|

市場調查報告書

商品編碼

2034998

日本資料中心建置:市場佔有率分析、產業趨勢與統計及成長預測(2026-2032)Japan Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2032) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

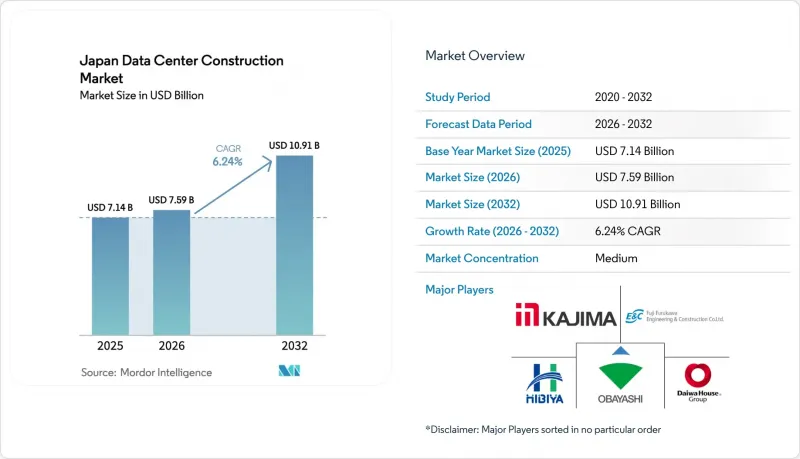

日本資料中心建設市場預計將從 2025 年的 71.4 億美元成長到 2026 年的 75.9 億美元,然後從 2026 年到 2032 年以 6.24% 的複合年成長率成長,到 2032 年達到 109.1 億美元。

在超大規模資料中心投資增加、強制主權雲端部署以及邊緣運算部署的推動下,大型專案規劃不斷推進。同時,地震工程的專業知識和液冷技術的創新正在增強企業的競爭優勢。來自日本房地產投資信託基金(J-REITs)的穩定資金流入,以及《經濟安全促進法》提供的補貼,持續緩解了國內營運商的資金籌措。關西電力公司和其他電力公司的輸電網升級計畫正在降低電力供應風險,高壓配電設計也適應了人口密集地區的需求。然而,技術純熟勞工短缺和地價飆升正在減緩建設速度,促使企業尋求模組化設計方案,並選擇在大都會圈以外的地區建設位置以控制成本。營運商越來越傾向於簽訂可再生能源購電協議,以保護利潤率免受價格波動的影響,這推動了能源供應向綠色能源豐富的北方地區的轉移。

日本資料中心建置市場趨勢與洞察

加速雲端運算、人工智慧和巨量資料工作負載

生成式人工智慧專案的激增導致機架密度超過100kW,電力需求成長高達20%,迫使營運商採用液冷系統。Softbank Corporation位於苫小牧的300MW園區目前正在建設中,樹立了新的標桿,並力爭實現100%可再生能源供電。櫻花網際網路等GPU雲端服務供應商預計到2025年利潤將成長476.3%,這印證了強勁的需求驅動力。日本大型石油公司出光興產目前正在供應可將冷卻能耗降低90%的液冷劑,為建構永續人工智慧基礎設施的區域價值鏈奠定了基礎。

美國和國內主要公司建設超大規模園區

AWS已累計2.26兆日圓用於2027年前的雲端基礎建設,預計每年將創造30,500個就業崗位,並對日本GDP產生5.57兆日圓的影響。 Oracle的80億美元計畫則專注於滿足客戶在東京和大阪的資料主權需求。在日本國內,KDDI和夏普正計劃透過合作打造亞洲最大的雲端園區之一,而EdgeConnex則在大阪部署140兆瓦的設施用於人工智慧叢集。這些多年期項目正在推動建築訂單的成長,並加劇對技術承包商的競爭。

電網瓶頸和電費飆漲

關西電力公司計劃投資超過1,500億日元,興建四座變電站,2026年起為新校區供電。電力公司面臨併網等待時間過長和電價差異的問題,北海道電價最高,北陸電價最低。成本上漲擠壓了利潤空間,而水冷技術的引進也導致電力消耗量歷史新高。一些公司正在簽訂可再生能源購電協議(PPA)或自建發電設施以規避風險。

細分市場分析

至2025年,電力基礎設施將佔銷售額的37.62%,並透過高壓開關設備和母線槽的升級改造,構成日本資料中心建設市場佔有率的基礎。服務業雖然規模較小,但預計到2032年將實現8.05%的複合年成長率,因為營運商願意為抗震設計、液冷設計和人工智慧工作負載佈局最佳化支付溢價。CanonIT解決方案公司位於東京西部的資料中心目前支援100kVA液冷機架,展示了混合冷卻技術的整合應用。自2021年以來,建築材料價格上漲了21%至24%,企業正轉向模組化施工和預製電力機房,以縮短交貨時間。

日本資料中心建置市場服務領域的擴張反映了生成式人工智慧普及所驅動的對容量規劃、試運行和維修諮詢服務的需求。儘管機械基礎設施正朝著絕緣液和晶片直接冷卻的方向發展,但IT基礎設施依然穩健,儘管越來越多的企業向雲端遷移,GPU伺服器的訂單仍在持續成長。

至2025年,三級資料中心將佔據日本資料中心建置市場56.42%的佔有率,主要服務於注重成本的企業和託管用戶。雖然四級資料中心專案數量較少,但預計到2032年將以8.43%的複合年成長率成長,因為超大規模營運商需要更高的資本投入才能不間斷地訓練人工智慧模型。大林組採用主動式隔震結構和超高強度鋼材,以確保地震多發地區四級資料中心的運作。

日本的Tier IV資料中心建設市場主要集中在東京-大阪走廊,該地區高昂的土地成本使得高密度、高可用性的設計方案成為可能。同時,隨著租戶將工作負載遷移到對容錯能力要求更高的雲端平台,Tier I和Tier II傳統資料中心的使用率正在下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速雲端運算、人工智慧和巨量資料工作負載

- 美國及國內主要雲端運算公司正在擴建超大規模園區。

- 關於主權雲端和資料居住的法規

- 5G的普及帶動了主要區域城市對邊緣資料中心的需求。

- 日本房地產投資信託基金資金流入用於建設毛坯資料中心的土地(表活動)

- 大型設施中用於降低風險的隔震技術(一個未充分討論的領域)

- 市場限制因素

- 電網瓶頸和電費飆漲

- 三級/四級認證的機電(機械、電氣和管道)技術人員短缺

- 環境許可核准流程漫長,並遭到當地居民的反對。

- 東京-千葉-神奈川走廊地價飆升(一個被忽視的趨勢)

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 日本資料中心建置關鍵統計數據

- 2023年及2024年日本資料中心總裝置容量(兆瓦)

- 2025-2030年日本在建IT總負荷(兆瓦)

- 日本資料中心建置的平均資本支出(Capex)和營運費用(Opex)

- 日本投資資料中心基礎建設的頂尖公司

第5章 市場規模及成長預測(價值,10億美元)

- 透過基礎設施

- 電力基礎設施

- 配電解決方案

- 配電單元

- 切換裝置

- 其他

- 備用電源解決方案

- UPS

- 發電機

- 配電解決方案

- 機械基礎設施

- 冷卻系統

- 液冷

- 空冷式

- 機架和機櫃

- 其他機械和設備

- 冷卻系統

- IT基礎設施

- 伺服器

- 貯存

- 其他IT基礎設施

- 一般建築

- 服務

- 設計與諮詢

- 一體化

- 支援和維護

- 電力基礎設施

- 基於層級的標準

- 一級和二級

- 三級

- Tier IV

- 依資料中心類型

- 託管資料中心

- 超大規模/自建資料中心

- 其他(企業/邊緣/模組化)

- 按最終用戶行業分類

- 銀行、金融服務、保險

- 資訊科技/通訊

- 政府/國防

- 衛生保健

- 其他最終用戶

第6章 競爭情勢

- 市佔率分析

- 公司簡介

- Obayashi Corporation

- Taisei Corporation

- Kajima Corporation

- Shimizu Corporation

- Takenaka Corporation

- Tokyu Construction

- Toda Corporation

- Maeda Corporation

- Daiwa House Industry Co., Ltd.

- Penta-Ocean Construction

- Fuji Furukawa Engineering and Construction

- Nishimatsu Construction

- Sumitomo Mitsui Construction

- Hazama Ando

- Kitano Construction

- Mirai-Build(Mirait Holdings)

- Haseko Corporation

- Kinden Corporation(EPC)

- JGC Japan

- DRP Construction Japan

- AECOM Japan

- Fluor Japan

- Hibiya Engineering Ltd

- ARUP Japan

第7章 市場機會與未來展望

The Japan data center construction market size is expected to grow from USD 7.14 billion in 2025 to USD 7.59 billion in 2026 and is forecast to reach USD 10.91 billion by 2032 at 6.24% CAGR over 2026-2032.

Rising hyperscale investments, sovereign-cloud mandates, and edge computing rollouts keep large projects in the pipeline, while seismic engineering expertise and liquid cooling innovations sharpen competitive advantages. The steady capital inflow from Japanese real-estate investment trusts (J-REITs), coupled with subsidies under the Economic Security Promotion Act, continues to ease financing constraints for domestic operators. Grid upgrade plans by Kansai Electric and other utilities mitigate power-availability risks, and higher voltage distribution designs support GPU-dense halls. However, skilled labor shortages and land-price inflation temper the build-out pace, pushing firms to pursue modular designs and secondary-metro sites for cost control. Operators increasingly favor renewable power purchasing agreements to protect margins from tariff volatility, reinforcing the shift toward northern regions with ample green energy.

Japan Data Center Construction Market Trends and Insights

Accelerating Cloud, AI and Big-Data Workloads

Rising generative-AI projects lift rack densities to 100 kW plus, raising electricity demand by up to 20% and forcing operators toward liquid immersion systems. SoftBank's 300 MW Tomakomai campus shows the new scale benchmark and targets 100% renewable power. GPU cloud providers such as Sakura Internet recorded a 476.3% profit jump in 2025, underscoring demand pull. Domestic oil major Idemitsu now supplies immersion fluids that cut cooling power 90%, anchoring a local value chain for sustainable AI infrastructure.

Hyperscale Campus Build-Outs by US and Domestic Majors

AWS has budgeted JPY 2.26 trillion through 2027, adding 30,500 annual jobs and JPY 5.57 trillion GDP impact. Oracle's USD 8 billion plan centers on data sovereignty clients in Tokyo and Osaka. On the domestic front, the KDDI-Sharp alliance aims to open Asia's largest cloud campus, while EdgeConneX is deploying 140 MW in Osaka to serve AI clusters. These multiyear programs anchor construction order books and intensify competition for skilled contractors.

Grid-Power Bottlenecks and Surging Electricity Tariffs

Kansai Electric will invest more than JPY 150 billion from 2026 on four substations serving new campuses. Operators face extended grid-connection queues and tariff spreads that make Hokkaido the most expensive and Hokuriku the least. Higher costs strain profit margins just as liquid cooling drives power draw above historic norms. Some firms lock renewable PPAs or install on-site generation to hedge exposure.

Other drivers and restraints analyzed in the detailed report include:

- Sovereign-Cloud and Data-Residency Regulations

- 5G-Driven Edge-DC Demand in Secondary Metros

- Scarcity of Tier-III/IV-Certified MEP Labor

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical infrastructure accounted for 37.62% of 2025 revenue, anchoring the Japan data center construction market share with high-voltage switchgear and busway upgrades. Services, though smaller, are forecast to achieve an 8.05% CAGR through 2032 as operators pay premiums for seismic engineering, immersion-cooling design, and AI workload layout optimization. Canon IT Solutions' West Tokyo site now supports 100 kVA liquid-cooled racks, showcasing hybrid cooling integration. Construction material inflation of 21-24% since 2021 pushes firms to modularize builds and pre-fabricate power rooms for faster delivery.

Japan data center construction market size expansion in services reflects demand for capacity-planning, commissioning, and retrofit consulting tied to generative-AI ramps. Mechanical infrastructure evolves toward dielectric fluids and direct-chip cooling, while IT infrastructure maintains steady orders for GPU servers despite enterprise cloud migration.

Tier III facilities maintained 56.42% Japan data center construction market share in 2025, serving enterprises and colocation tenants that value cost balance. Tier IV projects, though fewer, are rising at 8.43% CAGR through 2032 as hyperscale operators accept higher capital intensity for uninterrupted AI model training. Obayashi deploys active base isolation and ultra-high strength steel to secure Tier IV uptime in seismic zones.

Japan data center construction market size for Tier IV builds concentrates in the Tokyo-Osaka corridor where land costs justify high-density, high-availability designs. Tier I and Tier II legacy sites see attrition as tenants migrate workloads to cloud platforms demanding higher fault tolerance.

The Japan Data Center Construction Market is Segmented by Infrastructure (Electrical Infrastructure, Mechanical Infrastructure, and More), Tier Standard (Tier I and II, Tier III, and More), Data Center Type (Colocation, Hyperscale, and More), End User Industry (Banking Financial Services and Insurance, IT and Telecommunications, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Obayashi Corporation

- Taisei Corporation

- Kajima Corporation

- Shimizu Corporation

- Takenaka Corporation

- Tokyu Construction

- Toda Corporation

- Maeda Corporation

- Daiwa House Industry Co., Ltd.

- Penta-Ocean Construction

- Fuji Furukawa Engineering and Construction

- Nishimatsu Construction

- Sumitomo Mitsui Construction

- Hazama Ando

- Kitano Construction

- Mirai-Build (Mirait Holdings)

- Haseko Corporation

- Kinden Corporation (EPC)

- JGC Japan

- DRP Construction Japan

- AECOM Japan

- Fluor Japan

- Hibiya Engineering Ltd

- ARUP Japan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating cloud, AI and big-data workloads

- 4.2.2 Hyperscale campus build-outs by US and domestic cloud majors

- 4.2.3 Sovereign-cloud and data-residency regulations

- 4.2.4 5G-driven edge-DC demand in secondary metros

- 4.2.5 J-REIT capital inflows into shell-ready DC sites (under-the-radar)

- 4.2.6 Seismic base-isolation tech de-risking mega-facilities (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Grid-power bottlenecks and surging electricity tariffs

- 4.3.2 Scarcity of Tier-III/IV-certified MEP labour

- 4.3.3 Lengthy environmental licensing and community opposition

- 4.3.4 Escalating land prices inside Tokyo-Chiba-Kanagawa corridor (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Japan Data-Center Construction Statistics

- 4.8.1 Data Centers Total Installed Capacity (MW) in the Japan, 2023 and 2024

- 4.8.2 Total IT Load Under Construction in the Japan, MW, 2025 - 2030

- 4.8.3 Average Capex and Opex for the Japan Data Center Construction

- 4.8.4 Top Capex Spenders on Data Center Infrastructure in the Japan

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, US$ BN)

- 5.1 By Infrastructure

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 Power Distribution Solutions

- 5.1.1.1.1 Power Distribution Units

- 5.1.1.1.2 Switchgears

- 5.1.1.1.3 Others

- 5.1.1.2 Power Backup Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.1 Power Distribution Solutions

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Liquid-based Cooling

- 5.1.2.1.2 Air-based Cooling

- 5.1.2.2 Racks and Cabinets

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.3 IT Infrastructure

- 5.1.3.1 Servers

- 5.1.3.2 Storage

- 5.1.3.3 Other IT Infrastructure

- 5.1.4 General Construction

- 5.1.5 Services

- 5.1.5.1 Design and Consulting

- 5.1.5.2 Integration

- 5.1.5.3 Support and Maintenance

- 5.1.1 Electrical Infrastructure

- 5.2 By Tier Standard

- 5.2.1 Tier I and II

- 5.2.2 Tier III

- 5.2.3 Tier IV

- 5.3 By Data Center Type

- 5.3.1 Colocation Data Centers

- 5.3.2 Hyperscale / Self-built Data Centers

- 5.3.3 Others (Enterprise / Edge / Modular)

- 5.4 By End User Industry

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 IT and Telecommunications

- 5.4.3 Government and Defense

- 5.4.4 Healthcare

- 5.4.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Obayashi Corporation

- 6.2.2 Taisei Corporation

- 6.2.3 Kajima Corporation

- 6.2.4 Shimizu Corporation

- 6.2.5 Takenaka Corporation

- 6.2.6 Tokyu Construction

- 6.2.7 Toda Corporation

- 6.2.8 Maeda Corporation

- 6.2.9 Daiwa House Industry Co., Ltd.

- 6.2.10 Penta-Ocean Construction

- 6.2.11 Fuji Furukawa Engineering and Construction

- 6.2.12 Nishimatsu Construction

- 6.2.13 Sumitomo Mitsui Construction

- 6.2.14 Hazama Ando

- 6.2.15 Kitano Construction

- 6.2.16 Mirai-Build (Mirait Holdings)

- 6.2.17 Haseko Corporation

- 6.2.18 Kinden Corporation (EPC)

- 6.2.19 JGC Japan

- 6.2.20 DRP Construction Japan

- 6.2.21 AECOM Japan

- 6.2.22 Fluor Japan

- 6.2.23 Hibiya Engineering Ltd

- 6.2.24 ARUP Japan

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

資料中心建置市場:依資料中心類型、建設形式、等級、組件、建設服務類型及最終用戶產業分類-2026-2032年全球市場預測

資料中心建置市場:依資料中心類型、建設形式、等級、組件、建設服務類型及最終用戶產業分類-2026-2032年全球市場預測 2026年全球資料中心建置市場報告

2026年全球資料中心建置市場報告 全球資料中心建設市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球資料中心建設市場規模、佔有率、趨勢和成長分析報告(2026-2034) 資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備

資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備 資料中心建置市場規模、佔有率和趨勢分析報告:按基礎設施、層級、最終用途、地區和細分市場預測(2026-2033 年)

資料中心建置市場規模、佔有率和趨勢分析報告:按基礎設施、層級、最終用途、地區和細分市場預測(2026-2033 年) 2026-2030年全球資料中心建置市場

2026-2030年全球資料中心建置市場 新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 資料中心建置市場報告:按建設類型、資料中心類型、等級標準、產業垂直領域和地區分類(2026-2034 年)

資料中心建置市場報告:按建設類型、資料中心類型、等級標準、產業垂直領域和地區分類(2026-2034 年) 資料中心建置市場-全球產業規模、佔有率、趨勢、機會及預測(依基礎設施類型、層級、資料中心規模、最終用戶產業、地區及競爭格局分類,2021-2031)資料中心機械設備建置市場(依組件類型、液冷系統、建置類型、等級及計劃類型分類)-2026-2032年全球預測

資料中心建置市場-全球產業規模、佔有率、趨勢、機會及預測(依基礎設施類型、層級、資料中心規模、最終用戶產業、地區及競爭格局分類,2021-2031)資料中心機械設備建置市場(依組件類型、液冷系統、建置類型、等級及計劃類型分類)-2026-2032年全球預測