|

市場調查報告書

商品編碼

1940839

美國化肥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

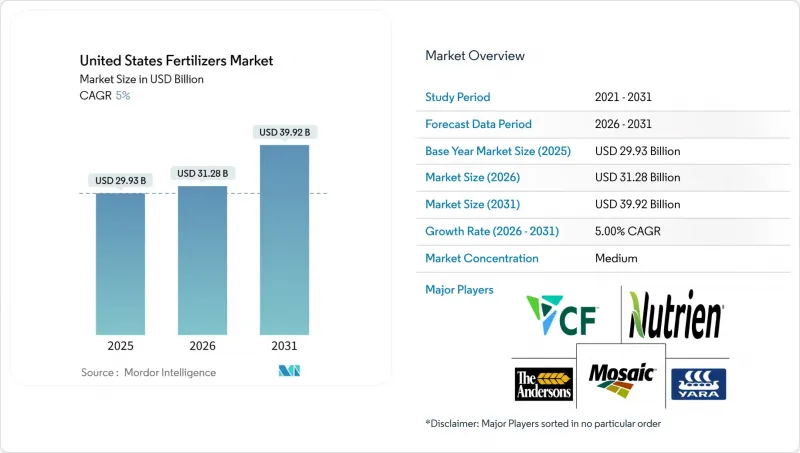

美國化肥市場預計將從 2025 年的 299.2 億美元成長到 2026 年的 313 億美元,到 2031 年達到 392.3 億美元,2026 年至 2031 年的複合年成長率為 4.62%。

在監管壓力日益增大的情況下,對作物營養的強勁需求、精密農業的日益普及以及鼓勵使用高效肥料的政策獎勵,共同支撐了收入成長。生產商正投資美國墨西哥灣沿岸沿岸的清潔氨產能,以對沖天然氣價格波動風險並滿足新的永續性標準。同時,密西西比河沿岸多式聯運物流網路的加強降低了中西部農民的運輸成本,並提高了市場應對原料價格波動的能力。日益激烈的競爭正促使前五大供應商進一步推動垂直整合,拓展數位化農業平台,並調整產品組合,轉向特種肥料和控釋肥料。

美國化肥市場趨勢與洞察

精密農業的現狀

目前,變數施肥系統已應用於70%的玉米和大豆種植面積,在確保產量的同時,可減少15%至20%的氮肥用量。在愛荷華州和伊利諾州,該系統的採用率超過85%,衛星影像、土壤感測器和產量測繪技術協同工作,提供切實可行的處方箋。 Nutrien公司每年投資2億美元,開發將感測器數據與產品推薦結合的數位化農藝平台。此模式提高了養分利用效率,並將諮詢服務與銷售連結起來。隨著越來越多的生產者實現成本節約和生產力提升,這項技術正將採購決策從“數量”轉向“價值”,從而促進了控釋產品的推廣應用,使養分輸送與作物需求相匹配。美國政府審核局(GAO)的一項模型估計,全產業推廣應用該技術可在不犧牲產量的前提下,將全國化肥用量減少高達12%。因此,向數據驅動型管理的轉變是美國化肥市場結構性成長的關鍵。

向高效肥料過渡

美國國稅局2024-37號公告將永續航空燃料積分(每加侖1.75美元)與已證實的氮肥利用效率掛鉤,顯著提升了對緩釋尿素、硝化抑制劑和脲酶抑制劑的需求。種植者正透過擴大產能來應對這項需求。 CF Industries已累計1.5億美元用於維修其位於唐納森維爾的工廠,使其能夠生產緩釋尿素;拜耳的碳排放項目已發放超過12.5萬個與這些產品相關的積分,證明其能夠直接減少農場溫室氣體排放。隨著碳市場和稅收政策的融合,需求正從小眾園藝領域轉向大型農業面積,推動了特種配方供應商基本客群的擴大和銷售成長。

天然氣價格波動

2024年,亨利港價格在每百萬英熱單位(MMBtu)2.10美元至6.80美元之間波動,波動幅度高達224%。由於原料成本佔氨生產成本的80%之多,這種波動幾乎直接影響氮肥生產成本。據CF工業公司稱,價格每變動1美元,年度利潤可能變動高達5,500萬美元。 2024年第三季度,當現貨天然氣價格超過每百萬英熱單位6美元時,沒有避險合約的小規模生產商減少了產量。這導致供應緊張,並抑制了對價格敏感的生產商的需求。伊利諾大學的一項分析發現,天然氣價格持續高於每百萬英熱單位5美元時,由於農民尋求成本更低的替代方案,施用量減少了高達12%。因此,這種波動在短期內會抑制養分總消耗量。

細分市場分析

2025年,與精準可變施肥配方相容的單一肥料(可針對土壤特定養分缺乏進行精準施肥)占美國肥料市場收入的77.35%。受玉米和大豆種植面積強勁成長的推動,預計到2031年,美國單一肥料市場將以4.74%的複合年成長率成長。預計到2024年,玉米面積將達到9,410萬英畝,並且由於持續依賴高氮肥用量,市場需求將保持穩定。然而,複合肥料由於其養分比例單一,往往無法滿足田間具體處方箋,因此成長受到限制。隨著網格土壤取樣辨識出集約化作物輪作中限制產量的養分缺乏情況,鋅和硼等微量元素的用量正以每年15-20%的速度成長。自 1990 年以來,工業硫沉降量急劇下降,導致許多土壤的硫含量低於其充足閾值,因此對次要營養物質(特別是硫)的需求正在恢復。

規模較大的農場出於田間經濟效益的考慮,仍然傾向於使用單一營養元素肥料,以便零售商在銷售點配製精確的配方。然而,小規模的農場和肥料供應有限的地區則出於便利性考慮,繼續使用複合肥料。隨著越來越多的州發現普遍存在的微量元素缺乏問題,預計美國肥料市場中微量元素添加劑的佔有率將會增加。在明尼蘇達州和北達科他州,有針對性地施用鐵肥使大豆產量每英畝提高了多達12蒲式耳,證明了投資回報。因此,種植者正在將微量元素混合包裝成散裝的氮磷鉀複合肥,以獲取新的高收益收入來源。單一營養元素產品仍將維持最大的市場佔有率,而補充營養元素產品將實現逐步成長。

由於成熟的供應鏈、低廉的單位成本以及與現有噴霧器的兼容性,預計到2025年,傳統顆粒狀和球狀肥料將佔總銷售額的76.10%。然而,隨著種植者越來越重視環境合規性和養分利用效率,特種配方肥料正以5.18%的複合年成長率快速成長。緩釋肥料,例如聚合物包膜尿素,能夠根據植物吸收時間穩定釋放氮肥,促使玉米帶地區的玉米種植系統採用率提高了25%。美國特種配方肥料市場主要由可與噴霧器系統整合以實現變數施肥的液體肥料所驅動。水溶性肥料在溫室和水耕種植中越來越受歡迎,因為精準的養分輸送可以減少廢棄物並提高作物品質。

美國環保署(EPA)的工人保護標準鼓勵使用能夠減少粉塵和施肥人員暴露的產品,從而推動了對液體肥料和包衣顆粒的需求。 Nutrien公司報告稱,其特種肥料部門在2024年實現了顯著的收入成長,這主要得益於其用於精密農業的控釋和液體肥料產品的強勁訂單。隨著特種肥料在監管更加嚴格的環境下,憑藉其多功能性,以及符合碳排放計劃和稅收優惠政策(這些政策要求肥料能夠證明其養分利用效率的提升),預計這一成長勢頭將進一步加快。

美國化肥市場按類型(複合肥、單質肥)、形態(常規肥、特種肥)、施用方法(葉面噴布、土培)和作物類型(田間作物、園藝作物、草坪和觀賞植物)進行細分。市場預測以價值(美元)和數量(公噸)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章 報告

第3章執行摘要主要發現

第4章 主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均養分施用率

- 微量營養素

- 田間作物

- 園藝作物

- 宏量營養素

- 田間作物

- 園藝作物

- 次要大量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 精密農業及技術整合的介紹

- 高效能肥料的研發與政策支持

- 農產品價格對農民購買力的影響

- 再生農業和排碳權

- 擴大墨西哥灣沿岸地區綠色氨的生產能力

- 密西西比州多式聯運化肥走廊

- 市場限制

- 天然氣價格波動對氮氣成本的影響

- 加強對營養物質徑流的監管

- 特種作物中的生物營養替代品

- 老化的氨氣管道網路所帶來的風險

第5章 市場規模及成長預測(數量與價值)

- 類型

- 複合肥

- 單一成分肥料

- 微量營養素

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 氮基

- 硝酸銨

- 無水氨

- 尿素

- 其他

- 磷酸鹽

- DAP

- MAP

- SSP

- TSP

- 鉀肥

- MoP

- 硫酸鉀

- 其他

- 中等元素

- 鈣

- 鎂

- 硫

- 微量營養素

- 形式

- 傳統的

- 特殊用途

- CRF

- 液體肥料

- SRF

- 水溶性

- 目的

- 土壤

- 葉面噴布

- 施肥和灌溉

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- 公司簡介

- CF Industries Holdings, Inc.

- Nutrien Ltd.

- The Mosaic Company

- The Andersons Inc.

- Yara International ASA

- Haifa Group

- ICL Group Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile SA

- Wilbur-Ellis Company LLC(Wilbur-Ellis Holdings Inc.)

- Intrepid Potash Inc.

- Compass Minerals International Inc.

- JR Simplot Company

- Growmark Inc.

- CHS Inc.

第7章:CEO們需要思考的關鍵策略問題

The United States fertilizers market is expected to grow from USD 29.92 billion in 2025 to USD 31.3 billion in 2026 and is forecast to reach USD 39.23 billion by 2031 at 4.62% CAGR over 2026-2031.

Strong demand for crop nutrients, growing adoption of precision agriculture, and policy incentives that reward enhanced-efficiency fertilizer use are sustaining revenue growth even as regulatory pressures tighten. Producers are investing in clean-ammonia capacity on the Gulf Coast to hedge natural gas volatility and meet emerging sustainability criteria. Meanwhile, intermodal logistics upgrades along the Mississippi River corridor are lowering delivered costs for Midwestern growers and helping the market absorb feedstock price shocks. Competitive intensity is rising as the five largest suppliers pursue vertical integration, expand digital agriculture platforms, and reposition portfolios toward specialty and controlled-release formulations.

United States Fertilizers Market Trends and Insights

Precision Agriculture Uptake

Variable-rate systems now guide fertilizer placement on 70% of corn and soybean acres, trimming nitrogen use by 15-20% while safeguarding yields . Adoption exceeds 85% in Iowa and Illinois, where satellite imagery, soil sensors, and yield mapping converge to deliver actionable prescriptions. Nutrien invests USD 200 million annually in digital agronomy platforms that integrate sensor data with product recommendations, a model that links advisory services to sales while improving nutrient use efficiency. As more growers verify savings and productivity gains, the technology is shifting purchasing decisions from volume to value, encouraging uptake of controlled-release products that match nutrient delivery to crop demand. Government Accountability Office modeling suggests industry-wide implementation could trim nationwide fertilizer use by as much as 12% without sacrificing output. This pivot toward data-driven management is therefore a structural growth lever for the United States fertilizers market.

Enhanced-Efficiency Fertilizers Shift

IRS Notice 2024-37 links a USD 1.75 per gallon sustainable aviation fuel credit to proof of enhanced-efficiency nitrogen use, creating an outsize pull for controlled-release urea, nitrification inhibitors, and urease inhibitors. Producers are scaling capacity in response; CF Industries earmarked USD 150 million to retrofit its Donaldsonville complex for controlled-release urea, while Bayer's Carbon Program has issued more than 125,000 credits tied to such products, confirming direct greenhouse-gas reductions on the farm. As carbon markets converge with tax policy, demand is migrating from niche horticulture into core commodity acreage, widening the customer base and accelerating top-line growth for suppliers of specialty formulations.

Natural Gas Price Volatility

Henry Hub prices oscillated between USD 2.10 and USD 6.80 per MMBtu in 2024, driving a 224% range that translates almost directly into nitrogen production costs because feedstock accounts for up to 80% of ammonia expenditure. CF Industries notes that every USD 1.00 swing moves annual margins by as much as USD 55 million. Small producers without hedged contracts curtailed output during the third quarter of 2024 when spot gas breached USD 6.00, tightening supply while curbing demand among price-sensitive growers. University of Illinois analysis indicates that sustained gas over USD 5.00 reduces application rates by up to 12% as farmers seek lower-cost alternatives. The volatility, therefore, acts as a near-term drag on total nutrient consumption.

Other drivers and restraints analyzed in the detailed report include:

- High Corn and Soybean Commodity Prices

- Regenerative Farming Carbon-Credit Programs

- Tighter Nutrient-Runoff Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers captured 77.35% of 2025 revenue in the United States fertilizers market because their single-nutrient formulations align neatly with precision variable-rate prescriptions that target soil-specific deficiencies. The United States fertilizers market size for straight formulations is projected to expand at a 4.74% CAGR through 2031 as corn and soybean acreage remains robust. Corn plantings reached 94.1 million acres in 2024 and continue to rely on high nitrogen rates, driving stable demand. For complex fertilizers, their blanket nutrient ratios often fail to align with site-specific prescriptions, thereby limiting growth. Micronutrients such as zinc and boron are increasing by 15-20% annually, as grid soil sampling identifies yield-limiting deficiencies in intensive rotations. Secondary nutrient demand, especially sulfur, is rebounding because industrial sulfur deposition has fallen sharply since 1990, pushing many soils below sufficiency thresholds.

Field-level economics still favor straight nutrients for large operations because retailers can blend to precise formulas at the point of sale. However, smaller farms and areas with limited custom application services continue to use complex grades for convenience. The United States fertilizers market share for micronutrient additives is likely to rise as more states document widespread deficiencies. Targeted iron applications in Minnesota and North Dakota lifted soybean yields by up to 12 bushels per acre, demonstrating the return on investment. Producers are therefore packaging micronutrients with bulk NPK blends to capture emerging high-margin revenue streams. Straight products will keep commanding the largest share, yet supplementary nutrients will provide incremental growth.

Conventional granular and prilled fertilizers delivered 76.10% of sales in 2025 owing to established supply chains, low per-unit cost, and compatibility with existing spreader equipment. Nevertheless, specialty formulations are expanding at a 5.18% CAGR as growers increasingly weigh environmental compliance and nutrient use efficiency. Controlled-release fertilizers such as polymer-coated urea allow steady nitrogen availability that synchronizes with crop uptake, leading to an adoption growth of 25% in Corn Belt corn systems. The United States fertilizers market size for specialty forms is bolstered by liquid solutions that integrate with sprayer fleets for variable-rate placement. Water-soluble formulations command high premiums in greenhouse and hydroponic operations where precise nutrient dosing curbs waste and boosts quality.

EPA Worker Protection Standards favor products that limit dust and applicator exposure, nudging demand toward liquids and coated granules. Nutrien reported significant revenue growth in its specialty division in 2024, citing strong orders for controlled-release and liquid products used in precision agriculture. The growth trajectory is expected to accelerate because specialty blends qualify for carbon programs and tax rebates that require demonstrated increases in nutrient efficiency, positioning them as multipurpose solutions in a tightening regulatory environment.

The United States Fertilizers Market is Segmented by Type (Complex, Straight), Form (Conventional, Specialty), Application Mode (Fertigation, Foliar, Soil), and Crop Type (Field Crops, Horticultural Crops, Turf & Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- CF Industries Holdings, Inc.

- Nutrien Ltd.

- The Mosaic Company

- The Andersons Inc.

- Yara International ASA

- Haifa Group

- ICL Group Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile SA

- Wilbur-Ellis Company LLC (Wilbur-Ellis Holdings Inc.)

- Intrepid Potash Inc.

- Compass Minerals International Inc.

- J.R. Simplot Company

- Growmark Inc.

- CHS Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Precision agriculture adoption and technology integration

- 4.5.2 Enhanced-efficiency fertilizer development and policy support

- 4.5.3 Commodity price impacts on farmer purchasing power

- 4.5.4 Regenerative farming and carbon-credit programs

- 4.5.5 Gulf Coast green-ammonia capacity build-out

- 4.5.6 Mississippi intermodal fertilizer corridors

- 4.6 Market Restraints

- 4.6.1 Natural gas price volatility effects on nitrogen costs

- 4.6.2 Tighter nutrient-runoff regulations

- 4.6.3 Biologic nutrition substitutes in specialty crops

- 4.6.4 Aging ammonia pipeline network risks

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Anhydrous Ammonia

- 5.1.2.2.3 Urea

- 5.1.2.2.4 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application

- 5.3.1 Soil

- 5.3.2 Foliar

- 5.3.3 Fertigation

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 CF Industries Holdings, Inc.

- 6.4.2 Nutrien Ltd.

- 6.4.3 The Mosaic Company

- 6.4.4 The Andersons Inc.

- 6.4.5 Yara International ASA

- 6.4.6 Haifa Group

- 6.4.7 ICL Group Ltd

- 6.4.8 Koch Industries Inc.

- 6.4.9 Sociedad Quimica y Minera de Chile SA

- 6.4.10 Wilbur-Ellis Company LLC (Wilbur-Ellis Holdings Inc.)

- 6.4.11 Intrepid Potash Inc.

- 6.4.12 Compass Minerals International Inc.

- 6.4.13 J.R. Simplot Company

- 6.4.14 Growmark Inc.

- 6.4.15 CHS Inc.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZERS CEOS

2026年全球生物炭肥料市場報告

2026年全球生物炭肥料市場報告 幾丁質肥料市場:2026-2032年全球市場預測(按應用、類型、原料、配方和分銷管道分類)肥料包膜市場:2026-2032年全球市場預測(以包膜化學、釋放機制、包膜養分類型、外形規格、製造流程、最終用途及通路分類)化肥市場:2026-2032年全球市場預測(依產品類型、作物類型、包裝、施用方法、最終用戶和分銷管道分類)藻類肥料市場:2026-2032年全球市場預測(依原料、產品類型、通路及應用分類)複合肥料市場:按產品類型、作物類型、物理形態和應用分類的全球市場預測,2026-2032年顆粒肥料市場:依產品類型、作物類型、配方類型、施用方法、包裝類型、使用時間、最終用戶和銷售管道分類-2026-2032年全球預測

幾丁質肥料市場:2026-2032年全球市場預測(按應用、類型、原料、配方和分銷管道分類)肥料包膜市場:2026-2032年全球市場預測(以包膜化學、釋放機制、包膜養分類型、外形規格、製造流程、最終用途及通路分類)化肥市場:2026-2032年全球市場預測(依產品類型、作物類型、包裝、施用方法、最終用戶和分銷管道分類)藻類肥料市場:2026-2032年全球市場預測(依原料、產品類型、通路及應用分類)複合肥料市場:按產品類型、作物類型、物理形態和應用分類的全球市場預測,2026-2032年顆粒肥料市場:依產品類型、作物類型、配方類型、施用方法、包裝類型、使用時間、最終用戶和銷售管道分類-2026-2032年全球預測 矽肥市場報告:按類型、形態、應用和地區分類(2026-2034年)

矽肥市場報告:按類型、形態、應用和地區分類(2026-2034年) ATS肥料市場規模、佔有率和成長分析:按產品類型、形態、應用、作物類型、最終用戶、分銷管道和地區分類 - 2026-2033年行業預測

ATS肥料市場規模、佔有率和成長分析:按產品類型、形態、應用、作物類型、最終用戶、分銷管道和地區分類 - 2026-2033年行業預測 越南化肥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

越南化肥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)