|

市場調查報告書

商品編碼

1940863

中國生物促效劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)China Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

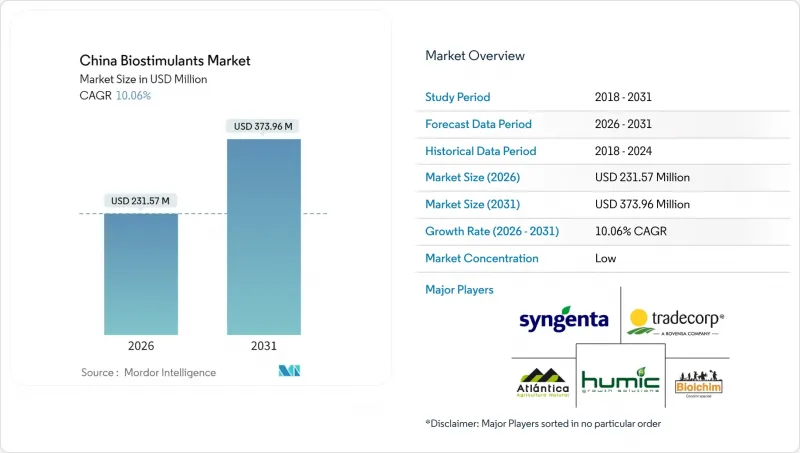

據估計,到 2026 年,中國生物促效劑市場規模將達到 2.3157 億美元,高於 2025 年的 2.104 億美元。

預計到 2031 年將達到 3.7396 億美元,2026 年至 2031 年的複合年成長率為 10.06%。

加快提高肥料利用效率的政策支持、穩固的保護性耕作面積以及在全國範圍內推廣智慧農業,為擴大需求創造了有利條件。海藻萃取物的主導地位、溫室栽培中氨基酸的日益普及以及治理土壤健康惡化的措施需要進一步加強。競爭差異化主要體現在品質保證、原料整合和數位化應用指導等。專利申請量的增加和活性化的外商直接投資表明,中國正走創新主導成長道路,這與中國加強糧食安全和減少農業投入排放的雙重目標相契合。

中國生物促效劑市場趨勢及洞察

政府獎勵措施促進永續投入品的採用

新的生態保護補償條例將於2024年實施,屆時生態保護區內生物促效劑成本的30%至50%將予以補償,從而縮小與化肥的價格差距。簡化的報名手續使得相容配方可在12個月內進入市場。國家碳中和目標的推進,提升了生物促效劑作為尿素和複合肥低排放替代品的重要性。省級專案基金每年撥款150億元人民幣(約21億美元),為零售商和大型農場提供優惠貸款和稅額扣抵,減輕其流動資金負擔。同時,科學研究津貼促進了適應中國多樣化土壤條件的產品研發,並增強了國內製造業的競爭力。

國內對有機農產品的需求不斷成長

食品安全問題改變了都市區的購買模式,促使有機農地面積擴大18%,到2023年達到240萬公頃。上海和深圳的有機蔬菜零售價格上漲了200%至300%,這與其較高的投入成本相符,也使得生物促效劑成為符合認證標準的營養補充工具。電商平台報告稱,有機農產品銷售額年增40%,主要得益於重視產品可追溯性的千禧世代和Z世代消費者。國家有機標準GB/T 19630的強制性要求迫使生產商用生物基材料取代合成肥料,從而維持了生鮮和加工食品領域對生物促效劑的需求。持續的都市化正在擴大消費群,並將消費者的偏好轉化為結構性的市場需求。

比傳統肥料價格高溢價

典型生物促效劑的價格可能是化學肥料的2到5倍,而胺基酸產品由於其複雜的水解過程和進口原料,價格也居高不下。平均面積僅0.6公頃的小規模農戶預算柔軟性有限,在西部省份推廣應用較為緩慢,因為這些地區的農戶收入比沿海地區低40%到50%。人民幣疲軟推高了進口原料成本,加劇了價格波動,擠壓了經銷商的利潤空間。省級補貼計劃在一定程度上緩解了這一負擔,但覆蓋範圍不均衡,導致市場滲透率不均。投資回報率的驗證仍然至關重要,而缺乏公共宣傳和指導正在減緩人們意識的轉變,並阻礙了抵消價格上漲擔憂的潛力。

細分市場分析

截至2025年,海藻萃取物佔中國生物促效劑市場佔有率的38.15%。這主要得益於山東省從養殖到提取的一體化生產群集,該集群降低了物流成本並確保了產品的新鮮度。消費者對海洋來源材料的偏好也推動了這個品類的發展,這與中國傳統的海帶消費文化相符。隨著加工商升級酵素輔助萃取生產線以提高細胞分裂素和生長素的濃度,預計中國海藻萃取物生物促效劑市場將穩定成長。氨基酸雖然市場規模較小,但溫室蔬菜行業的需求推動了其發展,因為精準施肥管理在該行業顯著提高了產量,預計到2031年,氨基酸的複合年成長率將達到13.09%。腐植酸和富裡酸在黑龍江省和內蒙古自治區的土壤改良計畫中需求穩定。蛋白質水解物則吸引了追求高品質的水果和漿果種植者的青睞。新興的幾丁聚醣和微生物聯合產品正在進行初步試驗,等待建立監管途徑以促進未來的發展。

胺基酸生產商正投資發酵技術,以實現在地化生產並減少對進口羽毛粉原料的依賴。青島西文生物科技有限公司推出了一條多級酶生產線,加工時間縮短了25%,遊離氨基酸含量得到提升,使其葉面營養產品脫穎而出。面對日益激烈的競爭,二線生產商正尋求與沿海加工商建立OEM合作關係,以充分利用其原料採購能力和全國銷售網路。數位化平台整合的拓展,促進了精準施肥,提高了人們對肥料相對於化肥附加價值的認知,並有助於維持其溢價優勢。

中國生物促效劑市場報告按形態(胺基酸、富裡酸、腐植酸、蛋白質水解物、海藻萃取物等)和作物類型(園藝作物、田間作物等)進行細分。市場預測以價值(美元)和數量(公噸)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章 報告

第3章執行摘要和主要發現

第4章:主要產業趨勢

- 有機耕作面積

- 人均有機產品支出

- 法律規範

- 中國

- 價值鍊和通路分析

- 市場促進因素

- 政府獎勵措施促進永續投入品的採用

- 國內對有機農產品的需求不斷成長

- 土壤健康狀況劣化及肥料利用效率目標

- 擴大中國沿海海藻養殖規模

- 保護性耕作的蓬勃發展帶動了對高附加價值材料需求的成長。

- 將生物活性劑整合到數位農業平台中

- 市場限制

- 比傳統肥料價格高溢價

- 缺乏統一的療效標準和監管規定

- 海藻原料供應的季節性變化

- 分銷通路庫存調整和農業投入品信貸週期收緊

第5章 市場規模及成長預測(價值及數量)

- 形式

- 胺基酸

- 富裡酸

- 腐植酸

- 蛋白質水解物

- 海藻萃取物

- 其他生物促效劑

- 作物類型

- 經濟作物

- 園藝作物

- 田間作物

第6章 競爭情勢

- 關鍵策略舉措

- 市佔率分析

- 公司概況

- 公司簡介

- Qingdao Seawin Biotech Group Co. Ltd.

- Beijing Leili Marine BioIndustry Inc.(Leili Group)

- Valagro(Syngenta)

- Trade Corporation International(Rovensa Group)

- Biolchim SpA(Hello Nature Group)

- Atlantica Agricola SA

- Humic Growth Solutions, Inc.

- Sinochem Holdings Corporation Ltd.

- Shandong Sukahan Bio-Technology Co. Ltd.(Sukahan Group)

- UPL Limited

- Corteva Agriscience

- Haifa Group

- Novonesis Group

- Koppert BV

- BASF SE

第7章:CEO們需要思考的關鍵策略問題

China biostimulants market size in 2026 is estimated at USD 231.57 million, growing from 2025 value of USD 210.4 million with 2031 projections showing USD 373.96 million, growing at 10.06% CAGR over 2026-2031.

Accelerated policy support for fertilizer-use efficiency, a robust protected-horticulture footprint, and a nationwide push for smart agriculture create favorable demand conditions. Seaweed extract leadership, rising amino-acid adoption in greenhouses, and soil-health degradation mitigation need further reinforcement. Competitive differentiation centers on quality assurance, raw-material integration, and digital application guidance. Intensifying patent filings and foreign direct investment signal an innovation-driven growth path that aligns with China's dual goals of food-security resilience and ag-input emission reduction.

China Biostimulants Market Trends and Insights

Government Incentives for Sustainable-Input Adoption

New ecological-protection compensation rules implemented in 2024 reimburse 30%-50% of biostimulant costs in eco-sensitive zones, closing price gaps with bulk fertilizers. Streamlined registration now completes within 12 months, accelerating market entry for compliant formulations. National carbon-neutrality commitments elevate biostimulants as low-emission substitutes for urea and compound fertilizers. Provincial pools totaling CNY 15 billion (USD 2.1 billion) per year provide concessional loans and tax credits that reduce working-capital stress for retailers and large farms. Parallel research grants foster domestic innovation that tailors products to China's diverse soils, reinforcing local manufacturing competitiveness.

Rising Domestic Demand for Organic Produce

Organic farmland expanded 18% in 2023 to 2.4 million hectares as food-safety concerns reshape urban purchasing patterns. Retail premiums of 200%-300% on organic vegetables in Shanghai and Shenzhen justify higher input costs, positioning biostimulants as certification-compliant nutrition tools. E-commerce platforms reported 40% year-over-year organic sales growth, led by millennial and Generation Z consumers who value traceability. Mandatory adherence to national organic standard GB/T 19630 forces growers to substitute synthetic fertilizers with bio-derived inputs, sustaining biostimulant demand across fresh and processed segments. Continuous urbanization widens the consumer base, converting preference into structural market demand.

High Price Premium Versus Conventional Fertilizers

Typical biostimulant prices exceed chemical fertilizers by two to five times, with amino-acid products at the upper band due to complex hydrolysis processes and imported substrates. Smallholder farmers averaging 0.6 hectares show limited budget flexibility, dampening uptake in western provinces where farm incomes trail coastal counterparts by 40%-50%. Yuan depreciation inflates costs for imported raw materials, amplifying volatility and compressing distributor margins. Province-level subsidy programs partially alleviate burdens but vary in coverage, creating uneven market penetration. Demonstrated return on investment remains critical, lack of extension training slows perception shifts that could offset sticker-shock concerns.

Other drivers and restraints analyzed in the detailed report include:

- Soil-Health Degradation and Fertilizer-Use-Efficiency Targets

- Expansion of Seaweed-Farming Capacity Along China's Coast

- Lack of Harmonized Efficacy Standards and Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Seaweed extracts held 38.15% of the China biostimulants market share in 2025, anchored by Shandong's integrated cultivation-to-extraction clusters that lower logistics costs and assure freshness. The category benefits from consumer preference for marine-derived inputs aligned with China's traditional kelp consumption culture. The China biostimulants market size for seaweed extracts is forecast to expand steadily as processors upgrade enzyme-assisted extraction lines to boost cytokinin and auxin concentrations. Amino acids, while representing a smaller revenue base, post a 13.09% CAGR through 2031, fueled by greenhouse vegetables where precision fertigation magnifies yield responses. Humic and fulvic acids enjoy stable demand from soil-remediation programs in Heilongjiang and Inner Mongolia. Protein hydrolysates attract niche demand in fruit orchards and berry plantations that seek quality premiums. Emerging chitosan and microbial consortium products occupy pilot-stage trials, pending regulatory pathways that can unlock future growth.

Amino-acid manufacturers invest in fermentation technologies to localize production, trimming dependency on imported feather meal substrates. Qingdao Seawin Biotech Group unveiled a multi-phase enzymatic line that cuts processing time 25% and raises free-amino-acid content, differentiating its foliar nutrient range. Competitive intensity prompts tier-two players to pursue OEM partnerships with coastal processors, cross-leveraging raw-material access and nationwide distributor networks. Wider digital-platform integration enables precise dosing, enhancing perceived value relative to fertilizers and supporting gradual premium retention.

The China Biostimulants Market Report is Segmented by Form (Amino Acids, Fulvic Acid, Humic Acid, Protein Hydrolysates, Seaweed Extracts, and More) and Crop Type (Horticultural Crops, Row Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Qingdao Seawin Biotech Group Co. Ltd.

- Beijing Leili Marine BioIndustry Inc. (Leili Group)

- Valagro (Syngenta)

- Trade Corporation International (Rovensa Group)

- Biolchim SpA (Hello Nature Group)

- Atlantica Agricola S.A.

- Humic Growth Solutions, Inc.

- Sinochem Holdings Corporation Ltd.

- Shandong Sukahan Bio-Technology Co. Ltd. (Sukahan Group)

- UPL Limited

- Corteva Agriscience

- Haifa Group

- Novonesis Group

- Koppert B.V.

- BASF SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Government incentives for sustainable-input adoption

- 4.5.2 Rising domestic demand for organic produce

- 4.5.3 Soil-health degradation and fertilizer-use-efficiency targets

- 4.5.4 Expansion of seaweed-farming capacity along China's coast

- 4.5.5 Protected-horticulture boom driving high-value input demand

- 4.5.6 Integration of biostimulants into digital-farming platforms

- 4.6 Market Restraints

- 4.6.1 High price premium versus conventional fertilizers

- 4.6.2 Lack of harmonized efficacy standards and regulations

- 4.6.3 Seasonal volatility in seaweed raw-material supply

- 4.6.4 Channel destocking and tighter ag-input credit cycles

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Qingdao Seawin Biotech Group Co. Ltd.

- 6.4.2 Beijing Leili Marine BioIndustry Inc. (Leili Group)

- 6.4.3 Valagro (Syngenta)

- 6.4.4 Trade Corporation International (Rovensa Group)

- 6.4.5 Biolchim SpA (Hello Nature Group)

- 6.4.6 Atlantica Agricola S.A.

- 6.4.7 Humic Growth Solutions, Inc.

- 6.4.8 Sinochem Holdings Corporation Ltd.

- 6.4.9 Shandong Sukahan Bio-Technology Co. Ltd. (Sukahan Group)

- 6.4.10 UPL Limited

- 6.4.11 Corteva Agriscience

- 6.4.12 Haifa Group

- 6.4.13 Novonesis Group

- 6.4.14 Koppert B.V.

- 6.4.15 BASF SE

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

生物促效劑市場:依形態、原料、應用方法和作物類型分類-2026-2032年全球市場預測

生物促效劑市場:依形態、原料、應用方法和作物類型分類-2026-2032年全球市場預測 全球生物促效劑市場 2026–2030

全球生物促效劑市場 2026–2030 全球生物促效劑市場:依活性成分、劑型、應用方法、作物類型和地區分類-預測至2031年

全球生物促效劑市場:依活性成分、劑型、應用方法、作物類型和地區分類-預測至2031年 生物促效劑市場機會、成長促進因素、產業趨勢分析及2026-2035年預測

生物促效劑市場機會、成長促進因素、產業趨勢分析及2026-2035年預測 生物促效劑市場預測至2034年-按作物類型、活性成分、劑型、通路、應用方法和地區分類的全球分析

生物促效劑市場預測至2034年-按作物類型、活性成分、劑型、通路、應用方法和地區分類的全球分析 生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 生物促效劑市場:按應用、作物類型、活性成分和地區分類

生物促效劑市場:按應用、作物類型、活性成分和地區分類 生物促效劑市場規模、佔有率、趨勢和預測:按產品類型、作物類型、形態、來源、分銷管道、應用、最終用戶和地區分類,2026-2034年歐洲生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

生物促效劑市場規模、佔有率、趨勢和預測:按產品類型、作物類型、形態、來源、分銷管道、應用、最終用戶和地區分類,2026-2034年歐洲生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球生物促效劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球生物促效劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)