|

市場調查報告書

商品編碼

1939586

歐洲生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

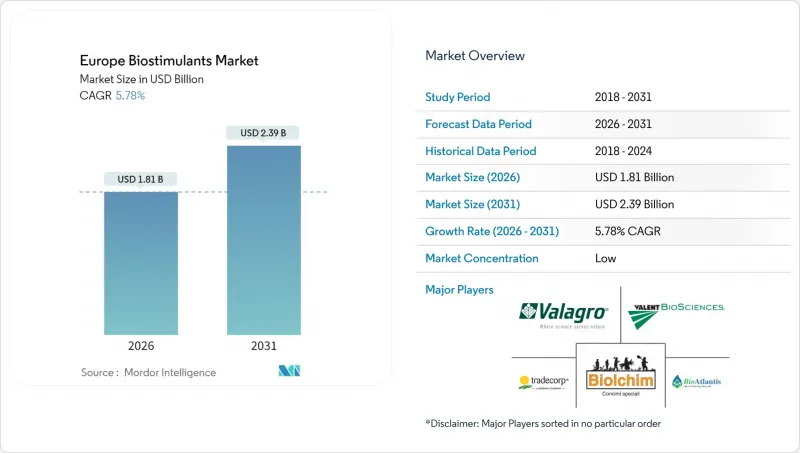

歐洲生物促效劑市場預計到 2026 年價值將達到 18.1 億美元,高於 2025 年的 17.1 億美元。

預計到 2031 年將達到 23.9 億美元,2026 年至 2031 年的複合年成長率為 5.78%。

市場前景反映了旨在遏制合成肥料使用的政策壓力不斷增加、有機耕地面積不斷擴大以及歐盟CE認證產品日益普及(這些都促進了跨境銷售)。技術進步使海藻萃取和微生物發酵成本降低了高達20%,縮小了生物投入品與傳統肥料之間的價格差距,從而增強了整體市場成長動能。精密農業的應用持續展現出田間盈利,尤其是在根據作物需求調整生物促效劑用量的變數施肥系統中。市場競爭強度仍較低,主要企業僅佔5.5%的市佔率。

歐洲生物促效劑市場趨勢與洞察

歐盟綠色交易和從農場到餐桌的化肥減量義務

歐盟已製定具有法律約束力的目標,將合成肥料的使用量減少20%。因此,成員國必須在其國家戰略計劃中展現出可衡量的進展。布列塔尼和巴伐利亞的田間試驗已經表明,當生物促效劑與變量噴霧器結合使用時,可實現12%至15%的替代效果。合作顧問目前正將合規性審核與生物投入建議相結合,以推動監管模式從「推式」轉變為「拉式」。設備供應商和投入品供應商正在聯合贊助農場試驗,以證明在低養分施用量下產量的穩定性,從而進一步降低推廣阻力。由於2026年起處罰力度加大,越來越多的農民開始簽訂多年期供應協議,採購帶有CE標誌的配方產品,以幫助他們達到規定的養分基準值。

擴大經認證的有機農田

從2020年到2023年,經認證的有機農地以每年3.6%的速度成長,達到1,770萬公頃(佔面積總面積的10.1%)。由於有機農業禁止使用大多數合成肥料,經認證的生物促效劑彌補了養分管理的不足,同時增強了植物的抗逆性。優質農產品的價格通常比傳統作物高出20%至40%,這抵消了更高的投入成本,並縮短了生物產品的投資回收期。零售商現在要求投入品來源必須經過第三方認證,這有利於那些擁有透明供應鏈和數位化可追溯性的製造商。這一趨勢正從奧地利等早期採用者擴展到義大利和西班牙的中型生產商,擴大了符合歐盟合格認證(CE)標籤資格的生產商群體。

缺乏統一的歐盟性能標準與通訊協定

雖然歐盟合格認證(CE)標誌簡化了市場進入流程,但目前歐洲範圍內仍缺乏田間功效標準,迫使農民依賴各國差異顯著的測試數據。農業合作社難以提供可靠的產品評級,而規避風險的生產者則往往等到本地案例研究出現後才會採用新產品。一些被認為功效較差的科學品牌和標籤可以合法共存,這模糊了市場訊號,損害了消費者信任。產業協會正在推動統一的通訊協定,但由於歐洲各地氣候帶和作物組合的顯著差異,達成共識的進程十分緩慢。在實現統一之前,買家只能依賴同業推薦和品牌聲譽,這往往導致銷售週期過長。

細分市場分析

到2025年,胺基酸將佔歐洲生物促效劑市場55.35%的佔有率,這反映了其在穀物、油籽和溫室作物中的廣泛應用。腐植酸製劑因其改善富碳土壤的能力而備受青睞,預計將成為成長最快的產品,2026年至2031年的複合年成長率將達到6.84%,隨著再生農業實踐的推廣,其表現將優於其他類別。性能差距的擴大表明,人們正從純粹的植物性材料轉向能夠重建土壤結構和微生物活性的解決方案,這與獎勵長期永續性的補貼體系相契合。

海藻萃取物仍然是有機認證計畫的基礎,而富裡酸在為高價值蔬果提供微量營養素方面也日益受到重視。蛋白質水解物因其能幫助作物在逆境下快速吸收氨基氮而備受專業種植者的青睞,而包括微生物混合物和胜肽複合物在內的各種「其他生物促效劑」則滿足了保護地栽培的特定需求。這些產品共同拓展了功能範圍,使經銷商能夠建立針對特定作物的營養組合,從而提高養分利用率、增強抗逆性並滿足區域監管要求。

歐洲生物促效劑市場報告按形態(胺基酸、富裡酸、腐植酸、蛋白質水解物、海藻萃取物和其他生物促效劑)、作物類型(經濟作物、園藝作物和田間作物)以及地區(法國、德國、義大利、荷蘭、俄羅斯、西班牙、土耳其、英國和歐洲其他地區)進行細分。市場預測以價值(美元)和數量(公噸)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章 報告

第3章執行摘要和主要發現

第4章 主要產業趨勢

- 有機耕作面積

- 人均有機產品支出

- 法律規範

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 價值鍊和通路分析

- 市場促進因素

- 歐盟綠色交易和從農場到餐桌的化肥減量義務

- 擴大經認證的有機農田

- 透過統一的CE標誌架構簡化市場進入

- 海藻提取和微生物發酵成本迅速下降

- 精密農業中的變數施肥技術在田間層面展現出投資報酬率

- 歐盟蛋白質作物研發資金激增,推動了對更高產量的需求。

- 市場限制

- 缺乏歐盟績效標準和通訊協定

- 與傳統肥料相比,價格溢價很高

- 大西洋和波羅的海水產養殖中海藻生物量供應的變異性

- 2024年及以後數位標籤和可追溯性的成本

第5章 市場規模和成長預測(價值和數量)

- 形式

- 胺基酸

- 富裡酸

- 腐植酸

- 蛋白質水解物

- 海藻萃取物

- 其他生物促效劑

- 作物類型

- 經濟作物

- 園藝作物

- 田間作物

- 國家

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 其他歐洲地區

第6章 競爭情勢

- 關鍵策略舉措

- 市佔率分析

- 公司列表

- 公司簡介。

- Valagro SpA

- Biolchim SpA

- BioAtlantis Limited

- Tradecorp International Pty Limited

- Valent Biosciences LLC

- Italpollina SpA

- BASF SE

- UPL Limited

- Syngenta AG

- Novozymes A/S

- Haifa Chemicals Ltd.

- Koppert BV

- Yara International ASA

- Isagro SpA

- SICIT Group SpA

- OMEX Agriculture Limited

- Humintech GmbH

- Atlantica Agricola SA

- Brandt Europe SL

- Andermatt Biocontrol AG

第7章:CEO們需要思考的關鍵策略問題

Europe biostimulants market size in 2026 is estimated at USD 1.81 billion, growing from 2025 value of USD 1.71 billion with 2031 projections showing USD 2.39 billion, growing at 5.78% CAGR over 2026-2031.

The outlook reflects accelerating policy pressure to curb synthetic fertilizer use, a growing organic acreage base, and widening access to Conformite Europeenne (CE) marked products that streamline cross-border sales. Technology improvements have trimmed seaweed extraction and microbial fermentation costs by up to 20%, bringing biological inputs closer to parity with conventional fertilizers and reinforcing the overall growth trajectory. Precision agriculture adoption continues to validate field-level returns, especially in variable-rate application systems that match biostimulant dosing to crop needs. Competitive intensity remains low, with top five players hold 5.5% share.

Europe Biostimulants Market Trends and Insights

EU Green Deal and Farm-to-Fork Fertilizer-Reduction Mandates

The European Union made its 20% synthetic-fertilizer-cut target legally binding, so every member state must show measurable progress within its national strategic plan. Field pilots in Brittany and Bavaria already record 12-15% substitution when biostimulants are paired with variable-rate spreaders. Cooperative advisers now bundle compliance audits with biological-input recommendations, turning regulation into a commercial pull rather than a push. Equipment vendors and input suppliers co-sponsor on-farm demonstrations that prove yield stability under lower nutrient rates, further easing adoption resistance. As penalty fees escalate from 2026 onward, growers are increasingly locking in multi-year supply contracts for Conformite Europeenne (CE)-marked formulations that help them meet mandated nutrient benchmarks.

Expansion of Certified Organic Farmland

Certified organic acreage expanded by 3.6% per year between 2020 and 2023, reaching 17.7 million hectares, equivalent to 10.1% of total farmland. Organic rules prohibit most synthetic fertilizers, so certified biostimulants fill the nutrient-management gap while supporting plant resilience. Premium farm-gate prices, often 20 to 40% higher than those for conventional crops, offset higher input costs and shorten the payback periods for biological products. Retailers now demand third-party verification of input provenance, which favors manufacturers with transparent supply chains and digital traceability. The trend extends beyond early adopters, such as Austria, to mid-sized producers in Italy and Spain, thereby widening the addressable base for Conformite Europeenne (CE)-certified labels.

Absence of EU-Wide Performance Standards and Protocols

Although Conformite Europeenne (CE) marking simplifies market access, there is still no pan-European benchmark for field-level efficacy, leaving farmers to rely on disparate national trial data. Advisory cooperatives struggle to issue definitive product rankings, so risk-averse growers delay adoption until local case studies accumulate. Low-performing labels can legally coexist with science-backed brands, muddying market signals and eroding trust. Industry associations are pushing for a unified protocol, but consensus remains slow due to the wide variation in climatic zones and crop mixes across Europe. Until harmonization arrives, buyers will lean on peer referral and brand reputation, which lengthens sales cycles.

Other drivers and restraints analyzed in the detailed report include:

- Harmonized Conformite Europeenne (CE)-Mark Framework Streamlining Market Access

- Rapid Cost Declines in Seaweed Extraction and Microbial Fermentation

- Higher Price Premium Versus Conventional Fertilizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids secured 55.35% of Europe biostimulants market share in 2025, reflecting their versatility across cereals, oilseeds, and greenhouse crops. Humic acid formulations, prized for their carbon-rich soil-conditioning benefits, are predicted to expand at the fastest 6.84% CAGR between 2026 and 2031, outpacing all other categories as regenerative agriculture practices spread. The widening performance gap underscores a shift from purely plant-focused inputs toward solutions that also rebuild soil structure and microbial activity, aligning with subsidy schemes that reward long-term sustainability.

Seaweed extracts continue to anchor certified-organic programs, while fulvic acids gain traction in micronutrient delivery for high-value fruits and vegetables. Protein hydrolysates appeal to specialty growers seeking fast amino-nitrogen uptake under stress, whereas the diverse "other biostimulants" pool including microbial blends and peptide complexes serves niche needs in protected cultivation. Collectively, these offerings broaden the functional palette, allowing distributors to craft crop-specific packages that improve nutrient efficiency, enhance stress resilience, and meet regionally distinct regulatory requirements.

The Europe Biostimulants Market Report is Segmented by Form (Amino Acids, Fulvic Acid, Humic Acid, Protein Hydrolysates, Seaweed Extracts, and Other Biostimulants), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Valagro S.p.A.

- Biolchim S.p.A.

- BioAtlantis Limited

- Tradecorp International Pty Limited

- Valent Biosciences LLC

- Italpollina S.p.A.

- BASF SE

- UPL Limited

- Syngenta AG

- Novozymes A/S

- Haifa Chemicals Ltd.

- Koppert B.V.

- Yara International ASA

- Isagro S.p.A.

- SICIT Group S.p.A.

- OMEX Agriculture Limited

- Humintech GmbH

- Atlantica Agricola S.A.

- Brandt Europe S.L.

- Andermatt Biocontrol AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Turkey

- 4.3.8 United Kingdom

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 EU Green Deal and Farm-to-Fork Fertilizer-Reduction Mandates

- 4.5.2 Expansion of Certified Organic Farmland

- 4.5.3 Harmonized CE-Mark Framework Streamlining Market Access

- 4.5.4 Rapid Cost Declines in Seaweed Extraction and Microbial Fermentation

- 4.5.5 Precision-ag variable-rate tech proving field-level ROI

- 4.5.6 Surge in EU protein-crop R&D funding driving yield-boost demand

- 4.6 Market Restraints

- 4.6.1 Absence of EU-Wide Performance Standards and Protocols

- 4.6.2 Higher Price Premium Versus Conventional Fertilizers

- 4.6.3 Seaweed biomass supply volatility in Atlantic & Baltic aquaculture

- 4.6.4 Digital labeling / traceability compliance costs post-2024

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Turkey

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Valagro S.p.A.

- 6.4.2 Biolchim S.p.A.

- 6.4.3 BioAtlantis Limited

- 6.4.4 Tradecorp International Pty Limited

- 6.4.5 Valent Biosciences LLC

- 6.4.6 Italpollina S.p.A.

- 6.4.7 BASF SE

- 6.4.8 UPL Limited

- 6.4.9 Syngenta AG

- 6.4.10 Novozymes A/S

- 6.4.11 Haifa Chemicals Ltd.

- 6.4.12 Koppert B.V.

- 6.4.13 Yara International ASA

- 6.4.14 Isagro S.p.A.

- 6.4.15 SICIT Group S.p.A.

- 6.4.16 OMEX Agriculture Limited

- 6.4.17 Humintech GmbH

- 6.4.18 Atlantica Agricola S.A.

- 6.4.19 Brandt Europe S.L.

- 6.4.20 Andermatt Biocontrol AG

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

生物促效劑市場:依形態、原料、應用方法和作物類型分類-2026-2032年全球市場預測

生物促效劑市場:依形態、原料、應用方法和作物類型分類-2026-2032年全球市場預測 全球生物促效劑市場 2026–2030

全球生物促效劑市場 2026–2030 全球生物促效劑市場:依活性成分、劑型、應用方法、作物類型和地區分類-預測至2031年

全球生物促效劑市場:依活性成分、劑型、應用方法、作物類型和地區分類-預測至2031年 生物促效劑市場機會、成長促進因素、產業趨勢分析及2026-2035年預測

生物促效劑市場機會、成長促進因素、產業趨勢分析及2026-2035年預測 生物促效劑市場預測至2034年-按作物類型、活性成分、劑型、通路、應用方法和地區分類的全球分析

生物促效劑市場預測至2034年-按作物類型、活性成分、劑型、通路、應用方法和地區分類的全球分析 生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

生物促效劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 生物促效劑市場:按應用、作物類型、活性成分和地區分類

生物促效劑市場:按應用、作物類型、活性成分和地區分類 生物促效劑市場規模、佔有率、趨勢和預測:按產品類型、作物類型、形態、來源、分銷管道、應用、最終用戶和地區分類,2026-2034年中國生物促效劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

生物促效劑市場規模、佔有率、趨勢和預測:按產品類型、作物類型、形態、來源、分銷管道、應用、最終用戶和地區分類,2026-2034年中國生物促效劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球生物促效劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球生物促效劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)