|

市場調查報告書

商品編碼

1940810

泰國網路安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thailand Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

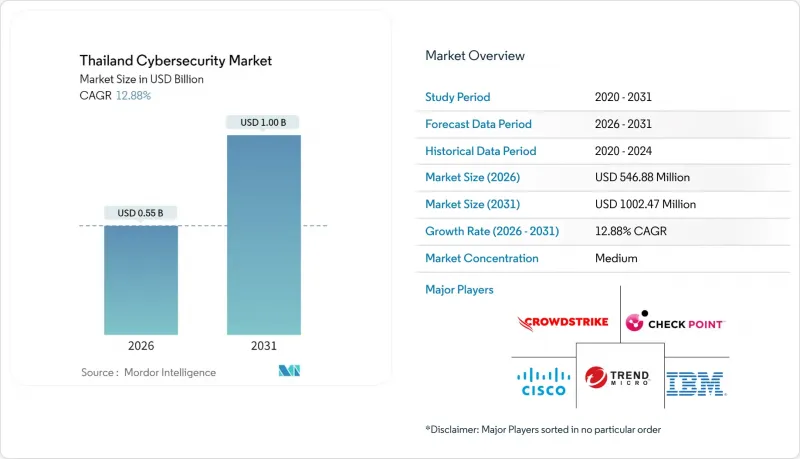

2025年泰國網路安全市場價值4.8448億美元,預計到2031年將達到10.0247億美元,高於2026年的5.4688億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 12.88%。

支付系統的數位化、公共部門雲端遷移以及工業界5G的普及正在擴大威脅面,並將網路安全支出轉向關鍵基礎設施投資。國家數位身分平台、PromptPay的成長以及G-Cloud政策正在推動各組織向零信任架構和雲端原生安全控制轉型。能夠提供泰語支援、符合PDPA標準的自動化解決方案以及託管服務交付的供應商,其表現始終優於僅提供產品的競爭對手。儘管人才短缺和中小企業對成本的敏感性仍然是阻礙因素,但勒索軟體攻擊的日益增多以及關鍵基礎設施監管的加強,已將網路風險提升至全國經營團隊的首要位置。

泰國網路安全市場趨勢與洞察

加速泰國金融服務業數位化銀行的普及

2023年,PromptPay處理了92億筆交易,總額達13.9兆泰銖(約4,270億美元),為行動銀行和開放API銀行業務創造了新的攻擊面。金融機構正在部署應用防火牆、交易等級異常偵測分析和身分編配,以滿足沙箱需求並保障行動管道的安全。基於強身份驗證和微隔離的零信任框架正在取代以防火牆為中心的設計。為了滿足金融機構的業務法規要求,支出重點正從事件回應轉向持續的威脅搜尋。供應商的差異化優勢正在轉向能夠自動產生合規報告並縮短混合環境中平均偵測時間的整合平台。

加速政府雲端遷移(G-Cloud 和 NDID)

數位政府發展局已撥款10億泰銖(約3000萬美元)用於2025年的雲端服務,加速政府各部會和機構採用G-Cloud。國家數位身分識別碼(NDID)註冊數量已超過5000萬,推動了生物識別身分管治和加密金鑰管理解決方案的採購。各機構必須遵守2025年網站安全標準,該標準強制要求加密、基於角色的存取控制和事件回應手冊。國際供應商已與國家網路安全中心(NCSA)簽署合作備忘錄,以實現威脅情報源的本地化並提供泰語安全營運中心(SOC)培訓。在多重雲端日益複雜的背景下,雲端安全態勢管理和合規自動化工具在競標清單中佔據主導地位。

泰語網路安全人員短缺

僅有58萬人具備足夠的數位技能,而每年IT專業畢業生人數仍維持在約3,500人。曼谷25%至30%的薪資成長迫使企業將安全營運中心(SOC)營運外包或延後計劃。在地化的認證計畫仍然匱乏,促使ISC2和NCSA共同發起一項計劃,目標是在2026年前培訓1萬人。然而,許多本地企業仍依賴通用IT人員來管理安全工具,這降低了其防禦成熟度,並增加了安全漏洞的風險。人才短缺導致採購週期延長,並促使企業傾向於採用包含專業知識的託管服務模式。

細分市場分析

到2025年,解決方案領域將佔泰國網路安全市場佔有率的60.88%,顯示企業仍將持續依賴邊界控制。雖然該領域對於分公司連接和OT隔離仍然至關重要,但隨著預算轉向雲端彈性,其成長速度正在放緩。受G-Cloud部署以及金融科技和電子商務企業採用多重雲端架構的推動,雲端安全正以16.05%的複合年成長率推動創新。能夠將以工作負載為中心的微隔離、CASB功能和合規性儀表板相結合的供應商,能夠滿足尋求深度網路防禦(NDID)的買家的需求。隨著企業面臨複雜的最佳化和技能短缺問題,專業服務和託管服務的需求正在成長。端點、數據和身份模組與基於人工智慧的異常檢測功能整合,這些功能可以從泰國資料集中學習,幫助團隊減少警報噪音並加快響應速度。

雲端原生安全防護也推動了對姿態管理工具的需求,這些工具能夠根據 PDPA 和 CII 標準對配置進行基準測試。受 API 驅動的銀行和超級應用生態系統的推動,應用程式安全方面的支出正在增加。在發生 5273 起資料外洩事件後,資料安全的迫切性促使支付工作流程中採用令牌化和資料防洩漏 (DLP) 技術。隨著零售商和醫療機構在雲端遷移截止日期前對敏感欄位進行加密,泰國以資料為中心的控制網路安全市場正在擴張。交付模式正從硬體設備轉向整合威脅情報、自動化和區域合規性組件的 SaaS 平台,預計到 2030 年,這一趨勢將重塑採購評估模式。

預計到2025年,雲端技術將佔泰國網路安全市場規模的64.26%,並在2031年之前以14.20%的複合年成長率成長。政府的「雲端優先」政策、AWS 50億美元的基礎設施投資承諾以及微軟的政府安全計劃,共同推動了向IaaS和PaaS的新計畫轉型。泰國銀行、金融和保險(BFSI)監管機構現已允許在其監管沙箱內運行公共雲端工作負載,鼓勵銀行遷移非核心應用程式並採用API安全閘道器。跨境資料流的需求正在推動由國家通訊業者營運的租戶管理加密金鑰和主權雲端區域的普及。

在公共產業、交通運輸和傳統SCADA營運商等對空氣間隙和確定性延遲要求極高的行業,本地部署解決方案仍然佔據主導地位。隨著工廠將OT網路連接到雲端分析平台,混合環境正在興起,這就需要一個統一的管理平台,涵蓋防火牆設備和雲端工作負載代理。提供兩種部署模式以及單一策略引擎的供應商正在贏得市場佔有率。泰國網路安全市場本地部署的佔有率正在逐漸下降,因為更新換代週期往往傾向於虛擬化部署模式,即使在私人資料中心也是如此。將5G MEC節點整合到雲端儀表板中正是這種融合部署趨勢的典型體現。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速泰國銀行、金融和保險(BFSI)產業數位化銀行服務的採用

- 加速政府雲端遷移(G-Cloud 和 NDID)

- 5G部署推動了對物聯網邊緣安全的需求

- 泰國電子商務商品交易總額(GMV)正在快速成長。

- 針對中小企業的勒索軟體即服務攻擊激增

- 東部經濟走廊的OT/ICS安全漏洞

- 市場限制

- 泰語網路安全人員短缺

- 中小企業的價格敏感型採購行為

- 修補遺留的關鍵基礎設施系統非常困難

- 網路保險市場的碎片化

- 產業價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

- 監管環境

- 技術展望

第5章 市場規模與成長預測

- 報價

- 解決方案

- 應用程式安全

- 雲端安全

- 資料安全

- 身分和存取管理

- 基礎設施保護

- 綜合風險管理

- 網路安全設備

- 端點安全

- 服務

- 專業服務

- 託管服務

- 解決方案

- 透過部署模式

- 本地部署

- 雲

- 按最終用戶行業分類

- BFSI

- 衛生保健

- 資訊科技/通訊

- 工業與國防

- 製造業

- 零售與電子商務

- 能源與公共產業

- 其他

- 按公司規模

- 小型企業

- 主要企業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- CrowdStrike Holdings, Inc.

- McAfee LLC

- International Business Machines Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Atos SE

- Thales Group

- NEC Corporation

- Accenture plc

- Deloitte Touche Tohmatsu Ltd.

- MFEC Public Company Limited

- G-Able Company Limited

- ACinfotec Company Limited

- National Telecom Public Company Limited

- Bangkok Systems and Software Co., Ltd.

第7章 市場機會與未來展望

The Thailand cybersecurity market was valued at USD 484.48 million in 2025 and estimated to grow from USD 546.88 million in 2026 to reach USD 1002.47 million by 2031, at a CAGR of 12.88% during the forecast period (2026-2031).

Payment-system digitalization, public-sector cloud migration, and industrial 5G adoption are expanding the threat surface and turning cybersecurity spending into critical infrastructure outlays. The National Digital ID platform, PromptPay growth, and G-Cloud policy have pushed organizations toward zero-trust architectures and cloud-native security controls. Vendors that combine Thai-language support, PDPA compliance automation, and managed service delivery continue to out-perform product-only competitors. The talent gap and SME cost sensitivity remain constraints, yet rising ransomware incidents and CII regulations keep cyber risk on executive agendas nationwide.

Thailand Cybersecurity Market Trends and Insights

Accelerated Digital-Banking Adoption in Thai BFSI

PromptPay processed 9.2 billion transactions worth THB 13.9 trillion (USD 0.427 trillion ) in 2023, exposing new attack surfaces in mobile and open-API banking. Financial institutions are deploying application firewalls, transaction-level anomaly analytics, and identity orchestration to meet sandbox requirements and protect mobile channels. Zero-trust frameworks built on strong authentication and micro-segmentation are replacing firewall-centric designs. Spending priorities are shifting from incident response toward continuous threat hunting that satisfies the Financial Institutions Business Act. Vendor differentiation now favors integrated platforms that automate compliance reporting and reduce mean-time-to-detect across hybrid environments.

Fast-Track Government Cloud Migration (G-Cloud and NDID)

The Digital Government Development Agency allocated THB 1 billion (USD 0.03 billion) for cloud services in FY 2025, accelerating G-Cloud rollouts across ministries. NDID enrollment has surpassed 50 million citizens, driving procurement of biometric identity governance and encryption key management. Agencies must comply with the 2025 Website Security Standard, which mandates encryption, role-based access, and incident response playbooks. International vendors have entered memoranda with NCSA to localize threat-intelligence feeds and Thai-language SOC training. Cloud security posture management and compliance automation tools dominate tender lists as multi-cloud complexity rises.

Shortage of Thai-Language Cybersecurity Talent

Only 0.58 million citizens possess adequate digital skills, and annual IT graduate output is roughly 3,500 professionals. Salary inflation of 25-30% in Bangkok prompts firms to outsource SOC operations or delay projects. Localized certification pathways remain scarce, so ISC2 and NCSA launched a program to train 10,000 practitioners by 2026. Nevertheless, most provincial enterprises rely on generalist IT staff to manage security tooling, lowering defense maturity and elevating breach risk. The talent shortfall prolongs procurement cycles and favors managed service models that embed expertise.

Other drivers and restraints analyzed in the detailed report include:

- 5G Rollout Spurring IoT-Edge Security Demand

- Rapid Growth of Thailand E-Commerce GMV

- Price-Sensitive SME Buyer Behavior

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held the largest 60.88% Thailand cybersecurity market share in 2025, underscoring the residual reliance on perimeter controls. The segment remains vital for branch connectivity and OT segregation, but its growth pace is moderating as budgets pivot to cloud resilience. Cloud Security leads the innovation curve with a 16.05% CAGR, propelled by G-Cloud rollouts and multi-cloud adoption among fintech and e-commerce operators. Vendors that fuse workload-centric micro-segmentation, CASB functions, and compliance dashboards resonate with buyers seeking NDID alignment. Professional Services and Managed Services expand as enterprises confront complex optimization and skills shortages. Endpoint, data, and identity modules integrate AI-based anomaly detection that learns from Thai-language data sets, helping teams cut alert noise and accelerate response.

Cloud-native protection also amplifies demand for posture-management tools that benchmark configurations against PDPA and CII baselines. Application Security spending rises alongside API-driven banking and super-app ecosystems. Data Security urgency grows after 5,273 leak cases, pushing tokenization and DLP adoption inside payment workflows. Thailand cybersecurity market size for data-centric controls is climbing as retailers and hospitals encrypt sensitive fields ahead of cloud migration deadlines. The offering mix is shifting from hardware appliances toward SaaS platforms that bundle threat intelligence, automation, and localized compliance artifacts, a trend expected to reshape procurement scoring models by 2030.

Cloud deployments captured 64.26% share of the Thailand cybersecurity market size in 2025 and are set to grow at a 14.20% CAGR through 2031. The government's Cloud First policy, AWS's USD 5 billion infrastructure pledge, and Microsoft's Government Security Program have tipped new projects toward IaaS and PaaS. BFSI regulators now permit public cloud workloads in regulatory sandboxes, encouraging banks to migrate non-core applications and adopt API security gateways. Cross-border data-flow requirements drive uptake of tenant-controlled encryption keys and sovereign cloud zones operated by National Telecom.

On-premise solutions still hold sway in utilities, transport, and legacy SCADA operators where air-gaps and deterministic latency matter. Hybrid environments emerge as plants connect OT networks to cloud analytics platforms, requiring unified management planes that span firewall appliances and cloud workload agents. Vendors supplying both form factors with a single policy engine win favor. Thailand cybersecurity market share for on-premise deployments gradually declines as refresh cycles favor virtual form factors even inside private data centers. Integration of 5G MEC nodes into cloud dashboards exemplifies the converging deployment story.

The Thailand Cybersecurity Market Report is Segmented by Offering (Solutions, Services), Deployment Mode (On-Premise, Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, and More), End-User Enterprise Size (Small and Medium Enterprises, Large Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- CrowdStrike Holdings, Inc.

- McAfee LLC

- International Business Machines Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Atos SE

- Thales Group

- NEC Corporation

- Accenture plc

- Deloitte Touche Tohmatsu Ltd.

- MFEC Public Company Limited

- G-Able Company Limited

- ACinfotec Company Limited

- National Telecom Public Company Limited

- Bangkok Systems and Software Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated digital-banking adoption in Thai BFSI

- 4.2.2 Fast-track government cloud migration (G-Cloud and NDID)

- 4.2.3 5G rollout spurring IoT-edge security demand

- 4.2.4 Rapid growth of Thailand E-commerce GMV

- 4.2.5 Surge in ransomware-as-a-service attacks on SMEs

- 4.2.6 OT/ICS security gaps in Eastern Economic Corridor

- 4.3 Market Restraints

- 4.3.1 Shortage of Thai-language cybersecurity talent

- 4.3.2 Price-sensitive SME buyer behavior

- 4.3.3 Legacy critical-infrastructure systems difficult to patch

- 4.3.4 Fragmented cyber-insurance landscape

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Others

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Palo Alto Networks, Inc.

- 6.4.3 Fortinet, Inc.

- 6.4.4 Check Point Software Technologies Ltd.

- 6.4.5 Trend Micro Incorporated

- 6.4.6 CrowdStrike Holdings, Inc.

- 6.4.7 McAfee LLC

- 6.4.8 International Business Machines Corporation

- 6.4.9 Microsoft Corporation

- 6.4.10 Amazon Web Services, Inc.

- 6.4.11 Atos SE

- 6.4.12 Thales Group

- 6.4.13 NEC Corporation

- 6.4.14 Accenture plc

- 6.4.15 Deloitte Touche Tohmatsu Ltd.

- 6.4.16 MFEC Public Company Limited

- 6.4.17 G-Able Company Limited

- 6.4.18 ACinfotec Company Limited

- 6.4.19 National Telecom Public Company Limited

- 6.4.20 Bangkok Systems and Software Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年

IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年 通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析

通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析 網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 2026-2030年全球公共部門網路安全市場

2026-2030年全球公共部門網路安全市場 全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034) 後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶人工智慧驅動的網路安全解決方案市場預測至2034年:按交付方式、技術類型、安全類型、部署方式、組織規模、最終用戶和地區分類的全球分析

後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶人工智慧驅動的網路安全解決方案市場預測至2034年:按交付方式、技術類型、安全類型、部署方式、組織規模、最終用戶和地區分類的全球分析 網路安全市場:按組件、安全類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測人工智慧網路安全市場預測至2034年—按交付方式、安全類型、部署方式、技術、應用、最終用戶和地區分類的全球分析金融科技網路安全解決方案市場預測至2034年-按組件、安全類型、部署模式、組織規模、應用、最終用戶和地區分類的全球分析

網路安全市場:按組件、安全類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測人工智慧網路安全市場預測至2034年—按交付方式、安全類型、部署方式、技術、應用、最終用戶和地區分類的全球分析金融科技網路安全解決方案市場預測至2034年-按組件、安全類型、部署模式、組織規模、應用、最終用戶和地區分類的全球分析