|

市場調查報告書

商品編碼

1940882

南美聚碳酸酯(PC)市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

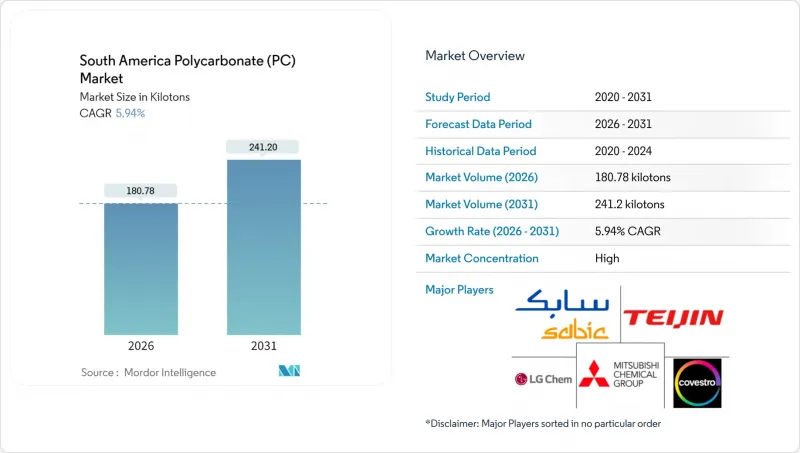

2025 年南美聚碳酸酯 (PC) 市場價值為 170.64 千噸,預計到 2031 年將達到 241.2 千噸,高於 2026 年的 180.78 千噸。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.94%。

前景取決於巴西建設業的復甦、阿根廷汽車業的反彈以及消費性電子設備的廣泛電氣化,這些因素共同推動終端用戶採用率的提高。製造商正積極響應政府的碳排放目標和有利於低碳材料的採購政策,並轉型使用含有回收和生物基成分的永續等級產品。憑藉大規模的加工基地和廣泛的分銷網路,巴西保持其作為供應中心的地位。然而,不斷上漲的聚合物進口關稅、天然氣價格上漲導致的原料成本壓力以及不斷發展的綠色建築標準,促使企業重塑競爭策略。那些能夠產品系列與循環經濟要求和節能建築標準相契合的區域性企業,預計將在整個預測期內贏得新的市場佔有率。

南美洲聚碳酸酯(PC)市場趨勢與展望

對輕型電動車的需求增加

電動車產量的擴大推動了電池模組、照明設備和內裝部件對聚碳酸酯的需求。阿根廷的目標是到2025年提高整車產量,預計將帶動對輕量化零件的需求,從而提升續航里程。巴西的組裝正在為儀錶板和充電樁指定使用抗衝擊等級的材料,這些材料比傳統的鋼或鋁更輕、更易於加工。政府將碳排放與稅收優惠掛鉤的獎勵正在推動車身部件和結構外殼中聚合物材料的替代應用。

家用電子電器生產的電氣化

區域設備製造商正在採用阻燃聚碳酸酯材料,以在滿足 UL 94 V-0 安全標準的同時,保持薄壁設計的自由度。沙烏地基礎工業公司 (SABIC) 於 2024 年 12 月和 2025 年 1 月推出的 LNP ELCRES CXL 共聚物,旨在提升智慧型手機、穿戴式裝置和充電器的耐化學性,這正是創新如何滿足新型外形規格需求的絕佳範例。

雙酚A原料價格波動

亞洲較低的運轉率正在擾亂全球雙酚A(BPA)價格,並侵蝕南美轉化商的利潤。巴西天然氣成本比美國和亞洲平均價格高出近2美元,加劇了這種壓力,使得當地聚合反應缺乏競爭力。

細分市場分析

預計到2025年,聚碳酸酯板材將佔據南美聚碳酸酯市場54.52%的佔有率,這主要得益於快速都市化地區屋頂、玻璃更換和標牌應用的需求成長。南美板材市場規模受惠於地方政府的稅收優惠政策,這些政策認可透光建築幕牆是一種節能投資。薄膜預計將以6.41%的複合年成長率成長,並在電子產品保護包裝和光介質應用領域獲得強勁成長勢頭。瓦楞板、實心板和多層板設計使建築師能夠在滿足日益嚴格的隔熱要求的同時,降低暖氣和冷氣負荷。阿根廷汽車組裝已開始採購用於內裝主機的薄板材,這項轉變預示著隨著電動車大規模生產的推進,薄板材的產量將會增加。

片材領域的長期競爭力將取決於擠出效率和樹脂籌資策略。將內部回收流程與生物基材料結合的製造商可以從尋求綠色建築認證的開發商那裡獲得溢價。薄膜加工商需要更嚴格的製程控制,並且往往聚集在巴西的電子產業群附近,因為在地採購可以顯著減少運輸時間和廢料。特種纖維在航太和安全玻璃應用領域仍然是一個小眾市場,但客製化模量和阻燃包裝可以提供更高的利潤率。

南美聚碳酸酯 (PC) 市場報告按產品類型(片材、薄膜及其他)、終端用戶行業(航太、汽車、建築施工、電氣電子、工業機械、包裝及其他終端用戶行業)和地區(巴西、阿根廷及其他南美國家)進行細分。市場預測以數量(噸)和價值(美元)兩種單位提供。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 由於電動車需求不斷成長,對輕型車的需求也日益成長。

- 家用電子電器製造的電氣化

- 巴西的建築熱潮與區域綠建築標準

- OEM廠商採用PC級材料,用於無需噴漆的高光澤外飾應用。

- 為滿足環境、社會和治理(ESG)要求,向再生/生物基塑膠的轉變正在加速。

- 市場限制

- 雙酚A原料價格波動

- 對進口特種PC等級材料的依賴

- 當地回收基礎建設延誤

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 進出口趨勢

- 價格趨勢

- 形態趨勢

- 回收利用概述

- 法律規範

- 巴西

- 阿根廷

- 終端用戶產業趨勢

- 航太(航太零件生產收入)

- 汽車(汽車產量)

- 建築與施工(新建建築占地面積)

- 電氣電子設備(電氣電子設備生產收入)

- 包裝(塑膠包裝量)

第5章 市場規模及成長預測(以金額為準及數量)

- 按產品形式

- 床單

- 電影

- 其他(紡織品等)

- 按最終用戶行業分類

- 航太工業

- 車

- 建築/施工

- 電氣和電子設備

- 工業和機械

- 包裝

- 其他終端用戶產業

- 按地區

- 巴西

- 阿根廷

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- Idemitsu Kosan Co.,Ltd.

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Group Corporation

- SABIC

- Samyang Corporation

- Teijin Limited

- Trinseo

- Wanhua

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

The South America Polycarbonate Market was valued at 170.64 kilotons in 2025 and estimated to grow from 180.78 kilotons in 2026 to reach 241.2 kilotons by 2031, at a CAGR of 5.94% during the forecast period (2026-2031).

The outlook hinges on Brazil's construction resurgence, Argentina's automotive rebound, and the broader electrification of consumer devices, collectively widening end-use adoption. Manufacturers are shifting toward sustainable grades that incorporate recycled or bio-attributed content, responding to government carbon targets and procurement policies that reward low-carbon materials. Brazil continues to anchor supply with its large processing base and extensive distribution networks. At the same time, rising import tariffs on polymers, feedstock cost pressures linked to high natural gas prices, and evolving green building codes are reshaping competitive tactics. Regional players that align their portfolios with circular economy mandates and energy-efficient construction standards are poised to capture new specification wins across the forecast period.

South America Polycarbonate (PC) Market Trends and Insights

Rising EV-Related Lightweighting Demand

Electric-vehicle production growth is driving increased demand for polycarbonate volumes in battery modules, lighting, and interior trim. Argentina aims to increase its production of assembled vehicles in 2025, which is expected to drive demand for lightweight components that enhance driving range. Brazilian assemblers specify impact-resistant grades for dashboards and charging stations that outperform traditional steel or aluminum in weight and processability. Government incentives that link tax relief to carbon-emission reductions reinforce polymer substitution in body parts and structural housings.

Electrification of Consumer-Electronics Production

Regional device manufacturers are turning to flame-retardant polycarbonate to meet UL 94 V-0 safety standards while retaining the freedom of thin-wall design. SABIC introduced LNP ELCRES CXL copolymers in December 2024 and January 2025, which enhance chemical resistance in smartphones, wearables, and chargers, highlighting how innovation addresses new form-factor needs.

Bisphenol-A Feedstock Price Volatility

Lower operating rates in Asia swing global BPA prices and erode South American converter margins. The pinch is amplified by Brazilian natural-gas costs, which are above levelized U.S. or Asian rates near USD 2, making local polymerization less competitive.

Other drivers and restraints analyzed in the detailed report include:

- Construction Boom in Brazil and Green-Building Codes

- Shift Toward Recycled/Bio-Based PC to Meet ESG Mandates

- Import Dependence for Specialty Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polycarbonate sheets held 54.52% of South America's polycarbonate market share in 2025 on the back of roofing, glazing, and signage applications in rapidly urbanizing corridors. The South America polycarbonate market size for sheets benefits from municipal tax incentives that rate daylight-harvesting facades as energy-saving investments. Films, posting a 6.41% CAGR, gain momentum in protective electronics packaging and optical media. Corrugated, solid, and multi-wall sheet designs enable architects to reduce HVAC loads while meeting increasingly stringent thermal insulation targets. Argentina's auto assemblers have begun sourcing thin-gauge sheets for interior consoles, a shift that foreshadows incremental tonnage gains once full EV production scales.

Long-run competitiveness in sheets hinges on extrusion efficiency and resin sourcing strategies. Producers that combine in-house recycling streams with bio-attributed feedstock can capture price premiums from developers pursuing green-building certification points. Film fabricators require tighter process control and often cluster near Brazil's electronics hubs, where localized supply slashes transit times and scrap rates. Specialty fibers remain niche in aerospace and safety glazing but deliver high margins through customized modulus and flame-retardant packages.

The South America Polycarbonate (PC) Market Report is Segmented by Product Form (Sheets, Films, and Others), End User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-User Industries), and Geography (Brazil, Argentina, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

List of Companies Covered in this Report:

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- Idemitsu Kosan Co.,Ltd.

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Group Corporation

- SABIC

- Samyang Corporation

- Teijin Limited

- Trinseo

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising EV-driven lightweighting demand

- 4.2.2 Electrification of consumer electronics manufacturing

- 4.2.3 Construction boom in Brazil and regional green-building codes

- 4.2.4 OEM adoption of paint-free, high-gloss exterior PC grades

- 4.2.5 Shift toward recycled/bio-based PC to meet ESG mandates

- 4.3 Market Restraints

- 4.3.1 Bisphenol-A feedstock price volatility

- 4.3.2 Import-dependence for specialty PC grades

- 4.3.3 Slow development of regional recycling infrastructure

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import and Export Trends

- 4.7 Price Trends

- 4.8 Form Trends

- 4.9 Recycling Overview

- 4.10 Regulatory Framework

- 4.10.1 Brazil

- 4.10.2 Argentina

- 4.11 End-use Sector Trends

- 4.11.1 Aerospace (Aerospace Component Production Revenue)

- 4.11.2 Automotive (Automobile Production)

- 4.11.3 Building and Construction (New Construction Floor Area)

- 4.11.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.11.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Form

- 5.1.1 Sheets

- 5.1.2 Films

- 5.1.3 Others (Fibers, etc.)

- 5.2 By End User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Packaging

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 Idemitsu Kosan Co.,Ltd.

- 6.4.5 LG Chem

- 6.4.6 Lotte Chemical

- 6.4.7 Mitsubishi Chemical Group Corporation

- 6.4.8 SABIC

- 6.4.9 Samyang Corporation

- 6.4.10 Teijin Limited

- 6.4.11 Trinseo

- 6.4.12 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment