的佔有率。南美、中東和非洲這三個地區擁有新興的汽車組裝中心和不斷擴展的電信基礎設施,預示著未來聚對聚丁烯對苯二甲酸酯(PBT)市場佔有率可能會多元化成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 工業自動化領域高速數據連接器的快速普及

- 亞洲電動車電池組組件正迅速從PA66材料轉向PBT材料

- 汽車業輕量化和金屬替代的主要趨勢

- 家用電子電器。

- 政府對再生工程塑膠含量的獎勵

- 市場限制因素

- 1,4-丁二醇價格的波動與生物琥珀酸的供應情況有關。

- 歐洲內燃機汽車生產的復甦速度比預期慢。

- 全球玻璃纖維短缺正在影響增強型PBT的成本。

- 價值鏈分析

- 監理情勢

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 新進入者的威脅

- 終端用戶領域的趨勢

- 航太(來自航太零件生產的銷售額)

- 汽車(汽車生產)

- 建築與施工(新建建築占地面積)

- 電氣和電子(電氣和電子產品生產產生的銷售收入)

- 包裝(塑膠包裝量)

第5章 市場規模和成長預測(價值和數量)

- 依產品類型

- 未修飾的PBT

- 改良型PBT

- 按最終用戶行業分類

- 車

- 電氣和電子

- 工業機械

- 其他

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 馬來西亞

- 亞太其他地區

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- BASF SE

- Celanese Corporation

- Chang Chun Group

- Evonik Industries AG

- Hengli Group Co. Ltd.

- Kolon Plastics Inc.

- LANXESS AG

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- Nan Ya Plastics Corporation

- Polyplastics Co. Ltd.

- SABIC

- Toray Industries Inc.

- Wuxi Xingsheng New Material Technology Co.

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

Polybutylene Terephthalate market size in 2026 is estimated at 1.69 million tons, growing from 2025 value of 1.62 million tons with 2031 projections showing 2.11 million tons, growing at 4.49% CAGR over 2026-2031.

This baseline underscores the polybutylene terephthalate market size leadership in engineering thermoplastics that combine dimensional stability, moisture resistance, and the ability to accept a broad additive portfolio. Momentum stems from the convergence of four macro forces: (1) aggressive electrification targets in global vehicle platforms, (2) exponential growth in factory-automation data rates, (3) tightening flame-retardant regulations in consumer devices, and (4) public-policy incentives for recycled engineering-resin content. Together they expand the polybutylene terephthalate market's relevance beyond its legacy under-hood presence toward high-performance battery-pack, high-speed connector, and precision industrial gear housings. Producer strategies pivot around vertical integration into 1,4-butanediol and glass-fiber supply, while OEMs prize secure local compounding to de-risk logistics, a dynamic that keeps regional pricing spreads narrow despite fresh Asia-Pacific capacity.

Global Polybutylene Terephthalate (PBT) Market Trends and Insights

Rapid Adoption of High-Speed Data Connectors in Industrial Automation

Industrial-automation equipment is shifting from serial field-bus architectures to multi-gigabit deterministic Ethernet, a transition that multiplies the number of high-frequency copper and fiber-optic interfaces per factory line. Connector housings must guarantee dielectric integrity at continuous ambient temperatures near 80 °C, resist machine-oil contamination, and tolerate repetitive hot-cold cycles. Glass-fiber reinforced UL 94 V-0 polybutylene terephthalate delivers the requisite dimensional stability, enabling plug-and-play IP67 connectors that cut machine-downtime risk. Japanese and German machine builders standardize on halogen-free PBT housings to comply with IEC 61076 cross-mating rules, positioning the polybutylene terephthalate market as the default material in next-generation robotics harnesses. Volume growth further accelerates as predictive-maintenance sensors migrate into every robotic joint, each demanding miniature over-molded PBT connectors that survive 10,000+ torsion cycles without micro-cracks.

Asia's Accelerating Shift from PA66 to PBT in EV Battery-Pack Components

Electric-vehicle battery manufacturers in China, South Korea, and Vietnam now specify PBT over PA66 for module frames, coolant manifolds, and voltage-sensing connectors owing to lower moisture uptake, superior electrolyte resistance, and tighter dimensional change across 125 °C fast-charge excursions. Cell-to-pack designs amplify these requirements because housings sit closer to high-energy cells. . American Tier-1 suppliers follow suit as they localize battery-component production in Mexico, creating a trans-Pacific demand bridge that cushions Asian producers against domestic price swings. Short-cycle platform refreshes in electric two-wheelers further support recurring formulation upgrades, embedding PBT into a wider mobility universe.

Volatility of 1,4-Butanediol Prices Linked to Bio-Succinic Acid Supply

Polybutylene terephthalate polymerization hinges on stable butanediol supply. Bio-based routes, though lower-carbon, remain concentrated in a handful of fermentation plants that can shut down for weeks when feed-sugar purity drifts, creating sudden spot-market spikes. Chinese PBT producers responded in 2024 by trimming reactor rates to protect margins, easing resin availability just as EV injection-molding orders peaked. Merchant converters without captive BDO faced delivery delays that rippled into electronics production schedules. While new petrochemical BDO capacity in the Middle East will reduce price stress by 2026, interim volatility lops 0.8 percentage points off the polybutylene terephthalate market CAGR trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Auto Lightweighting and Metal-Replacement Trend

- Rising Demand for Halogen-Free FR Grades in Consumer Electronics

- Slower-Than-Expected European ICE Vehicle Production Recovery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The modified-grade segment accounts for 68.15% of the overall volume and is on track for a 4.87% CAGR to 2031, underscoring its centrality to the polybutylene terephthalate market. At 30% glass loading, the tensile modulus climbs beyond 10 GPa while the HDT approaches 210 °C, enabling under-hood EV inverter covers that must withstand a 95 °C coolant surge without creep. Phosphorus-based flame-retardant formulations achieve a UL 94 V-0 rating at 0.4 mm with only marginal loss in flow, a breakthrough that enhances cavity-fill rates in 0.25 s cycle times and lowers gate pressures by 12 MPa. Modified grades, therefore, cement preferred-material status in high-density board-to-board connectors, fueling the polybutylene terephthalate market size for this subclass.

Unmodified PBT, retaining relevance where optical clarity or food-contact purity trumps mechanical strength. Medical syringe plungers exploit their low extractables, and additive-manufacturing filaments capitalize on their slow-crystallization window to build warp-free prototypes. Yet share slips incrementally as OEM engineering specifications escalate, channeling incremental demand into modified options. Compounders counter by blending bio-succinic BDO to grant unmodified grades sustainability appeal, reinforcing a modest but stable niche within the broader polybutylene terephthalate market.

The Polybutylene Terephthalate Market Report is Segmented by Product Type (Unmodified PBT and Modified PBT), End-User Industry (Automotive, Electrical and Electronics, Industrial and Machinery, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region accounts for 68.30% of consumption and is forecast to record the fastest 4.84% CAGR through 2031, reflecting the unparalleled integration of monomer, polymer, and compound capacity within the region. The recent expansions in Chongqing are targeted at biodegradable copolymers that unlock packaging end-markets. Such scale secures cost leadership while proximity to electronics and EV supply chains guarantees local offtake, preserving regional dominance in the polybutylene terephthalate market.

Demand in North America is growing as semiconductor reshoring and EV-battery localization compact supply lines. Producers exploit abundant shale-gas derivatives for cost-competitive feedstock, and automotive OEMs in the United States and Mexico drive sustained connector demand. Canadian regulatory pressure for recycled content prompts chemical-recycling investments that may yield the continent's first closed-loop PBT stream by 2027, enhancing differentiation in the polybutylene terephthalate market.

Despite sluggish ICE vehicle recovery in Europe, the region remains a technology testbed for bio-based feedstock and post-consumer resin initiatives. Continental compounders pilot solvent-based dissolution recycling that retains molecular weight, aiming to recapture 30% of post-industrial waste by 2028. These sustainability advances bolster the region's premium-grade supply share, even as overall volume languishes. South America, the Middle-East and Africa, together, have potential tied to emerging automotive assembly hubs and expanding telecommunications infrastructure, hinting at future diversification of the polybutylene terephthalate market share distribution.

- BASF SE

- Celanese Corporation

- Chang Chun Group

- Evonik Industries AG

- Hengli Group Co. Ltd.

- Kolon Plastics Inc.

- LANXESS AG

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- Nan Ya Plastics Corporation

- Polyplastics Co. Ltd.

- SABIC

- Toray Industries Inc.

- Wuxi Xingsheng New Material Technology Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of high-speed data connectors in industrial automation

- 4.2.2 Asia's accelerating shift from PA66 to PBT in EV battery-pack components

- 4.2.3 Mainstream auto lightweighting and metal-replacement trend

- 4.2.4 Rising demand for halogen-free FR grades in consumer electronics

- 4.2.5 Government incentives for recycled engineering plastics content

- 4.3 Market Restraints

- 4.3.1 Volatility of 1,4-butanediol prices linked to bio-succinic acid supply

- 4.3.2 Slower-than-expected European ICE vehicle production recovery

- 4.3.3 Tight global glass-fiber supply impacting reinforced-PBT cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Competitive Rivalry

- 4.6.5 Threat of New Entrants

- 4.7 End-use Sector Trends

- 4.7.1 Aerospace (Aerospace Component Production Revenue)

- 4.7.2 Automotive (Automobile Production)

- 4.7.3 Building and Construction (New Construction Floor Area)

- 4.7.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.7.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Unmodified PBT

- 5.1.2 Modified PBT

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Industrial and Machinery

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 Canada

- 5.3.2.2 Mexico

- 5.3.2.3 United States

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Celanese Corporation

- 6.4.3 Chang Chun Group

- 6.4.4 Evonik Industries AG

- 6.4.5 Hengli Group Co. Ltd.

- 6.4.6 Kolon Plastics Inc.

- 6.4.7 LANXESS AG

- 6.4.8 LG Chem Ltd.

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 Nan Ya Plastics Corporation

- 6.4.11 Polyplastics Co. Ltd.

- 6.4.12 SABIC

- 6.4.13 Toray Industries Inc.

- 6.4.14 Wuxi Xingsheng New Material Technology Co.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

Polybutylene Adipate Terephthalate市場:全球市場預測,2026-2032年聚丁烯對苯二甲酸酯市場:全球市場預測,2026-2032年

Polybutylene Adipate Terephthalate市場:全球市場預測,2026-2032年聚丁烯對苯二甲酸酯市場:全球市場預測,2026-2032年 聚聚丁烯對苯二甲酸酯(PBT)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

聚聚丁烯對苯二甲酸酯(PBT)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 聚丁烯對苯二甲酸酯市場報告:按類型、加工方法、最終用途產業和地區分類(2026-2034 年)全球Polybutylene Adipate Terephthalate市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

聚丁烯對苯二甲酸酯市場報告:按類型、加工方法、最終用途產業和地區分類(2026-2034 年)全球Polybutylene Adipate Terephthalate市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年聚丁烯對苯二甲酸酯(PBT)全球市場報告

2026年聚丁烯對苯二甲酸酯(PBT)全球市場報告 Polybutylene Adipate Terephthalate(PBAT) 市場(按等級、應用、最終用途產業和地區)- 預測至 2030 年

Polybutylene Adipate Terephthalate(PBAT) 市場(按等級、應用、最終用途產業和地區)- 預測至 2030 年 Polybutylene Adipate Terephthalate市場規模、佔有率、成長分析(按等級、應用、最終用途產業和地區)- 產業預測,2025 年至 2032 年

Polybutylene Adipate Terephthalate市場規模、佔有率、成長分析(按等級、應用、最終用途產業和地區)- 產業預測,2025 年至 2032 年 全球PBT單絲市場

全球PBT單絲市場 全球聚丁烯對苯二甲酸酯(PBT) 需求分析:按類型、應用、市場預測(至 2034 年)

全球聚丁烯對苯二甲酸酯(PBT) 需求分析:按類型、應用、市場預測(至 2034 年)