|

市場調查報告書

商品編碼

1940649

汽車預測技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Predictive Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

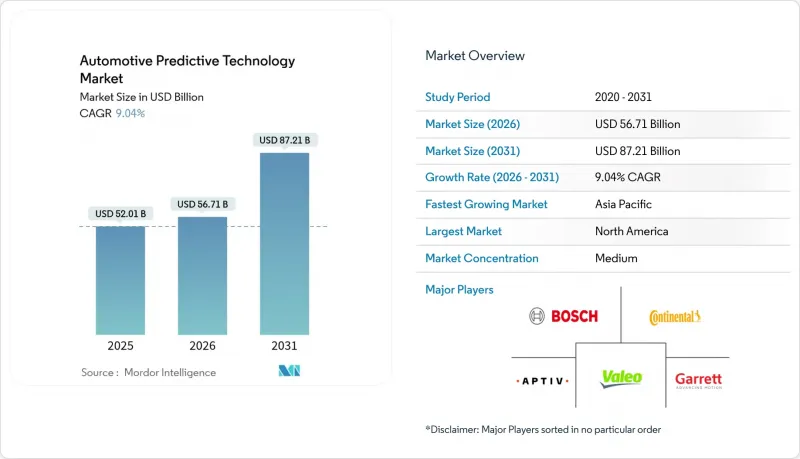

預計到 2026 年,汽車預測技術市場規模將達到 567.1 億美元,高於 2025 年的 520.1 億美元。

預計到 2031 年,該市場規模將達到 872.1 億美元,2026 年至 2031 年的複合年成長率為 9.04%。

這項快速擴張的驅動力在於業界正從被動維護轉向嵌入式智慧,後者能夠直接在車輛架構中提供即時洞察。邊緣運算與雲端分析相輔相成,使安全關鍵功能能夠在亞毫秒時間內做出決策。商業車隊管理人員透過將預測工具與 5G 車載資訊系統整合,顯著減少了計劃外維護;而採用基於使用情況分析的保險公司也報告稱,索賠頻率有所降低。安全和排放氣體方面的監管要求持續推動市場需求,而感測器成本的下降則降低了採用門檻。同時,NVIDIA、高通和微軟等技術供應商正透過將車規級 AI 晶片組和可擴展的雲端平台引入價值鏈,加劇市場競爭。

全球汽車預測技術市場趨勢與洞察

快速普及互聯車載資訊服務和5G技術

配備 5G 車載資訊系統的商用車輛,由於預測演算法能夠以低於 20 毫秒的延遲傳輸高解析度感測器數據,因此非計畫維修次數顯著減少。遠高於 4G 的網路吞吐量使得維護系統能夠持續分析振動、溫度和流體動態。車隊營運商可以將這些資訊轉化為動態維護計劃,從而相比固定間隔維護模式,顯著減少停機時間。乘用車同樣受益,可以透過空中下載 (OTA) 更新來升級預測軟體,從而最佳化零件壽命,而駕駛者不會察覺到車輛運行過程中產生的計算負荷,這些計算負荷正是車輛保持最佳狀態的關鍵所在。

OEM整合AI/ML用於預測性維護

汽車製造商正將神經網路技術融入車輛中央控制設備。 BMW的iDrive系統升級透過同時評估多個參數並產生個人化的健康檢查報告,減少了保固索賠。原始設備製造商(OEM)對匿名化車隊資料的掌控,使得新車型比以往車型更加智慧,因為演算法會利用數百萬小時的集體駕駛數據進行重新訓練。這種持續學習的過程重新定義了產品差異化,使車主更傾向於那些能夠預測故障發生的品牌。這不僅延長了零件的使用壽命,也提高了車輛的殘值。

資料隱私和網路安全問題

GDPR將遠端資訊處理資料歸類為個人識別訊息,即使經過匿名化處理,並設定了同意門檻,從而減緩了其普及。 2024年,針對聯網汽車的網路攻擊增加,凸顯了分散式預測架構的脆弱性。儘管汽車製造商在加密方面投入巨資,但消費者仍將隱私擔憂視為猶豫不決的主要原因。在身分驗證方案成熟之前,一些購車者可能會避免購買連網汽車。

細分市場分析

截至2025年,預測性維護將佔汽車預測技術市場48.62%的佔有率。隨著車隊從定期檢查轉向基於狀態的維修,營運商的維護成本顯著降低。由於駕駛者越來越重視即時通知以預防路邊故障,預計預警系統將以11.12%的複合年成長率成長。隨著監管機構強制要求使用高級駕駛輔助系統,安全分析技術正蓬勃發展。同時,交通最佳化正在將預測數據與智慧城市基礎設施結合。在商業領域,駕駛員行為監控正與提供保費折扣的保險計劃相結合,進一步加速了其普及應用。

這些應用場景逐漸趨於融合:單一軟體堆疊可以同時支援維修演算法、道路危險預測和駕駛引導儀錶板,預示著未來平台整合的趨勢。能夠將維護分析與即時安全警報結合的供應商,最有希望主導高級訂閱和資料變現的機會。

到2025年,乘用車將佔總收入的60.73%,而中型和重型商用車將以9.86%的複合年成長率實現最高成長。由於重型卡車每運作一小時就意味著錯失一次配送機會,因此提高其預計運轉率將為物流業者帶來即時的回報。

電氣化進一步提高了競爭門檻:預測性電池維護如今會影響路線規劃、充電時間最佳化和轉售定價。輕型商用車領域正在形成新的成長點,電商車隊採用預測模組,將維護與小包裹遞送高峰同步。雖然個人車仍將是最大的車隊基數,但商用車領域的營運壓力將影響未來十年的產品藍圖。

區域分析

預計到2025年,北美將佔據44.05%的市場佔有率,這主要得益於5G網路的廣泛覆蓋、不斷擴展的高速公路網路以及鼓勵採用遠端資訊處理技術的聯邦安全政策。重型卡車營運商經常面臨聯邦汽車運輸安全管理局(FMCSA)關於電子檢驗報告的法規要求,這進一步促使車隊採用預測性儀錶板。技術合作也不斷拓展,例如通用汽車將其OnStar遠端資訊處理系統與微軟Azure整合,為企業客戶提供一套分析服務。

亞太地區正以10.11%的複合年成長率快速成長,主要得益於中國到2030年新能源汽車銷售佔比達到40%的目標。因此,電池技術的發展前景是該地區的重點領域。日本供應商如電裝(Denso)正在將邊緣人工智慧晶片整合到下一代電控系統中,而韓國則憑藉三星的半導體技術鞏固了其在區域硬體領域的領先地位。在印度和新加坡,政府主導的智慧交通試點計畫正在加速城市分析與預測性車輛子系統的整合。這反映出一種更廣泛的生態系統趨勢,即超越單一車輛,在城市層面協調交通出行。

儘管隱私法規複雜,歐洲仍在穩步推進。德國製造商正在試驗一項跨廠商資料共用信任機制,以在遵守GDPR的前提下訓練全球模型;歐盟的跨境排放交易體係也促進了車隊範圍內的預測性監控。西門子交通和寶馬的聯合數位雙胞胎專案展示了工業IoT堆疊如何相互影響汽車分析,這表明歐洲的成長將取決於超越單一OEM廠商障礙的多方資料合作。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速普及互聯車載資訊服務和5G技術

- OEM整合AI/ML用於預測性維護

- 更嚴格的車輛安全和排放氣體法規

- 電動汽車車隊的不斷擴大需要進行預測性電池維護

- 用於車載預測處理的邊緣人工智慧晶片

- 基於使用情況的保險對駕駛員分析的需求

- 市場限制

- 資料隱私和網路安全問題

- 高昂的實施和整合成本

- 熟練的資料科學人才短缺

- 預測模型在不同氣候條件和運作週期下的可靠性

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過使用

- 預測性維護

- 主動預警

- 安全保障

- 交通管理

- 駕駛員行為監控

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 透過部署

- 本地部署

- 基於雲端的

- 透過硬體

- ADAS組件

- 遠端資訊處理控制單元

- 感應器

- GPS模組

- 相機

- 其他

- 最終用戶

- OEM

- 售後市場

- 透過技術

- 機器學習

- 巨量資料分析

- 人工智慧

- 物聯網整合

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- Aptiv PLC

- Valeo SA

- ZF Friedrichshafen AG

- Garrett Motion Inc.

- NXP Semiconductors NV

- Siemens AG

- IBM Corporation

- Teletrac Navman

- Harman International Industries, Inc.

- Verizon Connect

- Trimble Inc.

- Geotab Inc.

- Uptake Technologies Inc.

- NVIDIA Corporation

- Microsoft Corporation

- PTC Inc.

- SAP SE

第7章 市場機會與未來展望

Automotive predictive technology market size in 2026 is estimated at USD 56.71 billion, growing from 2025 value of USD 52.01 billion with 2031 projections showing USD 87.21 billion, growing at 9.04% CAGR over 2026-2031.

This rapid expansion stems from the industry's migration from reactive maintenance to embedded intelligence that delivers real-time insights directly inside the vehicle architecture. Edge computing now complements cloud analytics, enabling sub-millisecond decision-making for safety-critical functions. Commercial fleet managers have documented notable drops in unplanned maintenance when predictive tools are integrated with 5G telematics, while insurers that adopt usage-based analytics report lower claim frequencies. Regulatory mandates for safety and emissions continually pull demand upward, and falling sensor costs ease adoption barriers. In parallel, technology suppliers such as NVIDIA, Qualcomm, and Microsoft intensify competition by bringing automotive-grade AI chipsets and scalable cloud platforms into the value chain.

Global Automotive Predictive Technology Market Trends and Insights

Rapid Adoption of Connected Telematics and 5G

Commercial vehicles equipped with 5G telematics exhibit significantly fewer unscheduled service events because predictive algorithms stream high-resolution sensor data with latency below 20 milliseconds. Network throughput that is significantly greater than 4G lets maintenance systems analyze vibration, temperature, and fluid dynamics continuously. Fleet operators translate these insights into dynamic service schedules, cutting downtime over fixed-interval models. Passenger cars benefit as well, receiving over-the-air predictive software updates that optimize component life while drivers remain unaware of the computing workloads that keep the vehicle in peak condition.

OEM Integration of AI/ML for Predictive Maintenance

Automakers are embedding neural networks in central vehicle controllers; BMW's iDrive upgrade evaluates several parameters at once to generate personalized health diagnostics, trimming warranty claims. OEM control of anonymized fleet data makes every new model release smarter than the last because algorithms retrain on millions of collective driving hours. This continuum of learning redefines product differentiation; owners gravitate toward brands that can predict faults before they surface, thereby extending component life and boosting residual value.

Data-Privacy and Cybersecurity Concerns

GDPR classifies telematics data as personally identifiable even when anonymized, forcing consent hurdles that slow deployments. Cyberattacks on connected vehicles rose in 2024, highlighting vulnerabilities in distributed predictive architectures. Automakers spend heavily on encryption, yet consumers still cite privacy worries among top purchase hesitations. Until certification schemes mature, some buyers will avoid always-connected vehicles.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Emphasis on Vehicle Safety and Emissions

- Expansion of EV Fleets Requiring Battery Prognostics

- High Implementation and Integration Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Predictive maintenance held a 48.62% share of the automotive predictive technology market in 2025. Operators documented maintenance savings once vehicles switched from scheduled service to condition-based repairs. Proactive alerts are on track for an 11.12% CAGR because drivers value real-time notifications that prevent roadside failures. Safety and security analytics gain momentum as regulators mandate advanced driver assistance upgrades, while traffic optimization marries predictive data with smart-city infrastructure. In commercial scenarios, driver-behavior monitoring dovetails with insurance programs that offer premium discounts, further accelerating adoption.

These use cases are starting to converge. A single software stack can now feed maintenance algorithms, road-hazard predictions, and driver coaching dashboards simultaneously, pointing to future platform consolidation. Vendors that combine maintenance insights with real-time safety warnings are best positioned to command premium subscriptions and data monetization opportunities.

Passenger cars contributed 60.73% revenue in 2025, yet medium and heavy commercial vehicles carry the highest forward momentum at a 9.86% CAGR. Every hour of downtime costs a heavy-duty truck in lost deliveries, which makes predictive uptime an immediate payback for logistics operators.

Electrification amplifies the stakes: battery prognostics now inform route planning, charge-window optimization, and resale pricing. Light commercial vans add another layer of growth with e-commerce fleets adopting predictive modules that sync servicing around parcel-delivery peaks. Although personal vehicles remain the largest unit base, the commercial segment's operational pressures will shape product roadmaps for the next decade.

The Automotive Predictive Technology Market Report is Segmented by Application (Predictive Maintenance, Proactive Alerts, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Deployment (On-Premise, Cloud-Based), Hardware (ADAS Components, Telematics Control Units, and More), End User (OEM, Aftermarket), Technology, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured a 44.05% share in 2025 on the back of 5G coverage, a major portion of major highway miles, and federal safety policies that reward telematics adoption. Heavy truck operators often face Federal Motor Carrier Safety Administration mandates requiring electronic inspection reporting, further nudging fleets toward predictive dashboards. Technology alliances proliferate; General Motors links its OnStar telematics with Microsoft Azure to push analytics-as-a-service packages to corporate customers.

Asia-Pacific is expanding at a 10.11% CAGR, catalyzed by China's New Energy Vehicle target of 40% EV sales by 2030 . Battery prognosis, therefore, ranks high on local priority lists. Japanese suppliers such as Denso bundle edge-AI chips inside next-generation electronic control units, and South Korea leverages semiconductor muscle from Samsung to cement regional leadership in hardware. Government-funded smart-transport pilots in India and Singapore accelerate urban analytics integration with predictive vehicle subsystems, reflecting a broader ecosystem push beyond individual vehicles toward city-level mobility orchestration.

Europe posts steady gains despite thorny privacy rules. German manufacturers pilot cross-vendor data-sharing trusts that satisfy GDPR while still training global models, and the EU's cross-border emissions-trading schemes encourage fleetwide predictive monitoring. Siemens Mobility's Digital Twin program in collaboration with BMW, shows how industrial IoT stacks cross-fertilize automotive analytics, indicating that European growth will hinge on multiparty data alliances that transcend single OEM silos.

- Robert Bosch GmbH

- Continental AG

- Aptiv PLC

- Valeo SA

- ZF Friedrichshafen AG

- Garrett Motion Inc.

- NXP Semiconductors N.V.

- Siemens AG

- IBM Corporation

- Teletrac Navman

- Harman International Industries, Inc.

- Verizon Connect

- Trimble Inc.

- Geotab Inc.

- Uptake Technologies Inc.

- NVIDIA Corporation

- Microsoft Corporation

- PTC Inc.

- SAP SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Connected Telematics and 5G

- 4.2.2 OEM Integration of AI/ML for Predictive Maintenance

- 4.2.3 Regulatory Emphasis on Vehicle Safety and Emissions

- 4.2.4 Expansion of EV Fleets Requiring Battery Prognostics

- 4.2.5 Edge-AI Chips Enabling On-Vehicle Predictive Processing

- 4.2.6 Usage-Based Insurance Demand for Driver Analytics

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cybersecurity Concerns

- 4.3.2 High Implementation and Integration Costs

- 4.3.3 Shortage of Skilled Data-Science Talent

- 4.3.4 Reliability of Predictive Models Across Climates and Duty-Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Predictive Maintenance

- 5.1.2 Proactive Alerts

- 5.1.3 Safety and Security

- 5.1.4 Traffic Management

- 5.1.5 Driver Behavior Monitoring

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Deployment

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.4 By Hardware

- 5.4.1 ADAS Components

- 5.4.2 Telematics Control Units

- 5.4.3 Sensors

- 5.4.4 GPS Modules

- 5.4.5 Cameras

- 5.4.6 Others

- 5.5 By End User

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Technology

- 5.6.1 Machine Learning

- 5.6.2 Big-Data Analytics

- 5.6.3 Artificial Intelligence

- 5.6.4 IoT Integration

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.5.5 Rest of Middle-East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Aptiv PLC

- 6.4.4 Valeo SA

- 6.4.5 ZF Friedrichshafen AG

- 6.4.6 Garrett Motion Inc.

- 6.4.7 NXP Semiconductors N.V.

- 6.4.8 Siemens AG

- 6.4.9 IBM Corporation

- 6.4.10 Teletrac Navman

- 6.4.11 Harman International Industries, Inc.

- 6.4.12 Verizon Connect

- 6.4.13 Trimble Inc.

- 6.4.14 Geotab Inc.

- 6.4.15 Uptake Technologies Inc.

- 6.4.16 NVIDIA Corporation

- 6.4.17 Microsoft Corporation

- 6.4.18 PTC Inc.

- 6.4.19 SAP SE

7 Market Opportunities & Future Outlook

汽車預測技術市場:依產品、技術、車輛類型、應用、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

汽車預測技術市場:依產品、技術、車輛類型、應用、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 汽車預測性維護市場規模、佔有率和成長分析:按車輛類型、零件、部署類型、最終用戶和地區分類-2026-2033年產業預測

汽車預測性維護市場規模、佔有率和成長分析:按車輛類型、零件、部署類型、最終用戶和地區分類-2026-2033年產業預測 汽車預測技術市場規模、佔有率和成長分析:按技術、組件、應用、車輛類型、部署模式、最終用戶和地區分類-2026-2033年產業預測

汽車預測技術市場規模、佔有率和成長分析:按技術、組件、應用、車輛類型、部署模式、最終用戶和地區分類-2026-2033年產業預測 汽車預測技術市場規模、佔有率和成長分析:按應用、車輛類型、部署模式、硬體、技術和地區分類-2026-2033年產業預測

汽車預測技術市場規模、佔有率和成長分析:按應用、車輛類型、部署模式、硬體、技術和地區分類-2026-2033年產業預測 汽車技術市場預測:規模、佔有率、成長和全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

汽車技術市場預測:規模、佔有率、成長和全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 2026年全球汽車故障預測市場報告

2026年全球汽車故障預測市場報告 汽車預測性維護市場:按組件、技術、車輛類型、部署模式和最終用戶分類-2026-2032年全球市場預測2026年全球汽車市場預測分析報告全球汽車預測分析市場:依技術、類型、車輛類型、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測

汽車預測性維護市場:按組件、技術、車輛類型、部署模式和最終用戶分類-2026-2032年全球市場預測2026年全球汽車市場預測分析報告全球汽車預測分析市場:依技術、類型、車輛類型、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測 2026-2030年全球汽車預測性維護市場

2026-2030年全球汽車預測性維護市場