|

市場調查報告書

商品編碼

1940682

車載充電器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Automotive On-board Charger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

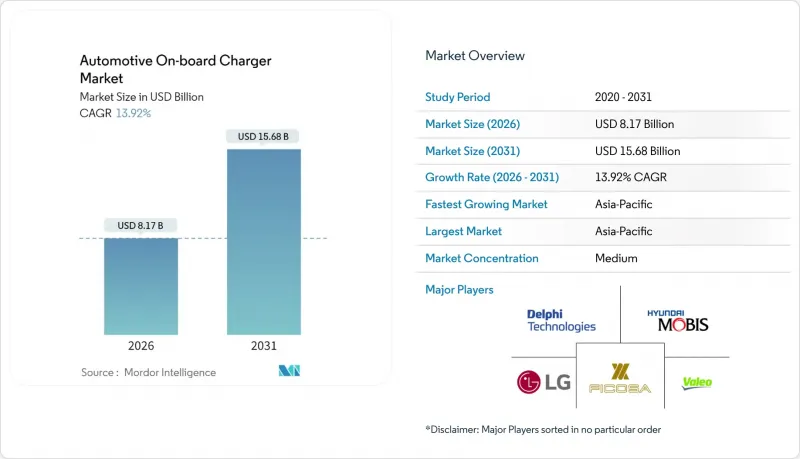

預計汽車車載充電器市場將從 2025 年的 71.7 億美元成長到 2026 年的 81.7 億美元,到 2031 年將達到 156.8 億美元,2026 年至 2031 年的複合年成長率為 13.92%。

主要經濟體電動車強制令的激增、向800V汽車平臺的快速轉型以及寬能能隙半導體價格的持續下降,共同推動了規範升級週期,並提升了對高功率充電解決方案的整體需求。在歐洲和部分亞洲市場,汽車製造商正將11-22kW的充電單元作為標準配置,以充分利用三相住宅電網的優勢。北美原始設備製造商(OEM)優先考慮本土充電器生產和ISO 15118合規性,在成本敏感度和聯邦獎勵之間尋求平衡。隨著一級供應商與繞過傳統價值鏈、追求牽引整合架構的純半導體公司爭奪市場佔有率,競爭日益激烈。同時,政策制定者正在收緊鋁製機殼的安全性和可回收性法規,這增加了設計變更的需求,並為供應商擴大了商機。預計這些結構性因素將在未來十年內支撐車載充電器市場持續兩位數的成長。

全球車用充電器市場趨勢及洞察

積極的全球電動車滲透目標和購車獎勵

各國零排放法規和購車補貼正在推動車載充電器基本規格的提升,因為汽車製造商競相提案具有競爭力的總擁有成本 (TCO)。中國2025年新能源汽車銷售目標、歐盟2030年所有車輛二氧化碳排放減半的要求以及加州「先進清潔汽車II」計劃,都在加速標配11kW或22kW交流充電功能的車型上市。韓國的目標是在本十年末大幅提高電動車的普及率,現代摩比斯計劃從本十年後半期開始擴大整合充電控制單元 (ICCU) 的生產。此舉凸顯了該地區需求的快速成長,並有助於降低碳化矽 (SiC) 裝置的價格。同時,補貼計畫也擴大提供家用充電樁代金券。這不僅縮短了消費者投資購買高功率壁掛式充電樁的投資回收期,也證明了汽車製造商投資於車載充電器雙向功率傳輸和ISO 15118認證等先進功能的合理性。

快速過渡到800V車載系統,可實現11-22kW車載充電器

向 800V 電氣系統的過渡重新定義了成本績效的界限,它能夠在不增加銅材用量或熱負荷的情況下實現高功率密度。現代的 E-GMP 和通用的 Ultium 可快速充電,其 22kW 的交流充電容量與住宅能源套利完美互補。 FORVIA HELLA 等供應商正在將英飛凌的 CoolSiC 模組整合機殼,以實現最高效率並將冷卻板面積減少三分之一,從而釋放引擎室空間用於輔助電子設備。早期採用者利用充電時間的縮短來獲取溢價,並在將獎勵合格與最低充電性能標準掛鉤的市場中獲得寶貴的合規積分。隨著一級供應商對 800V 相容設計進行預先認證,二級採用者面臨著更短的設計時間,從而推動了對承包參考平台的需求。這種協同效應正在推動基礎級功率等級的提高,並將車載充電器市場擴展到傳統的 3.3-7.4kW 範圍之外。

22kW三相車載充電器中寬能能隙基板持續高成本

儘管晶圓代工廠擴張創下紀錄,但碳化矽晶錠產量比率仍低於五分之三,氮化鎵外延片前置作業時間超過30晶粒,基板成本仍居高不下。車規級650V碳化矽MOSFET晶片的價格仍比平面矽IGBT高出三到四分之三,這使得高功率三相設計僅限於高階品牌和商用車領域。散熱器和電磁干擾屏蔽進一步增加了系統材料成本,部分抵消了寬能能隙帶來的密度優勢。在成本敏感的C級跨界車市場,每瓦0.02美元的價格差異就意味著組件成本增加約45美元,這擠壓了價格彈性較大市場的零售利潤。因此,原始設備製造商(OEM)推遲了在歐洲以外地區推出22kW可選充電線的計劃,直到成本下降,這暫時限制了下一代充電器在車載充電市場的滲透率。

細分市場分析

從 2025 年到 2031 年,商用車的複合年成長率最高,達 14.05%,而乘用車在 2025 年佔車用充電器市場規模的 65.82%。由於以倉庫為中心的運作週期強調最大限度地減少待機時間,物流運營商正在指定使用 22kW 雙向充電器,以最大限度地提高夜間能源處理能力並參與公用事業需量反應計劃。

由於潛在車牌基數較大,乘用車仍將支撐其絕對出貨量,但隨著平台通用限制了期權價格的彈性,其單價貢獻將會下降。安全法規、網路安全要求和可回收性規則的趨同將增加車隊專用解決方案的非經常性工程成本,從而為專業供應商提供利潤空間。車隊也率先使用增值分析功能,例如充電器利用率儀錶板和預防性維護警報,這使得整合式車載充電器解決方案的獲利模式更加多元化。因此,儘管不同車型的發展趨勢將塑造不同的成長軌跡,但總體而言,車載充電器市場將保持兩位數的收入成長。

截至2025年,純電動車(BEV)將佔車用充電器市場76.18%的佔有率,並將在2031年之前維持14.02%的複合年成長率。純電動滑板式架構釋放了後軸上方的空間,從而可以安裝集中式電力電子設備艙,車載充電器(OBC)、牽引逆變器和直流-直流轉換器共用一個標準冷卻迴路。由於底置式燃料箱的限制,這種佈局能夠實現插電式混合動力汽車(PHEV)佈局無法複製的成本節約型協同工作。

儘管插電式混合動力汽車持續滿足監管和區域市場的小眾需求,但由於成本和重量控制,雙燃料系統的複雜性限制了車載充電器(OBC)的額定功率,使其僅為7.4kW左右。中國和歐洲的監管積分制度正在逐步降低插電式混合動力汽車(PHEV)的獎勵倍數,從而削弱了高階充電功能的商業價值。供應商優先考慮為純電動車(BEV)車隊客韌體,以實現動態相位切換和諧波抑制,同時保持插電式混合動力車的設計基本上衍生BEV的設計。預計到2029年,純電動車將佔西歐新車註冊量的一半,供應商預測,純電動車專用車用充電器將佔總收入的85%以上,這鞏固了車載充電器市場的長期成長前景。

區域分析

亞太地區將引領車用充電器市場,到2025年將佔據37.35%的市場佔有率,並將繼續保持領先地位,到2031年將以14.07%的複合年成長率成長,這主要得益於中國GB38031-2025電池安全標準和創紀錄的電動車推廣政策。截至2023年底,中國當地已安裝數百萬個公共和私人充電樁。這項里程碑式的成就不僅樹立了充電密度標準,也使得在高層公寓大樓等共用三相立管的場所實現家庭充電成為可能。為完成鋁製機殼回收配額,中國工業和資訊化部正在推進材料替代舉措。

歐洲作為全球第二大市場,持續保持強勁成長動能。這一成長勢頭主要得益於《汽車基礎設施法規》(AFIR) 的實施,該法規強制要求充電樁符合 ISO 15118 標準,並規定了跨歐洲交通網路沿線充電站的密度。德國和法國正在將核能和可再生能源併入電網,以穩定其碳排放強度。這種整合使得電力公司能夠利用中高容量充電樁的車網互動 (V2G) 功能,提供動態費率方案。

北美地區受惠於《通膨控制法案》下的先進製造業稅額扣抵。此外,由東北電動車計劃(NEVI)資助的走廊開發案也有助於加強該地區的基礎設施。然而,除高階品牌外,大容量充電樁的普及率仍然有限,這主要是由於單相住宅供電的限制。為此,汽車製造商推出了高功率的雙相充電樁,但市場滲透率仍然不高。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 積極的全球電動車普及目標和購車激勵措施

- 快速遷移至 800V 汽車架構,實現 11-22kW 車用電腦

- 由於SIC/GAN裝置價格下降,OBC功率密度不斷提高。

- 歐盟和美國資金籌措計畫中強制性的 ISO 15118/即插即用和 V2G 條款

- 一級供應商/OEM過渡到牽引整合式雙向3合1電力驅動橋(OBC)

- 新興市場太陽能光電系統整合商通路:屋頂太陽能光電發電+相容車載電池的電動車套餐捆綁銷售

- 市場限制

- 22kW三相OBC中寬能能隙基板持續高成本

- 隨著直流超快充電器(功率超過350kW)的普及,汽車零件製造商不願改進交流充電器的規格。

- 高密度城市中住宅11kW擴容的併網瓶頸。

- 中國廢料回收法規即將對大型OBC鋁製外殼課稅。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 按車輛類型

- 搭乘用車

- 商用車輛

- 依動力傳動系統類型

- 電池式電動車(BEV)

- 插電式混合動力電動車(PHEV)

- 額定功率

- 小於 3.3 千瓦

- 3.3~11 kW

- 11千瓦或以上

- 按銷售管道

- 原廠配套設備

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 埃及

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BorgWarner Inc.

- Hyundai Mobis

- LG Electronics

- STMicroelectronics

- Ficosa International SA

- Valeo SE

- Delta Energy Systems AG

- Toyota Industries Corp.

- Brusa Elektronik AG

- VisIC Technologies

- Infineon Technologies AG

- Eaton Corp.

- DENSO Corp.

- Panasonic Industry

- TDK Corp.

- Onsemi

- Stercom Power Solutions

- Delta-Q Technologies

第7章 市場機會與未來展望

The Automotive On-board Charger Market is expected to grow from USD 7.17 billion in 2025 to USD 8.17 billion in 2026 and is forecast to reach USD 15.68 billion by 2031 at 13.92% CAGR over 2026-2031.

Surging electric-vehicle adoption mandates across major economies, the rapid migration to 800 V vehicle platforms, and steady declines in wide-band-gap semiconductor pricing collectively reinforce a cycle of specification upgrades that lift overall demand for higher-power charging solutions. Automakers leverage three-phase residential grids in Europe and selected Asian markets to standardize 11-22 kW units. North American OEMs balance cost sensitivities against federal incentives, prioritizing domestic charger production and ISO 15118 compliance. Competitive momentum intensifies as tier-1 suppliers defend share against semiconductor specialists that bypass traditional value chains to pursue traction-combined architectures. At the same time, policymakers tighten safety and recyclability rules on aluminum housings, creating incremental redesign requirements that expand supplier addressable revenue. Together, these structural forces sustain double-digit growth for the Automotive on-board charger market through the decade.

Global Automotive On-board Charger Market Trends and Insights

Aggressive Global EV Adoption Targets & Purchase Incentives

National zero-emission mandates and purchase subsidies elevate the baseline specification of on-board chargers as OEMs race to deliver compelling total-cost-of-ownership propositions. China's new-energy vehicle sales goal for 2025, the European Union's half of fleet-wide CO2-reduction requirement for 2030, and California's Advanced Clean Cars II program together accelerate model launches that embed 11 kW or 22 kW AC capability as standard equipment . With South Korea aiming for a significant increase in EV adoption by the end of the decade, Hyundai Mobis is set to ramp up production of integrated charging control units (ICCU) starting in the latter half of the decade. This move underscores a regional demand surge, contributing to a price drop for SiC devices. Meanwhile, subsidy frameworks are increasingly offering home-charging vouchers. This tactic not only shortens the payback period for consumers investing in higher-power wallboxes but also validates OEMs' investments in advanced features like bi-directional energy flow and ISO 15118 authentication for on-board chargers.

Rapid Switch To 800 V Vehicle Architectures Enabling 11-22 kW OBCs

The migration toward 800 V electrical systems reshapes cost-performance frontiers by enabling higher power densities without proportional increases in copper mass or thermal overhead. Hyundai's E-GMP and GM's Ultium demonstrate quick charging scenarios, making 22 kW AC capability a natural complement for residential energy arbitrage . Suppliers such as FORVIA HELLA integrate Infineon CoolSiC modules into compact housings, achieving maximum efficiency and reducing cooling plate area by one-third, freeing under-hood volume for auxiliary electronics. Early adopters leverage reduced charge times to command pricing premiums and secure valuable compliance credits in markets that tie incentive eligibility to minimum charging performance thresholds. As tier-1s pre-qualify 800 V-ready designs, secondary adopters face compressed design windows, intensifying the demand for turnkey reference platforms. The net effect elevates base-grade power ratings and scales the Automotive on-board charger market beyond its historical 3.3-7.4 kW spine.

Persistently High Wide-Band-Gap Substrate Costs in 22 kW Three-Phase OBCs

Despite record foundry expansions, SiC boule yields under three-fifths and GaN epi-wafer lead times surpassing 30 weeks prolong elevated substrate economics. Automotive-grade 650 V SiC MOSFET die still commands a 3-4 times premium over planar silicon IGBTs, limiting high-power three-phase designs to premium badges and commercial fleets. Heat-spreading plates and EMI shielding further inflate system material costs, offsetting some of the density gains from wide-band-gap adoption. For value-oriented C-segment crossovers, each USD 0.02 / W price delta translates to roughly USD 45 in incremental BOM, pressuring retail margins in price-elastic markets. OEMs thus defer 22 kW option codes outside Europe until cost curves decline, creating a temporary ceiling on the penetration rate of next-gen chargers in the Automotive on-board charger market.

Other drivers and restraints analyzed in the detailed report include:

- Declining SiC/GaN Device Prices Lifting OBC Power Density

- Mandatory ISO 15118 / Plug-and-Charge & V2G Readiness Clauses

- OEM Hesitancy To Up-Spec AC Chargers As DC Ultra-Fast Networks Accelerate

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial vehicles contributed the fastest 14.05% CAGR during 2025-2031, even though passenger cars controlled 65.82% of the Automotive on-board charger market size in 2025. Depot-centric duty cycles reward fleets that minimize dwell times; thus, logistics operators specify 22 kW bi-directional chargers to maximize overnight energy throughput and participate in utility demand-response.

Passenger cars will continue to anchor absolute shipments because of larger addressable license-plate bases, yet their unit-value contribution tapers as platform commonization curbs option-pricing latitude. The convergence of safety regulations, cybersecurity mandates, and recyclability rules amplifies non-recurring engineering outlays for fleet-specific solutions, giving specialized suppliers a margin buffer. Fleets also pioneer value-added analytics such as charger-utilization dashboards and preventive-maintenance alerts that monetarily differentiate integrated OBC offerings. Consequently, vehicle-type dynamics shape divergent growth trajectories but collectively keep the broader Automotive on-board charger market on a double-digit revenue track.

Battery electric vehicles captured 76.18% of the Automotive on-board charger market share in 2025 and maintain the lead with a 14.02% CAGR through 2031. Pure-electric skateboard architectures free volume above the rear axle, enabling centralized power-electronics bays where OBCs, traction inverters, and DC-DC stages share a standard coolant loop. Due to under-floor fuel-tank constraints, this packaging unlocks cost collaborations that PHEV layouts cannot replicate.

Plug-in hybrids continue to serve compliance and rural-market niches, but their dual-fuel complexity caps OBC ratings near 7.4 kW to manage cost and mass. Regulatory credit systems in China and Europe progressively lower bonus multipliers for PHEVs, tightening the business case for premium charging upgrades. Suppliers prioritize firmware customization for BEV fleets-enabling dynamic phase switching and harmonic mitigation-while keeping PHEV designs largely derivative. As BEVs cross half of new-car registrations in Western Europe by 2029, suppliers expect BEV-dedicated OBCs to represent more than 85% of total revenue, solidifying long-term growth prospects for the Automotive on-board charger market.

The Automotive On-Board Charger Market Report is Segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Powertrain Type (Battery Electric Vehicles and Plug-In Hybrid Electric Vehicles), Power Rating (Less Than 3. 3 KW, 3. 3-11 KW, and More Than 11 KW), Sales Channel (OEM-Installed and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific led with 37.35% share of the Automotive on-board charger market size in 2025 and continues to outpace peers at a 14.07% CAGR through 2031, buoyed by China's GB38031-2025 battery-safety mandate and record EV adoption incentives. By the close of 2023, mainland installations boasted millions of public and private charging units. This milestone set density thresholds, making home charging feasible for high-rise apartments with shared three-phase risers. In a move to address recycling quotas on aluminum housings, the Chinese Ministry of Industry and Information Technology spurred material-substitution initiatives.

Europe, holding the second spot, continues to witness vigorous growth. This momentum is primarily fueled by AFIR's mandates on ISO 15118 compatibility and the requisite density of charging stations along the Trans-European Transport Network. Germany and France are weaving nuclear and renewable energy into their grids to stabilize grid-carbon intensity. This integration empowers utilities to roll out dynamic tariff products, capitalizing on the vehicle-to-grid capabilities of mid-to-high capacity chargers.

North America is reaping the benefits of the Inflation Reduction Act's advanced-manufacturing tax credits. Additionally, NEVI-funded corridor developments are bolstering the region's infrastructure. However, the adoption of higher-capacity chargers remains limited outside luxury brands, primarily due to the constraints of single-phase residential services. In response, OEMs offer dual chargers with higher output capacities, though market penetration is still modest.

- BorgWarner Inc.

- Hyundai Mobis

- LG Electronics

- STMicroelectronics

- Ficosa International S.A.

- Valeo SE

- Delta Energy Systems AG

- Toyota Industries Corp.

- Brusa Elektronik AG

- VisIC Technologies

- Infineon Technologies AG

- Eaton Corp.

- DENSO Corp.

- Panasonic Industry

- TDK Corp.

- Onsemi

- Stercom Power Solutions

- Delta-Q Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aggressive Global EV Adoption Targets & Purchase Incentives

- 4.2.2 Rapid Switch To 800 V Vehicle Architectures Enabling 11-22 kW OBCs

- 4.2.3 Declining SIC/GAN Device Prices Lifting OBC Power Density

- 4.2.4 Mandatory ISO 15118 / Plug-&-Charge & V2G Readiness Clauses In EU & US Funding Schemes

- 4.2.5 Tier-1/OEM Migration To Traction-Integrated & Bidirectional OBCs (3-In-1 E-Axle)

- 4.2.6 PV-Integrator Channel In Emerging Markets Bundling Rooftop Solar + OBC-Ready EV Packages

- 4.3 Market Restraints

- 4.3.1 Persistently High Wide-Band-Gap Substrate Costs In 22 Kw Three-Phase OBCs

- 4.3.2 OEM Hesitancy To Up-Spec AC Chargers As DC Ultra-Fast (>=350 Kw) Roll-Outs Accelerate

- 4.3.3 Grid-Connection Bottlenecks For Residential 11 Kw Upgrades In Dense Cities

- 4.3.4 Impending Scrap-Recycling Regulation In China Taxing Large OBC Aluminum Housings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Powertrain Type

- 5.2.1 Battery Electric Vehicles (BEVs)

- 5.2.2 Plug-in Hybrid Electric Vehicles (PHEVs)

- 5.3 By Power Rating

- 5.3.1 Less than 3.3 kW

- 5.3.2 3.3-11 kW

- 5.3.3 More than 11 kW

- 5.4 By Sales Channel

- 5.4.1 OEM-installed

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 UAE

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Nigeria

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BorgWarner Inc.

- 6.4.2 Hyundai Mobis

- 6.4.3 LG Electronics

- 6.4.4 STMicroelectronics

- 6.4.5 Ficosa International S.A.

- 6.4.6 Valeo SE

- 6.4.7 Delta Energy Systems AG

- 6.4.8 Toyota Industries Corp.

- 6.4.9 Brusa Elektronik AG

- 6.4.10 VisIC Technologies

- 6.4.11 Infineon Technologies AG

- 6.4.12 Eaton Corp.

- 6.4.13 DENSO Corp.

- 6.4.14 Panasonic Industry

- 6.4.15 TDK Corp.

- 6.4.16 Onsemi

- 6.4.17 Stercom Power Solutions

- 6.4.18 Delta-Q Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

汽車充電器市場:2026-2032年全球市場預測(依車輛類型、電壓、輸出功率及銷售管道分類)

汽車充電器市場:2026-2032年全球市場預測(依車輛類型、電壓、輸出功率及銷售管道分類) 全球電動車車載充電器市場:依動力類型、車輛類型、輸出功率、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測

全球電動車車載充電器市場:依動力類型、車輛類型、輸出功率、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測 交流電動車車載充電器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、安裝類型、最終用戶、功能、設備及解決方案分類

交流電動車車載充電器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、安裝類型、最終用戶、功能、設備及解決方案分類 車載充電器市場規模、佔有率、趨勢和預測(按功率輸出、車輛類型、動力方式、分銷管道和地區分類),2026-2034年

車載充電器市場規模、佔有率、趨勢和預測(按功率輸出、車輛類型、動力方式、分銷管道和地區分類),2026-2034年 2026年全球車用充電器市場報告雙向汽車電池充電器市場報告(2026 年)

2026年全球車用充電器市場報告雙向汽車電池充電器市場報告(2026 年) 電動車車用充電器市場-全球產業規模、佔有率、趨勢、機會與預測:按動力類型、車輛類型、分銷管道、設計類型、產品類型、地區和競爭格局分類,2021-2031年

電動車車用充電器市場-全球產業規模、佔有率、趨勢、機會與預測:按動力類型、車輛類型、分銷管道、設計類型、產品類型、地區和競爭格局分類,2021-2031年 電動汽車車載充電器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

電動汽車車載充電器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 全球雙向充電市場(至2035年):按應用(V2G、V2H、V2L)、動力類型(純電動車、插電式混合動力車)、車輛類型(乘用車、輕型商用車)、充電型(交流電充電、直流充電)、最終用戶和地區分類

全球雙向充電市場(至2035年):按應用(V2G、V2H、V2L)、動力類型(純電動車、插電式混合動力車)、車輛類型(乘用車、輕型商用車)、充電型(交流電充電、直流充電)、最終用戶和地區分類 2032 年車用充電器市場預測:按車輛類型、推進類型、充電器類型、輸出功率、最終用戶和地區進行的全球分析

2032 年車用充電器市場預測:按車輛類型、推進類型、充電器類型、輸出功率、最終用戶和地區進行的全球分析