|

市場調查報告書

商品編碼

2035036

越南暖通空調市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Vietnam HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

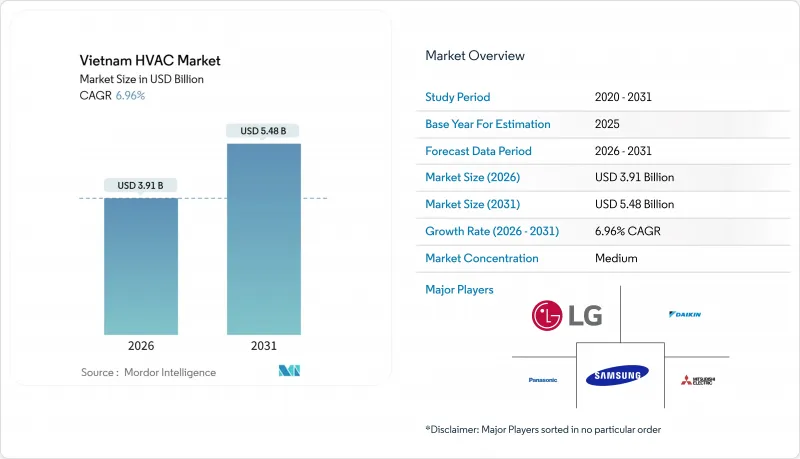

預計到 2026 年,越南 HVAC 市場規模將達到 39.1 億美元,到 2031 年將達到 54.8 億美元,預測期內複合年成長率為 6.96%。

強勁的GDP成長、加速的都市化以及持續不斷的綜合用途建築項目正在推動越南暖通空調(HVAC)市場的發展,並擴大了住宅、商業和工業應用領域的基本客群。外商直接投資在電子組裝和半導體封裝領域的湧入刺激了對精密潔淨室HVAC系統的需求,而疫情後酒店業的復甦則帶動了對集中式冷卻器和低噪音艙室系統的需求。政府對節能的獎勵,以及將於2025年生效的無管道空調強制性性能標準,正在提升消費者對變頻設備和變冷媒流量(VRF)平台的偏好,從而重塑越南HVAC市場的競爭格局。同時,更嚴格的冷媒法規和區域供冷試點計畫也為提供低全球暖化潛值(GWP)冷媒、整合控制系統和基於績效的服務合約的供應商創造了新的商機。

越南暖通空調市場趨勢與洞察

旅遊和酒店業的擴張

旅遊業正逐步復甦,朝著2025年設定的2,500萬人次的目標邁進。目前,全國飯店建築規劃客房數量已超過49,800間,主要集中在胡志明市、河內、峴港和富國島。飯店企業正著力採用集中式冷卻器、VRF系統和符合QCVN 09:2017/BXD能源效率標準的低雜訊無管道機組,促使承包商引入變頻壓縮機和R-32冷媒。國際品牌要求符合ASHRAE 55熱舒適度標準和ISO 7730指標,這推動了建築管理系統的應用,以降低高峰時段的用電需求。康體設施和水療區需要精確的濕度控制,這增加了對高效能空調的需求。為了降低生命週期成本,飯店業正在加速向熱回收通風系統和基於績效的維護合約轉型。

可支配所得增加和都市化

隨著都市化接近45%,河內和胡志明市等大都會圈的人口正以每年3-4%的速度成長。這推動了越南暖通空調市場向中高層公寓的擴張。家庭收入的成長使中產階級購屋者能夠將窗型冷氣更換為多區域變頻分離式空調系統,而高階專案也擴大預先安裝VRF系統。將於2025年1月起強制實施的TCVN 7830:2021最低性能標準正逐步淘汰恆速機型,並增加對變速平台的需求。開發商正在獲得綠色建築認證,並將高CSPF評分作為吸引購屋者的行銷手段。 LG、大金和三菱電機等廠商的在地化生產縮短了前置作業時間,並支援完善的售後服務網路,這對於住宅決策至關重要。

安裝和維護成本高昂

集中式冷卻器、VRF系統和無塵室空調需要專門的設計、風管和結構維修,這會使初始專案投資增加20-30%,限制了中小企業和預算敏感型開發商採用這些系統。由於需要定期處理冷媒、更換過濾器和調整數位控制設備,且所有這些都需要經過認證的技術人員,因此生命週期維護成本很高。符合QCVN 21:2015/BLDTBXH和ASHRAE標準的暖通空調專業人員短缺,推高了人事費用,並在發生故障時延長了停機時間。省會城市的小規模住宅用戶往往更傾向於選擇成本較低的定速機組,即使這會導致更高的能源費用。獲得優惠融資管道有限也進一步減緩了高效節能維修的普及。

細分市場分析

到2025年,空調設備將佔越南暖通空調(HVAC)市場銷售額的45.43%,預計到2031年,該細分市場將以7.43%的複合年成長率成長。在越南暖通空調市場,由於無管道迷你分離式空調能夠連接單相電源且所需結構改造極少,因此在住宅應用中佔據主導地位。商業設施的買家則更傾向於可變冷媒流量(VRF)系統,該系統能夠獨立控制每個區域並回收餘熱,從而提高開放式辦公室和共享辦公空間在部分負載下的效率。在飯店、醫院和製冷量超過500冷噸的高層辦公大樓中,對冷卻器的需求保持穩定,螺桿式和離心式壓縮機因其在滿負荷和部分負荷下均具有較高的性能係數(COP)而備受青睞。採用R-32冷媒和微通道冷凝器可降低冷媒負荷並提高傳熱係數。由於即插即用的便利性,屋頂式空調機組和終端空調仍然是小規模零售商店和獨立教室的標準配備。

由於熱帶地區氣溫低於18°C的情況較為罕見,暖氣設備市場仍屬於小眾市場。然而,度假村和醫院等優先考慮冷凝器廢熱能源回收的場所,正擴大採用熱泵熱水器。通風產品,包括專用室外空氣引入系統、熱回收通風機和基於二氧化碳的智慧需量控制,正隨著QCVN 04:2019/BXD法規對室外空氣引入和排放的監管日益嚴格而穩步成長。在無塵室和醫療隔離病房中,配備EC馬達和ULPA過濾器的風機過濾機組能夠滿足更嚴格的顆粒物和病原體標準。提供包含整合控制系統的暖通空調和通風系統的供應商,可以透過快速試運行和數據分析能力脫穎而出。

預計到2025年,越南暖通空調(HVAC)市場中,維修和升級改造將佔61.64%。這主要歸因於提高能源效率的需求,以及在QCVN 09:2017/BXD實施前建造的建築物引入數位化控制系統。 2010年以前建造的辦公大樓、飯店和零售設施的業主經常將恆速冷卻器和氣動控制系統更換為變頻驅動系統和建築管理系統,從而每年降低高達30%的電費。對年用電量超過1000噸當量(TOE)的設施進行強制性的VNEEP審計,可獲得優惠貸款和稅收優惠,將投資回收期縮短至五年以內,從而擴大了越南暖通空調市場的維修服務規模。住宅領域的需求主要來自中等收入家庭,他們正在用更安靜、支援Wi-Fi的智慧分離式空調取代現有的更換,這些空調可以整合到智慧家庭生態系統中。

受諸如守添樂天生態智慧城和河內附近東安智慧城等大型企劃的推動,新建建築的空調系統安裝預計將以7.89%的複合年成長率成長。整合設計團隊正在利用BIM和預製機電模組來縮短工期並最大限度地減少材料浪費。守添和芹苴的區域供冷可行性研究建議採用高效能冷卻器、蓄熱槽和三級循環系統來服務混合用途叢集。北部工業中心的待開發區工廠正在毛坯階段安裝符合ISO標準的無塵室和高靜壓空調機組,以避免高昂的維修成本。隨著建築業向綠色認證轉型,高效能空調系統增加的初始成本越來越能被其降低的營運成本和吸引租戶的優勢所抵消。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 旅遊和酒店業的蓬勃發展

- 可支配所得增加和都市化

- 政府對節能建築的獎勵

- 商業地產建設快速成長

- 在智慧城市計畫中引入區域供冷

- 外資潔淨室製造廠的擴張

- 市場限制因素

- 安裝和維護成本高昂

- 電費波動導致營運成本增加

- 技術純熟勞工短缺導致安裝前置作業時間延長。

- 國內低全球暖化潛勢冷媒的生產能力有限。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 關鍵績效指標

第5章 市場規模與成長預測

- 依設備類型

- 加熱設備

- 鍋爐和暖氣爐

- 熱泵

- 單元式加熱器

- 通風設備

- 空調(AHU)

- 空氣過濾器

- 風機盤管機組

- 加濕器和除濕器

- 空調設備

- 單元空調

- 管道式分離空調

- 無管道迷你分離式空調

- 整體式屋頂安裝

- 可變冷媒流量(VRF)系統

- 室內空調

- 包裝式終端空調

- 冷卻器

- 單元空調

- 加熱設備

- 按安裝類型

- 新建工程

- 維修和更換

- 最終用戶

- 住宅

- 商業的

- 產業

- 按建築類型(商業)

- 辦公大樓

- 醫療設施

- 飯店及休閒

- 零售商店和購物中心

- 教育機構

- 資料中心

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- LG Electronics Inc.

- Panasonic Holdings Corporation

- Carrier Global Corporation

- Samsung Electronics Co., Ltd.

- Hitachi Air Conditioning Ltd.

- Johnson Controls International plc(York)

- Toshiba Carrier Corporation

- Voltas Limited

- Gree Electric Appliances Inc.

- Trane Technologies plc

- Fujitsu General Ltd.

- Midea Group Co., Ltd.

- Sharp Corporation

- Refrigeration Electrical Engineering Corporation(REE)

- Goodman Manufacturing Company, LP

- Lennox International Inc.

- Electrolux AB

第7章 市場機會與未來展望

The Vietnam HVAC market size stood at USD 3.91 billion in 2026 and is projected to reach USD 5.48 billion by 2031, advancing at a 6.96% CAGR over the forecast period.

Robust GDP growth, accelerating urbanization, and a steady pipeline of mixed-use construction are enlarging the Vietnam HVAC market by broadening the customer base across residential, commercial, and industrial applications. Foreign direct investment into electronics assembly and semiconductor packaging is spurring demand for precision cleanroom air-handling, while the hospitality sector's post-pandemic rebound is boosting requirements for centralized chillers and low-noise guest-room systems. Government energy-efficiency incentives, together with mandatory performance standards for non-ducted air conditioners that took effect in 2025, are tilting preferences toward inverter-driven equipment and variable refrigerant flow platforms, reshaping competitive positioning in the Vietnam HVAC market. At the same time, tighter refrigerant regulations and district-cooling pilots are creating white-space opportunities for suppliers of low-GWP refrigerants, integrated controls, and performance-based service contracts.

Vietnam HVAC Market Trends and Insights

Growing Tourism And Hospitality Sector

Visitor arrivals are rebounding toward the 25 million target set for 2025, and the national hotel pipeline now tops 49,800 rooms concentrated in Ho Chi Minh City, Hanoi, Da Nang, and Phu Quoc. Hotels are specifying centralized chillers, VRF systems, and low-noise ductless units that meet QCVN 09:2017/BXD efficiency benchmarks, pushing contractors to incorporate inverter compressors and R-32 refrigerant. International brands require compliance with ASHRAE 55 thermal-comfort standards and ISO 7730 metrics, prompting the integration of building management systems to reduce peak electrical demand during high-occupancy periods. Wellness amenities and spa zones require precise humidity control, driving demand for high-efficiency air-handling units. The sector's focus on life-cycle cost savings is accelerating the shift toward energy-recovery ventilators and performance-based maintenance contracts.

Rising Disposable Income And Urbanization

Urbanization is near 45%, and metropolitan populations in Hanoi and Ho Chi Minh City are growing 3-4% annually, extending the Vietnam HVAC market across mid-rise condominiums and high-rise apartments. Rising household incomes enable middle-class buyers to upgrade from window units to multi-zone inverter mini-splits, while luxury projects increasingly pre-install VRF systems. TCVN 7830:2021 minimum performance thresholds, mandatory since January 2025, are phasing out fixed-speed models and reinforcing demand for variable-speed platforms. Developers align with green-building labels to attract buyers, using high CSPF scores as marketing levers. Localized production by LG, Daikin, and Mitsubishi Electric reduces lead times and supports after-sales service networks that are critical to residential purchase decisions.

High Installation And Maintenance Costs

Centralized chillers, VRF platforms, and cleanroom air-handling units require specialized engineering, ductwork fabrication, and structural adaptations that can add 20-30% to project capital outlays, restricting adoption among SMEs and budget-sensitive developers. Lifecycle service costs are elevated by periodic refrigerant handling, filter replacement, and digital controls calibration, all of which demand certified technicians. A shortage of HVAC professionals trained to QCVN 21:2015/BLDTBXH and ASHRAE standards pushes wages upward and extends downtime when failures occur. Smaller residential customers in secondary cities gravitate toward fixed-speed units that cost less despite higher energy bills. Limited access to concessional financing further slows the uptake of high-efficiency retrofits.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth Of Commercial Real-Estate Construction

- Expansion Of Foreign-Invested Cleanroom Manufacturing Plants

- Volatile Electricity Tariffs Increasing Operating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-conditioning equipment captured 45.43% of the Vietnam HVAC market revenue share in 2025, and the segment is poised to grow at a 7.43% CAGR through 2031. In the Vietnam HVAC market, ductless mini-splits dominate residential applications because they can be wired to single-phase power and require minimal structural work. Commercial buyers favor variable refrigerant flow systems that provide zone independence and recover waste heat, improving part-load efficiency across open-plan offices and co-working spaces. Chiller demand is stable in hotels, hospitals, and high-rise offices where plant capacities exceed 500 TR, with screw and centrifugal compressors preferred for high COPs at both full and part load. The shift toward R-32 refrigerant and microchannel condensers is reducing charge volumes and improving heat-transfer coefficients. Packaged rooftop units and terminal air conditioners remain staples in small retail and stand-alone classrooms owing to their plug-and-play serviceability.

Heating equipment remains a niche because tropical temperatures seldom drop below 18 °C, but heat-pump water heaters are gaining traction in resorts and hospitals that value energy recovered from condenser waste heat. Ventilation products, including dedicated outdoor-air systems, energy-recovery ventilators, and smart CO2-based demand control, are registering steady gains as QCVN 04:2019/BXD tightens fresh-air and smoke-extraction mandates. In cleanrooms and healthcare isolation wards, fan-filter units with EC motors and ULPA filters meet stricter particulate and pathogen thresholds. Suppliers that bundle air-conditioning and ventilation equipment with unified controls can differentiate on commissioning speed and data analytics capabilities.

Retrofit and replacement accounted for 61.64% of the Vietnam HVAC market in 2025, as buildings erected before QCVN 09:2017/BXD seek energy-efficiency upgrades and digital controls. Owners of pre-2010 offices, hotels, and retail centers frequently replace fixed-speed chillers and pneumatic controls with inverter-driven systems and building management systems, cutting annual electricity bills by as much as 30%. VNEEP audit mandates for facilities surpassing 1,000 TOE per year unlock concessional loans and tax incentives that shorten payback to fewer than five years, expanding the Vietnam HVAC market size for retrofit services. Residential demand is driven by mid-income households upgrading to quieter, Wi-Fi-enabled mini-splits that integrate with smart-home ecosystems.

New-build installations are projected to grow at a 7.89% CAGR, powered by mega-projects such as Thu Thiem's Lotte Eco Smart City and Dong Anh Smart City near Hanoi. Integrated design teams employ BIM and prefabricated MEP modules to accelerate schedules and minimize material waste. District-cooling feasibility studies in Thu Thiem and Can Tho favor high-efficiency chillers, thermal storage tanks, and tertiary loops serving mixed-use clusters. Greenfield factories in northern industrial hubs install ISO-compliant cleanrooms and high-static-pressure air-handling units during the shell-and-core stage to avoid costly retrofits. As construction shifts toward green certification, first-cost premiums for high-efficiency HVAC are increasingly justified by lower operational expenditure and tenant attraction.

The Vietnam HVAC Market Report is Segmented by Equipment Type (Air-Conditioning Equipment, Heating Equipment, and Ventilation Equipment), Installation Type (New Construction, and Retrofit and Replacement), End User (Residential, Commercial, and Industrial), and Building Type (Office Buildings, Data Centers, Hospitality and Leisure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- LG Electronics Inc.

- Panasonic Holdings Corporation

- Carrier Global Corporation

- Samsung Electronics Co., Ltd.

- Hitachi Air Conditioning Ltd.

- Johnson Controls International plc (York)

- Toshiba Carrier Corporation

- Voltas Limited

- Gree Electric Appliances Inc.

- Trane Technologies plc

- Fujitsu General Ltd.

- Midea Group Co., Ltd.

- Sharp Corporation

- Refrigeration Electrical Engineering Corporation (REE)

- Goodman Manufacturing Company, L.P.

- Lennox International Inc.

- Electrolux AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Tourism and Hospitality Sector

- 4.2.2 Rising Disposable Income and Urbanization

- 4.2.3 Government Incentives for Energy-Efficient Buildings

- 4.2.4 Rapid Growth of Commercial Real-Estate Construction

- 4.2.5 Adoption of District Cooling in Smart-City Projects

- 4.2.6 Expansion of Foreign-Invested Cleanroom Manufacturing Plants

- 4.3 Market Restraints

- 4.3.1 High Installation and Maintenance Costs

- 4.3.2 Volatile Electricity Tariffs Increasing Operating Costs

- 4.3.3 Skilled Labor Shortage Inflating Installation Lead Times

- 4.3.4 Limited Domestic Production of Low-GWP Refrigerants

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Key Performance Indicators

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Heating Equipment

- 5.1.1.1 Boilers and Furnaces

- 5.1.1.2 Heat Pumps

- 5.1.1.3 Unitary Heaters

- 5.1.2 Ventilation Equipment

- 5.1.2.1 Air Handling Units (AHUs)

- 5.1.2.2 Air Filters

- 5.1.2.3 Fan Coil Units

- 5.1.2.4 Humidifiers and Dehumidifiers

- 5.1.3 Air-Conditioning Equipment

- 5.1.3.1 Unitary Air Conditioners

- 5.1.3.1.1 Ducted Splits

- 5.1.3.1.2 Ductless Mini-Splits

- 5.1.3.1.3 Packaged Rooftops

- 5.1.3.1.4 Variable Refrigerant Flow (VRF) Systems

- 5.1.3.2 Room Air Conditioners

- 5.1.3.3 Packaged Terminal Air Conditioners

- 5.1.3.4 Chillers

- 5.1.3.1 Unitary Air Conditioners

- 5.1.1 Heating Equipment

- 5.2 By Installation Type

- 5.2.1 New Construction

- 5.2.2 Retrofit / Replacement

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Building Type (Commercial)

- 5.4.1 Office Buildings

- 5.4.2 Healthcare Facilities

- 5.4.3 Hospitality and Leisure

- 5.4.4 Retail Stores and Malls

- 5.4.5 Educational Institutions

- 5.4.6 Data Centers

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 LG Electronics Inc.

- 6.4.4 Panasonic Holdings Corporation

- 6.4.5 Carrier Global Corporation

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Hitachi Air Conditioning Ltd.

- 6.4.8 Johnson Controls International plc (York)

- 6.4.9 Toshiba Carrier Corporation

- 6.4.10 Voltas Limited

- 6.4.11 Gree Electric Appliances Inc.

- 6.4.12 Trane Technologies plc

- 6.4.13 Fujitsu General Ltd.

- 6.4.14 Midea Group Co., Ltd.

- 6.4.15 Sharp Corporation

- 6.4.16 Refrigeration Electrical Engineering Corporation (REE)

- 6.4.17 Goodman Manufacturing Company, L.P.

- 6.4.18 Lennox International Inc.

- 6.4.19 Electrolux AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

測試、調整和平衡服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用途、地區和競爭對手分類,2021-2031 年

測試、調整和平衡服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用途、地區和競爭對手分類,2021-2031 年 暖通空調幫浦市場規模、佔有率和成長分析:按泵浦類型、應用、容量、技術、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測

暖通空調幫浦市場規模、佔有率和成長分析:按泵浦類型、應用、容量、技術、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測 暖氣片市場規模、佔有率和成長分析:按產品類型、材質、應用和地區分類-2026-2033年產業預測

暖氣片市場規模、佔有率和成長分析:按產品類型、材質、應用和地區分類-2026-2033年產業預測 2026-2030年全球工業暖通空調市場

2026-2030年全球工業暖通空調市場 2026-2030年全球暖氣、通風和空調(HVAC)售後市場

2026-2030年全球暖氣、通風和空調(HVAC)售後市場 HVAC市場商機、成長要素、產業趨勢分析及2026-2035年預測。

HVAC市場商機、成長要素、產業趨勢分析及2026-2035年預測。 暖通空調租賃設備市場:按設備類型、租賃期限、動力來源和最終用戶分類-2026-2032年全球預測

暖通空調租賃設備市場:按設備類型、租賃期限、動力來源和最終用戶分類-2026-2032年全球預測 2026年全球氫動力攜帶式可攜式空調市場報告

2026年全球氫動力攜帶式可攜式空調市場報告 HVAC幫浦市場規模、佔有率和趨勢分析報告:按階段、泵浦類型、應用、地區和細分市場預測(2026-2033年)暖通空調電纜市場:2026-2032年全球市場預測(依產品類型、額定電壓、導體材料、絕緣類型及應用分類)

HVAC幫浦市場規模、佔有率和趨勢分析報告:按階段、泵浦類型、應用、地區和細分市場預測(2026-2033年)暖通空調電纜市場:2026-2032年全球市場預測(依產品類型、額定電壓、導體材料、絕緣類型及應用分類)