|

市場調查報告書

商品編碼

1871107

汽車預測性維護感測器市場機會、成長促進因素、產業趨勢分析及2025-2034年預測Automotive Predictive Maintenance Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

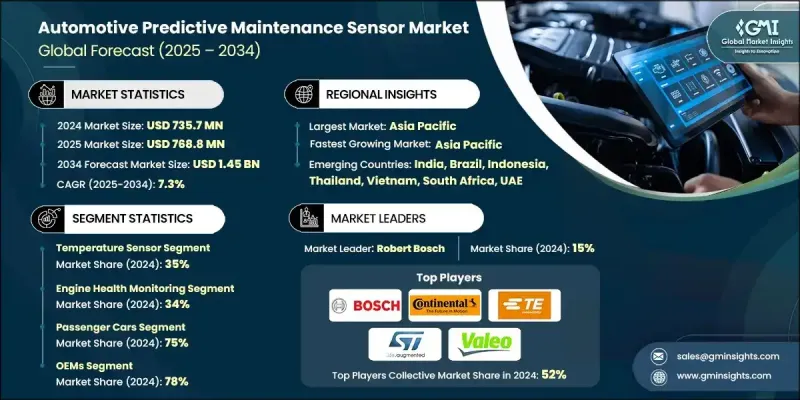

2024 年全球汽車預測性維護感測器市場價值為 7.357 億美元,預計到 2034 年將以 7.3% 的複合年成長率成長至 14.5 億美元。

市場成長的驅動力在於人們對車輛可靠性、運作安全性和成本效益日益成長的重視。預測性維護感測器在即時評估關鍵汽車零件的狀況方面發揮著至關重要的作用,能夠在故障發生前識別潛在問題。這種從被動或定期維護轉向主動維護策略的轉變,有助於減少車輛停機時間並降低營運成本。隨著車輛日益複雜,整合了先進的機械和電子系統,對持續監控的需求也不斷成長。政府安全法規也日益嚴格,促使製造商整合先進的診斷和監控系統。此外,物聯網框架支援的聯網車輛能夠實現集中式資料擷取和分析,從而提高預測性維護的精度和響應速度。在車輛設計、製造和營運週期中更廣泛地採用數據驅動的維護實踐,將繼續推動汽車預測性維護感測器市場的發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.357億美元 |

| 預測值 | 14.5億美元 |

| 複合年成長率 | 7.3% |

2024年,溫度感測器市佔率達到35%,預計到2034年將以9.14%的複合年成長率成長。溫度感測器是預測性維護中最廣泛應用的技術之一,因為它們有助於監控引擎、電池和空調系統等關鍵系統。溫度變化會導致過熱或零件性能下降,因此這些感測器對於早期故障檢測至關重要。透過提供即時溫度資料,這些感測器使維修團隊能夠主動安排維修,最大限度地減少計劃外停機時間,降低成本,並提高車輛的整體耐用性和可靠性。

2024年,引擎健康監測細分市場佔據34%的市場佔有率,預計2025年至2034年間將以7.04%的複合年成長率成長。由於引擎的高價值及其在車輛性能中的核心作用,引擎監控仍然是預測性維護中最關鍵的應用之一。該細分市場中的預測感測器可追蹤振動、溫度和燃油效率等眾多參數,有助於偵測異常情況,避免其演變為代價高昂的損壞。預測和預防潛在引擎故障的能力,為汽車製造商和車隊營運商在保持最佳性能和延長使用壽命方面提供了顯著的競爭優勢。

亞太地區汽車預測性維護感測器市場佔據44%的市場佔有率,預計2024年市場規模將達到3.237億美元。該地區的領先地位主要歸功於其強大的汽車生產基地,佔全球汽車產量的一半以上。亞太地區一直是技術進步的中心,在電動車、連網汽車和自動駕駛汽車系統方面取得了快速發展。該地區的製造商正大力投資於智慧汽車平台,這些平台依靠即時感測器資料來準確預測維護需求。結構性成長、產業現代化和強勁的技術發展正在鞏固亞太地區在全球市場的領先地位。

汽車預測性維護感測器市場的主要參與者包括海拉(Hella)、羅伯特·博世(Robert Bosch)、意法半導體(STMicroelectronics)、法雷奧(Valeo)、英飛凌科技(Infineon Technologies)、泰科電子(TE Con田nectivity)、大陸集團(Continental)、薩塔科技(Murata Technologies)製作(Murata Technologies)。為了鞏固其在汽車預測性維護感測器市場的地位,領先企業正在採取多項策略措施。許多企業致力於開發更高精度、更耐用、整合能力更強的先進感測器技術,以滿足連網汽車和電動車的需求。對研發的投入仍然是重中之重,旨在支持預測分析和資料處理領域的創新。與汽車製造商和技術供應商的策略合作與夥伴關係正在加速智慧維護系統的部署。此外,各企業也正在擴大產能並最佳化其全球供應鏈,以滿足不斷成長的區域需求。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預報

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 法規遵從要求(ISO 26262、聯合國歐洲經濟委員會法規)

- 車隊利用率最佳化要求

- 電動車普及加速

- 高級駕駛輔助系統整合

- 維護營運成本削減壓力

- 產業陷阱與挑戰

- 前期實施成本高

- 資料隱私和安全問題

- 市場機遇

- 軟體定義車輛架構的採用

- 5G 和先進連線部署

- 自動駕駛汽車開發

- 循環經濟和永續發展舉措

- 成長促進因素

- 成長潛力分析

- 專利分析

- 波特的分析

- PESTEL 分析

- 成本細分分析

- 技術格局

- 當前技術趨勢

- 新興技術

- 監管環境

- 價格趨勢

- 按地區

- 透過感測器

- 投資報酬率和商業案例分析

- 總擁有成本框架

- 實施成本結構

- 量化效益評估

- 投資與融資趨勢分析

- 實施路線圖框架

- 分階段部署策略

- 整合複雜性分析

- 變更管理要求

- 成功因素識別

- 性能基準測試框架

- 關鍵績效指標的定義與衡量

- 產業最佳實務分析

- 比較性能指標

- 持續改進模式

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新應用程式上線

- 擴張計劃和資金

第5章:市場估算與預測:依感測器類型分類,2021-2034年

- 主要趨勢

- 振動感測器

- 溫度感測器

- 壓力感測器

- 濕度感測器

- 聲學感測器

- 其他

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 引擎健康監測

- 變速箱和變速箱監控

- 電池和電氣系統監控

- 輪胎和車輪監測

- 冷卻系統監控

- 其他

第7章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商業銷售通路

- 輕型商用車銷售通路(LCV)

- 中型商業銷售通路(MCV)

- 重型商用車銷售通路(HCV)

第8章:市場估算與預測:依銷售管道分類,2021-2034年

- 主要趨勢

- OEM

- 售後市場

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 菲律賓

- 泰國

- 韓國

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球參與者

- Aptiv

- Continental

- Denso

- Infineon Technologies

- NXP Semiconductors

- Robert Bosch

- TE Connectivity

- ZF Friedrichshafen

- Murata

- 區域玩家

- Allegro MicroSystems

- KEYENCE

- Magna International

- Melexis

- NIRA Dynamics

- Sensata Technologies

- Siemens

- Valeo

- 新興參與者/顛覆者

- Augury Systems

- C3.ai

- Delphi Technologies

- Predii

- Presenso Analytics

- Revvo Technologies

- Samsara

- Tactile Mobility

- Uptake Technologies

The Global Automotive Predictive Maintenance Sensor Market was valued at USD 735.7 million in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 1.45 Billion by 2034.

Market growth is driven by the growing emphasis on vehicle reliability, operational safety, and cost efficiency. Predictive maintenance sensors play a vital role in assessing the condition of critical automotive components in real time, identifying potential issues before failures occur. This shift from reactive or scheduled maintenance to proactive strategies is helping reduce vehicle downtime and lower operational costs. As vehicles become increasingly complex, incorporating advanced mechanical and electronic systems, the need for continuous monitoring is expanding. Government safety regulations are also getting stricter, pushing manufacturers to integrate advanced diagnostic and monitoring systems. Furthermore, connected vehicles supported by IoT frameworks enable centralized data gathering and analysis, improving the precision and responsiveness of predictive maintenance. The broader adoption of data-driven maintenance practices across vehicle design, manufacturing, and operation cycles continues to shape the evolution of the automotive predictive maintenance sensor market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $735.7 million |

| Forecast Value | $1.45 billion |

| CAGR | 7.3% |

The temperature sensor category held a 35% share in 2024 and is expected to grow at a CAGR of 9.14% through 2034. Temperature sensors are among the most widely used technologies in predictive maintenance, as they help monitor essential systems such as engines, batteries, and HVAC units. Variations in temperature can lead to overheating or component degradation, making these sensors crucial for early fault detection. By delivering real-time temperature data, these sensors allow maintenance teams to schedule repairs proactively, minimizing unplanned downtime, reducing expenses, and enhancing the overall durability and reliability of vehicles.

The engine health monitoring segment held a 34% share in 2024 and is forecast to grow at a CAGR of 7.04% between 2025 and 2034. Engine monitoring remains one of the most critical applications within predictive maintenance due to the engine's high value and central role in vehicle performance. Predictive sensors in this segment track numerous parameters such as vibration, temperature, and fuel efficiency, helping detect irregularities before they escalate into costly damage. The ability to predict and prevent potential engine failures provides automakers and fleet operators with a significant competitive edge in maintaining optimal performance and longevity.

Asia Pacific Automotive Predictive Maintenance Sensor Market held a 44% share and generated USD 323.7 million in 2024. The region's dominance can be attributed to its strong automotive production base, accounting for over half of global vehicle output. Asia Pacific continues to be a hub for technological advancement, with rapid progress in electric, connected, and autonomous vehicle systems. Manufacturers in the region are heavily investing in smart vehicle platforms that rely on real-time sensor data to predict maintenance needs accurately. Structural growth, industrial modernization, and robust technological development are reinforcing Asia Pacific's leadership in the global market.

Prominent players in the Automotive Predictive Maintenance Sensor Market include Hella, Robert Bosch, STMicroelectronics, Valeo, Infineon Technologies, TE Connectivity, Continental, Sensata Technologies, and Murata. To strengthen their position in the automotive predictive maintenance sensor market, leading companies are adopting several strategic measures. Many are focusing on developing advanced sensor technologies with higher accuracy, durability, and integration capability to meet the demands of connected and electric vehicles. Investments in research and development remain a priority to support innovation in predictive analytics and data processing. Strategic collaborations and partnerships with automakers and technology providers are helping accelerate the deployment of smart maintenance systems. In addition, companies are expanding production capacities and optimizing their global supply chains to meet growing regional demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Sensor

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory compliance requirements (ISO 26262, UNECE regulations)

- 3.2.1.2 Fleet utilization optimization demands

- 3.2.1.3 Electric vehicle adoption acceleration

- 3.2.1.4 Advanced driver assistance system integration

- 3.2.1.5 Cost reduction pressures in maintenance operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Software-defined vehicle architecture adoption

- 3.2.3.2 5G and advanced connectivity deployment

- 3.2.3.3 Autonomous vehicle development

- 3.2.3.4 Circular economy and sustainability initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Technology landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By sensor

- 3.11 ROI and business case analysis

- 3.11.1 Total cost of ownership framework

- 3.11.2 Implementation cost structure

- 3.11.3 Quantified benefits assessment

- 3.12 Investment & funding trends analysis

- 3.13 Implementation roadmap framework

- 3.13.1 Phased deployment strategies

- 3.13.2 Integration complexity analysis

- 3.13.3 Change management requirements

- 3.13.4 Success factor identification

- 3.14 Performance benchmarking framework

- 3.14.1 KPI definition and measurement

- 3.14.2 Industry best practice analysis

- 3.14.3 Comparative performance metrics

- 3.14.4 Continuous improvement models

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New application launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Sensor, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Vibration sensor

- 5.3 Temperature sensor

- 5.4 Pressure sensor

- 5.5 Humidity sensor

- 5.6 Acoustic sensor

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Engine health monitoring

- 6.3 Transmission & gearbox monitoring

- 6.4 Battery & electrical system monitoring

- 6.5 Tire & wheel monitoring

- 6.6 Cooling system monitoring

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial sales channels

- 7.3.1 Light commercial sales channels (LCV)

- 7.3.2 Medium commercial sales channels (MCV)

- 7.3.3 Heavy commercial sales channels (HCV)

Chapter 8 Market Estimates & Forecast, By Sales channel, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 Philippines

- 9.4.7 Thailand

- 9.4.8 South Korea

- 9.4.9 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aptiv

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 Infineon Technologies

- 10.1.5 NXP Semiconductors

- 10.1.6 Robert Bosch

- 10.1.7 TE Connectivity

- 10.1.8 ZF Friedrichshafen

- 10.1.9 Murata

- 10.2 Regional Players

- 10.2.1 Allegro MicroSystems

- 10.2.2 KEYENCE

- 10.2.3 Magna International

- 10.2.4 Melexis

- 10.2.5 NIRA Dynamics

- 10.2.6 Sensata Technologies

- 10.2.7 Siemens

- 10.2.8 Valeo

- 10.3 Emerging Players / Disruptors

- 10.3.1 Augury Systems

- 10.3.2 C3.ai

- 10.3.3 Delphi Technologies

- 10.3.4 Predii

- 10.3.5 Presenso Analytics

- 10.3.6 Revvo Technologies

- 10.3.7 Samsara

- 10.3.8 Tactile Mobility

- 10.3.9 Uptake Technologies

2026年全球汽車故障預測市場報告

2026年全球汽車故障預測市場報告 汽車預測性維護市場:按組件、技術、車輛類型、部署模式和最終用戶分類-2026-2032年全球市場預測2026年全球汽車市場預測分析報告

汽車預測性維護市場:按組件、技術、車輛類型、部署模式和最終用戶分類-2026-2032年全球市場預測2026年全球汽車市場預測分析報告 汽車預測技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車預測技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球汽車預測分析市場:依技術、類型、車輛類型、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測

全球汽車預測分析市場:依技術、類型、車輛類型、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測 2026-2030年全球汽車預測性維護市場

2026-2030年全球汽車預測性維護市場 全球預測性汽車診斷解決方案市場預測(至2032年),按解決方案類型、車輛類型、部署模式、最終用戶和地區分類

全球預測性汽車診斷解決方案市場預測(至2032年),按解決方案類型、車輛類型、部署模式、最終用戶和地區分類 全球汽車預測分析市場規模、佔有率、行業分析報告(按組件、車輛類型、最終用戶、應用和地區分類)、展望和預測(2025-2032 年)2032 年汽車技術市場預測:按組件、部署、車輛類型、技術、應用、最終用戶和地區進行的全球分析

全球汽車預測分析市場規模、佔有率、行業分析報告(按組件、車輛類型、最終用戶、應用和地區分類)、展望和預測(2025-2032 年)2032 年汽車技術市場預測:按組件、部署、車輛類型、技術、應用、最終用戶和地區進行的全球分析 汽車預測分析市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車預測分析市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測