|

市場調查報告書

商品編碼

1940815

越南容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Container Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

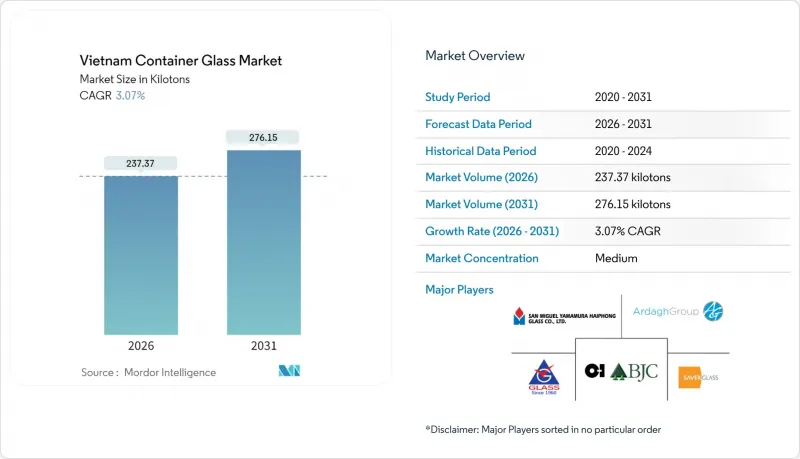

2025年越南容器玻璃市場價值為230.30千噸,預計2031年將達到276.15千噸,高於2026年的237.37千噸。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.07%。

人口穩定成長、可支配收入增加以及越南作為區域出口樞紐的地位支撐了市場需求,而對永續包裝的監管支持則增強了長期前景。預計到2024年,製造業的外國直接投資(FDI)將達到255.8億美元,這將推動熔爐升級以提高效率和產能。飲料、化妝品和製藥業的優質化趨勢促使品牌所有者更傾向於使用玻璃而非塑膠,因為他們追求更優異的阻隔性能和更高階的貨架形象。儘管電價上漲和再生寶特瓶(rPET)的替代正在減緩市場成長勢頭,但越南修訂後的《藥品管理法》(將於2025年7月生效)中包含的優惠政策正在推動對琥珀色和I型藥用玻璃的特殊需求。建立覆蓋全國的廢玻璃回收網路對於脫碳和成本控制仍然至關重要,對回收基礎設施的投資已被列為戰略重點。

越南玻璃容器市場趨勢與洞察

ESG主導的出口包裝轉變

國際買家,主要來自歐洲和北美,對高階食品和飲料進口包裝的可回收要求日益成長,迫使越南出口商從塑膠包裝轉向玻璃包裝。咖啡、茶葉和特色食品生產商表示,採用玻璃包裝可獲得15-20%的價格溢價,推動了越南玻璃容器市場的發展。玻璃包裝也有助於提升原產地品牌形象,並降低與環境標準相關的貿易政策風險。從越南採購的跨國公司正在供應商合約中加入嚴格的永續性條款,從而確保越南國內玻璃製造商的穩定銷售。這種轉變在主要出口港口附近尤其明顯。中期來看,預期環境、社會和治理(ESG)合規將推動出口導向需求以0.8%的複合年成長率成長。

外商直接主導的爐窯升級與產能擴張

2024年,將有255.8億美元的製造業外商直接投資流入越南,透過合資企業促進技術向越南玻璃容器市場的轉移。引進的富氧燃燒爐與傳統設備相比,可減少約18%的二氧化碳排放。位於平陽省和海防省的新生產線將降低燃料消耗,提高著色柔軟性,使生產商能夠在不影響生產線效率的前提下,擴大高利潤琥珀色玻璃的生產。這項多年投資計劃,加上越南工業園區的擴建,將確保玻璃級堿灰和耐火材料的進口需求穩定。從長遠來看,現代化生產能力的擴張將提高國內供應的韌性,並降低對進口藥品瓶灌裝的依賴。

電力成本上漲和電網不穩定

2024年10月,越南平均零售電費達到每度電2103.11越南盾,尖峰時段3,640越南盾。能源成本約佔玻璃生產成本的23%,因此價格上漲會擠壓利潤空間,並抑制熔爐維修。停電會促使企業投資柴油發電設施,但也會因批次溫度降低而導致更高的廢品率。政府計劃將2025年360億美元基礎設施預算的80%以上用於發電和輸電項目,以穩定電力供應。然而,短期波動預計將使預期複合年成長率下降0.6個百分點。

細分市場分析

預計到2025年,飲料業將以60.74%的市場佔有率引領越南玻璃容器市場,並在2031年之前保持銷量主導地位,這主要得益於國內啤酒產量的擴大和出口型烈酒裝瓶商數量的增加。玻璃瓶仍然是高階拉格啤酒和精釀啤酒品牌的首選,這得益於成熟的可回收瓶系統,該系統降低了單位填充成本。化妝品和個人護理品行業雖然銷售小規模,但預計將成為成長最快的品類,複合年成長率達3.52%,這反映了消費者可支配收入的增加和電子商務的日益普及。高所得消費者將玻璃容器與產品純度連結起來,這使得中端本土品牌能夠在不犧牲利潤率的情況下提升包裝等級。藥品玻璃的需求受益於修訂後的《藥品法》推動的國內灌裝和包裝生產線的建立,從而確保了對ISO認證管瓶的穩定需求。調味品和蜂蜜等食品應用領域也呈現穩定成長,這主要得益於對日本和韓國的出口需求。同時,儘管產量不高,但作為最高階的細分市場,香水的單位盈利最高。

從絕對數量來看,預計2026年至2031年間,飲料業將成為越南玻璃容器市場噸位成長最大的產業。同時,由於增值裝飾加工、小批量生產以及高階護膚品所需的厚壁規格,化妝品行業的利潤率預計將有所提高。醫藥玻璃受到嚴格的監管標準約束,這些標準構成了准入壁壘,限制了競爭,從而支撐了其特殊的溢價。因此,均衡的終端使用者結構將增強生產商的抗風險能力,並減輕因大宗商品價格波動和飲料季節性週期造成的收入波動。

越南玻璃容器市場報告按最終用戶(飲料[含酒精飲料(啤酒、葡萄酒、烈酒、其他酒精飲料)、非酒精飲料(碳酸飲料、乳製品飲料等)]、食品[果醬和果凍、調味品和醬料等]、化妝品和個人護理等)和顏色(無色、琥珀色、綠色等)進行細分。市場預測以千噸為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 出口包裝的ESG主導轉型

- 外商主導的爐窯升級與產能擴張

- 擴大製藥生產

- 快速成長的化妝品和個人護理行業

- 政府針對一次性塑膠製品的舉措

- 酒精飲料產量迅速成長

- 市場限制

- 電力成本上漲和電網不穩定

- 替代壓力用於rPET瓶

- 玻璃屑收集基礎設施的漏洞

- 物流和損失挑戰

- PESTEL 分析

- 產業供應鏈分析

- 越南容器玻璃熔爐的生產能力和位置

- 工廠選址及投產

- 生產能力

- 爐型

- 所產玻璃的顏色

- 貨櫃玻璃進出口資料 - 主要進出口目的地

- 進口量及進口額(2021-2024 年)

- 出口量和出口額(2021-2024 年)

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 原料分析

- 玻璃包裝的回收趨勢

- 玻璃包裝需求與供給分析

第5章 市場規模與成長預測

- 最終用戶

- 飲料

- 酒精飲料

- 啤酒

- 葡萄酒

- 烈酒

- 其他酒精飲料(蘋果酒和其他發酵飲料)

- 非酒精性

- 果汁

- 碳酸軟性飲料(CSD)

- 乳製品飲料

- 其他非酒精飲料

- 酒精飲料

- 食品(果醬、果凍、橘子醬、蜂蜜、香腸和調味品、食用油、醃菜)

- 化妝品和個人護理

- 藥品(不含管瓶和安瓿瓶)

- 香水

- 飲料

- 按顏色

- 綠色的

- 琥珀色

- 無色透明

- 其他顏色

第6章 競爭情勢

- 市場集中度

- 策略趨勢與發展

- 公司市佔率分析(基於當前產能)

- 公司簡介

- OI BJC Vietnam Glass Company Limited

- San Miguel Yamamura Hai Phong Glass Co., Ltd.

- Thuduc Glass Bottle Joint Stock Company

- Bao Minh Glass Joint Stock Company

- San Miguel Yamamura Phu Tho Packaging Co., Ltd.

- Saverglass SAS

- Verallia Packaging SAS

- Ardagh Group SA

- Go Vap Glass

- Bormioli Rocco

第7章 市場機會與未來展望

The Vietnam container glass market was valued at 230.30 kilotons in 2025 and estimated to grow from 237.37 kilotons in 2026 to reach 276.15 kilotons by 2031, at a CAGR of 3.07% during the forecast period (2026-2031).

Steady population growth, rising disposable incomes, and Vietnam's position as a regional export base underpin demand, while regulatory support for sustainable packaging reinforces long-term prospects. Foreign direct investment (FDI) into manufacturing, worth USD 25.58 billion in 2024, is catalyzing furnace upgrades that improve efficiency and capacity. Premiumization trends in beverages, cosmetics, and pharmaceuticals favor glass over plastic as brand owners seek superior barrier properties and a premium shelf image. Electricity price escalation and rPET substitution temper momentum, yet incentives embedded in Vietnam's amended Law on Pharmacy, effective July 2025, expand specialized demand for amber and Type I pharmaceutical glass. Building a nationwide cullet collection network remains vital for decarbonization and cost control, positioning recycling infrastructure investment as a strategic priority.

Vietnam Container Glass Market Trends and Insights

ESG-Driven Export Packaging Shift

International buyers, especially in Europe and North America, increasingly require recyclable packaging for premium food and beverage imports, prompting Vietnam's exporters to switch from plastic to glass. Coffee, tea, and specialty food producers report 15-20% price premiums when adopting glass, bolstering the Vietnam container glass market. Glass also supports origin branding efforts and mitigates trade-policy risks related to environmental standards. Multinational corporations sourcing from Vietnam embed strict sustainability clauses in supplier contracts, ensuring a stable offtake for domestic glass producers. This shift intensifies near major ports where export consolidation occurs. Over the medium term, ESG compliance is expected to lift export-oriented demand by an incremental 0.8% of the forecast CAGR.

FDI-Driven Furnace Upgrades and Capacity Additions

USD 25.58 billion in manufacturing FDI in 2024 channels technology transfer into the Vietnam container glass market through joint ventures that deploy oxy-combustion furnaces able to trim CO2 emissions by about 18% versus legacy units. New lines in Binh Duong and Hai Phong cut fuel consumption and widen color flexibility, letting producers chase higher-margin amber batches without compromising line efficiency. Multi-year investment schedules align with Vietnam's industrial-park expansion, guaranteeing steady glass-grade soda ash imports and furnace-refractory demand. Over the long term, modern capacity raises domestic supply resilience and limits import reliance on bottles for pharmaceutical filling operations.

Electricity Cost Inflation and Grid Instability

Average retail electricity tariffs hit VND 2,103.11 per kWh in October 2024, with peak-hour rates soaring to VND 3,640 per kWh. Energy accounts for roughly 23% of glass production cost, so spikes compress margins and deter furnace rebuilds. Grid outages drive investment in diesel backup and elevate scrap rates when batch temperatures fall. The government plans to allocate over 80% of a USD 36 billion 2025 infrastructure budget to power generation and transmission, aiming to stabilize supply. Still, near-term volatility subtracts 0.6 percentage points from expected CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Manufacturing Expansion

- Booming Cosmetics and Personal Care Sector

- rPET Bottle Substitution Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The beverages segment dominated the Vietnam container glass market with 60.74% market share in 2025 and is expected to maintain volume leadership through 2031 as domestic beer output scales and export-oriented spirits bottlers expand. Glass bottles remain preferred for premium lager and craft beer branding, supported by established returnable bottle systems that reduce per-fill cost. Cosmetics and personal care, though smaller in tonnage, are projected as the fastest-growing category at a 3.52% CAGR, reflecting rising disposable incomes and e-commerce penetration. High-spend consumers link glass with product purity, enabling mid-sized local brands to trade up packaging without sacrificing margin. Pharmaceutical glass demand benefits from new domestic fill-finish lines encouraged by the amended pharmacy law, ensuring consistent offtake for ISO-certified vials. Food applications such as condiments and honey experience stable growth, powered by export demand to Japan and South Korea, while perfumery, the most premium niche, commands the highest unit revenue despite modest volumes.

In absolute terms, beverages are forecast to add the largest incremental tonnage to the Vietnam container glass market size over 2026-2031. Cosmetics, however, deliver margin upside through value-added decoration, smaller batch runs, and thicker-wall specifications favored by luxury skincare. Pharmaceutical glass's stringent regulatory standards set a high barrier to entry, limiting competition and supporting specialized price premiums. A balanced end-user portfolio, therefore, enhances producer resilience, smoothing revenue against commodity price swings and seasonal beverage cycles.

The Vietnam Container Glass Market Report is Segmented by End-User (Beverages [Alcoholic {Beer, Wine, Spirits, Other Alcoholic Beverages}, and Non-Alcoholic {Carbonated Drinks (CSDs), Dairy Product Based Drinks, and More}], Food [Jam and Jelly, Condiments and Sauces, and More], Cosmetics and Personal Care, and More), Color (Flint, Amber, Green, and More). The Market Forecasts are Provided in Terms of Volume (Kilotons).

List of Companies Covered in this Report:

- O-I BJC Vietnam Glass Company Limited

- San Miguel Yamamura Hai Phong Glass Co., Ltd.

- Thuduc Glass Bottle Joint Stock Company

- Bao Minh Glass Joint Stock Company

- San Miguel Yamamura Phu Tho Packaging Co., Ltd.

- Saverglass SAS

- Verallia Packaging SAS

- Ardagh Group S.A.

- Go Vap Glass

- Bormioli Rocco

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ESG-Driven Export Packaging Shift

- 4.2.2 FDI-Driven Furnace Upgrades and Capacity Additions

- 4.2.3 Pharmaceutical Manufacturing Expansion

- 4.2.4 Booming Cosmetics and Personal Care Sector

- 4.2.5 Government Push Against Single-Use Plastics

- 4.2.6 Surging Alcoholic Beverage Output

- 4.3 Market Restraints

- 4.3.1 Electricity Cost Inflation and Grid Instability

- 4.3.2 rPET Bottle Substitution Pressure

- 4.3.3 Weak Cullet Collection Infrastructure

- 4.3.4 Logistics and Breakage Challenges

- 4.4 PESTEL Analysis

- 4.5 Industry Supply-Chain Analysis

- 4.6 Container Glass Furnace Capacity and Locations in Vietnam

- 4.6.1 Plant Locations and Year of Commencement

- 4.6.2 Production Capacities

- 4.6.3 Types of Furnaces

- 4.6.4 Color of Glass Produced

- 4.7 Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1 Import Volume and Value, 2021-2024

- 4.7.2 Export Volume and Value, 2021-2024

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Raw Material Analysis

- 4.10 Recycling Trends for Glass Packaging

- 4.11 Demand vs Supply Analysis for Glass Packaging

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user

- 5.1.1 Beverages

- 5.1.1.1 Alcoholic

- 5.1.1.1.1 Beer

- 5.1.1.1.2 Wine

- 5.1.1.1.3 Spirits

- 5.1.1.1.4 Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2 Non-Alcoholic

- 5.1.1.2.1 Juices

- 5.1.1.2.2 Carbonated Drinks (CSDs)

- 5.1.1.2.3 Dairy Product Based Drinks

- 5.1.1.2.4 Other Non-Alcoholic Beverages

- 5.1.1.1 Alcoholic

- 5.1.2 Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3 Cosmetics and Personal Care

- 5.1.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5 Perfumery

- 5.1.1 Beverages

- 5.2 By Color

- 5.2.1 Green

- 5.2.2 Amber

- 5.2.3 Flint

- 5.2.4 Other Colors

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 O-I BJC Vietnam Glass Company Limited

- 6.4.2 San Miguel Yamamura Hai Phong Glass Co., Ltd.

- 6.4.3 Thuduc Glass Bottle Joint Stock Company

- 6.4.4 Bao Minh Glass Joint Stock Company

- 6.4.5 San Miguel Yamamura Phu Tho Packaging Co., Ltd.

- 6.4.6 Saverglass SAS

- 6.4.7 Verallia Packaging SAS

- 6.4.8 Ardagh Group S.A.

- 6.4.9 Go Vap Glass

- 6.4.10 Bormioli Rocco

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

玻璃器皿市場-2026-2032年全球市場預測

玻璃器皿市場-2026-2032年全球市場預測 玻璃器皿市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年)玻璃瓶市場:依材質、顏色、容量、應用及通路分類-2026-2032年全球市場預測

玻璃器皿市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年)玻璃瓶市場:依材質、顏色、容量、應用及通路分類-2026-2032年全球市場預測 酒精飲料瓶市場規模、佔有率和成長分析:按形狀、容量、材質、應用和地區分類-2026-2033年產業預測

酒精飲料瓶市場規模、佔有率和成長分析:按形狀、容量、材質、應用和地區分類-2026-2033年產業預測 全球保溫瓶市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。

全球保溫瓶市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。 德國容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026-2034年全球容器玻璃市場規模、佔有率、趨勢和成長分析報告

德國容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026-2034年全球容器玻璃市場規模、佔有率、趨勢和成長分析報告 日本玻璃容器市場規模、佔有率、趨勢和預測:按產品、最終用途行業和地區分類,2026-2034年

日本玻璃容器市場規模、佔有率、趨勢和預測:按產品、最終用途行業和地區分類,2026-2034年 2026年全球容器玻璃市場報告2026年全球運動水壺市場報告

2026年全球容器玻璃市場報告2026年全球運動水壺市場報告