|

市場調查報告書

商品編碼

1940739

泰國資訊科技與安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thailand IT And Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

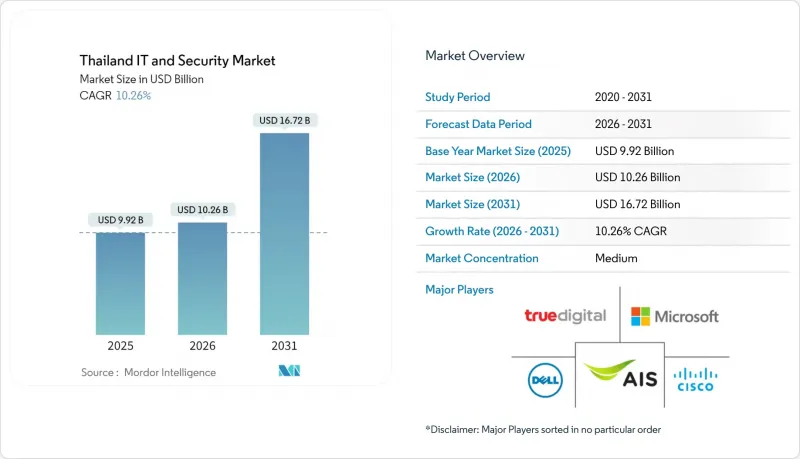

2025年泰國IT和安全市場價值89.5億美元,預計到2031年將達到204.4億美元,高於2026年的102.7億美元。

預測期(2026-2031 年)的複合年成長率預計為 14.78%。

這一快速成長反映了泰國作為東協數位基礎設施中心的地位、其以雲端優先的公共部門政策以及持續湧入的超大規模資料中心(總投資已超過85億美元)。覆蓋95%人口的強大5G網路、15億泰銖的國家人工智慧預算以及跨境電子商務的蓬勃發展,都在推動邊緣到雲端架構的普及。由於泰國網路安全專業人員短缺3萬人,以及新的資料保護法規導致合規支出增加,企業買家越來越傾向於選擇託管服務。來自DTAC日益激烈的競爭、與True Corporation合併後網路覆蓋範圍的重組,以及美國雲端服務供應商競相實現可用區本地化,都進一步加劇了競爭。預計這些因素將推動泰國IT和安全市場在未來十年保持兩位數的成長。

泰國IT與安全市場趨勢及洞察

雲端優先政策加速公共部門的數位轉型

數位政府發展局強制要求各機構採用雲端技術,從而取消部門採購,並在安全、整合和分析服務方面實現規模經濟。基於 ISO/IEC 27001 的集中式框架提高了新供應商的准入門檻,而國家網路安全局與Google雲端的合作則為政府工作負載增加了人工智慧驅動的威脅偵測能力。本地雲端區域解決了資料主權問題,並隨著各機構將預算從硬體轉向託管平台,增強了泰國的 IT 和安全市場。

5G基礎設施將加速邊緣運算的普及

Advanced Info Services 95% 的人口覆蓋率支援工廠、醫院和物流中心的低延遲應用。東部經濟走廊的製造工廠將感測器數據傳輸到雲端 AI 引擎,實現即時品管。同時,True Corporation 的「True Cyber Safe」每天為行動用戶過濾 10 萬個風險連結。這使得通訊業者能夠從單純的連接供應商轉型為邊緣平台營運商,進一步鞏固其在泰國 IT 和安全市場的地位。

網路安全人才短缺限制了市場成長

目前,銀行為聘請高級分析師支付180萬泰銖(約5萬美元)的年薪,確保獲得稀缺的專業人才,但需求仍比供應多出3萬人。中小企業無力應對薪資上漲,被迫延後計劃或將業務外包給MSSP(資安管理服務提供者)。大學正努力擴充課程,而人才則紛紛湧向新加坡尋求更高薪的工作,這導致泰國IT和安全市場發展放緩。

細分市場分析

到2025年,服務收入將佔總收入的41.64%,企業將傾向選擇託管安全營運中心(SOC)、威脅狩獵和整合解決方案。在人才持續短缺的情況下,泰國IT和保全服務市場規模預計將以10.55%的複合年成長率成長。 True Corporation等通訊業者正在將安全和連接服務捆綁銷售,以提升銷售高收入服務。雖然由於資料中心和5G網路的資本支出,硬體收入穩定成長,但商品化正在抑製成長。軟體,尤其是人工智慧輔助分析軟體,預計將實現最快的成長速度,因為訂閱模式將預算從資本支出轉向營運成本。

這種構成比轉變反映了泰國市場從以硬體為中心的架構向軟體定義、服務導向的架構的演變。專業整合商將舊有系統與雲端API連接起來,而供應商則提供自動化方案來彌補勞動力短缺。這種轉變有助於泰國IT和安全市場在不斷上漲的工資壓力下保持高效運作。

2025年,雲端運算將佔泰國IT和安全市場佔有率的53.12%,複合年成長率將達到16.43%,顯示雲端運算在各垂直領域的應用日益廣泛。超大規模資料中心業者在泰國的推出解決了資料居住問題,並增強了受監管銀行遷移關鍵業務工作負載的信心。雖然本地部署仍將在國防和關鍵基礎設施領域繼續保留,但隨著企業將本地控制與彈性運算結合,混合模式正日益受到青睞。

雲端安全功能正日益超越傳統防火牆,促使風險規避型負責人加快遷移計畫。日益複雜的整合需求推動了託管安全服務提供者 (MSSP) 的需求,而 SD-WAN 正在取代 MPLS 以降低電路成本。隨著通訊業者在工廠和醫院部署邊緣節點,混合部署預計將推動泰國 IT 和安全市場規模的擴大。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 泰國公共部門雲端優先政策

- 加速 5G 部署,以支援從邊緣到雲端的各種應用場景

- 電子商務的快速成長推動了超大規模資料中心的建設

- 董事會層級採納 NIST CSF 和 ISO/IEC 27001 標準,以滿足出口市場要求

- 日本和美國製造商「泰國+」近岸外包的興起

- 金融科技監理沙盒推動開放API安全支出

- 市場限制

- 分散式中小企業的IT預算週期

- 網路安全專業人員短缺3萬人

- 傳統 MPLS 合約會減緩雲端遷移速度

- 泰銖波動下,對進口半導體的高度依賴

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 定價分析

第5章 市場規模與成長預測

- 按組件

- 硬體和設備

- 軟體

- 服務

- 透過部署模式

- 本地部署

- 雲

- 混合

- 按組織規模

- 主要企業

- 小型企業

- 按最終用戶行業分類

- BFSI

- 政府/國防

- 製造業

- 衛生保健

- 零售與電子商務

- 能源與公共產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Advanced Info Service Public Co. Ltd(AIS)

- True Digital Group Co. Ltd

- Dell Technologies Inc.

- Cisco Systems Inc.

- International Business Machines Corp.(IBM)

- Microsoft Corporation

- Hewlett Packard Enterprise Co.

- Fujitsu(Thailand)Co. Ltd

- Fortinet Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd

- Trend Micro Inc.

- Kaspersky Lab

- Samsung Electronics Co. Ltd

- Acer Inc.

- Lenovo Group Ltd

- G-Able Co. Ltd

- MFEC Public Co. Ltd

- Digital Government Development Agency(DGA)

- SIAMDATA Co. Ltd

第7章 市場機會與未來趨勢

- 閒置頻段與未滿足需求評估

The Thailand IT and Security market was valued at USD 8.95 billion in 2025 and estimated to grow from USD 10.27 billion in 2026 to reach USD 20.44 billion by 2031, at a CAGR of 14.78% during the forecast period (2026-2031).

This surge reflects Thailand's positioning as ASEAN's digital-infrastructure hub, the public-sector cloud-first mandate, and sustained hyperscale data-center inflows that already top USD 8.5 billion. Robust 5G coverage of 95% of the population, a THB 1.5 billion national AI budget, and cross-border e-commerce flows energize adoption of edge-to-cloud architectures. Enterprise buyers increasingly favor managed services because the country lacks 30,000 cybersecurity professionals, while new data-protection rules elevate compliance spending. The DTAC heightens competitive intensity-True Corporation merger that reshapes network reach, and by U.S. cloud providers racing to localize availability zones. These forces converge to keep the Thailand IT and Security market on a double-digit growth path through the decade.

Thailand IT And Security Market Trends and Insights

Cloud-First Policy Accelerates Public-Sector Digital Transformation

The Digital Government Development Agency mandates cloud adoption across ministries, dissolving siloed procurement and creating scale for security, integration, and analytics services. Centralized frameworks anchored on ISO/IEC 27001 raise entry barriers for new vendors, while the National Cyber Security Agency's alliance with Google Cloud layers AI-driven threat detection onto government workloads. Local cloud regions address data-sovereignty concerns, bolstering the Thailand IT and Security market as agencies shift budget from hardware to managed platforms.

5G Infrastructure Enables Edge-Computing Proliferation

Advanced Info Service's 95% population coverage underpins low-latency applications in factories, hospitals, and logistics hubs. Manufacturing plants in the Eastern Economic Corridor now stream sensor data to cloud AI engines for real-time quality control, while True Corporation's "True CyberSafe" filters 100,000 risky links per day for mobile users. Telcos thus graduate from connectivity providers to edge-platform operators, deepening their stake in the Thailand IT and Security market.

Cyber-Security Talent Shortage Constrains Market Growth

Banks now pay senior analysts THB 1.8 million (USD 50,000) to secure scarce experts, yet demand still exceeds supply by 30,000 roles. SMEs cannot match wage inflation and therefore defer projects or outsource to MSSPs. Universities scramble to scale curricula, while talent migrates to higher-paying Singapore roles, subtracting momentum from the Thailand IT and Security market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Growth Drives Hyperscale Data-Center Demand

- Export Manufacturing Drives Enterprise Security Compliance

- SME Budget Fragmentation Delays Technology Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

YServices contributed 41.64% of 2025 revenue as enterprises chose managed SOC, threat-hunting, and integration offerings. The Thailand IT and Security market size for services is projected to climb at a 10.55% CAGR as talent scarcity persists. Telecom operators such as True Corporation bundle security with connectivity to upsell higher-margin offerings. Hardware revenues rise steadily on data-center and 5G network capex, but commoditization caps growth. Software, especially AI-assisted analytics, records the fastest run-rate because subscription models shift budgets from capex to opex.

The mix signals Thailand's evolution from hardware-centric builds to software-defined, service-oriented architectures. Specialized integrators tie legacy systems to cloud APIs, while vendors deliver automated playbooks that offset human shortfalls. This pivot keeps the Thailand IT and Security market efficient even as wage pressure mounts.

Cloud controlled 53.12% of the Thailand IT and Security market share in 2025, and sustained a 16.43% CAGR, indicating deepening adoption across verticals. Hyperscalers neutralize data-residency concerns by launching Thai regions, giving regulated banks confidence to migrate core workloads. On-premises persists in defense and critical infrastructure, but hybrid models gain favor as enterprises pair local control with elastic compute.

Cloud security capabilities now often surpass legacy firewalls, prompting risk-averse buyers to accelerate lift-and-shift roadmaps. Integration complexity fuels MSSP demand, while SD-WAN replaces MPLS to cut circuit costs. The Thailand IT and Security market size attached to hybrid deployments will widen as telcos push edge nodes to factories and hospitals.

The Thailand IT and Security Market Report is Segmented by Component (Hardware and Devices, Software, Services), Deployment Mode (On-Premises, Cloud, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Government and Defense, Manufacturing, Healthcare, Retail and E-Commerce, Energy and Utilities), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Advanced Info Service Public Co. Ltd (AIS)

- True Digital Group Co. Ltd

- Dell Technologies Inc.

- Cisco Systems Inc.

- International Business Machines Corp. (IBM)

- Microsoft Corporation

- Hewlett Packard Enterprise Co.

- Fujitsu (Thailand) Co. Ltd

- Fortinet Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd

- Trend Micro Inc.

- Kaspersky Lab

- Samsung Electronics Co. Ltd

- Acer Inc.

- Lenovo Group Ltd

- G-Able Co. Ltd

- MFEC Public Co. Ltd

- Digital Government Development Agency (DGA)

- SIAMDATA Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first policy in Thai public sector

- 4.2.2 Acceleration of 5G rollout enabling edge-to-cloud use-cases

- 4.2.3 E-commerce boom driving hyperscale data-center build-outs

- 4.2.4 Board-level adoption of NIST CSF and ISO/IEC 27001 to meet export-market mandates

- 4.2.5 Rise of "Thailand PLUS" near-shoring by Japanese and US manufacturers

- 4.2.6 FinTech regulatory sandbox pushing open-API security spend

- 4.3 Market Restraints

- 4.3.1 Fragmented SME IT budget cycles

- 4.3.2 Shortage of 30,000 cyber-security professionals

- 4.3.3 Legacy MPLS contracts delaying cloud migration

- 4.3.4 High dependence on imported semiconductors amid Baht volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware and Devices

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Government and Defense

- 5.4.3 Manufacturing

- 5.4.4 Healthcare

- 5.4.5 Retail and E-commerce

- 5.4.6 Energy and Utilities

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core segments, Financials as available, Strategic information, Market rank/share, Products and services, Recent developments)

- 6.4.1 Advanced Info Service Public Co. Ltd (AIS)

- 6.4.2 True Digital Group Co. Ltd

- 6.4.3 Dell Technologies Inc.

- 6.4.4 Cisco Systems Inc.

- 6.4.5 International Business Machines Corp. (IBM)

- 6.4.6 Microsoft Corporation

- 6.4.7 Hewlett Packard Enterprise Co.

- 6.4.8 Fujitsu (Thailand) Co. Ltd

- 6.4.9 Fortinet Inc.

- 6.4.10 Palo Alto Networks Inc.

- 6.4.11 Check Point Software Technologies Ltd

- 6.4.12 Trend Micro Inc.

- 6.4.13 Kaspersky Lab

- 6.4.14 Samsung Electronics Co. Ltd

- 6.4.15 Acer Inc.

- 6.4.16 Lenovo Group Ltd

- 6.4.17 G-Able Co. Ltd

- 6.4.18 MFEC Public Co. Ltd

- 6.4.19 Digital Government Development Agency (DGA)

- 6.4.20 SIAMDATA Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

資料安全即服務 (DSaaS) 市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、應用、產業垂直領域和地區分類-2026-2033 年產業預測

資料安全即服務 (DSaaS) 市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、應用、產業垂直領域和地區分類-2026-2033 年產業預測 資料安全態勢管理 (DSPM) 市場規模、佔有率和趨勢分析報告:按組件、部署類型、組織規模、資料類型、應用程式、最終用戶、地區和細分市場預測 (2026–2033)

資料安全態勢管理 (DSPM) 市場規模、佔有率和趨勢分析報告:按組件、部署類型、組織規模、資料類型、應用程式、最終用戶、地區和細分市場預測 (2026–2033) 資料安全與態勢管理市場預測至2034年-依資料環境、元件、組織規模、資料敏感程度、應用、最終使用者和地區分類的全球分析

資料安全與態勢管理市場預測至2034年-依資料環境、元件、組織規模、資料敏感程度、應用、最終使用者和地區分類的全球分析 安全支出市場:按應用程式、部署模式、組件、安全支出類型、最終用戶和地區分類

安全支出市場:按應用程式、部署模式、組件、安全支出類型、最終用戶和地區分類 資料安全市場:按組件類型、部署模式、組織規模和產業分類 - 2026-2032年全球市場預測

資料安全市場:按組件類型、部署模式、組織規模和產業分類 - 2026-2032年全球市場預測 2026年全球IT安全諮詢服務市場報告

2026年全球IT安全諮詢服務市場報告 教育安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

教育安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球IT安全諮詢服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)資料驅動型保全服務市場,依服務、部署模式、安全技術、組織規模及垂直產業分類,全球預測,2026-2032年軟體開發安全諮詢服務市場:按服務類型、部署類型、安全類型、組織規模和產業分類 - 全球預測(2026-2032 年)

全球IT安全諮詢服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)資料驅動型保全服務市場,依服務、部署模式、安全技術、組織規模及垂直產業分類,全球預測,2026-2032年軟體開發安全諮詢服務市場:按服務類型、部署類型、安全類型、組織規模和產業分類 - 全球預測(2026-2032 年)