|

市場調查報告書

商品編碼

1939694

越南鋁業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Aluminum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

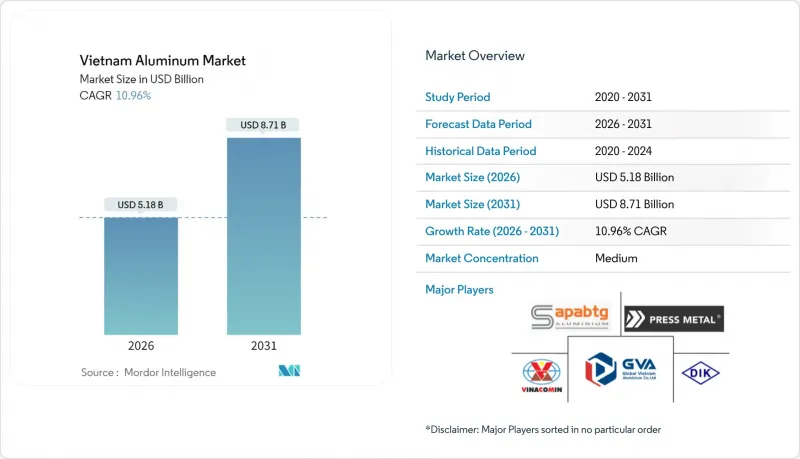

預計越南鋁市場規模將從 2025 年的 46.7 億美元成長到 2026 年的 51.8 億美元,到 2031 年將達到 87.1 億美元,2026 年至 2031 年的複合年成長率為 10.96%。

這一上升趨勢,加上豐富的礬土蘊藏量、新增氧化鋁產能以及交通運輸和建築行業的需求,使越南鋁市場成為亞洲成長最快的價值鏈之一。電動車產量的成長、綠建築法規的推行以及包裝循環利用目標的實現,正在推動結構性需求的成長,而上游58億噸礬土蘊藏量的穩定供應則為長期供應提供了保障。政府第866號決議批准到2030年建造8座加工廠和19個探勘計劃,進一步促進了市場成長,儘管目前的運轉率平均仍高達70%,顯示仍有發展空間。

越南鋁市場趨勢及展望

汽車產業輕量化發展的趨勢

越南擁有858家通過IATF 16949認證的供應商,這推動了汽車鋁材的需求成長,並將越南納入區域汽車平臺。在電動車生產中,電池機殼和溫度控管系統所需的鋁材用量比傳統車型高出約30%,越南的目標是到2030年實現都市區車輛50%的電動化。儘管在地採購政策鼓勵零件外包,但商用車輛車隊正在採用鋁製零件,以最大限度地提高負載容量並滿足排放標準。世界銀行估計,到2050年,向電動車的轉型將創造650萬個製造業就業崗位,這將支撐鑄造、擠壓和扁鋼供應鏈的金屬需求。隨著整車製造商擴大產能,越南鋁市場將受益於鋁坯和鋁錠需求的成長,從而吸引新的二次冶煉廠進入市場。

公共和綠色建築建設快速成長

2024年,公共支出300億美元,這將在短期內刺激對帷幕牆、屋頂材料和結構型材的需求。 2024年第一季,獲得綠色認證的建築數量達到430座,其中EDGE和LEED認證佔比高達75.69%。鋁材因其可回收性和良好的熱效率而被廣泛應用。到2030年,政府將累計1,350億美元用於電力發展第八期規劃,將推動高壓結構和太陽能板框架對鋁材的需求。胡志明市耗資115億美元的高速公路規劃和12億美元的交通基礎設施改善項目也將促進型材消費量的成長。

電力價格上漲和碳價格風險

穩定且低成本的電力對鋁提煉至關重要,但越南工業平均電價預計將在2024年上漲,這將擠壓利潤空間。一些工廠的運轉率被限制在30%至40%。歐盟的碳邊境調節機制(CBAM)可能影響價值3.0766億美元的鋁出口,導致出貨量減少4%,相當於每年損失1,200萬美元的收入。第八個電力發展計畫要求實施市場定價,除非可再生能源得到保障,否則將對電解計劃帶來壓力。出口商將不得不降低碳排放強度或支付CBAM費用,這將削弱越南在鋁市場的成本優勢。

細分市場分析

到2025年,擠壓件將佔越南鋁材市場的39.42%,主要得益於對窗框、帷幕牆和汽車型材的持續需求。預計到2027年,基礎設施投資將達到958億美元,這將使擠壓廠保持較高的運轉率。同時,嚴格的LEED和EDGE標準也認可採用陽極氧化和隔熱系統的產品。為因應美國的反傾銷令,出口合作夥伴正在改善製程流程,從而鞏固其品質領先地位。預計到2031年,鑄件市場將以13.62%的複合年成長率成長,因為汽車製造商正在尋求在本地生產用於電動車平台的輕量化零件。

IATF 16949認證仍是OEM供貨的先決條件,也是越南作為東協第二大認證中心地位的基礎。像美華精密工業這樣的製造商,60%的銷售額來自國內,其餘部分出口到日本、美國和澳大利亞,這反映了越南在中游加工領域日益增強的競爭力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 汽車產業輕量化發展的趨勢

- 公共和綠色建築建設快速成長

- 包裝需求復甦(食品、飲料和製藥業)

- 國內礬土及氧化鋁計劃擴張

- 電動車和電池外殼的快速本地化

- 市場限制

- 面臨高電價和碳定價風險

- 低成本的鋼材、塑膠和複合材料替代品

- 對初級金屬和鋼坯的進口依賴

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 透過加工方法

- 鑄件

- 擠出成型

- 鍛件

- 扁鋼產品

- 顏料和粉末

- 按最終用戶行業分類

- 車

- 航太與國防

- 建築/施工

- 電氣和電子行業

- 包裝

- 工業的

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alcoa Corporation

- Daiki Aluminium Industry Co. Ltd

- Emirates Global Aluminium PJSC

- GARMCO

- Global Vietnam Aluminum Co., Ltd(GVA)

- Kobe Steel Ltd

- Norsk Hydro ASA

- Press Metal

- RusAL

- Sapa Ben Thanh Aluminium Profiles Co., Ltd.(Sapa BTG)

- Vietnam Coal and Mineral Industries Group

第7章 市場機會與未來展望

The Vietnam Aluminum Market is expected to grow from USD 4.67 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 8.71 billion by 2031 at 10.96% CAGR over 2026-2031.

This uptrend positions the Vietnam aluminum market among the fastest-growing value chains in Asia as abundant bauxite reserves, new alumina capacity, and demand from mobility and construction converge. Rising EV production, green-building mandates, and packaging circularity targets foster structural demand, while upstream security from 5.8 billion tonnes of bauxite supports long-term supply. Government Decision 866 authorizing eight processing facilities plus 19 exploration projects through 2030 further underpins growth, although capacity utilization still averages 70%, highlighting operational headroom.

Vietnam Aluminum Market Trends and Insights

Auto-sector Lightweighting Push

Automotive aluminum demand is reinforced by 858 IATF 16949-certified suppliers that integrate Vietnam into regional vehicle platforms. EV production uses nearly 30% more aluminum per unit than conventional models for battery enclosures and thermal systems, and Vietnam targets 50% electric urban vehicles by 2030. Local content policies fuel component outsourcing, while commercial fleets adopt aluminum parts to maximize payload and comply with emission norms. The World Bank estimates the EV transition could generate 6.5 million manufacturing jobs by 2050, a scenario that sustains metal demand across casting, extrusion, and flat-rolled supply chains. As OEMs expand capacity, the Vietnam aluminum market benefits from rising billet and ingot off-take, incentivizing new secondary smelters.

Booming Public and Green-Building Construction

Public spending of USD 30 billion in 2024 on transport and power facilities injected near-term demand for curtain walls, roofing, and structural extrusions. Green-certified buildings rose to 430 in Q1 2024, with EDGE and LEED accounting for 75.69% of certifications, favoring aluminum for its recyclability and thermal efficiency. Power Development Plan VIII earmarks USD 135 billion through 2030, driving aluminum demand for high-voltage structures and solar frames. Ho Chi Minh City's USD 11.5 billion highway program and USD 1.2 billion of transport upgrades boost extruded profile consumption.

High Electricity Tariffs and Carbon-Pricing Exposure

Aluminum smelting requires constant low-cost power, yet Vietnam's average industrial tariff rose in 2024, compressing margins and limiting capacity use to 30-40% in some plants. The EU's Carbon Border Adjustment Mechanism affects USD 307.66 million of aluminum exports and could trim shipments by 4%, translating into USD 12 million revenue loss per year. Power Development Plan VIII calls for market-based pricing, pressuring electrolysis projects unless they secure renewables. Exporters must cut carbon intensity or pay CBAM fees that erode the Vietnam aluminum market's cost advantage.

Other drivers and restraints analyzed in the detailed report include:

- Rebound in Packaging Demand (Food-Drink and Pharmaceuticals)

- Expansion of Domestic Bauxite and Alumina Projects

- Import Dependence for Primary Metal and Billets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusions commanded 39.42% of the Vietnam aluminum market in 2025 on the back of sustained demand for window frames, curtain walls, and vehicle profiles. Rising infrastructure outlays valued at USD 95.8 billion through 2027 keep extrusion mills running at high throughput, while strict LEED and EDGE criteria reward anodized and thermally broken systems. Compliance with U.S. antidumping orders incentivizes process upgrades among cooperative exporters, reinforcing quality leadership. Castings are projected to grow at a 13.62% CAGR to 2031 as automakers localize lightweight components for EV platforms.

Certification under IATF 16949 remains a prerequisite for OEM supply and underpins Vietnam's ranking as ASEAN's second-largest certified base. Producers like Mien Hua Precision generate 60% of sales domestically and export the remainder to Japan, the U.S., and Australia, reflecting the country's expanding mid-stream competitiveness.

The Vietnam Aluminum Market Report is Segmented by Processing Type (Castings, Extrusions, Forgings, Flat Rolled Products, and Pigments and Powders) and End-User Industry (Automotive, Aerospace and Defense, Building and Construction, Electrical and Electronics, Packaging, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alcoa Corporation

- Daiki Aluminium Industry Co. Ltd

- Emirates Global Aluminium PJSC

- GARMCO

- Global Vietnam Aluminum Co., Ltd (GVA)

- Kobe Steel Ltd

- Norsk Hydro ASA

- Press Metal

- RusAL

- Sapa Ben Thanh Aluminium Profiles Co., Ltd. (Sapa BTG)

- Vietnam Coal and Mineral Industries Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Auto-sector lightweighting push

- 4.2.2 Booming public and green-building construction

- 4.2.3 Rebound in packaging demand (food-drink and pharmaceuticals)

- 4.2.4 Expansion of domestic bauxite and alumina projects

- 4.2.5 Rapid EV/battery-housing localisation

- 4.3 Market Restraints

- 4.3.1 High electricity tariffs and carbon-pricing exposure

- 4.3.2 Cheap steel/plastics and composite substitutes

- 4.3.3 Import dependence for primary metal and billets

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Processing Type

- 5.1.1 Castings

- 5.1.2 Extrusions

- 5.1.3 Forgings

- 5.1.4 Flat Rolled Products

- 5.1.5 Pigments and Powders

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Packaging

- 5.2.6 Industrial

- 5.2.7 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alcoa Corporation

- 6.4.2 Daiki Aluminium Industry Co. Ltd

- 6.4.3 Emirates Global Aluminium PJSC

- 6.4.4 GARMCO

- 6.4.5 Global Vietnam Aluminum Co., Ltd (GVA)

- 6.4.6 Kobe Steel Ltd

- 6.4.7 Norsk Hydro ASA

- 6.4.8 Press Metal

- 6.4.9 RusAL

- 6.4.10 Sapa Ben Thanh Aluminium Profiles Co., Ltd. (Sapa BTG)

- 6.4.11 Vietnam Coal and Mineral Industries Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Aluminium Recycling and Circular-Economy Plays

- 7.3 High-end EV and Battery-pack Components

全球最小框架鋁合金窗系統市場-產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭對手分類,2021-2031年

全球最小框架鋁合金窗系統市場-產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭對手分類,2021-2031年 鋁市場規模、佔有率和成長分析:按產品類型、合金類型、最終用途產業、加工方法、鋁品種和地區分類-2026-2033年產業預測

鋁市場規模、佔有率和成長分析:按產品類型、合金類型、最終用途產業、加工方法、鋁品種和地區分類-2026-2033年產業預測 2026-2030年全球鋁型材市場

2026-2030年全球鋁型材市場 2026-2030年全球鋁市場

2026-2030年全球鋁市場 2026-2030年全球鋁粉、鋁膏及鋁片市場

2026-2030年全球鋁粉、鋁膏及鋁片市場 鋁市場機會、成長要素、產業趨勢分析及2026-2035年預測

鋁市場機會、成長要素、產業趨勢分析及2026-2035年預測 鋁系統市場:依製造流程、形狀、產品類型和應用分類-2026-2032年全球市場預測鋁市場:按類型、形狀、原料、等級、加工方法和應用分類-2026-2032年全球市場預測鋁導體市場:依導體類型、絕緣方式、額定電壓和應用分類-2026-2032年全球市場預測

鋁系統市場:依製造流程、形狀、產品類型和應用分類-2026-2032年全球市場預測鋁市場:按類型、形狀、原料、等級、加工方法和應用分類-2026-2032年全球市場預測鋁導體市場:依導體類型、絕緣方式、額定電壓和應用分類-2026-2032年全球市場預測 鋁市場:依產品、加工、應用及地區分類

鋁市場:依產品、加工、應用及地區分類