|

市場調查報告書

商品編碼

2035014

5G專用網路:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)5G Private Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

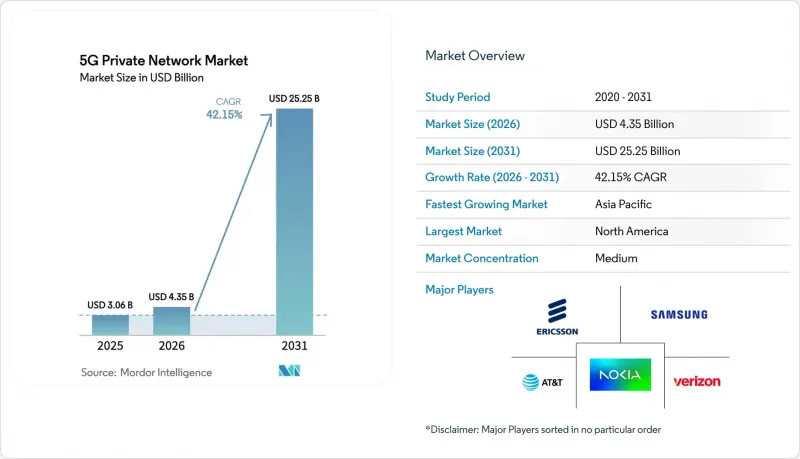

預計 5G 專用網路市場將從 2025 年的 30.6 億美元成長到 2026 年的 43.5 億美元,然後在 2031 年達到 252.5 億美元,2026 年至 2031 年的複合年成長率為 42.15%。

人們對確定性蜂窩網路連線(而非 Wi-Fi)的偏好日益成長,5G 獨立組網核心網的全球部署,以及區域許可頻率分配方案的放寬,都推動了這一擴張。 5G工業IoT模組和小型基地台價格的下降進一步降低了進入門檻,使中型製造商、港口和公共產業能夠更有理由進行新的部署。網路供應商和超大規模資料中心業者之間的策略合作,透過結合邊緣運算和資料主權工作負載的託管服務,正在加速 5G 的普及。所有這些因素共同推動 5G 專網市場保持兩位數的持續成長,同時也重塑各地區和各產業的企業連結策略。

全球5G專用網路市場趨勢與洞察

成熟的 5G SA 核心網可用於企業級 SASE 整合

雲端原生 5G 獨立組網 (SA) 核心網現已整合 SASE(安全計費系統)功能,使企業能夠透過單一管理介面,在其 OT(營運技術)和 IT 領域應用零信任策略。愛立信和谷歌雲端聯合運營“5G 核心網即服務”,使製造商無需現場 EPC 專家即可實現彈性擴展。微軟也採用了類似的模式,將完整的 5G 核心網路整合到 Azure Stack Edge 中。這使得受監管的設施能夠透過 Azure 入口網站管理其網路,同時將資料保留在本地。整合的身份管理、網路分段和流量最佳化功能縮短了多站點工廠和物流中心的整合時間。早期採用者報告稱,由於策略更新會自動反映到所有站點,因此部署週期更短,維護成本更低。這些優勢的結合提高了可實現的投資報酬率閾值,並擴大了 5G 專用網路市場的潛在基本客群。

700 MHz、CBRS 和區域頻寬頻寬的放鬆管制

共用且頻譜頻譜沒有全國性行動牌照的業者能夠建立專用網路。美國聯邦通訊委員會 (FCC) 擴展了 CBRS 的相關規定,延長了傳輸時區並縮小了動態保護區,從而確保了公共產業和校園等場所無線環境的可預測性。在日本的本地 5G 模式下,已頒發了 153 張 Sub-6 GHz 頻段的牌照,這表明簡化的流程能夠促進企業網路的快速部署。根據美國國家電信和資訊管理局 (NTIA) 的數據,自 2021 年以來,已有超過 27 萬台新的 CBRS 設備被激活,其中許多設備用於本地製造業叢集。獲得價格合理的頻段可以降低整體擁有成本 (TCO),鼓勵通訊業者提供批發頻譜切片,並推動 5G 專用網路市場在業界的更廣泛應用。

特定產業應用情境下多頻段認證的 5G 設備短缺

企業通常需要能夠在Sub-6GHz和毫米波頻段漫遊,同時符合嚴格安全和無菌標準的設備。然而,極少有供應商能夠提供在所有目標頻寬都經過認證的可靠平板電腦、相機或AR頭顯,這迫使他們採用混合網路設計,從而增加了支援成本。由於醫療設備核准這項額外的監管障礙,醫療產業的部署更具挑戰性。在認證覆蓋範圍擴大之前,設備短缺將減緩新產業進入5G專用網路市場的步伐。

細分市場分析

到2025年,硬體將佔5G專網市場的47.20%,這反映了對無線設備、演進封包核心網路和邊緣運算叢集的初始投資。然而,隨著企業越來越傾向於託管生命週期模式,服務領域預計將以44.10%的複合年成長率成長,超過設備銷售的成長速度。諾基亞表示,採用服務主導的部署模式,快速部署和持續最佳化能夠幫助78%的客戶在六個月內實現投資回報。這種轉變反映了雲端原生編配的普及,它正在將價值從硬體轉移到軟體和支援。隨著複雜性的增加,託管偵測與回應、效能調優和應用程式上線將成為核心收入來源。因此,到2030年,服務領域與硬體領域的收入差距將縮小,並重塑5G專網市場的供應商獲利模式。

軟體介於硬體和服務之間,提供策略控制、網路切片和數位雙胞胎分析,將無線數據轉化為商業洞察。低程式碼編配使OT工程師無需向營運商提交工單即可為新的生產線啟動網路切片。從長遠來看,軟體的利潤率可能高於硬體和服務,但其成長速度將與平台採用率曲線保持一致。這些趨勢共同確保5G專網產業將持續保持多元化的收入來源,並且其綜合價值成長最為迅速。

到2025年,Sub-6 GHz頻段將佔據5G專網市場61.10%的佔有率。這是因為其1公里的小區覆蓋半徑使其適用於大規模工廠、礦場和園區。由於天線面積較小,中頻段也成為堅固手持終端機和感測器的首選。毫米波(mmWave)雖然覆蓋範圍僅限於數十米,但隨著工廠採用高清機器視覺和擴增實境(AR)維護技術來管理工作站,其年複合成長率(CAGR)高達43.80%。混合部署模式正在興起,中波頻段提供廣泛的覆蓋範圍,而毫米波疊加層則為組裝單元提供Gigabit級通訊。支援雙頻無線電的開放式無線接取網路(Open-RAN)藍圖可望簡化此類混合拓撲結構並加速其部署。

這些細微頻段的利用將進一步拉大供應商之間的差距。針對反射性室內空間波束成形最佳化的無線存取網(RAN)供應商將贏得毫米波頻段的競標,而擁有宏無線電專案實力雄厚的老牌公司將在6GHz以下頻段的競標中佔據主導地位。在整個預測期內,儘管毫米波的市佔率將會上升,但仍將低於中波水平,因為對於許多現有工廠而言,部署高密度小型基地台網路並不經濟。儘管如此,這些頻段的組合工具包將鞏固私有5G在工業數位化領域相對於Wi-Fi 7的優越升級路徑地位。

《5G專用網路市場報告》按組件(硬體、軟體、服務)、頻率(6GHz以下、毫米波[24GHz以上])、企業規模(中小企業、大型企業)、產業(製造業、能源和公共產業、運輸和物流、石油和天然氣、醫療保健、國防和公共安全等)和地區進行細分。

區域分析

預計到2025年,北美將佔據5G專用網路市場30.50%的佔有率,這得益於可用的CBRS頻段、早期工業物聯網試點計畫以及聯邦政府對關鍵基礎設施現代化建設的大力投入。中西部和墨西哥灣沿岸地區的製造業叢集正迅速從Wi-Fi遷移到5G網路,因為蜂窩通訊能夠為自主機器人提供無干擾的移動性。公共安全機構也加大投資,Verizon已在29個城市為緊急應變人員提供專用的5G網路切片,以確保在網路擁塞期間的優先通訊。

亞太地區預計將實現44.00%的複合年成長率,並預計在2031年之前縮小領先差距。日本監管機構正在分配Sub-6 GHz和4.7 GHz頻段的專用本地授權頻段,這將使兩年內能夠建立超過150個企業網路。在中國,確定性調度和RedCap設備等5.5G(5G-Advanced)功能的試點計畫正在進行中,以支援汽車和採礦業的大規模園區部署。印度等新興經濟體正利用「生產連結獎勵計畫(PLI)」計劃,將私有5G引入新的半導體工廠和物流園區,進一步推動區域發展動能。

在歐洲,由於頻譜使用成本持續高昂以及各成員國產業政策不盡相同,5G技術的普及速度緩慢但穩定地推進。儘管如此,在德國「工業4.0」補貼和法國智慧城市示範計畫等措施的推動下,市場需求仍在持續成長。裡加港為自主海上無人機提供的專用5G網路表明,歐盟海上走廊的覆蓋範圍可延伸至離岸100英里,這是Wi-Fi連接無法實現的。南美洲、中東和非洲的5G技術仍處於起步階段,但石油、天然氣和採礦業的早期示範表明,隨著設備普及率的提高,市場需求將會成長。綜合來看,各區域的趨勢表明,在預測期內,5G專用網路市場的廣度和深度都將得到提升。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 成熟的 5G SA 核心網可用於企業級 SASE 整合

- 放寬 700 MHz、CBRS 和區域授權頻寬。

- 與 5G工業IoT模組和專用 RAN小型基地台的價格正在下降。

- 透過超大規模資料中心業者)。

- 針對關鍵基礎設施的新IT/OT網路安全法規

- 為現有設備的工業維修提供供應商融資計劃

- 市場限制因素

- 特定產業缺乏多頻段認證的5G設備

- 全球頻寬框架碎片化正在減緩漫遊互通性。

- 中型整合商缺乏整合複雜系統的能力

- 延長現有設備流程自動化維修的投資報酬率週期

- 價值鏈/供應鏈分析

- 技術展望

- 監理情勢

- 波特五力分析

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 頻寬

- 低於 6 GHz

- 毫米波(24 GHz 以上)

- 按公司規模

- 小型企業

- 大公司

- 按行業

- 製造業

- 能源與公共產業

- 運輸/物流

- 石油和天然氣

- 衛生保健

- 國防/公共安全

- 企業和校園

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Qualcomm Technologies, Inc.

- NEC Corporation

- NTT Ltd./NTT DOCOMO

- Verizon Communications Inc.

- ATandT Inc.

- Deutsche Telekom AG

- Mavenir Systems Inc.

- Altiostar(Rakuten)

- Rakuten Symphony

- Fujitsu Limited

- Siemens AG

- Bosch Rexroth AG

- Amazon Web Services Inc.

第7章 市場機會與未來展望

The 5G Private Network Market size is expected to grow from USD 3.06 billion in 2025 to USD 4.35 billion in 2026 and is forecast to reach USD 25.25 billion by 2031 at 42.15% CAGR over 2026-2031.

Growing preference for deterministic cellular connectivity over Wi-Fi, the global roll-out of 5G Standalone cores, and liberalized local-licence spectrum schemes underpin this expansion. Declining prices of 5G industrial IoT modules and small cells further lower entry barriers, allowing mid-tier manufacturers, ports, and utilities to justify new deployments. Strategic collaborations between network vendors and hyperscalers accelerate adoption by bundling managed services with edge compute for data-sovereign workloads. Together, these forces position the 5G private network market for sustained double-digit growth while reshaping enterprise connectivity strategies across regions and verticals.

Global 5G Private Network Market Trends and Insights

Mature 5G SA Core Availability for Enterprise SASE Integration

Cloud-native 5G Standalone cores now ship with built-in SASE functions, allowing enterprises to apply zero-trust policies across OT and IT domains from a single pane of glass. Ericsson and Google Cloud jointly run 5G Core-as-a-Service, giving manufacturers elastic scaling without on-site EPC specialists. Microsoft mirrors this model by embedding a full 5G core inside Azure Stack Edge so that regulated facilities can retain data on-prem while managing the network from the Azure portals. Unified identity, segmentation, and traffic optimisation cut integration time for multi-site factories and logistics hubs. Early adopters report faster rollout cycles and reduced maintenance overhead because policy updates propagate automatically to every site. Together, these efficiencies raise the attainable ROI threshold, broadening the addressable base for the 5G private network market.

700 MHz, CBRS & Local-Licence Spectrum Liberalisation

Shared and lightly licensed spectrum unlocks private networks for entities that do not own nationwide mobile concessions. The FCC's expanded CBRS rules lengthen transmission windows and trim Dynamic Protection zones, giving utilities and campuses predictable radio conditions. Japan's local 5G model has already issued 153 Sub-6 GHz licences, proving that simplified processes can fast-track enterprise networks. NTIA data show more than 270,000 new CBRS device activations since 2021, many in rural manufacturing clusters. Access to affordable spectrum lowers total cost of ownership, pressures operators to offer wholesale slices, and propels the 5G private network market toward wider vertical adoption.

Scarcity of Multi-Band Certified 5G Devices for Vertical-Specific Use Cases

Enterprises often require devices that roam across Sub-6 GHz and mmWave bands while meeting stringent safety or sterility norms. Yet only a handful of suppliers certify rugged tablets, cameras, or AR headsets across all target bands, forcing hybrid network designs that raise support costs. Healthcare deployments struggle even more because medical device approvals add another regulatory layer. Until broader certification coverage emerges, device scarcity will temper the pace at which new verticals join the 5G private network market.

Other drivers and restraints analyzed in the detailed report include:

- Falling Price of 5G-Industrial IoT Modules & Private-RAN Small Cells

- Edge-Native 5G Network-as-a-Service Offers from Hyperscalers

- Complex Systems-Integration Skill Gap at Mid-Tier Integrators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware commanded 47.20% of the 5G private network market in 2025, reflecting the upfront spend on radios, evolved packet cores, and edge compute clusters. Yet, Services are projected to grow at a 44.10% CAGR, outpacing equipment sales as enterprises favour managed lifecycle models. Nokia finds 78% of customers achieve payback within six months when adopting a service-led rollout, thanks to faster commissioning and continuous optimisation. The shift also mirrors the spread of cloud-native orchestration, which moves value from boxes to software and support. As complexity rises, managed detection and response, performance tuning, and application onboarding become core revenue streams. Consequently, Services will narrow the revenue gap with Hardware by 2030, reshaping vendor monetisation across the 5G private network market.

Software sits between the two, providing policy control, network slicing, and digital twin analytics that translate radio data into business insights. Low-code orchestration lets OT engineers spin up slices for new production lines without ticketing an operator. Over time, Software margins are likely to exceed both Hardware and Services, but their growth pace will track platform adoption curves. Together, these dynamics ensure the 5G private network industry remains a multi-revenue-stream arena where integration value grows fastest.

Sub-6 GHz held 61.10% share of the 5G private network market size in 2025 because one-kilometre cell radii suit large plants, mines, and campuses. Rugged handhelds and sensors also favour mid-band because antenna footprints stay small. mmWave, while confined to tens-of-metre footprints, posts a 43.80% CAGR as factories deploy high-definition machine vision and AR maintenance at workstations. Hybrid deployments emerge, mid-band provides blanket coverage, mmWave overlays pump gigabits to assembly cells. Open-RAN roadmaps that support dual-band radios promise to simplify such mixed topologies, boosting uptake.

This nuanced spectrum play widens vendor differentiation. RAN suppliers with beamforming optimisations for reflective indoor spaces win mmWave bids, whereas incumbents strong in macro radio planning dominate Sub-6 GHz tenders. Over the forecast horizon, mmWave's share will rise yet remain below mid-band because many brownfield plants cannot justify dense small-cell grids. Even so, the combined spectrum toolkit cements private 5G as a superior upgrade path over Wi-Fi 7 for industrial digitalisation.

The 5G Private Network Market Report is Segmented by Component (Hardware, Software, and Services), Frequency (Sub-6 GHz, Mmwave [More Than 24 GHz]), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Vertical (Manufacturing, Energy and Utilities, Transportation and Logistics, Oil and Gas, Healthcare, Defense and Public Safety, and More), and Geography.

Geography Analysis

North America captured 30.50% of the 5G private network market in 2025, thanks to ready CBRS spectrum, early IIoT pilots, and strong federal funding for critical-infrastructure modernisation. Manufacturing clusters in the Midwest and Gulf Coast rapidly migrate from Wi-Fi because cellular provides interference-immune mobility for autonomous robots. Public-safety agencies also invest, with Verizon offering dedicated 5G slices for first responders across 29 cities, ensuring priority communications during congestion.

Asia-Pacific is forecast to record a 44.00% CAGR, narrowing the leadership gap by 2031. Japan's regulator issues dedicated local-licence spectrum in both Sub-6 GHz and 4.7 GHz bands, prompting more than 150 enterprise networks within two years. China pilots 5.5G (5G-Advanced) features such as deterministic scheduling and RedCap devices, underpinning large-scale campus deployments in automotive and mining. Emerging economies like India ride the Production-Linked Incentive scheme to embed private 5G in new semiconductor fabs and logistics parks, further boosting regional momentum.

Europe follows with a slower but steady uptake as spectrum fees remain higher and industrial policy varies by member state. Nonetheless, initiatives like Germany's Industrie 4.0 subsidies and France's smart-city pilots keep demand rising. The Port of Riga's private 5G for autonomous sea drones proves how EU maritime corridors can extend coverage 100 miles offshore, a feat unviable with Wi-Fi links. South America and the Middle East & Africa remain in nascent stages, yet early oil, gas, and mining proofs hint at rising demand once device availability widens. Taken together, regional dynamics ensure the 5G private network market gains depth as well as breadth over the forecast horizon.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Qualcomm Technologies, Inc.

- NEC Corporation

- NTT Ltd./NTT DOCOMO

- Verizon Communications Inc.

- ATandT Inc.

- Deutsche Telekom AG

- Mavenir Systems Inc.

- Altiostar (Rakuten)

- Rakuten Symphony

- Fujitsu Limited

- Siemens AG

- Bosch Rexroth AG

- Amazon Web Services Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mature 5G SA core availability for enterprise SASE integration

- 4.2.2 700 MHz, CBRS and local-licence spectrum liberalisation

- 4.2.3 Falling price of 5G-Industrial IoT modules and private-RAN small cells

- 4.2.4 Edge-native 5G network-as-a-service offers from hyperscalers

- 4.2.5 New IT/OT cybersecurity mandates in critical infrastructure

- 4.2.6 Vendor financing programs for brownfield industrial retrofits

- 4.3 Market Restraints

- 4.3.1 Scarcity of multi-band certified 5G devices for vertical-specific use cases

- 4.3.2 Fragmented global spectrum frameworks delaying roaming interoperability

- 4.3.3 Complex systems-integration skill gap at mid-tier integrators

- 4.3.4 Prolonged ROI cycles for brownfield process-automation retrofits

- 4.4 Value/Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Frequency

- 5.2.1 Sub-6 GHz

- 5.2.2 mmWave (More than 24 GHz)

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Vertical

- 5.4.1 Manufacturing

- 5.4.2 Energy and Utilities

- 5.4.3 Transportation and Logistics

- 5.4.4 Oil and Gas

- 5.4.5 Healthcare

- 5.4.6 Defense and Public Safety

- 5.4.7 Enterprises and Campus

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Telefonaktiebolaget LM Ericsson

- 6.4.2 Nokia Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 ZTE Corporation

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Juniper Networks, Inc.

- 6.4.8 Qualcomm Technologies, Inc.

- 6.4.9 NEC Corporation

- 6.4.10 NTT Ltd./NTT DOCOMO

- 6.4.11 Verizon Communications Inc.

- 6.4.12 ATandT Inc.

- 6.4.13 Deutsche Telekom AG

- 6.4.14 Mavenir Systems Inc.

- 6.4.15 Altiostar (Rakuten)

- 6.4.16 Rakuten Symphony

- 6.4.17 Fujitsu Limited

- 6.4.18 Siemens AG

- 6.4.19 Bosch Rexroth AG

- 6.4.20 Amazon Web Services Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

私人 5G 市場(2026-2030 年):機會、挑戰、策略與預測

私人 5G 市場(2026-2030 年):機會、挑戰、策略與預測 2026年第五代(5G)企業專用網路全球市場報告2026年全球私有5G設備市場報告2026年5G新型無線全球市場報告

2026年第五代(5G)企業專用網路全球市場報告2026年全球私有5G設備市場報告2026年5G新型無線全球市場報告 公共網路叢集收發器市場按產品類型、技術、頻率類型、最終用戶、應用和分銷管道分類,全球預測(2026-2032年)

公共網路叢集收發器市場按產品類型、技術、頻率類型、最終用戶、應用和分銷管道分類,全球預測(2026-2032年) 5G企業專用網路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類

5G企業專用網路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類 全球私有5G市場,2025-2029年

全球私有5G市場,2025-2029年 5G新空口市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、工作頻率、架構、應用、產業、區域和競爭格局分類,2021-2031年預測

5G新空口市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、工作頻率、架構、應用、產業、區域和競爭格局分類,2021-2031年預測 2032年專用LTE和5G企業網路市場預測:按組件、部署模式、頻段、網路技術、組織規模、最終用戶和地區分類的全球分析全球私人 5G 和企業連接市場:預測至 2032 年—按組件、部署方式、頻寬、組織規模、頻率類型、最終用戶和地區進行分析

2032年專用LTE和5G企業網路市場預測:按組件、部署模式、頻段、網路技術、組織規模、最終用戶和地區分類的全球分析全球私人 5G 和企業連接市場:預測至 2032 年—按組件、部署方式、頻寬、組織規模、頻率類型、最終用戶和地區進行分析