|

市場調查報告書

商品編碼

1940801

社群媒體聆聽:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Social Media Listening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

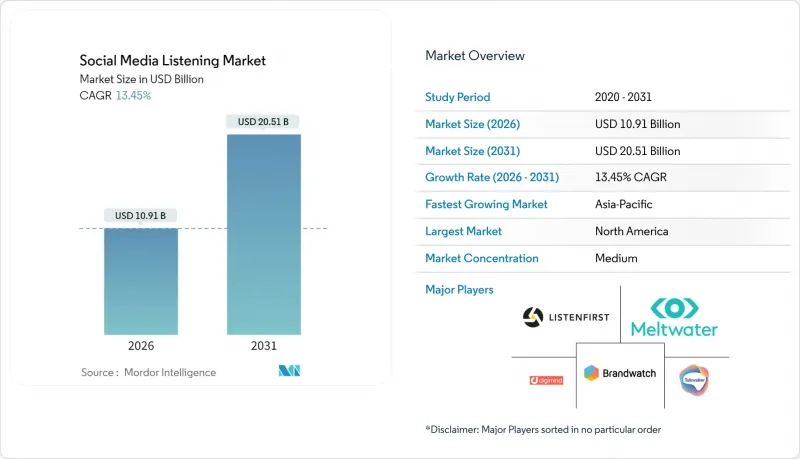

預計到 2025 年,社群媒體監聽市場價值將達到 96.2 億美元,到 2031 年將達到 205.1 億美元,高於 2026 年的 109.1 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 13.45%。

這一上升趨勢主要源自於企業轉向主動互動,依賴於社交平臺上捕捉到的早期情緒訊號。北美地區保持主導地位,這得益於幾起備受矚目的危機事件後,人們對品牌安全的日益關注。同時,亞太地區成長最快,這主要得益於在地化平台的擴張和智慧型手機普及率的加速提升。儘管軟體仍然是核心投資領域,但隨著企業需要客製化的工作流程和人工智慧模型的訓練,對專業服務的需求也在不斷成長。雖然文本分析仍然佔據主導地位,但隨著短影片在許多網路上的傳播量超過文本,影片分析的規模正在迅速擴大。

全球社群媒體聆聽市場趨勢與洞察

在主導的危機中降低品牌風險

隨著網紅爭議造成的經濟損失日益加劇,即時社群媒體情報已成為企業風險管理團隊的必備工具。擁有成熟監聽系統的品牌,其徵兆偵測與反應速度比僅依賴傳統監控方式的品牌快4.3倍,進而顯著降低損失。企業風險管理儀錶板整合了運作警報系統,使公關、法務和顧客關懷部門能夠協調快速回應。這種迫切性在面向消費者的產業尤為突出,因為一則病毒式傳播的貼文就可能毀掉數月累積的品牌價值。這種策略轉變促使各大平台增加了對危機應變模組的預算投入。能夠提供預測評分和自動化工作流程的供應商正成為風險規避型負責人的首選。

生成式人工智慧情感分析提升亞太地區零售業投資報酬率

大規模語言模型 (LLM) 正在重新定義情緒分析的準確性,尤其是在那些因語碼轉換和俚語而難以進行傳統自然語言處理 (NLP) 的市場中。 GPT-4 在二元情緒分析任務中達到了 93% 的準確率,從而能夠跨多語言地區提供高度精準的洞察。亞太地區的零售商正在迅速利用這項進步來最佳化促銷活動和產品改進。跨境經銷商尤其受惠於 LLM 無需額外分析師團隊即可處理多種亞洲語言的能力。澳洲保健品製造商 Blackmores 利用以微信為中心的監測來識別消費者日益成長的擔憂,並調整通訊,從而幫助其擴大了在中國的市場佔有率。這項投資報酬率高的成功案例正在加速那些注重低利潤、高銷售量的電商企業採用 LLM 技術。

資料隱私監管碎片化

各地隱私法規的差異迫使供應商應對區域性的特定退出機制、刪除權和資料居住義務。 《加州消費者隱私法案》(CCPA) 帶來了營運負擔,要求對敏感資訊進行精細化的消費者控制和獨特的流程管理。小型供應商難以資金籌措持續的法規更新費用,隨著合規成本的上升,產業整合也正在加速。企業買家通常會部署獨立的區域實例,這削弱了全球整合控制面板的價值,並降低了投資報酬率預期。

細分市場分析

至2025年,軟體將佔據社群媒體監聽市場67.20%的佔有率,鞏固其作為企業社交智慧核心基礎的地位。負責人傾向於選擇整合監聽、互動和分析功能,並將洞察結果直接與宣傳活動管理工具對接的套件。為此,供應商正在整合API層,以連接客戶資料平台和商業智慧倉庫,從而支援更廣泛的數位體驗策略。這種商品搭售的趨勢能夠保障授權收入,即使基礎監控功能日趨普及。

業務收益雖然規模較小,但正以16.02%的複合年成長率成長,因為企業越來越將社交智慧視為一種以結果為導向的能力,而非即插即用的工具集。服務提供者現在提供危機模擬、競爭情報作戰室以及針對特定產業術語的大型語言模型 (LLM) 客製化調優服務。缺乏全天候服務的中型企業更青睞託管服務,而人工智慧調優合約則在需要領域安全模型的受監管行業中開闢了一片天地。這種雙軌成長使得純粹的社群媒體監聽服務供應商和混合型服務供應商都能在社群媒體監聽市場保持競爭力。

到2025年,大型企業將佔總支出的64.10%,因為它們正將監聽結果整合到CRM、產品和合規系統的資料湖架構中。多品牌集團利用可視化區域情緒波動的儀錶板來協調反駁論點和拓展宣傳活動。此外,隨著資訊長們優先考慮簡化的合約和提供ISO認證安全框架的供應商,企業採購週期正在推動整合。

然而,中小企業是成長最快的細分市場,年複合成長率(CAGR)高達 15.35%。雲端定價、基於模板的部署和互動式使用者介面正在降低准入門檻。經合組織的一項調查預測,中小企業採用人工智慧工具的比例將從 2024 年的 26% 上升到 2025 年的 39%,這反映了數位化的加速。將社群媒體「對話」策略與客戶評價結合的小規模出口企業表示,客戶獲取效率得到了提升,驗證了這項投資的價值。供應商正以捆綁式免費加值產品瞄準這一細分市場,當需要更深入的分析或多用戶訪問時,這些產品會過渡到付費計劃。

區域分析

北美地區預計到2025年將維持41.20%的收入佔有率,這得益於其技術成熟度和在近期危機後加強的嚴格品牌保護策略。金融服務和醫療保健公司正在將社交資料整合到受監管的申訴處理系統中,以遵守諸如《加州消費者隱私法案》(CCPA)等賦予消費者廣泛資料權利的法規。持續的投資重點在於高精度風險檢測模組,以在貼文病毒式傳播之前保護品牌價值。

亞太地區預計到2031年將以16.02%的複合年成長率成長,這主要得益於平台普及率的飆升和行動商務的強勢地位。中國封閉式的網路環境要求供應商對語言模型和API連接器進行精細化調整。一些品牌,例如微信上的Blackmores,已經成功應對了這種複雜性,並實現了市場佔有率的快速成長。在印度市場,智慧型手機的普及以及區域語言社交網路的興起,使得多語言支援成為必然之選。東南亞市場用戶參與度很高,但需要能夠適應不同方言的自然語言處理技術,這推動了對服務合作夥伴的需求。

在歐洲,GDPR帶來的負擔與機會之間的平衡正在推動隱私保護分析領域的創新。媒體預算向社群影片的轉移,帶動了對多模態聲量佔有率(SOV)儀錶板的需求。拉丁美洲和中東及非洲地區雖然面積不大,但充滿活力,其成長主要集中在都市區中心和尋求衡量當地民意指標的跨國公司。海灣國家政府正在加速採用社群媒體監聽技術來追蹤大眾對服務品質的看法,從而擴大了公共部門對社群媒體監聽市場的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 危機期間以網紅為主導的品牌風險緩解策略(北美)

- 生成式人工智慧情感分類提升亞太地區零售業投資報酬率

- 歐洲電視廣告支出向社群影片的轉移正在推動對SOV分析的需求。

- 銀行、金融和保險 (BFSI) 行業申訴的監管回應時間要求

- 遊戲和直播的爆炸式成長正在創造豐富的影片和音訊資料集。

- 開放API行銷技術生態系統推動平台整合

- 市場限制

- 資料隱私法規碎片化(GDPR、CCPA、PDPA)

- 低資源語言中多語言人工智慧的準確率差距

- X(Twitter)和 Meta 提高了 API 存取費用

- 由於與內部BI/CDP重複採購,導致採購疲勞。

- 技術展望

- 監理展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素評估

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按組織規模

- 主要企業

- 中小企業

- 按分析類型

- 文字分析

- 影像分析

- 影片分析

- 語音/音訊分析

- 透過使用

- 品牌健康追蹤

- 客戶經驗管理

- 競爭標竿分析

- 潛在客戶開發和銷售監控

- 宣傳活動管理

- 危機管理

- 按行業

- 零售與電子商務

- BFSI

- 資訊科技和電信

- 媒體與娛樂

- 醫療保健和生命科學

- 旅遊與飯店

- 教育

- 其他(政府機構、非政府組織)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞

- 澳洲和紐西蘭

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- 海灣合作理事會國家

- 土耳其

- 以色列

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Meltwater

- Sprinklr

- Brandwatch(Cision LLC)

- NetBase Quid

- Talkwalker

- Digimind

- Khoros

- Clarabridge(Qualtrics)

- Mention

- Hootsuite Inc.

- Agorapulse

- Awario

- Zignal Labs

- ListenFirst

- Synthesio(Ipsos)

- Reputology

- Linkfluence

- Socialbakers(Astute)

- Keyhole Inc.

- Brand24

- Vendor Positioning Matrix

第7章 市場機會與未來展望

The social media listening market was valued at USD 9.62 billion in 2025 and estimated to grow from USD 10.91 billion in 2026 to reach USD 20.51 billion by 2031, at a CAGR of 13.45% during the forecast period (2026-2031).

The uptrend stems from enterprises shifting toward proactive engagement that relies on early sentiment signals captured on social platforms. North America retains leadership, aided by heightened brand-safety concerns following several high-profile crises, while Asia-Pacific records the steepest growth as localized platforms expand and smartphone adoption accelerates. Software remains the core investment category, although demand for expert services is climbing because firms need tailored workflows and AI model training. Text analytics still dominates, but video analytics is scaling quickly as short-form video overtakes text on many networks.

Global Social Media Listening Market Trends and Insights

Brand-risk Mitigation Amid Influencer-led Crises

Escalating financial fallout from influencer controversies is making real-time social intelligence indispensable for corporate risk teams. Brands with mature listening setups now detect brewing issues and respond 4.3 times faster than peers relying only on traditional monitoring, sharply limiting damage. Always-on alerts are being plugged into enterprise risk dashboards so PR, legal, and customer-care units can coordinate rapid remediation. Consumer-facing sectors feel the greatest urgency because a single viral post can erase months of equity building. The strategic shift elevates budget allocation for crisis-specific modules inside leading platforms. Vendors that embed predictive scoring and automated workflows gain preference among risk-averse buyers.

Generative-AI Sentiment Classification Boosting APAC Retail ROI

Large language models are rewriting sentiment analysis accuracy in markets where code-switching and slang frustrated legacy NLP. GPT-4 attains 93% precision on binary sentiment tasks, unlocking high-fidelity insights for multilingual regions. Retailers in Asia-Pacific quickly exploit the advance to fine-tune promotions and product tweaks. Cross-border sellers gain particular leverage because LLMs handle multiple Asian languages without separate analyst teams. Australian supplement maker Blackmores used WeChat-centric monitoring to spot rising consumer concerns and recast messaging, contributing to share gains in China. The ROI narrative accelerates adoption among e-commerce brands mindful of razor-thin margins.

Fragmented Data-Privacy Regimes

Divergent privacy statutes force vendors to juggle opt-outs, deletion rights, and data-residency mandates that vary by region. The California Consumer Privacy Act exemplifies the operational burden, requiring granular consumer controls and unique workflows for sensitive information. Smaller suppliers struggle to fund continuous rule updates, accelerating consolidation as compliance costs escalate. Enterprise buyers often deploy separate regional instances, diluting the value of unified global dashboards and dampening ROI expectations.

Other drivers and restraints analyzed in the detailed report include:

- Shift of TV Ad Spend to Social Video in Europe Raises SOV Analytics Demand

- Regulatory Response-Time Mandates for BFSI Complaints

- Multilingual AI Accuracy Gaps for Low-Resource Languages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for a 67.20% share of the social media listening market in 2025, cementing its role as the backbone of enterprise social intelligence stacks. Buyers prefer integrated suites that merge listening, engagement, and analytics so that insights flow directly into campaign orchestration tools. Platform vendors respond by embedding API layers that connect to customer data platforms and BI warehouses, supporting broader digital-experience strategies. The bundling trend protects license revenue even as basic monitoring commoditizes.

Services revenue, though smaller, is advancing at 16.02% CAGR because firms increasingly view social intelligence as an outcome-driven function rather than a plug-and-play toolset. Providers now offer crisis simulations, competitive war-rooms, and bespoke LLM fine-tuning that map to sector-specific jargon. Managed services resonate with mid-market brands lacking 24/7 coverage, while AI-tuning engagements carve a niche among regulated sectors that need domain-safe models. The dual-track growth keeps both pure-play and hybrid vendors relevant in the social media listening market.

Large enterprises commanded 64.10% of 2025 spending because they integrate listening outputs into data-lake architectures that span CRM, product, and compliance systems. Multi-brand conglomerates rely on dashboards that surface sentiment spikes per region, enabling coordinated rebuttal or campaign amplification. Enterprise buying cycles also drive consolidation as CIOs favor vendors offering contractual simplicity and ISO-certified security frameworks.

SMEs, however, represent the fastest-growing cohort with a projected 15.35% CAGR. Cloud pricing tiers, template-based onboarding, and conversational UI lower entry barriers. OECD research shows that 39% of SMEs used AI tools in 2025, up from 26% in 2024, mirroring broader digital acceleration. Small exporters pairing listening with social "talking" tactics report sharper customer gains, validating investment. Vendors target this segment with bundled freemium offerings that graduate to paid tiers once analytic depth and multiseat access become essential.

The Social Media Listening Market Report is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Analytics Type (Text Analytics, Image Analytics, and More), Application (Brand Health Tracking, Crisis Management, and More), Industry Vertical (Retail and E-Commerce, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 41.20% revenue lead in 2025, supported by technology maturity and stringent brand-protection postures following recent crises. Financial-services and healthcare firms integrate social data into regulated complaint systems to comply with statutes like the California Consumer Privacy Act, which grants consumers sweeping data rights. Ongoing investment focuses on high-precision risk detection modules that shield brand equity before posts trend.

Asia-Pacific is forecast to grow at 16.02% CAGR to 2031, propelled by soaring platform penetration and the dominance of mobile commerce. China's walled-garden networks oblige vendors to fine-tune language models and API connectors; brands that master this complexity, such as Blackmores on WeChat, unlock rapid share gains. India's rise combines smartphone affordability with regional-language social networks that demand multilingual coverage. Southeast Asian markets present high engagement but require dialect-adaptive NLP, keeping service partners busy.

Europe balances opportunity with heavy GDPR compliance overhead, spurring innovation in privacy-preserving analytics. The pivot of media budgets toward social video intensifies demand for multimodal share-of-voice dashboards. Latin America, the Middle East, and Africa are smaller yet dynamic, with growth centered in urban hubs and among multinationals that need regional sentiment gauges. Gulf governments increasingly adopt listening to track public opinion on service quality, expanding public-sector demand in the social media listening market.

- Meltwater

- Sprinklr

- Brandwatch (Cision LLC)

- NetBase Quid

- Talkwalker

- Digimind

- Khoros

- Clarabridge (Qualtrics)

- Mention

- Hootsuite Inc.

- Agorapulse

- Awario

- Zignal Labs

- ListenFirst

- Synthesio (Ipsos)

- Reputology

- Linkfluence

- Socialbakers (Astute)

- Keyhole Inc.

- Brand24

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brand-risk mitigation amid influencer-led crises (North America)

- 4.2.2 Generative-AI sentiment classification boosting APAC retail ROI

- 4.2.3 Shift of TV ad spend to social video in Europe raises SOV analytics demand

- 4.2.4 Regulatory response-time mandates for BFSI complaints

- 4.2.5 Gaming and livestreaming surge generating rich video/audio data sets

- 4.2.6 Open-API martech ecosystems driving platform consolidation

- 4.3 Market Restraints

- 4.3.1 Fragmented data-privacy regimes (GDPR, CCPA, PDPA)

- 4.3.2 Multilingual AI accuracy gaps for low-resource languages

- 4.3.3 API access fee hikes from X (Twitter) and Meta

- 4.3.4 Overlap with in-house BI/CDP causing procurement fatigue

- 4.4 Technological Outlook

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises (SMEs)

- 5.3 By Analytics Type

- 5.3.1 Text Analytics

- 5.3.2 Image Analytics

- 5.3.3 Video Analytics

- 5.3.4 Voice/Audio Analytics

- 5.4 By Application

- 5.4.1 Brand Health Tracking

- 5.4.2 Customer Experience Management

- 5.4.3 Competitive Benchmarking

- 5.4.4 Lead Generation and Sales Monitoring

- 5.4.5 Campaign Management

- 5.4.6 Crisis Management

- 5.5 By Industry Vertical

- 5.5.1 Retail and E-commerce

- 5.5.2 BFSI

- 5.5.3 IT and Telecom

- 5.5.4 Media and Entertainment

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Travel and Hospitality

- 5.5.7 Education

- 5.5.8 Others (Government, NGOs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Australia and New Zealand

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC Countries

- 5.6.5.2 Turkey

- 5.6.5.3 Israel

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Meltwater

- 6.4.2 Sprinklr

- 6.4.3 Brandwatch (Cision LLC)

- 6.4.4 NetBase Quid

- 6.4.5 Talkwalker

- 6.4.6 Digimind

- 6.4.7 Khoros

- 6.4.8 Clarabridge (Qualtrics)

- 6.4.9 Mention

- 6.4.10 Hootsuite Inc.

- 6.4.11 Agorapulse

- 6.4.12 Awario

- 6.4.13 Zignal Labs

- 6.4.14 ListenFirst

- 6.4.15 Synthesio (Ipsos)

- 6.4.16 Reputology

- 6.4.17 Linkfluence

- 6.4.18 Socialbakers (Astute)

- 6.4.19 Keyhole Inc.

- 6.4.20 Brand24

- 6.5 Vendor Positioning Matrix

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment