|

市場調查報告書

商品編碼

1693836

亞太地區聚碳酸酯(PC)-市場佔有率分析、產業趨勢與成長預測(2024-2029年)Asia-Pacific Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

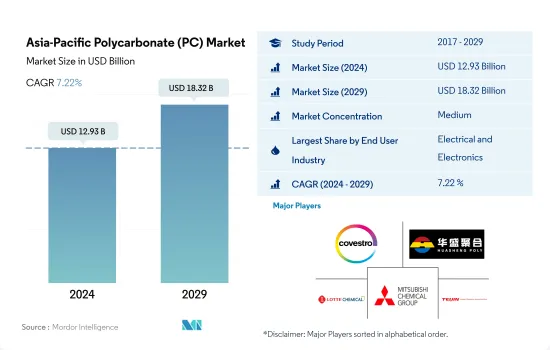

亞太聚碳酸酯 (PC) 市場規模預計在 2024 年為 129.3 億美元,預計到 2029 年將達到 183.2 億美元,預測期內(2024-2029 年)的複合年成長率為 7.22%。

電氣電子產業保持優勢

- 聚碳酸酯用途廣泛且耐用,廣泛應用於各行各業。應用包括冰箱、農業溫室、工業和公共建築、建築幕牆、手術器械、藥物輸送系統、血液血液透析機膜、血液儲存器、血液過濾器等。電氣和電子產業是該地區聚碳酸酯的最大消費產業,2022 年將佔據 45% 以上的市場佔有率。

- 2017年至2019年,聚碳酸酯需求穩定成長,年成長率與前一年同期比較為5.14%和3.53%。這一成長主要得益於電子產業產量的增加。

- 2020年,新冠疫情限制了營運、旅行和貿易,導致聚碳酸酯需求與前一年同期比較減3.71%。受影響尤其嚴重的是汽車和工業機械產業,2019 年產量分別下降了 12.52% 和 16.65%。然而,隨著限制的放寬,對聚碳酸酯的需求逐漸恢復,其中中國和印度在推動成長方面發揮了關鍵作用。

- 預計在預測期內,用聚碳酸酯替代傳統丙烯酸和玻璃的趨勢將日益成長,這將推動對這種材料的需求。在亞太地區所有終端用戶產業中,印度電氣和電子產業預計將經歷最高成長,預測期內銷量複合年成長率為 7.63%。總體而言,該地區對聚碳酸酯的需求預計在預測期內將達到 5.66% 的複合年成長率(數量)和 7.22% 的以金額為準。

中國保持數量和價值優勢

- 亞太地區是全球最大的聚碳酸酯消費地區,到 2022 年將佔據超過 63.07% 的市場。在亞太地區,聚碳酸酯在電氣和電子、汽車、航太零件製造和醫療設備製造業有著廣泛的應用。

- 2017年至2019年期間,聚碳酸酯的需求呈現穩定成長,主要得益於中國和印度等國家塑膠包裝產業的蓬勃發展。 2020年,疫情期間的營運和貿易限制導致勞動力短缺、原料短缺等各種限制因素嚴重影響了各個終端用戶產業,從而對該地區對聚碳酸酯的需求產生了負面影響。尤其是澳洲的聚碳酸酯需求受到明顯影響。 2020年全國需求年與前一年同期比較40.96%,與前一年同期比較地區較去年同期下降3.71%。

- 2021年,限制措施有所放鬆,聚碳酸酯需求恢復至疫情前的水準。這一成長的主要驅動力是印度等國家的工業活動的快速成長。預計這一成長趨勢將在整個預測期內持續下去,其中印度對聚碳酸酯的需求增幅在所有國家中最高。總體而言,預測期內亞太地區對聚碳酸酯的需求預計將達到 5.60% 的複合年成長率(按數量計算)。

亞太地區聚碳酸酯(PC)市場趨勢

東南亞國協快速成長推動電子產品生產

- 在亞太地區,電氣和電子設備生產收入從 2020 年到 2021 年成長了 13.9%。電子產品部門佔大多數亞洲國家出口總額的 20-50%。電視、收音機、電腦和行動電話等大多數的家用電子電器產品都是在東協地區生產。

- 東協是硬碟生產的領先者,超過 80% 的硬碟在該地區生產。整體而言,東協的電氣和電子(E&E)產業比其他產業更依賴外國投入和技術,53%的電氣和電子出口可歸因於東協電氣和電子出口中嵌入的外國增加價值(FVA)或外國投入。

- 泰國和馬來西亞等國家是該地區電子產品生產的領導者。泰國擁有東南亞最大的電子組裝基地之一,在硬碟、積體電路和半導體生產領域居領先地位。它是全球第二大空調製造商和全球第四大冰箱製造商。

- 電子產業極大地受益於東協的一體化生產網路,這有助於改善與中國和日本等亞洲經濟強國的貿易。

- 2019-2020年,中國佔全球電器出口的11.2%,數位產品出口成長5.8%。亞洲開發銀行稱,中國為該地區的電子產品提供了龐大的市場。泰國、日本、中國、馬來西亞、印度和菲律賓等國家繼續在該地區電子產品生產領域處於領先地位。

亞太地區聚碳酸酯(PC)產業概況

亞太地區聚碳酸酯(PC)市場適度整合,前五大公司佔59.21%的市佔率。市場的主要企業包括科思創股份公司、海南華盛新材料科技、樂天化學、三菱化學株式會社、帝人株式會社等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 聚碳酸酯(PC)貿易

- 價格趨勢

- 形態趨勢

- 回收概述

- 聚碳酸酯(PC)回收趨勢

- 法律規範

- 澳洲

- 中國

- 印度

- 日本

- 馬來西亞

- 韓國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 電氣和電子

- 工業/機械

- 包裝

- 其他

- 國家

- 澳洲

- 中國

- 印度

- 日本

- 馬來西亞

- 韓國

- 其他亞太地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- Hainan Huasheng New Material Technology Co., Ltd.

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Corporation

- Sinochem

- Sinopec SABIC Tianjin Petrochemical Company(SSTPC)

- Teijin Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 5000174

The Asia-Pacific Polycarbonate (PC) Market size is estimated at 12.93 billion USD in 2024, and is expected to reach 18.32 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Electrical and electronics industry to maintain its dominance

- Polycarbonates are widely utilized in various industries due to their versatile and durable nature. They find applications in refrigerators, agricultural houses, industrial and public buildings, facades, surgical instruments, drug delivery systems, hemodialysis membranes, blood reservoirs, and blood filters. The electrical and electronics industry has been the largest consumer of polycarbonate in the region, and it accounted for over 45% of the market share in 2022.

- Between 2017 and 2019, polycarbonate demand experienced steady growth, with Y-o-Y rates of 5.14% and 3.53%, respectively. The increasing production in the electronics industry primarily drove this growth.

- In 2020, the COVID-19 pandemic led to operational, travel, and trade restrictions, resulting in a decline in the demand for polycarbonates by 3.71% compared to the previous year. The automotive and industrial machinery industries were particularly affected, experiencing declines of 12.52% and 16.65% in their 2019 volumes, respectively. However, as the restrictions eased, the demand for polycarbonates gradually recovered, with China and India playing a significant role in driving the growth.

- The growing trend of substituting traditional acrylics and glass with polycarbonates is expected to drive the demand for the material in the forecast period. Among all end-user industries in the Asia-Pacific region, the electrical and electronics industry in India is projected to witness the highest growth, with a CAGR of 7.63% in terms of volume during the forecast period. Overall, the regional demand for polycarbonates is expected to record a CAGR of 5.66% in volume terms and 7.22% in value terms throughout the forecast period.

China to maintain its dominance both in terms of volume and value

- The Asia-Pacific region is the largest consumer of polycarbonates globally, occupying a share of over 63.07% in 2022. In the Asia-Pacific region, polycarbonates find various applications in the electrical and electronics, automotive, aerospace components manufacturing, and healthcare devices manufacturing industries.

- During 2017-2019, the demand for polycarbonates witnessed steady growth, mainly driven by the rapid growth in the plastic packaging industry in countries like China and India. In 2020, various restraining factors, like worker unavailability and raw material shortages caused by operational and trade restrictions during the pandemic, severely affected various end-user industries, thereby negatively affecting the polycarbonate demand in the region. Among all countries, the polycarbonate demand in Australia was affected severely. In 2020, the country's Y-o-Y demand volume declined by 40.96%, whereas the regional Y-o-Y decline was 3.71%.

- In 2021, as the restrictions eased, the polycarbonate demand rose back to its pre-pandemic level. This growth was majorly driven by the rapid growth in industrial activities in countries like India. This growth trend is expected to continue throughout the forecast period, with India witnessing the highest growth in polycarbonate demand among all countries. Overall, the polycarbonate demand in the Asia-Pacific region is expected to record a CAGR of 5.60% (in volume) during the forecast period.

Asia-Pacific Polycarbonate (PC) Market Trends

Rapid growth in ASEAN countries to foster electronics production

- The Asia-Pacific region saw an increase in electrical and electronics production revenue by 13.9% from 2020 to 2021. The electronics sector accounts for 20-50% of the total value of most Asian countries' exports. Consumer electronics such as televisions, radios, computers, and cellular phones are largely manufactured in the ASEAN region.

- ASEAN leads the production of hard drives, with over 80% of hard drives being manufactured in the region. Overall, the electrical and electronics (E&E) industry in ASEAN relies more on foreign inputs and technology than other industries, with 53% of E&E exports arising from foreign value added (FVA) or foreign inputs integrated into ASEAN's E&E exports.

- Countries like Thailand and Malaysia lead in the production of electronics in the region. Thailand, home to one of the largest electronics assembly bases in Southeast Asia, leads in the production of hard drives, integrated circuits, and semiconductors. It ranks second in manufacturing air conditioning units and fourth in the global refrigerators market.

- The electronics industry has greatly benefitted from ASEAN's integrated production networks, which foster improved trade with larger Asian economies like China and Japan.

- China held an 11.2% share of global exports in electrical products and registered a growth of 5.8% in the export of digital products from 2019 to 2020. According to the Asian Development Bank, China provides a large market for electronics in the region. Countries such as Thailand, Japan, China, Malaysia, India, and the Philippines continue to lead the region in the production of electronics.

Asia-Pacific Polycarbonate (PC) Industry Overview

The Asia-Pacific Polycarbonate (PC) Market is moderately consolidated, with the top five companies occupying 59.21%. The major players in this market are Covestro AG, Hainan Huasheng New Material Technology Co., Ltd., Lotte Chemical, Mitsubishi Chemical Corporation and Teijin Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Australia

- 4.6.2 China

- 4.6.3 India

- 4.6.4 Japan

- 4.6.5 Malaysia

- 4.6.6 South Korea

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Japan

- 5.2.5 Malaysia

- 5.2.6 South Korea

- 5.2.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 Hainan Huasheng New Material Technology Co., Ltd.

- 6.4.5 LG Chem

- 6.4.6 Lotte Chemical

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Sinochem

- 6.4.9 Sinopec SABIC Tianjin Petrochemical Company (SSTPC)

- 6.4.10 Teijin Limited

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms