|

市場調查報告書

商品編碼

1940773

遠端儲槽監控系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Remote Tank Monitoring System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

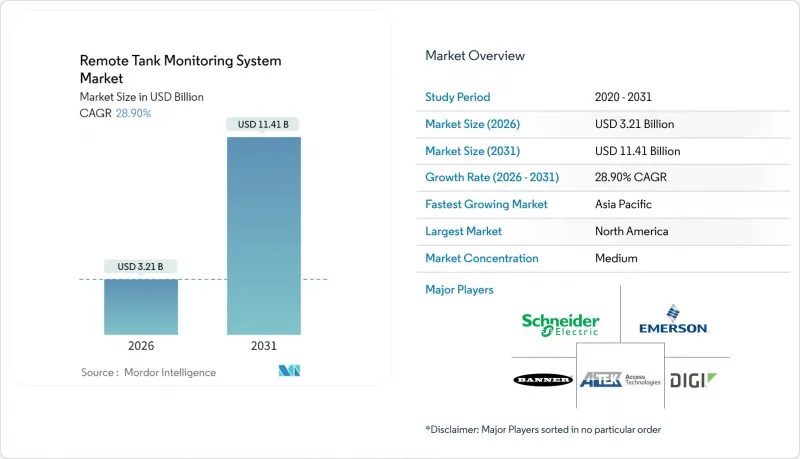

預計遠端儲槽監控系統市場將從 2025 年的 24.9 億美元成長到 2026 年的 32.1 億美元,到 2031 年將達到 114.1 億美元,2026 年至 2031 年的複合年成長率為 28.9%。

強勁成長反映了工業IoT的日益普及、衛星和低功耗廣域網路(LPWAN)連接技術的日益成熟,以及日益嚴格的環境法規要求對液體儲存進行持續監控。產業相關人員正從被動式資產管理轉向預測式資產管理,由此帶來的效率提升、更少的車輛出勤、更嚴格的庫存管理以及更快的洩漏檢測,正吸引著資產所有者和保險公司採用自動化遙測技術。如今,競爭優勢主要體現在能夠將感測器數據轉化為可執行洞察的軟體分析技術上,而基於訂閱的硬體即服務(HaaS)模式正在降低初始成本門檻,並加速遠端儲罐監控系統解決方案的普及。

全球遠端儲罐監控系統市場趨勢與洞察

擴大石油、天然氣和化學品儲存基礎設施

根據國際能源總署(IEA)的數據,到2024年,全球油氣儲存能力預計將成長12%,因為各公司正在為實現能源轉型目標而建立策略儲備。化學企業也在採取類似措施以應對原料價格波動,這兩種趨勢都推動了遠端儲罐監控系統市場的需求。營運商傾向於擴充性的多站點平台,這些平台能夠與現有的SCADA系統整合,並將資料傳輸到雲端進行分析,從而實現全系統最佳化。能夠整合衛星通訊鏈路和蜂窩回程傳輸的供應商,目前正贏得資本密集型計劃的多年期框架合約。

基於雲端的物聯網平台的普及

預計到 2024 年,微軟 Azure IoT 和 AWS IoT Core 在工業應用情境中的年成長率將達到 40%,其中儲槽遙測將成為成長最快的新增工作負載之一。雲端技術的應用使得基於機器學習的洩漏偵測、自動補給觸發和預測性維護等功能成為可能,而這些功能在傳統的 SCADA 系統中幾乎無法實現。中型企業正在利用訂閱定價模式來避免大規模支出 (CAPEX),這進一步加速了遠端儲罐監控系統解決方案的普及。

高昂的初始硬體和整合成本

從感測器到雲端的完整部署,每個儲罐的成本可能在 15,000 美元到 45,000 美元之間,而且整合成本通常超過硬體成本。管理儲罐數量較少的小型企業很難證明如此高昂的支出是合理的。這種限制正推動遠端儲罐監控系統市場向模組化套件和硬體即服務 (HaaS) 訂閱模式發展,將成本從資本支出 (CAPEX) 轉移到營運支出 (OPEX),使用戶能夠在投資回報率顯現時進行擴展。

細分市場分析

2025年,具備低成本和簡單二進位警報功能的點位式液位計佔據市場主導地位,市佔率高達57.92%。同時,連續式液位計平台正贏得許多高價值計劃,以29.6%的複合年成長率成長,反映出監管審核和即時物流對持續可視性的要求日益成長。預計2025年至2030年間,連續式液位計安裝相關的收入將為遠端儲槽監控系統市場規模增加40億美元。

在製藥和精細化工行業,高解析度雷達和導波雷達探頭的投入正在增加,因為±1毫米的精度有助於提高產品品質。點式液位計系統仍然是丙烷和小型工業儲罐的標配,但隨著浮球開關逐漸被淘汰,原始設備製造商(OEM)正在將雲端控制面板作為標準配置,從而推動了數位式桿式液位計的普及。

到2025年,接觸式感測技術將佔總收入的61.55%,而非接觸式感測技術預計將超越其他類別,這主要得益於超音波和FMCW雷達等避免流體接觸的技術。非接觸式技術的快速成長將推高平均售價,而先進的訊號處理軟體將為供應商提供新的利潤成長途徑。遠端儲槽監控系統的安裝商也指出,由於沒有接觸流體的零件,維護成本降低,現場來訪頻率減少,這些優勢進一步提升了物聯網在農村資產中的價值。

光學和雷射設備在無菌藥品批量處理等高價值應用中佔據主導地位,而機械帶形水尺仍然用於視覺冗餘對於遵守衛生法規至關重要的領域,儘管數位改造套件正朝著將捲尺浮子測量數據傳輸到 SCADA 的方向發展,從而減少了人工浸入檢查。

區域分析

截至2025年,北美仍將維持領先地位,市佔率達34.05%,推動要素SPCC法規的實施、廣泛的油氣基礎設施以及工業IoT的早期應用。聯邦政府對農村寬頻的津貼正在推動低功耗廣域網路(LPWAN)的擴展,進一步加速農業省份遠端油罐監控系統的普及。加拿大計劃擴大戰略石油儲備,並整合各業者的資產管理平台,這正在形成跨境發展動能。

預計亞太地區將實現最快成長,到2031年複合年成長率將達到33.1%。即時儲槽遙測技術對於中國和印度的大規模煉油廠和石化廠擴建計畫以及東南亞的採礦計劃而言,對於安全措施和環境、社會及治理(ESG)報告都至關重要。區域各國政府也正在實施符合經合組織標準的土壤和水資源保護條例,要求地下儲槽所有者實施持續監測。

在歐洲,嚴格的環境指令和工業脫碳計畫正在支撐著經濟的穩定成長。一款用於計算散裝液體物流中範圍3排放的雲端儀錶板正受到歐洲大型企業的熱烈歡迎,這些企業的目標是在2030年實現碳中和。同時,在中東、非洲和南美洲,液化天然氣、海水淡化和採礦等基礎設施投資正在推動新計畫的開展,從而提升遠端儲罐監控系統的市場潛力。然而,短期內經濟逆風預計將抑制需求成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大石油、天然氣和化學品儲存基礎設施

- 基於雲端的物聯網平台的興起

- 加強全球資金外流預防和庫存控制

- 衛星物聯網技術為偏遠地區的油罐提供覆蓋

- HaaS訂閱模式降低了資本投資門檻

- 範圍 3 ESG 報告給散裝液體供應鏈帶來壓力

- 市場限制

- 高昂的初始硬體和整合成本

- 網路安全和資料所有權問題

- 鋼鋁關稅增加設備物料清單成本

- 負責任的電池廢棄物永續性

- 價值鏈分析

- 監管環境

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 影響市場的宏觀經濟因素

第5章 市場規模與成長預測

- 透過監測類型

- 點級監測

- 連續液位監測

- 透過技術

- 接觸式感應器

- 浮子式和捲尺式壓力表

- 磁致伸縮

- 靜水壓力

- 非接觸式感測器

- 超音波

- 雷達/調頻連續波

- 光學/雷射

- 接觸式感應器

- 連結性別

- 蜂窩通訊(4G LTE、5G、NB-IoT、Cat-M)

- LPWAN(LoRaWAN、Sigfox)

- 衛星(低軌道/地球同步軌道)

- 短距離無線/Wi-Fi/BLE

- 按油箱類型

- 地面固定屋頂

- 地面式浮動頂

- 地下/UST

- 按產能

- 不足10,000公升

- 10,000-50,000 L

- 50,001-200,000 L

- 超過20萬公升

- 按最終用戶行業分類

- 石油和天然氣

- 化學品和石油化工

- 供水/污水處理

- 食品/飲料

- 農業與灌溉

- 發電

- 採礦和金屬

- 製藥和醫療保健

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric SE

- Emerson Electric Co.

- Banner Engineering Corp.

- ATEK Access Technologies, LLC(TankScan)

- Anova(DataOnline Corp.)

- Digi International Inc.

- Otodata Wireless Network Inc.

- SkyBitz Inc.

- Powelectrics Ltd.

- Dunraven Systems Limited

- Endress+Hauser Group

- Honeywell International Inc.

- Vega Grieshaber KG

- RemoteTank(Alpha Wireless Automation, Inc.)

- Rugged Telemetry

- Tekelek Group

- Tank Utility, Inc.(Generac Power Systems, Inc.)

- Cavagna Group

- Angus Energy LLC

- Mistras Group, Inc.

第7章 市場機會與未來展望

The Remote Tank Monitoring System market is expected to grow from USD 2.49 billion in 2025 to USD 3.21 billion in 2026 and is forecast to reach USD 11.41 billion by 2031 at 28.9% CAGR over 2026-2031.

Solid growth reflects the widening adoption of industrial IoT, the maturation of satellite and LPWAN connectivity, and tighter environmental regulations that require continuous visibility into liquid storage. Sector participants are shifting from reactive maintenance to predictive asset management, and the resulting efficiency gains, lower truck rolls, tighter inventory control, and faster spill detection continue to draw both asset owners and insurers toward automated telemetry. Competitive differentiation now centers on software analytics that convert sensor data into actionable insights, while subscription-based Hardware-as-a-Service (HaaS) models reduce upfront cost barriers and accelerate the adoption of remote tank monitoring system solutions.

Global Remote Tank Monitoring System Market Trends and Insights

Expansion of Oil and Gas and Chemical Storage Infrastructure

IEA data showed global oil and gas storage capacity increasing by 12% in 2024 as firms built strategic reserves while pursuing energy transition goals . Chemical producers mirrored this pattern to buffer feedstock volatility, and both trends amplified demand for remote tank monitoring system market deployments. Operators favor scalable, multi-site platforms that integrate with existing SCADA systems and feed cloud analytics for portfolio-wide optimization. Vendors able to integrate satellite links and cellular backhaul now win multi-year frame agreements on heavy-capital projects.

Proliferation of Cloud-Based IoT Platforms

Microsoft Azure IoT and AWS IoT Core logged a 40% annual growth in industrial use cases by 2024, with tank telemetry among the fastest-growing add-on workloads. Cloud ingestion unlocks machine-learning leak detection, automated replenishment triggers, and predictive maintenance capabilities that were previously seldom possible in legacy SCADA systems. Mid-market operators tap subscription pricing to sidestep large CAPEX, further accelerating the uptake of remote tank monitoring system market solutions.

High Upfront Hardware and Integration Costs

A full sensor-to-cloud deployment can run USD 15,000-45,000 per tank, with integration often exceeding the hardware bill. SMEs managing a handful of tanks struggle to justify such spend. This restraint steers the remote tank monitoring system market toward modular kits and HaaS subscriptions, which shift costs from CAPEX to OPEX, allowing users to scale as ROI becomes evident.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global Spill-Prevention and Inventory Regulations

- Satellite-IoT Coverage for Ultra-Remote Tanks

- Cyber-Security and Data-Ownership Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Point-level devices led the 2025 field with a 57.92% share, aided by low cost and simple binary alarms. Continuous-level platforms captured higher-value projects, and their 29.6% CAGR signals a shift toward always-on visibility, as demanded by regulatory audits and just-in-time logistics. Revenue linked to continuous installations is set to add USD 4 billion to the remote tank monitoring system market size between 2025 and 2030.

Spending is tilting toward high-resolution radar and guided-wave radar probes in pharmaceuticals and fine chemicals, where +-1 mm accuracy yields quality dividends. Point-level remains entrenched in propane and small industrial tanks, yet aging float switches increasingly give way to digital stick probes as OEMs bundle cloud dashboards by default.

Contact technologies delivered 61.55% of 2025 sales, but non-contact sensing is expected to outpace all other categories, driven by ultrasonic and FMCW radar that avoid fluid contact. The non-contact boom lifts' average selling prices and advanced signal processing software make it a new margin lever for vendors. Remote tank monitoring system adopters also cite lower maintenance costs, no wetted parts means fewer field visits, which compounds the IoT value in rural assets.

Optical and laser devices occupy premium niches such as sterile pharmaceutical batching. Meanwhile, mechanical tape gauges persist where visual redundancy is mandatory for insurance compliance, although digital retrofit kits now stream tape-float readings into SCADA to reduce manual dip checks.

The Remote Tank Monitoring System Market Report is Segmented by Monitoring Type (Point-Level, Continuous-Level), Technology (Contact Sensors, Non-Contact Sensors), Connectivity (Cellular, LPWAN, and More), Tank Type (Above-Ground Fixed-Roof, and More), Capacity (<10, 000 L, 10, 000 - 50, 000 L, and More), End-User Industry (Oil and Gas, Chemicals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained a 34.05% lead in 2025, driven by SPCC enforcement, extensive oil and gas infrastructure, and early industrial IoT adoption. Federal grants for rural broadband enhance LPWAN coverage, further propelling the deployment of remote tank monitoring systems in agricultural states. Canada's renewed strategic petroleum reserve buildout adds cross-border momentum as operators harmonize asset management platforms.

The Asia-Pacific region is expected to deliver the most rapid growth, with a 33.1% CAGR through 2031. Massive refinery and petrochemical expansions in China and India, alongside Southeast Asian mining projects, require real-time tank telemetry for both safety and ESG reporting purposes. Regional governments also roll out soil-and-water-protection rules mirroring OECD standards, compelling underground tank owners to adopt continuous monitoring.

Stringent environmental directives and industrial decarbonization programs underpin Europe's steady growth. Cloud dashboards that calculate Scope 3 emissions from bulk-liquid logistics are finding eager users among European majors seeking to meet their 2030 carbon-neutral targets. In parallel, the Middle East, Africa, and South America show rising potential for the remote tank monitoring system market as infrastructure investments in LNG, desalination, and mining unlock greenfield projects, although economic headwinds temper near-term volumes.

- Schneider Electric SE

- Emerson Electric Co.

- Banner Engineering Corp.

- ATEK Access Technologies, LLC (TankScan)

- Anova (DataOnline Corp.)

- Digi International Inc.

- Otodata Wireless Network Inc.

- SkyBitz Inc.

- Powelectrics Ltd.

- Dunraven Systems Limited

- Endress+Hauser Group

- Honeywell International Inc.

- Vega Grieshaber KG

- RemoteTank (Alpha Wireless Automation, Inc.)

- Rugged Telemetry

- Tekelek Group

- Tank Utility, Inc. (Generac Power Systems, Inc.)

- Cavagna Group

- Angus Energy LLC

- Mistras Group, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of oil and gas and chemical storage infrastructure

- 4.2.2 Proliferation of cloud-based IoT platforms

- 4.2.3 Stricter global spill-prevention and inventory regulations

- 4.2.4 Satellite-IoT coverage for ultra-remote tanks

- 4.2.5 HaaS subscription models lowering capex barriers

- 4.2.6 Scope-3 ESG reporting pressure on bulk-liquid supply chains

- 4.3 Market Restraints

- 4.3.1 High upfront hardware and integration costs

- 4.3.2 Cyber-security and data-ownership concerns

- 4.3.3 Steel/aluminum tariffs inflating device BOM

- 4.3.4 Battery-waste sustainability liabilities

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Monitoring Type

- 5.1.1 Point-Level Monitoring

- 5.1.2 Continuous-Level Monitoring

- 5.2 By Technology

- 5.2.1 Contact Sensors

- 5.2.1.1 Float and Tape Gauge

- 5.2.1.2 Magnetostrictive

- 5.2.1.3 Hydrostatic Pressure

- 5.2.2 Non-Contact Sensors

- 5.2.2.1 Ultrasonic

- 5.2.2.2 Radar/FMCW

- 5.2.2.3 Optical/Laser

- 5.2.1 Contact Sensors

- 5.3 By Connectivity

- 5.3.1 Cellular (4G LTE, 5G, NB-IoT, Cat-M)

- 5.3.2 LPWAN (LoRaWAN, Sigfox)

- 5.3.3 Satellite (LEO/GEO)

- 5.3.4 Short-Range RF/Wi-Fi/BLE

- 5.4 By Tank Type

- 5.4.1 Above-Ground Fixed-Roof

- 5.4.2 Above-Ground Floating-Roof

- 5.4.3 Underground/UST

- 5.5 By Capacity

- 5.5.1 <10,000 L

- 5.5.2 10,000 - 50,000 L

- 5.5.3 50,001 - 200,000 L

- 5.5.4 >200,000 L

- 5.6 By End-User Industry

- 5.6.1 Oil and Gas

- 5.6.2 Chemicals and Petrochemicals

- 5.6.3 Water and Wastewater

- 5.6.4 Food and Beverage

- 5.6.5 Agriculture and Irrigation

- 5.6.6 Power Generation

- 5.6.7 Mining and Metals

- 5.6.8 Pharmaceuticals and Healthcare

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Southeast Asia

- 5.7.4.7 Rest of Asia Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Kenya

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Emerson Electric Co.

- 6.4.3 Banner Engineering Corp.

- 6.4.4 ATEK Access Technologies, LLC (TankScan)

- 6.4.5 Anova (DataOnline Corp.)

- 6.4.6 Digi International Inc.

- 6.4.7 Otodata Wireless Network Inc.

- 6.4.8 SkyBitz Inc.

- 6.4.9 Powelectrics Ltd.

- 6.4.10 Dunraven Systems Limited

- 6.4.11 Endress+Hauser Group

- 6.4.12 Honeywell International Inc.

- 6.4.13 Vega Grieshaber KG

- 6.4.14 RemoteTank (Alpha Wireless Automation, Inc.)

- 6.4.15 Rugged Telemetry

- 6.4.16 Tekelek Group

- 6.4.17 Tank Utility, Inc. (Generac Power Systems, Inc.)

- 6.4.18 Cavagna Group

- 6.4.19 Angus Energy LLC

- 6.4.20 Mistras Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

燃料箱船服務市場-全球產業規模、佔有率、趨勢、機會、預測:按材料類型、容量、燃料類型、營運商、地區和競爭格局分類,2021-2031年

燃料箱船服務市場-全球產業規模、佔有率、趨勢、機會、預測:按材料類型、容量、燃料類型、營運商、地區和競爭格局分類,2021-2031年 燃料箱市場:2026-2032年全球市場預測(依材料、燃料類型、容量、應用及通路分類)

燃料箱市場:2026-2032年全球市場預測(依材料、燃料類型、容量、應用及通路分類) 摩托車燃料箱市場報告:按容量、應用和地區分類(2026-2034 年)

摩托車燃料箱市場報告:按容量、應用和地區分類(2026-2034 年) 2026年全球折疊式燃料箱市場報告2026年全球罐車市場報告汽車用液氫市場:2026-2032年全球市場預測(按氫形態、儲存技術、加氫基礎設施、車輛類型、應用和最終用戶分類)

2026年全球折疊式燃料箱市場報告2026年全球罐車市場報告汽車用液氫市場:2026-2032年全球市場預測(按氫形態、儲存技術、加氫基礎設施、車輛類型、應用和最終用戶分類) 全球國防外掛油箱市場:2026-2036LNG駁船加註系統市場按組件、安裝類型、推進類型、駁船類型、應用和最終用戶分類,全球預測(2026-2032年)

全球國防外掛油箱市場:2026-2036LNG駁船加註系統市場按組件、安裝類型、推進類型、駁船類型、應用和最終用戶分類,全球預測(2026-2032年) 自供電水質監測系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類卡車加油系統市場按組件、燃料類型、技術、支付方式、最終用途和車輛類型分類-全球預測(2026-2032 年)

自供電水質監測系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類卡車加油系統市場按組件、燃料類型、技術、支付方式、最終用途和車輛類型分類-全球預測(2026-2032 年)