|

市場調查報告書

商品編碼

1940855

教育安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Education Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

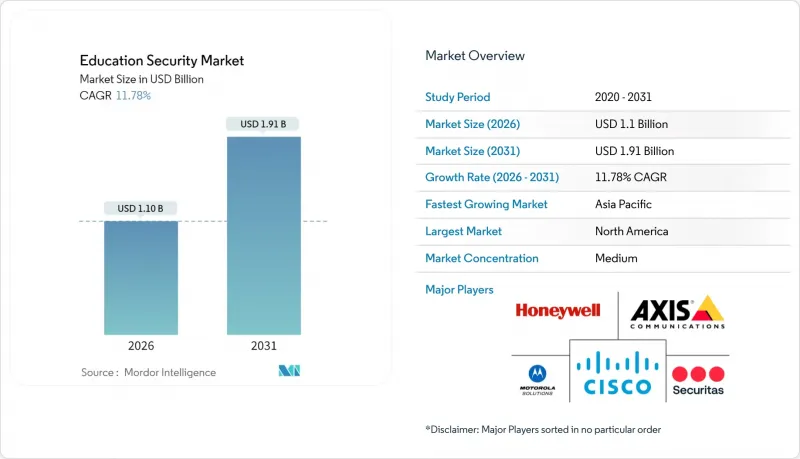

教育安全市場預計將從 2025 年的 9.8 億美元成長到 2026 年的 11 億美元,預計到 2031 年將達到 19.1 億美元,2026 年至 2031 年的複合年成長率為 11.78%。

預算撥款的增加,例如聯邦政府根據《K-12教育網路安全法案》津貼的2億美元撥款,已將學校定位為關鍵基礎設施。物理威脅和數位威脅的融合(2022年至2024年校園網路攻擊激增156%)正在推動對整合防護解決方案的需求。人工智慧(AI)驅動的影像分析技術可在三到五秒內偵測到可疑活動,從而縮短事件回應時間,並加速其在各學區的普及應用。北美以37.31%的收入佔有率引領教育安全市場,而亞太地區則以13.8%的複合年成長率實現了最快成長,這主要得益於數十億美元的智慧校園計劃。全球企業集團和雲端原生專家競相調整其安全產品以適應嚴格的學生資料法規,因此市場競爭強度仍然適中。

全球教育安全市場趨勢與洞察

用於早期威脅偵測的人工智慧行為偵測技術

先進的電腦視覺模型正在將安全防護從被動響應轉變為主動預測。 2024年,Verkada在500個學區部署的系統顯示,基於人工智慧的可疑人員警報回應時間縮短了67%,異常檢測準確率高達94%。加州一個學區報告稱,實施該系統後,事件發生率降低了43%,這表明該技術在減少校園霸凌和武器相關事件方面卓有成效。目前,為了減少誤報,系統正在實施情境分析,將位置、時間以及過往風險記錄等因素納入考量。然而,演算法需要6到12個月的基線影像才能穩定運行,這需要大規模的邊緣運算投資。將人工智慧與合規性儀錶板整合的供應商,透過促進FERPA合規性的實施,正在教育安全市場中佔據優勢。

政府安全津貼加速技術更新週期

自2024年以來,總額超過12億美元的「制止校園暴力」津貼,使即使是規模小規模的學區也能繞過過時的模擬系統,採用雲端原生平台。德克薩斯州已撥款3億美元用於校園安全,佛羅裡達州的「守護者」計畫每年撥款1.5億美元,從而形成同步更新周期,有利於採用承包解決方案。津貼指標要求可衡量的結果,因此供應商將事件分析儀表板作為標準配置。多年支援義務條款確保系統維護,同時穩定供應商收入。隨著資金越來越與基於環境、社會和治理(ESG)的安全關鍵績效指標(KPI)相一致,學區正在優先考慮能夠將安全事件轉化為審核的社會影響評分的平台。

初始採購成本和生命週期成本不斷上升

全校範圍的部署平均成本在 15 萬至 50 萬美元之間,年度服務費最高可達資本支出的 25%,這給預算有限的學區帶來了巨大壓力。專業安裝會增加 30% 至 40% 的成本,而不斷演變的威脅要求每三到五年進行大規模系統升級。津貼項目通常不包括軟體許可和雲端儲存更新,迫使一些學區只能以備用模式運行高級系統。提供基於效能定價和模組化升級的供應商正在減少預算摩擦,並改善整個教育安全產業的整體擁有成本指標。

細分市場分析

到2025年,安保服務仍將佔教育安保市場總收入的41.12%,儘管自動化技術發展迅速,安保服務仍將是教育安保市場的基礎。保安人員滿足監管要求,並能增強相關人員的安心。由人工智慧分析驅動的警報監控服務將以13.72%的複合年成長率超越所有其他服務。結合人工巡邏、無人機空影像和行動儀錶板的混合安保模式正在改變傳統的津貼角色。越來越多的學區正在撥款建造即時指揮中心,從而推動了對系統整合和託管服務合約的需求。

在教育安全市場,隨著教育機構整合供應商組合,系統整合服務預計將會成長。隨著人員審查法規日益嚴格,入職前篩檢正在復甦。諮詢服務正向網路安全審核和以ESG(環境、社會和治理)為基礎的安全報告方向發展。提供捆綁式服務套件的供應商透過簡化採購流程,實現了高於市場平均的成長。

到2025年,硬體將佔據教育安全市場52.15%的佔有率,這主要得益於攝影機和門禁控制設備的捆綁部署。然而,軟體領域13.05%的複合年成長率凸顯了向分析主導、雲端管理架構的轉變。邊緣運算攝影機透過將人工智慧直接嵌入設備,模糊了組件之間的界限,從而減少了資料中心的面積。視訊管理平台的訂閱定價模式將資本支出轉化為可預測的營運支出。

服務收入約佔總收入的四分之一,學區擴大將維護、韌體更新和威脅監控外包。隨著供應商將功能從專用硬體轉移到透過無線更新進行功能升級,教育安全市場的軟體部分將持續成長。

區域分析

到2025年,北美將佔教育安全市場收入的36.85%,美國聯邦政府14億美元的撥款將加速技術更新換代。加拿大各省政府也紛紛效仿,安大略省實施了一項1.8億加元的項目,用於更新其視訊監控和門禁系統。墨西哥的現代化計畫已撥款8,900萬美元用於公立學校安全技術,擴大了區域供應商管道。

預計到2031年,亞太地區將以13.63%的複合年成長率實現最高成長。中國正將高達15%的780億美元教育改革資金用於綜合安防,加速大規模採購。印度的智慧校園投資超過120億美元,東南亞各國的教育部門也將安全解決方案納入其數位化學習計畫。全球相機巨頭的在地化生產提高了交付速度,滿足了國內採購需求,進一步加劇了教育安防市場的競爭。

歐洲在應對GDPR方面穩步推進,德國已投資28億歐元用於建造數位化學校,英國也投資6.5億英鎊用於採用隱私納入設計技術的基礎建設。中東和非洲地區總支出雖落後,但存在一些高成長領域。阿拉伯聯合大公國的「智慧學校」計劃和沙烏地阿拉伯的「2030願景」教育支柱正在刺激對雲端多語言安全套件的需求。能夠應對不同資料居住規則的供應商更有可能在這些地區成功拓展業務。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 校園即時影像分析需求快速成長

- 校園暴力和破壞行為事件日益增多

- 政府安全津貼加速技術更新週期

- 新興經濟體的基礎建設現代化計劃

- 利用人工智慧驅動的行為檢測技術進行早期威脅識別

- ESG相關的安全關鍵績效指標用於指導資金籌措決策

- 市場限制

- 高昂的初始採購成本和生命週期成本

- 持續存在的隱私和資料保護問題

- 實體和網路安全架構不統一

- 校園保全人員短缺

- 宏觀經濟因素的影響

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過服務

- 安全

- 入職前篩選

- 安全諮詢

- 系統整合與管理

- 警報監控服務

- 其他私人保全服務

- 按組件

- 硬體

- 軟體

- 服務

- 透過安全解決方案

- 視訊監控系統

- 門禁系統

- 緊急通訊系統

- 網路安全解決方案

- 透過部署模式

- 本地部署

- 雲

- 混合

- 按設施

- 小學和中學教育設施

- 高等教育設施

- 其他教育設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- Honeywell International Inc.

- Motorola Solutions Inc.

- Securitas AB

- Axis Communications AB

- Genetec Inc.

- Verkada Inc.

- Hangzhou Hikvision Digital Technology Co. Ltd.

- Johnson Controls International plc

- Robert Bosch GmbH

- ADT Inc.

- Allied Universal Topco LLC

- Prosegur Compania de Seguridad SA

- Hanwha Vision Co., Ltd.

- Zhejiang Dahua Technology Co. Ltd.

- Gallagher Group Limited

- Silverseal Corporation

- SEICO Inc.

- Kisi Inc.

- AxxonSoft LLC

- Eagle Eye Networks Inc.

第7章 市場機會與未來展望

The education security market is expected to grow from USD 0.98 billion in 2025 to USD 1.1 billion in 2026 and is forecast to reach USD 1.91 billion by 2031 at 11.78% CAGR over 2026-2031.

Rising federal allocations, such as the USD 200 million K-12 Education Cybersecurity Act grant, have positioned schools as critical-infrastructure sites. Converging physical and digital threats, underscored by a 156% jump in campus cyberattacks between 2022 and 2024, sharpen demand for integrated protection. Artificial-intelligence video analytics now detect suspicious behavior within 3-5 seconds, shortening incident response times and bolstering adoption momentum across districts. North America leads the education security market with a 37.31% revenue share, while the Asia-Pacific region records the fastest growth at a 13.8% CAGR, driven by multi-billion-dollar smart campus programs. Competitive intensity remains moderate as global conglomerates and cloud-native specialists vie to align security offerings with strict student-data regulations.

Global Education Security Market Trends and Insights

AI-Enabled Behavioural Detection for Early Threat Identification

Advanced computer vision models are increasingly shifting security from a reactive to a predictive mode. Verkada rollouts across 500 districts in 2024 demonstrated 67% faster responses after AI person-of-interest alerts, achieving 94% accuracy in anomaly detection. Districts in California reported a 43% decline in incidents following the deployment, highlighting the technology's effectiveness in reducing bullying and weapons-related events. Contextual analytics now factor in location, time of day, and historical risk to curb false positives. However, campuses must capture 6-12 months of baseline footage before algorithms stabilize, requiring sizable edge-compute investments. Vendors that bundle AI with compliance dashboards gain an edge in the education security market by easing FERPA-aligned rollouts.

Government Safety Grants Accelerating Technology Refresh Cycles

Since 2024, STOP School Violence grants exceeding USD 1.2 billion have enabled smaller districts to bypass legacy analog systems and adopt cloud-native platforms. Texas earmarked USD 300 million for school security, and Florida's Guardian Program injects USD 150 million annually, creating synchronized refresh cycles that favor turnkey solutions. Grant metrics demand measurable outcomes, prompting vendors to ship incident analytics dashboards as standard. Mandatory multi-year support clauses stabilize provider revenue while ensuring system upkeep. As funds increasingly link to ESG-based safety KPIs, districts prioritize platforms that convert security events into auditable social-impact scores.

High Upfront Procurement and Lifecycle Costs

Complete campus installations average USD 150,000-500,000, with annual service fees consuming up to 25% of capital outlays, straining tight district budgets. Specialized installations raise costs by 30-40%, and major system refreshes are required every 3-5 years to counter evolving threats. Grant schemes rarely cover software licensing or cloud-storage renewals, prompting some districts to run sophisticated systems in fallback modes. Vendors offering outcome-based pricing and modular upgrades mitigate budget friction and improve total cost-of-ownership metrics across the education security industry.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Incidence of School Violence and Vandalism

- Infrastructure Modernisation Programs in Emerging Economies

- Persistent Privacy and Data-Protection Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Guarding services generated 41.12% of 2025 revenue, anchoring the education security market despite the rapid advancement of automation. Visible officers fulfill regulatory mandates and boost stakeholder reassurance. Alarm-monitoring services, fueled by AI analytics, outpace all services at 13.72% CAGR. Hybrid guard models that combine human patrols with drone feeds and mobile dashboards are reshaping traditional roles. Districts allocating grant funds toward real-time command centers elevate demand for systems integration and managed service contracts.

The education security market size for systems integration services is set to expand as institutions consolidate their vendor portfolios. Pre-employment screening rebounds amid stricter personnel vetting rules. Consulting engagements evolve into cybersecurity audits and ESG-based safety reporting. Vendors offering bundled service suites achieve above-market growth by lowering procurement complexity.

Hardware accounted for 52.15% of the education security market share in 2025, driven by the rollout of bulk cameras and access controls. Yet software's 13.05% CAGR underscores the shift toward analytics-driven, cloud-managed architectures. Edge-enabled cameras blur component lines by embedding AI directly on devices, shrinking data-center footprints. Subscription pricing for video-management platforms converts capital expenditure into predictable operating outlays.

Services accounted for nearly one-quarter of total revenue as districts increasingly outsourced maintenance, firmware updates, and threat monitoring. The education security market size for software will continue expanding as vendors decouple functionality from proprietary hardware and push feature upgrades via over-the-air updates.

The Education Security Market Report is Segmented by Services (Guarding, Pre-Employment Screening, and More), Component (Hardware, Software, and Services), Security Solution (Video Surveillance Systems, Access Control Systems, and More), Deployment Mode (On-Premise, Cloud, and Hybrid), Facilities (Primary and Secondary Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 36.85% of the education security market revenue in 2025, led by the United States' USD 1.4 billion in combined federal grants that catalyzed rapid technology refresh cycles. Canadian provinces echo this trend, with Ontario's CAD 180 million program upgrading video surveillance and access-control stacks. Mexico's modernization drive earmarks USD 89 million for public-school safety technology, broadening regional supplier pipelines.

Asia-Pacific posts the most aggressive 13.63% CAGR through 2031. China's USD 78 billion education overhaul allocates up to 15% for integrated security, fast-tracking large-scale procurements. India's smart-campus investments surpass USD 12 billion, and Southeast Asian ministries bundle safety solutions within digital-learning rollouts. Local manufacturing by global camera giants shortens delivery cycles and satisfies domestic-content mandates, heightening competitive churn within the education security market.

Europe advances steadily on GDPR context compliance. Germany commits EUR 2.8 billion to digital schools, and the United Kingdom channels GBP 650 million toward infrastructure fortified by privacy-by-design tools. The Middle East and Africa trail in aggregate spending yet exhibit pockets of high growth-UAE smart-school projects and Saudi Arabia's Vision 2030 education pillar stimulate demand for cloud-ready, multi-lingual security suites. Suppliers adept at navigating divergent data-residency rules are more likely to succeed in scaling across these regions.

- Cisco Systems Inc.

- Honeywell International Inc.

- Motorola Solutions Inc.

- Securitas AB

- Axis Communications AB

- Genetec Inc.

- Verkada Inc.

- Hangzhou Hikvision Digital Technology Co. Ltd.

- Johnson Controls International plc

- Robert Bosch GmbH

- ADT Inc.

- Allied Universal Topco LLC

- Prosegur Compania de Seguridad S.A.

- Hanwha Vision Co., Ltd.

- Zhejiang Dahua Technology Co. Ltd.

- Gallagher Group Limited

- Silverseal Corporation

- SEICO Inc.

- Kisi Inc.

- AxxonSoft LLC

- Eagle Eye Networks Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for real-time video analytics on campuses

- 4.2.2 Heightened incidence of school violence and vandalism

- 4.2.3 Government safety grants accelerating technology refresh cycles

- 4.2.4 Infrastructure modernisation programs in emerging economies

- 4.2.5 AI-enabled behavioural detection for early threat identification

- 4.2.6 ESG-linked safety KPIs guiding funding decisions

- 4.3 Market Restraints

- 4.3.1 High upfront procurement and lifecycle costs

- 4.3.2 Persistent privacy and data-protection concerns

- 4.3.3 Disjointed physical-cybersecurity architectures

- 4.3.4 Shortage of skilled campus security personnel

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Services

- 5.1.1 Guarding

- 5.1.2 Pre-Employment Screening

- 5.1.3 Security Consulting

- 5.1.4 Systems Integration and Management

- 5.1.5 Alarm Monitoring Services

- 5.1.6 Other Private Security Services

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Security Solution

- 5.3.1 Video Surveillance Systems

- 5.3.2 Access Control Systems

- 5.3.3 Emergency Communication Systems

- 5.3.4 Cybersecurity Solutions

- 5.4 By Deployment Mode

- 5.4.1 On-Premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By Facilities

- 5.5.1 Primary and Secondary Facilities

- 5.5.2 Higher Education Facilities

- 5.5.3 Other Educational Facilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 South-East Asia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Motorola Solutions Inc.

- 6.4.4 Securitas AB

- 6.4.5 Axis Communications AB

- 6.4.6 Genetec Inc.

- 6.4.7 Verkada Inc.

- 6.4.8 Hangzhou Hikvision Digital Technology Co. Ltd.

- 6.4.9 Johnson Controls International plc

- 6.4.10 Robert Bosch GmbH

- 6.4.11 ADT Inc.

- 6.4.12 Allied Universal Topco LLC

- 6.4.13 Prosegur Compania de Seguridad S.A.

- 6.4.14 Hanwha Vision Co., Ltd.

- 6.4.15 Zhejiang Dahua Technology Co. Ltd.

- 6.4.16 Gallagher Group Limited

- 6.4.17 Silverseal Corporation

- 6.4.18 SEICO Inc.

- 6.4.19 Kisi Inc.

- 6.4.20 AxxonSoft LLC

- 6.4.21 Eagle Eye Networks Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

資料安全即服務 (DSaaS) 市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、應用、產業垂直領域和地區分類-2026-2033 年產業預測

資料安全即服務 (DSaaS) 市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、應用、產業垂直領域和地區分類-2026-2033 年產業預測 資料安全態勢管理 (DSPM) 市場規模、佔有率和趨勢分析報告:按組件、部署類型、組織規模、資料類型、應用程式、最終用戶、地區和細分市場預測 (2026–2033)

資料安全態勢管理 (DSPM) 市場規模、佔有率和趨勢分析報告:按組件、部署類型、組織規模、資料類型、應用程式、最終用戶、地區和細分市場預測 (2026–2033) 資料安全與態勢管理市場預測至2034年-依資料環境、元件、組織規模、資料敏感程度、應用、最終使用者和地區分類的全球分析

資料安全與態勢管理市場預測至2034年-依資料環境、元件、組織規模、資料敏感程度、應用、最終使用者和地區分類的全球分析 安全支出市場:按應用程式、部署模式、組件、安全支出類型、最終用戶和地區分類

安全支出市場:按應用程式、部署模式、組件、安全支出類型、最終用戶和地區分類 資料安全市場:按組件類型、部署模式、組織規模和產業分類 - 2026-2032年全球市場預測

資料安全市場:按組件類型、部署模式、組織規模和產業分類 - 2026-2032年全球市場預測 2026年全球IT安全諮詢服務市場報告

2026年全球IT安全諮詢服務市場報告 泰國資訊科技與安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

泰國資訊科技與安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球IT安全諮詢服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)資料驅動型保全服務市場,依服務、部署模式、安全技術、組織規模及垂直產業分類,全球預測,2026-2032年軟體開發安全諮詢服務市場:按服務類型、部署類型、安全類型、組織規模和產業分類 - 全球預測(2026-2032 年)

全球IT安全諮詢服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)資料驅動型保全服務市場,依服務、部署模式、安全技術、組織規模及垂直產業分類,全球預測,2026-2032年軟體開發安全諮詢服務市場:按服務類型、部署類型、安全類型、組織規模和產業分類 - 全球預測(2026-2032 年)