|

市場調查報告書

商品編碼

1940630

鋁:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Aluminum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

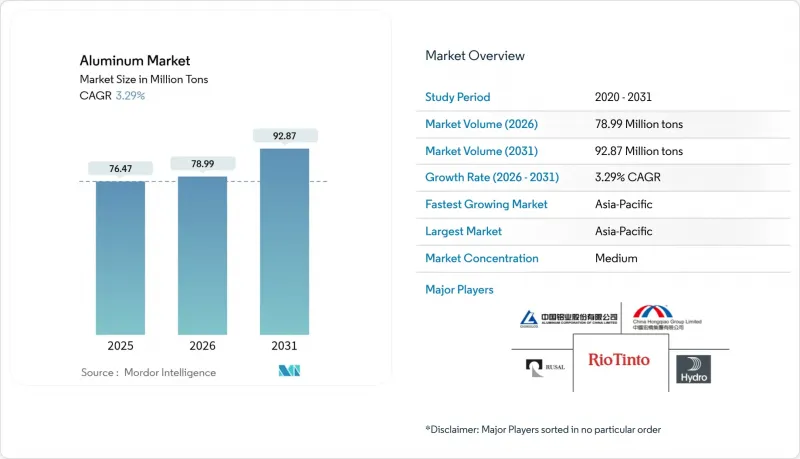

預計鋁市場將從 2025 年的 7,647 萬噸成長到 2026 年的 7,899 萬噸,到 2031 年將達到 9,287 萬噸,2026 年至 2031 年的複合年成長率為 3.29%。

鋁的強勁成長歸功於其作為全球第二大常用金屬的地位、無與倫比的強度重量比以及閉合迴路回收能力——該能力使其能夠回收利用已生產金屬的75%。快速電氣化、可再生能源的擴張以及永續包裝的強制性要求都在推動需求成長,而生產商則面臨脫碳目標、電價波動和貿易政策變化等挑戰。主要企業正將資金集中投入綠色冶煉和廢料回收,而下游客戶則簽訂長期供應合約以應對原物料價格波動。儘管亞太地區目前佔據鋁生產主導地位並保持著最快的成長速度,但區域產能上限、地緣政治風險以及碳邊境調節措施正在推動北美和沿岸地區地區的新投資。擁有低碳鋼坯、深度回收能力和多工藝柔軟性的綜合運營商預計將佔據更大的鋁市場佔有率。

全球鋁市場趨勢與洞察

電動車主導需求的快速成長

電池式電動車(BEV)的鋁用量將是內燃機車的三倍,預計到2024年,北美地區每輛車的鋁用量將達到885磅。由於每減重10%,續航里程約增加7%,汽車製造商目前正指定使用鋁材製造素車、電池托盤、碰撞結構和溫度控管系統。儘管電動車在成熟市場的滲透率在2028年後可能會趨於穩定,但不斷變化的車型組合將繼續增加單位車輛的金屬用量,從而在汽車總銷量波動的情況下,維持鋁市場的成長勢頭。

亞太基礎建設熱潮

亞太地區規劃中的大型企劃支撐了長期需求前景。自2000年以來,中國的鋁消費量年均成長約16%,遠超其他地區約1%的成長速度。智慧城市電網、高速鐵路和跨境輸電線路都依賴鋁的導電性和耐腐蝕性,這確保了該地區對鋁錠和加工產品的需求。儘管結構性經濟放緩會帶來週期性風險,但歷史上獎勵策略支出能夠緩解景氣衰退,並使鋁市場長期維持在高位。

能源價格波動

電力成本約佔冶煉現金成本的40%。 2024年歐洲現貨電價飆漲導致多家冶煉廠減產,年供應量減少超過100萬噸。由於爐體凍結可能造成永久性損壞,冶煉廠無法以低成本縮減產量,這加劇了其受日內價格波動的影響。雖然可再生能源能夠提供長期穩定性,但過渡性資金籌措和電網瓶頸正在擠壓短期利潤空間,並限制鋁產業在高價地區的擴張。

細分市場分析

到2025年,壓製產品將佔鋁市場佔有率的35.05%,這主要得益於建築型材、散熱器和汽車碰撞安全部件的需求成長。擁有大量低碳鋼坯的擠壓製造商已簽訂了長期供應契約,並獲得了溢價。預計到2031年,鑄件將以3.5%的最快成長,這主要得益於汽車汽車車體結構中巨型鑄造訂單的應用。設備製造商報告稱,他們的壓鑄生產線已排滿至2027年,凸顯了產能的快速擴張,而產能擴張將繼續推動動力傳動系統和底盤應用領域鋁市場規模的擴大。

扁鋼產品在飲料罐鋼板和汽車面板領域佔據著穩固的地位。先進的鋼廠正在實施閉合迴路廢鋼回收系統,以減少碳排放並確保原料供應穩定。鍛件供應起落架和軍用車輛,憑藉嚴格的品質標準,維持著一個利潤豐厚的細分市場。顏料和粉末為電子產品和積層製造(3D列印)提供支持,其成長取決於航太和醫療設備領域對3D列印機的採用。鋁材多樣化的加工能力展現了其適應性,也解釋了為什麼綜合製造商持續策略性地投資於擠壓機、軋延和壓鑄單元,以確保在更廣泛的鋁材市場中佔有一席之地。

此鋁市場報告按加工工藝類型(鑄造、擠壓、鍛造、扁平材、顏料和粉末)、終端用戶行業(汽車、航太與國防、建築與施工、電氣與電子、包裝及其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔全球鋁產量的69.58%,並在2031年之前以3.51%的複合年成長率成長。儘管由於北京4500萬噸的產能上限,新建冶煉廠的速度有所放緩,但下游加工業務仍在持續擴張,這提振了國內對鋁坯進口的需求,並推動了馬來西亞和印尼等再生鋁產業中心的投資。在印度,新的鑄造計劃正在擴建,以滿足智慧城市住宅和鐵路電氣化的需求,進一步增強了該地區對鋁市場的影響力。

預計2024年北美鋁產量將成長3.4%,但仍存在400萬噸的供不應求。聯邦政府的激勵措施推動了EGA在奧克拉荷馬州投資40億美元建設年產60萬噸的冶煉廠,以及Century Aluminum投資5億美元建設綠色陽極工廠——這是自1980年以來美國當地首個新增原生陽極生產產能。歐洲的鋁產量受到能源衝擊和冶煉廠關閉的影響,導致鋁坯溢價上漲,進口依賴度增加。然而,碳邊境調節機制(CBAM)的激勵措施和再生能源補貼正在吸引全行業的維修計劃,例如力拓在冰島部署的ELYSIS電解槽,這些項目預計在2020年代末實現無碳金屬生產。

海灣合作理事會國家正利用低成本電力出口高附加價值擠壓坯料,而非洲的礬土管道則為提煉提供原料,以實現鋁市場價值鏈的本地化。南美洲的鋁產量已趨於穩定,其中以富含氧化鋁的巴西為首,但仍受到物流挑戰和資金短缺的限制。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車主導了對輕型汽車需求的快速成長

- 亞太基礎建設熱潮

- 可再生能源驅動鋁需求

- 邁向永續包裝

- 氫能相容的綠色冶煉能力

- 市場限制

- 能源價格波動

- 碳邊境調節稅和ESG篩選

- 罐頭中石墨烯塗層鋼的威脅

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 進出口趨勢

- 定價分析

第5章 市場規模與成長預測

- 按處理類型

- 鑄件

- 擠出成型

- 鍛件

- 扁鋼產品

- 顏料和粉末

- 按最終用戶行業分類

- 車

- 航太/國防

- 建築/施工

- 電氣和電子

- 包裝

- 產業

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alcoa Corporation

- AluminIum BahraIn BSC(Alba)

- Aluminum Corp of China(Chalco)

- China Hongqiao Group Limited

- East Hope Group

- Emirates Global Aluminium PJSC

- Novelis Inc.

- Norsk Hydro ASA

- Rio Tinto

- RUSAL

- Xinfa Group

- Vedanta Aluminium

- Century Aluminum Company.

第7章 市場機會與未來展望

The Aluminum market is expected to grow from 76.47 million tons in 2025 to 78.99 million tons in 2026 and is forecast to reach 92.87 million tons by 2031 at 3.29% CAGR over 2026-2031.

Robust growth follows aluminum's position as the second most used metal, its unbeatable strength-to-weight ratio, and a closed-loop recyclability profile that keeps 75% of all metal ever produced in circulation. Rapid electrification, renewable-energy build-outs, and sustainable packaging mandates are converging to lift demand even as producers confront decarbonization targets, volatile power prices, and trade policy shifts. Top players are channeling capital toward green smelting and scrap recovery, while downstream customers lock in long-run supply to shield themselves from raw material shocks. Asia-Pacific dominates current volumes and retains the fastest trajectory, yet regional capacity ceilings, geopolitical risks, and carbon-border fees are driving fresh investments in North America and the Gulf. Integrated operators with low-carbon billet, recycling depth, and multi-process flexibility stand to capture a growing share of the Aluminum market.

Global Aluminum Market Trends and Insights

Surging EV-led Lightweighting Demand

Battery electric vehicles house triple the aluminum content of internal-combustion models, hitting 885 lb per car in North America during 2024. Every 10% mass cut extends driving range by roughly 7%, so automakers now specify aluminum for body-in-white, battery trays, crash structures, and thermal systems. EV penetration may plateau in mature markets after 2028, yet model-mix evolution keeps per-unit metal intensity rising, preserving a growth channel for the Aluminum market even as total auto sales fluctuate.

APAC Infrastructure Boom

Asia-Pacific's megaproject pipeline underpins long-cycle demand visibility. Chinese consumption expanded nearly 16% per year since 2000, dwarfing 1% rates elsewhere. Smart-city grids, high-speed rail, and cross-border power links rely on aluminum's conductivity and corrosion resistance, ensuring the region's pull on both primary ingot and fabricated products. Structural slowdowns pose cyclical risk, but stimulus outlays historically cushion downturns, keeping the Aluminum market on an elevated base in the long horizon.

Energy-Price Volatility

Electricity accounts for nearly 40% of smelting cash costs. European spot power spikes in 2024 forced multiple curtailments that erased over 1 million tons of annualized supply. Smelters cannot ramp down cheaply because frozen pots risk permanent damage, amplifying exposure to intraday price swings. Renewables add long-term stability, but transition financing and grid bottlenecks clamp near-term margins, trimming expansion appetite in high-tariff regions across the aluminium industry.

Other drivers and restraints analyzed in the detailed report include:

- Sustainable Packaging Shift

- Hydrogen-Ready Green Smelting Capacity

- Carbon-Border Tariffs and ESG Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusions represented 35.05% of Aluminum market share in 2025 on the back of architectural profiles, heat sinks, and vehicle crash-management parts. Extruders able to deliver low-carbon billet at scale are capturing long-term supply contracts with premium pricing clauses. Castings follow as the fastest riser at 3.5% through 2031, buoyed by giga-casting adoption in automotive body structures. Equipment builders report booked-out die-casting lines until 2027, highlighting a capacity sprint that keeps the Aluminum market size expanding within powertrain and chassis applications.

Flat-rolled products hold a solid slot across beverage can stock and auto panel sheet. Forward-looking mills integrate closed-loop scrap systems, shrinking carbon footprints and locking in feedstock surety. Forgings serve landing-gear and military vehicles, sustaining a high-margin niche underpinned by stringent quality standards. Pigments and powders cater to electronics and additive manufacturing; their trajectory depends on printer penetration rates in aerospace and medical device sectors. The multi-process spectrum underscores aluminum's adaptability and explains why integrated producers maintain strategic investments across extrusion presses, rolling mills, and die-casting cells to secure wallet share within the broader Aluminum market.

The Aluminum Report is Segmented by Processing Type (Castings, Extrusions, Forgings, Flat-Rolled Products, and Pigments and Powders), End-User Industry (Automotive, Aerospace and Defense, Building and Construction, Electrical and Electronics, Packaging, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific retained 69.58% of global volume in 2025 and is tracking a 3.51% CAGR through 2031. While Beijing's 45 million-ton ceiling slows greenfield smelters, downstream fabrication keeps expanding, propelling internal billet import needs and stimulating investment in secondary aluminum hubs across Malaysia and Indonesia. India scales new cast-house projects to meet smart-city housing and railway electrification, reinforcing the region's gravitational pull on the Aluminum market.

North America produced 3.4% more aluminum products in 2024, yet still logged a 4 million-ton supply deficit. Federal incentives now underpin EGA's USD 4 billion, 600,000-ton Oklahoma smelter and Century Aluminum's USD 500 million green-anode plant, marking the first primary capacity additions stateside since 1980. Europe's share is influenced by energy shocks, shuttered smelters, driving up billet premiums, and elevating import reliance. Yet CBAM incentives and subsidized renewable electricity are luring retrofit projects, such as Rio Tinto's ELYSIS cell roll-out in Iceland, that promise carbon-free metal by late-decade across the aluminium industry.

The GCC leverages low-cost power to export value-added extrusion logs, while Africa's bauxite pipelines flow toward refining ventures that seek to capture more of the Aluminum market value chain locally. South American volumes remain steady around alumina-rich Brazil but are constrained by logistics hurdles and capital scarcity.

- Alcoa Corporation

- AluminIum BahraIn B.S.C. (Alba)

- Aluminum Corp of China (Chalco)

- China Hongqiao Group Limited

- East Hope Group

- Emirates Global Aluminium PJSC

- Novelis Inc.

- Norsk Hydro ASA

- Rio Tinto

- RUSAL

- Xinfa Group

- Vedanta Aluminium

- Century Aluminum Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EV-Led Lightweighting Demand

- 4.2.2 APAC Infrastructure Boom

- 4.2.3 Renewable-Energy Aluminum Demand

- 4.2.4 Sustainable Packaging Shift

- 4.2.5 Hydrogen-Ready Green Smelting Capacity

- 4.3 Market Restraints

- 4.3.1 Energy-Price Volatility

- 4.3.2 Carbon-Border Tariffs and ESG Scrutiny

- 4.3.3 Graphene-Coated Steel Threat in Cans

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Import-Export Trends

- 4.7 Pricing Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Processing Type

- 5.1.1 Castings

- 5.1.2 Extrusions

- 5.1.3 Forgings

- 5.1.4 Flat-Rolled Products

- 5.1.5 Pigments and Powders

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Packaging

- 5.2.6 Industrial

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alcoa Corporation

- 6.4.2 AluminIum BahraIn B.S.C. (Alba)

- 6.4.3 Aluminum Corp of China (Chalco)

- 6.4.4 China Hongqiao Group Limited

- 6.4.5 East Hope Group

- 6.4.6 Emirates Global Aluminium PJSC

- 6.4.7 Novelis Inc.

- 6.4.8 Norsk Hydro ASA

- 6.4.9 Rio Tinto

- 6.4.10 RUSAL

- 6.4.11 Xinfa Group

- 6.4.12 Vedanta Aluminium

- 6.4.13 Century Aluminum Company.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

磷酸鋁市場:依形態、等級、應用和分銷管道分類-2026-2032年全球市場預測乙醯丙酮鋁市場:依等級、形態、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測二氧化碳鋁瓶市場:依容量、瓶型、壓力、最終用途及通路分類,全球預測(2026-2032年)

磷酸鋁市場:依形態、等級、應用和分銷管道分類-2026-2032年全球市場預測乙醯丙酮鋁市場:依等級、形態、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測二氧化碳鋁瓶市場:依容量、瓶型、壓力、最終用途及通路分類,全球預測(2026-2032年) 多金屬鋁夾芯板市場報告:按金屬、發泡材、應用和地區分類(2026-2034 年)

多金屬鋁夾芯板市場報告:按金屬、發泡材、應用和地區分類(2026-2034 年) 鋁市場分析及預測(至2035年):類型、產品類型、應用、形式、材質類型、技術、最終用戶、組件、功能

鋁市場分析及預測(至2035年):類型、產品類型、應用、形式、材質類型、技術、最終用戶、組件、功能 越南鋁業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

越南鋁業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球氧化鋁和鋁製品市場報告2026年全球鋁市場報告2026年全球鋁擠型市場報告2026年全球鋁渣市場報告

2026年全球氧化鋁和鋁製品市場報告2026年全球鋁市場報告2026年全球鋁擠型市場報告2026年全球鋁渣市場報告