|

市場調查報告書

商品編碼

1940715

越南紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

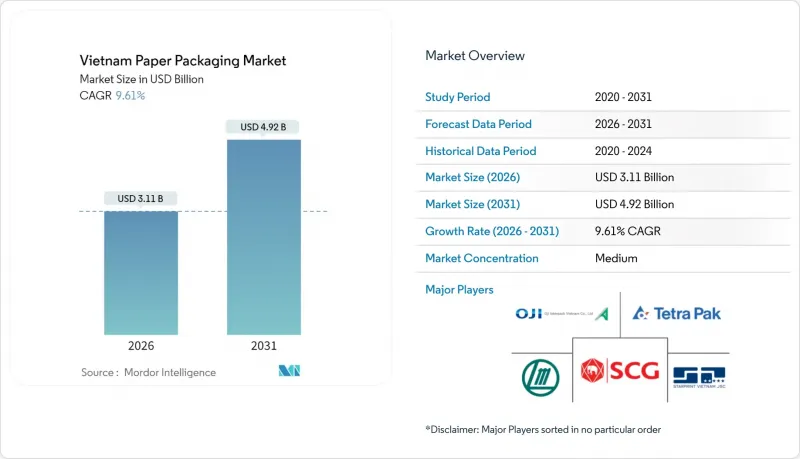

越南紙包裝市場在 2025 年的價值為 28.4 億美元,預計到 2031 年將達到 49.2 億美元,高於 2026 年的 31.1 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 9.61%。

這一成長幅度遠超全球平均水平,凸顯了越南在東南亞不斷演變的供應鏈結構中的戰略地位。中產階級消費的成長、強勁的外國直接投資以及諸如生產者延伸責任制(EPR)等監管激勵措施,都在推動對紙質包裝的需求。電子商務小包裹量的快速成長、消費品和電子產品生產的轉移以及品牌所有者的碳減排承諾,共同促進了越南紙質包裝市場的發展。同時,原生紙漿短缺和廢紙進口法規的波動造成了供應摩擦,價格和產能擴張仍然是關注的焦點。

越南紙包裝市場趨勢與洞察

電子商務小包裹量快速成長

2024年,越南國內電子商務銷售額達到兩位數成長,帶動了胡志明市、河內和峴港等城市的小包裹配送量激增。這一成長帶動了對專為應對多式聯運物流鏈而設計的瓦楞紙箱的需求。省會城市的微型倉配中心正在調整訂單包裝,採用較小尺寸的紙箱,以便放入小包裹櫃和兩輪式配送架。越南政府第221/QD-TTg號決定旨在使物流對GDP的貢獻率達到9%至11%,鼓勵自動化升級,而這需要標準化的包裝尺寸以實現高速分揀。計劃在2030年投資50億美元用於智慧物流基礎設施建設,為近期物流量的成長提供了清晰的預期。此次小包裹熱潮正迅速提振越南的紙質包裝市場。

消費品和電子產品快速境外外包至越南

2025年新增外商直接投資的66%以上將流入加工製造業,刺激南北工業區工廠對運輸紙箱的需求。以河南省一家投資9,000萬美元的工廠為首的休閒食品製造商,在優先考慮100%永續採購目標的同時,也推動了對箱板紙的穩定需求。從中國遷至越南的電子組裝製造商,指定使用符合全球品質標準的防靜電襯紙、防潮層和白面牛皮紙襯紙。跨國公司的在地化要求正在推動越南國內紙板生產,以減少進口依賴和範圍3排放。因此,越南紙包裝市場受益於與外國公司工廠運作計畫相關的長期訂單。

國內原生紙漿結構性短缺及對進口的依賴

由於缺乏大型永續種植園,越南造紙廠無法滿足不斷成長的牛皮紙需求。 2023年初,儘管進口量較上季成長9.2%,但包裝紙總消費量仍達284,530噸,這一缺口凸顯出來。外匯波動和運費成本會直接反映在箱板紙價格上,影響加工業者的利潤率。依賴長纖維的高檔箱板紙經常出現短缺,迫使用戶縮減生產規模或支付額外費用。因此,纖維短缺是限制越南紙包裝市場發展的結構性因素。

細分市場分析

截至2025年,箱板紙將佔越南紙包裝市場57.18%的佔有率。這反映了越南以出口為導向的經濟結構,其全球運輸需要堅固耐用的瓦楞紙板。白面牛皮紙在電子產業叢集中佔據了較高的價格地位,而再生瓦楞紙則滿足了國內食品飲料物流的需求。兼具成本優勢和強度的半化學加工瓦楞紙正吸引買家的目光。儘管紙板的規模仍然較小,但在藥品標籤和零售展示需求不斷成長的推動下,預計到2031年將實現11.13%的複合年成長率。普通漂白硫酸鹽紙漿紙板和折疊紙板為跨國快速消費品公司提供了實現品牌差異化所需的高品質表面。隨著環保標籤成為採購標準,對塗佈和非塗佈再生紙板的需求也不斷成長。利樂公司擴大產能後,已將其55%的產量分配給了本地買家,這表明該公司對高階紙盒的需求充滿信心。

隨著工業園區倉庫建設的推進,越南紙包裝市場中的箱板紙部分預計將穩步擴張,而紙板市場規模預計將受益於有利於輕型、高再生材料含量產品的監管壓力,這使得市場定位從通用襯紙轉向專為特定最終用途和小批量印刷而設計的高附加值紙板。

2025年,受電子商務和出口貨運量成長的主導,瓦楞紙箱和貨櫃將佔越南紙包裝市場50.12%的佔有率。大型貨運公司需要B型和C型瓦楞紙箱進行海運,這兩種紙箱兼具抗壓性和裝載效率。 2030年,越南將投資50億美元建造智慧物流基礎設施,以確保瓦楞紙箱的持續供應。同時,隨著醫療保健和個人護理品牌尋求防篡改和商店展示解決方案,折疊紙盒的複合年成長率將達到10.96%。數位印刷補貼鼓勵紙盒客製化,並支撐其高階定價。

在纖維供應穩定之前,薄瓦楞紙板的市場機會將十分有限。為此,紙盒採用輕質塗佈紙基材,以最大限度地減少材料用量,並符合範圍3的排放目標。模塑紙漿嵌件整合到折疊紙盒中,進一步提升了產品的差異化優勢。越南的紙包裝市場正從散裝運輸向兼具結構保護和銷售點吸引力的混合型SKU不斷演變。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務小包裹數量快速成長

- 消費品和電子產品快速境外外包至越南

- 塑膠淘汰條例

- 國際品牌所有者的範圍 3 碳減排推動了輕質再生紙板的開發

- 區域城市中社交電商和微型倉配的興起

- 高速數位印刷生產線的稅收優惠投資

- 市場限制

- 國內原生紙漿原料結構性短缺;高度依賴進口

- 改變廢紙進口政策和品管

- 美國和歐盟針對木材產品的貿易措施收緊了紙漿材料的供應。

- 工業用電價格上漲對中小瓦楞紙箱製造商帶來壓力

- 產業供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按年級

- 紙板

- 固態漂白硫酸鹽紙漿(SBS)

- 未漂白硫酸鹽紙漿(SUS)

- 折疊紙盒(FBB)

- 塗佈再生紙板(CRB)

- 未塗佈再生紙板(URB)

- 其他等級的紙板

- 貨櫃紙板

- 白色牛皮紙襯墊

- 其他牛皮紙

- 白色頂部測試襯墊

- 其他測試襯墊

- 半化學合成長笛

- 再生公寓

- 其他年級

- 紙板

- 依產品

- 可折疊瓦楞紙箱

- 瓦楞紙箱和容器

- 其他產品

- 按最終用戶行業分類

- 食物

- 飲料

- 衛生保健

- 個人護理

- 家居用品

- 電氣和電子設備

- 其他終端用戶產業

- 按包裝類型

- 硬紙板(紙板、厚紙)

- 半硬質(可折疊紙箱,不包括硬紙板箱)

- 軟性紙製品(小袋、包裝紙)

- 模塑纖維和紙漿包裝產品

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SONG LAM Trading & Packaging Production CO., Ltd

- Asia Pulp & Paper Group(APP)

- Tetra Pak International SA

- Oji Interpack Vietnam Co., Ltd

- Khang Thanh Manufacturing CO., LTD

- Hanh Packaging Co. Ltd

- SCG Paper Public Company Limited

- BINH MINH PAT CO.,LTD

- Kraft of Asia Paperboard & Packaging Co., Ltd..

- HC Packaging Vietnam Company Limited

- Starprint Vietnam Joint Stock Company

- Nippon Paper Industries Co., Ltd.

- Box-Pak(Malaysia)Bhd.

- Lee & Man Paper Manufacturing Ltd.

- Sai Gon Paper Corporation

- Dong Hai Ben Tre Joint Stock Company

- Nine Dragons Paper(Holdings)Limited

- Rengo Co., Ltd

第7章 市場機會與未來展望

The Vietnam paper packaging market was valued at USD 2.84 billion in 2025 and estimated to grow from USD 3.11 billion in 2026 to reach USD 4.92 billion by 2031, at a CAGR of 9.61% during the forecast period (2026-2031).

This expansion significantly outpaces the global average, underscoring Vietnam's strategic role in Southeast Asia's evolving supply chain framework. Rising middle-class consumption, robust foreign direct investment, and regulatory incentives such as extended producer responsibility requirements are accelerating demand for paper-based formats. The surge in e-commerce parcel volumes, the relocation of fast-moving consumer goods and electronics production, and brand-owner carbon-cut commitments all converge to bolster the Vietnam paper packaging market.Meanwhile, virgin-fiber shortages and volatile recovered-paper import rules create supply-side friction that keeps prices and capacity expansion in sharp focus.

Vietnam Paper Packaging Market Trends and Insights

Booming e-commerce parcel volumes

National e-commerce turnover rose at a double-digit pace in 2024, driving aggregate parcel flows across Ho Chi Minh City, Hanoi, and Da Nang. The uptick amplifies demand for corrugated shipping containers engineered to survive multimodal logistics chains. Micro-fulfillment centers in tier-2 cities are shifting order profiles toward smaller-format boxes that fit parcel lockers and two-wheeler delivery racks. Vietnam's Decision 221/QD-TTg targets a 9%-11% logistics GDP contribution, prompting automation upgrades that require standardized packaging dimensions for high-speed sortation. Capital spending of USD 5 billion earmarked for smart-logistics infrastructure through 2030 cements near-term volume visibility. The Vietnam paper packaging market gains immediate tailwinds from this parcel boom.

Rapid FMCG and electronics off-shoring into Vietnam

Over 66% of 2025's fresh FDI pledges flowed into processing and manufacturing, catalyzing plant-level demand for transport-worthy cartons in Northern and Southern industrial belts. Snack-food producers, exemplified by the USD 90 million Ha Nam facility, anchor steady containerboard pull-through while prioritizing 100% sustainable sourcing goals. Electronics assemblers relocating from China specify anti-static liners, moisture barriers, and white-top kraftliners that meet global quality codes. Localization mandates by multinational corporations promote in-country board production to cut import reliance and Scope-3 emissions. As a result, the Vietnam paper packaging market secures long-run orders tied to foreign plant commissioning schedules.

Structural shortfall of domestic virgin fiber; import dependence

Vietnam's mills cannot meet surging kraftliner demand because the country lacks large-scale, sustainable forestry plantations. In early 2023, total packaging-paper consumption hit 284,530 tons even as imports rose 9.2% month-on-month, underscoring the gap. Currency swings and freight costs translate quickly into linerboard prices, affecting converter margins. Premium grades that rely on long fiber face periodic shortages, forcing users to down-spec or pay surcharges. The fiber deficit, therefore, acts as a structural drag on the Vietnam paper packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Plastic phase-out regulations (EPR and DRS)

- Foreign brand owners' Scope-3 carbon cuts push lightweight recycled board

- Volatile recovered-paper import policy and quality controls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Containerboard held 57.18% of the Vietnam paper packaging market share in 2025, a reflection of Vietnam's export-oriented profile that relies on robust corrugating medium for global shipping. White-top kraftliner commands premium pricing in electronics clusters, whereas recycled fluting satisfies domestic food-and-beverage logistics. Semi-chemical fluting attracts buyers, balancing cost and strength. Cartonboard, although smaller, records an 11.13% CAGR to 2031, propelled by rising pharmaceutical labeling needs and retail-ready displays. Solid bleached sulfate and folding boxboard deliver high-graphics surfaces essential for brand differentiation among multinational FMCG firms. Coated recycled board and uncoated recycled board gain traction as eco-labels become purchasing criteria. Tetra Pak's capacity boost dedicates 55% output to local buyers, signaling confidence in premium carton uptake.

The Vietnam paper packaging market size for containerboard is projected to rise steadily alongside warehouse construction in industrial parks. Meanwhile, the Vietnam paper packaging market size for cartonboard stands to benefit from regulatory pressure favoring lightweight formats with higher recycled content. Market positioning is thus shifting from commodity liner toward value-added board engineered for specific end uses and shorter print runs.

Corrugated Boxes and Containers accounted for 50.12% of the Vietnam paper packaging market size in 2025, as e-commerce and export shipping dominated volume patterns. Large shippers require B- and C-flute cases that strike a balance between crush resistance and stacking efficiency for sea freight. The rollout of USD 5 billion in smart-logistics infrastructure through 2030 ensures continued corrugated throughput. Folding cartons, however, are expanding at an 10.96% CAGR as healthcare and personal-care brands seek tamper-evident, shelf-ready solutions. Digital print subsidies accelerate carton customization, which supports premium pricing.

Down-gauge opportunities in corrugated remain limited until fiber supply stabilizes. In contrast, cartons utilize lightweight coated substrates to minimize material usage and align with Scope 3 emission targets. Molded pulp inserts integrated into folding-carton formats further differentiate offerings. The Vietnam paper packaging market is continuing to evolve from bulk shippers toward hybrid SKUs that combine structural protection with point-of-sale appeal.

The Vietnam Paper Packaging Market Report is Segmented by Grade (Cartonboard, and Containerboard), Product (Folding Cartons, Corrugated Boxes and Containers, and More), End-User Industry (Food, Beverage, Healthcare, Household Care, Electrical and Electronics, and More), Packaging Format (Rigid, Semi-Rigid, Molded Fiber and Pulp Packaging Products, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SONG LAM Trading & Packaging Production CO., Ltd

- Asia Pulp & Paper Group (APP)

- Tetra Pak International S.A.

- Oji Interpack Vietnam Co., Ltd

- Khang Thanh Manufacturing CO., LTD

- Hanh Packaging Co. Ltd

- SCG Paper Public Company Limited

- BINH MINH P.A.T CO.,LTD

- Kraft of Asia Paperboard & Packaging Co., Ltd..

- HC Packaging Vietnam Company Limited

- Starprint Vietnam Joint Stock Company

- Nippon Paper Industries Co., Ltd.

- Box-Pak (Malaysia) Bhd.

- Lee & Man Paper Manufacturing Ltd.

- Sai Gon Paper Corporation

- Dong Hai Ben Tre Joint Stock Company

- Nine Dragons Paper (Holdings) Limited

- Rengo Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming e-commerce parcel volumes

- 4.2.2 Rapid FMCG and electronics off-shoring into Vietnam

- 4.2.3 Plastic phase-out regulations

- 4.2.4 Foreign brand owners' Scope-3 carbon cuts push lightweight recycled board

- 4.2.5 Rise of social-commerce micro-fulfilment in tier-2 cities

- 4.2.6 Tax-incentivised investments in high-speed digital printing lines

- 4.3 Market Restraints

- 4.3.1 Structural shortfall of domestic virgin fibre; import dependence

- 4.3.2 Volatile recovered-paper import policy and quality controls

- 4.3.3 US/EU trade actions on wood products tighten pulpwood feedstock

- 4.3.4 Industrial power-tariff hikes squeeze SME corrugators

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade

- 5.1.1 Cartonboard

- 5.1.1.1 Solid Bleached Sulphate (SBS)

- 5.1.1.2 Solid Unbleached Sulphate (SUS)

- 5.1.1.3 Folding Boxboard (FBB)

- 5.1.1.4 Coated Recycled Board (CRB)

- 5.1.1.5 Uncoated Recycled Board (URB)

- 5.1.1.6 Other Cartonboard Grades

- 5.1.2 Containerboard

- 5.1.2.1 White-top Kraftliner

- 5.1.2.2 Other Kraftliners

- 5.1.2.3 White-top Testliner

- 5.1.2.4 Other Testliners

- 5.1.2.5 Semi-chemical Fluting

- 5.1.2.6 Recycled Fluting

- 5.1.3 Other Grades

- 5.1.1 Cartonboard

- 5.2 By Product

- 5.2.1 Folding Cartons

- 5.2.2 Corrugated Boxes and Containers

- 5.2.3 Other Products

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Personal Care

- 5.3.5 Household Care

- 5.3.6 Electrical and Electronics

- 5.3.7 Other End-User Industries

- 5.4 By Packaging Format

- 5.4.1 Rigid (Corrugated, Solid Board)

- 5.4.2 Semi-rigid (Folding Cartons excluding Solid Board Boxes)

- 5.4.3 Flexible Paper (Sachets, Wraps)

- 5.4.4 Molded Fiber and Pulp Packaging Products

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SONG LAM Trading & Packaging Production CO., Ltd

- 6.4.2 Asia Pulp & Paper Group (APP)

- 6.4.3 Tetra Pak International S.A.

- 6.4.4 Oji Interpack Vietnam Co., Ltd

- 6.4.5 Khang Thanh Manufacturing CO., LTD

- 6.4.6 Hanh Packaging Co. Ltd

- 6.4.7 SCG Paper Public Company Limited

- 6.4.8 BINH MINH P.A.T CO.,LTD

- 6.4.9 Kraft of Asia Paperboard & Packaging Co., Ltd..

- 6.4.10 HC Packaging Vietnam Company Limited

- 6.4.11 Starprint Vietnam Joint Stock Company

- 6.4.12 Nippon Paper Industries Co., Ltd.

- 6.4.13 Box-Pak (Malaysia) Bhd.

- 6.4.14 Lee & Man Paper Manufacturing Ltd.

- 6.4.15 Sai Gon Paper Corporation

- 6.4.16 Dong Hai Ben Tre Joint Stock Company

- 6.4.17 Nine Dragons Paper (Holdings) Limited

- 6.4.18 Rengo Co., Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

可拉伸紙包裝市場:依材料等級、包裝形式、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測紙包裝材料市場:依產品類型、材料類型、印刷技術和應用分類-2026-2032年全球預測

可拉伸紙包裝市場:依材料等級、包裝形式、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測紙包裝材料市場:依產品類型、材料類型、印刷技術和應用分類-2026-2032年全球預測 紙包裝市場規模、佔有率、趨勢和預測:按產品類型、等級、包裝等級、最終用途產業和地區分類,2026-2034年

紙包裝市場規模、佔有率、趨勢和預測:按產品類型、等級、包裝等級、最終用途產業和地區分類,2026-2034年 中國紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲紙包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

中國紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲紙包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 全球紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球紙墊製造機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球紙瓶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球蜂窩紙板市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球紙墊製造機械市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球紙瓶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球蜂窩紙板市場規模、佔有率、趨勢和成長分析報告(2026-2034)